Street Calls of the Week

Introduction & Market Context

SECO SpA (BIT:IOT), a global player in edge computing and IoT solutions, presented its fiscal year 2024 results on April 28, 2025, highlighting resilience in a challenging market environment. The Italian technology company managed to exceed its guidance despite industry-wide destocking trends that affected revenues throughout the year. With shares trading at €1.88, near the lower end of its 52-week range (€1.46-€3.67), investors are closely watching for signs of the recovery SECO’s management team projects for 2025.

Executive Summary

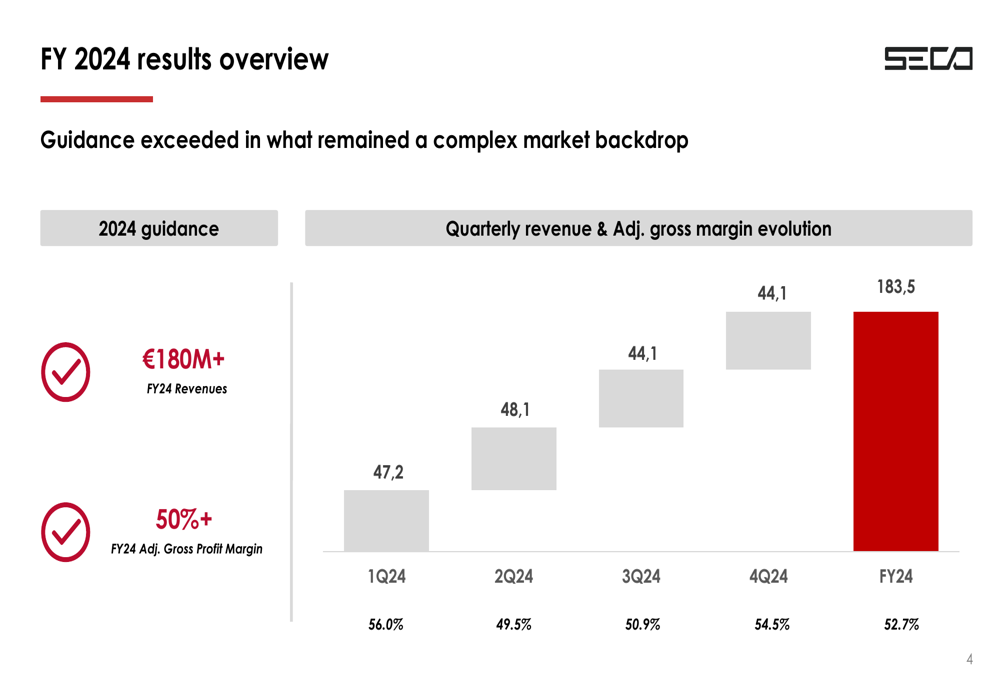

SECO reported FY 2024 revenue of €183.5 million, surpassing its guidance of €180+ million, though representing a 12.5% decline from the previous year. The company maintained strong gross profit margins at 52.7%, exceeding its 50%+ target and demonstrating the resilience of its business model despite market headwinds.

As shown in the following quarterly performance chart, the company saw stabilization in revenues during the second half of 2024, with improving gross margins in Q4:

"We’ve exceeded our guidance despite a complex market backdrop," said Massimo Mauri, Chief Executive Officer of SECO. "Our focus on high-margin custom solutions and diversified client base has allowed us to maintain industry-leading gross margins while navigating the challenging environment."

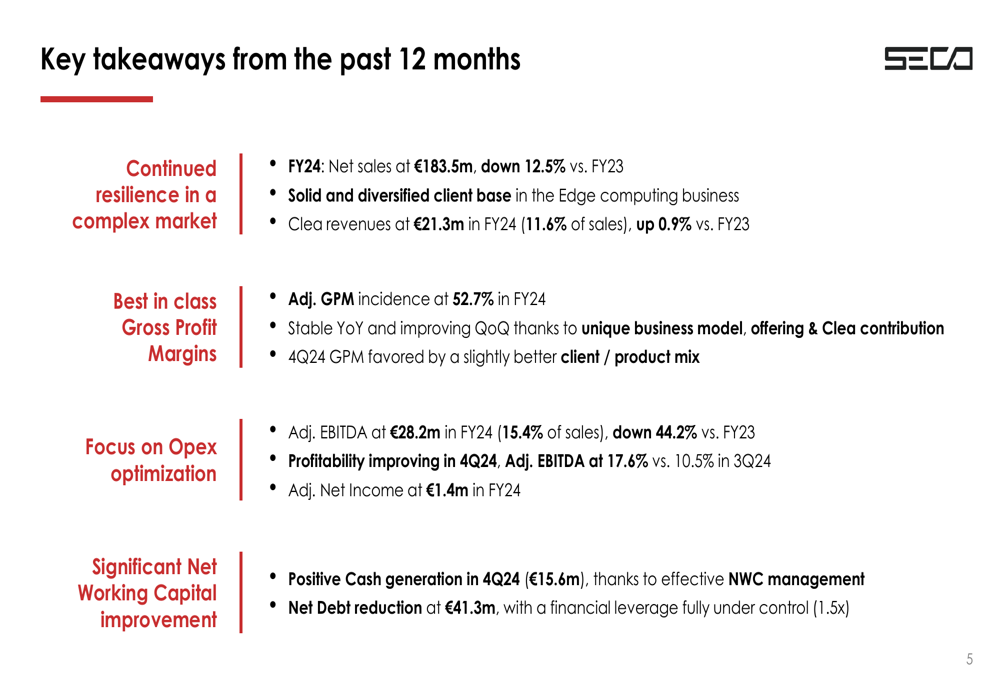

The company’s key takeaways from FY 2024 highlight both the challenges faced and the progress made in strategic areas:

Detailed Financial Analysis

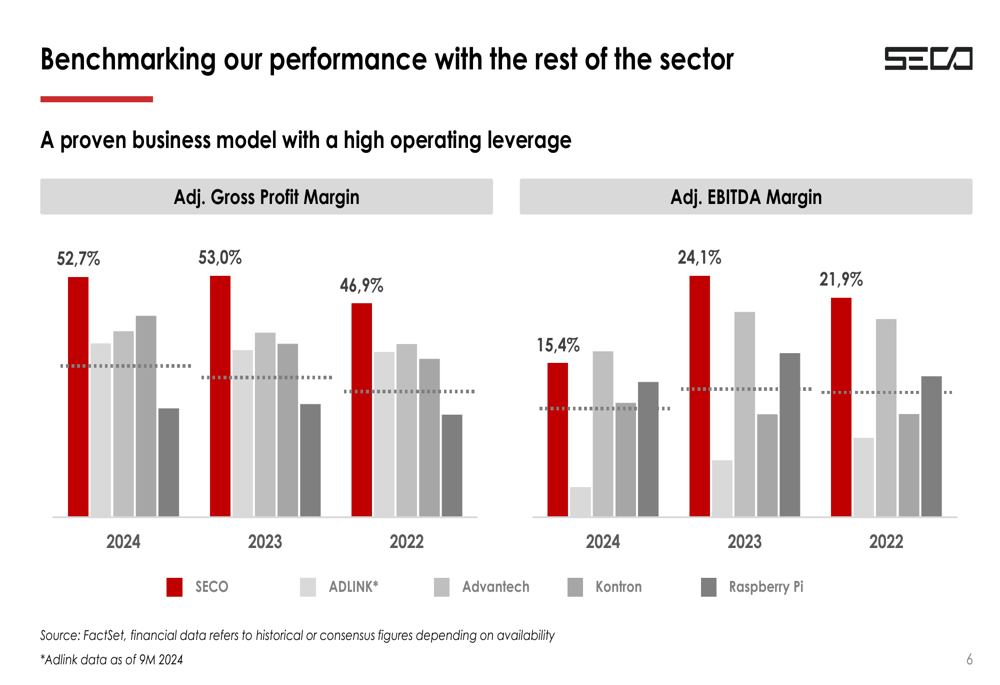

SECO’s financial performance in FY 2024 reflects the impact of market headwinds, with net sales declining from €209.8 million in FY 2023 to €183.5 million. Despite this revenue decrease, the company maintained strong gross margins at 52.7%, nearly unchanged from 53.0% in the previous year. However, adjusted EBITDA fell to €28.2 million (15.4% of sales) from €50.6 million (24.1%) in FY 2023, and adjusted net income dropped significantly to €1.4 million from €22.9 million.

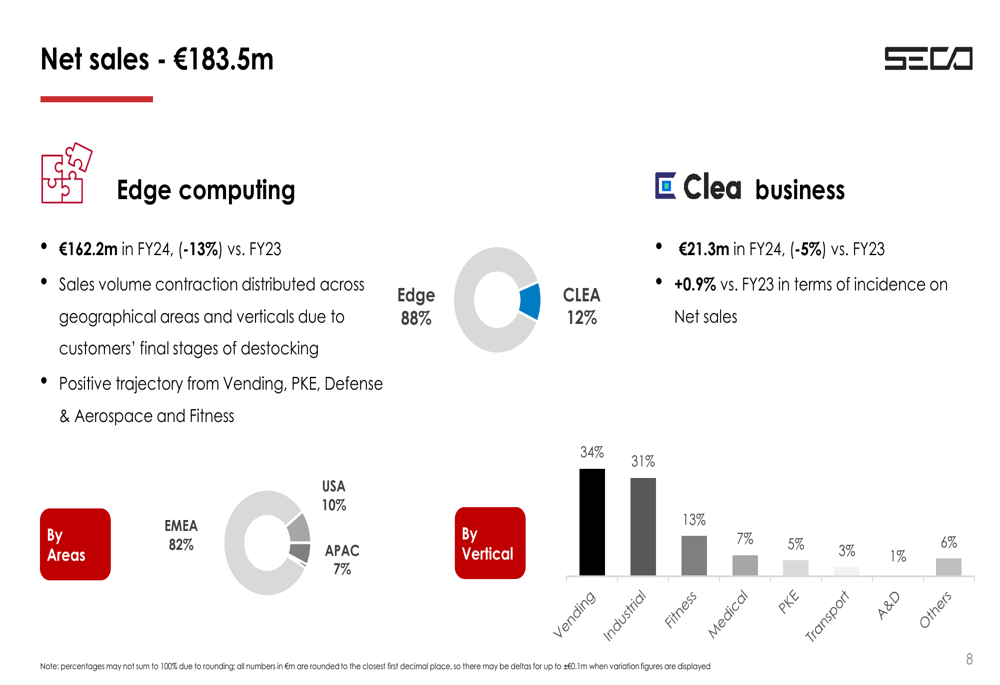

The company’s sales breakdown reveals a diversified business across multiple sectors, with vending (34%) and industrial applications (31%) representing the largest segments. Geographically, SECO remains heavily concentrated in EMEA (82%), with growing presence in the USA (10%) and APAC (7%).

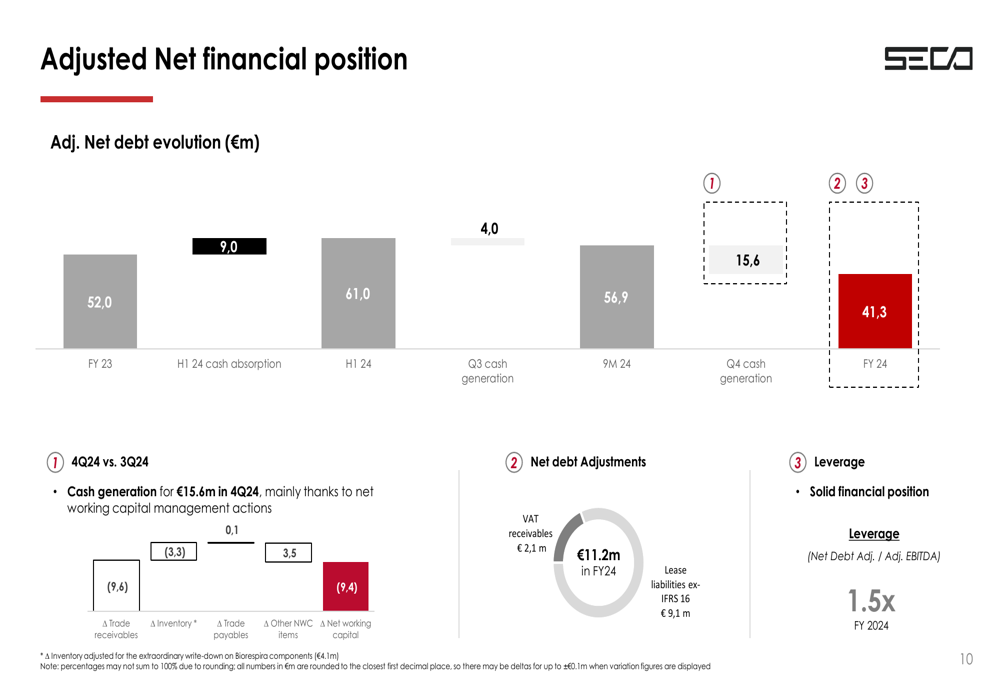

A key positive development in Q4 was the significant improvement in cash generation, with €15.6 million generated primarily through effective working capital management. This helped reduce net debt to €41.3 million, maintaining a manageable financial leverage of 1.5x.

When benchmarked against competitors, SECO’s gross profit margins remain competitive, though its EBITDA margins lag behind some peers:

Strategic Initiatives & Partnerships

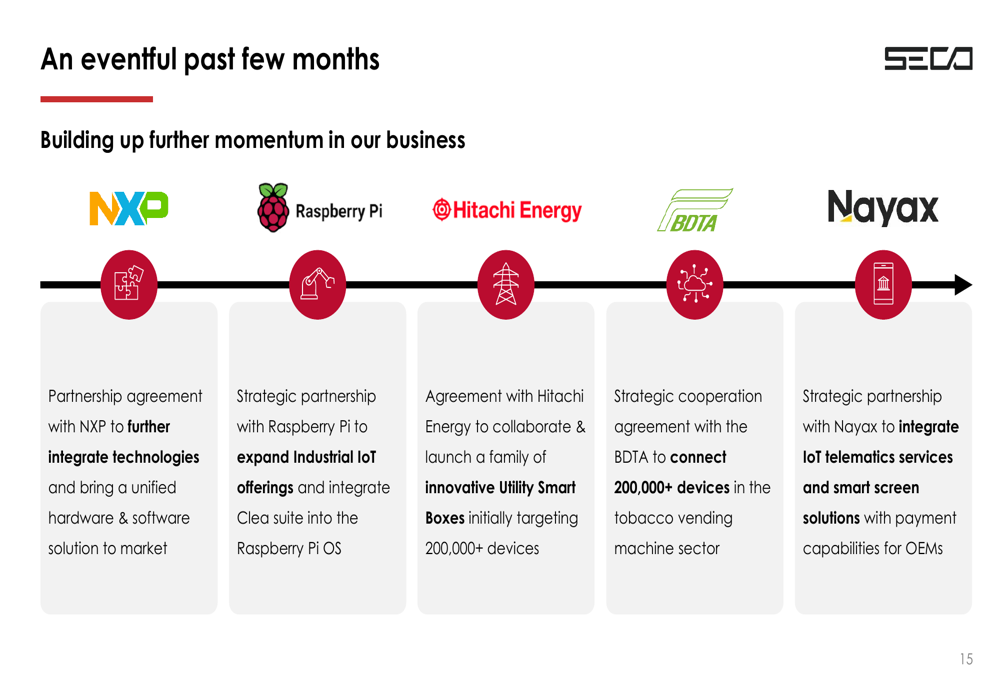

SECO has been actively building strategic partnerships to strengthen its market position and drive future growth. These collaborations span across major technology providers and industry leaders:

The partnership with Raspberry Pi is particularly noteworthy as it expands SECO’s Industrial IoT offerings and integrates its Clea suite into the Raspberry Pi OS. Similarly, the agreement with Hitachi (OTC:HTHIY) Energy targets 200,000+ devices in the utility sector, while the BDTA partnership aims to connect 200,000+ tobacco vending machines.

These partnerships are already showing traction with the Clea platform, SECO’s IoT and AI solution:

"Our Clea platform is gaining significant traction with clients and partners," explained Lorenzo Mazzini, Chief Financial Officer. "The long-term agreements with Hitachi Energy and BDTA are expected to generate substantial recurring revenue streams, with €1 million and €8 million in yearly recurring revenue respectively."

Product Pipeline & Growth Drivers

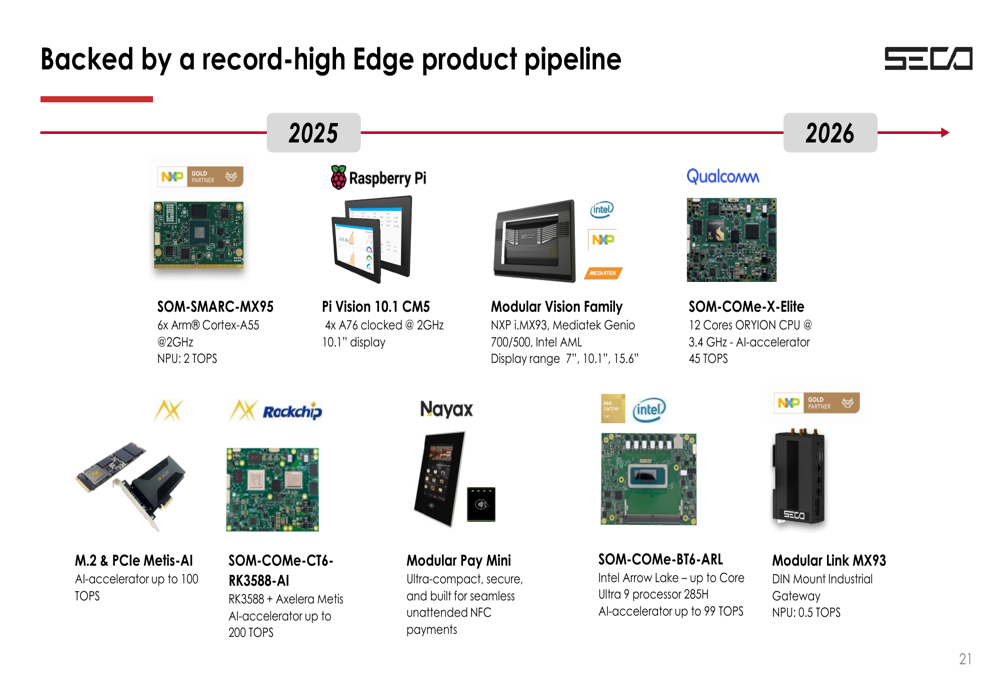

SECO is positioning itself to capitalize on the growing demand for AI-powered edge computing solutions. The company showcased several new products at Embedded World 2025, including collaborations with Qualcomm (NASDAQ:QCOM), AXELERA, and Raspberry Pi.

The company’s product pipeline for 2025-2026 is robust, featuring a range of edge computing solutions designed to address diverse market needs:

SECO has identified several key growth drivers for 2025, including a record-high new product pipeline, increasing traction for its Clea platform, and an improving macroeconomic backdrop:

Forward-Looking Statements

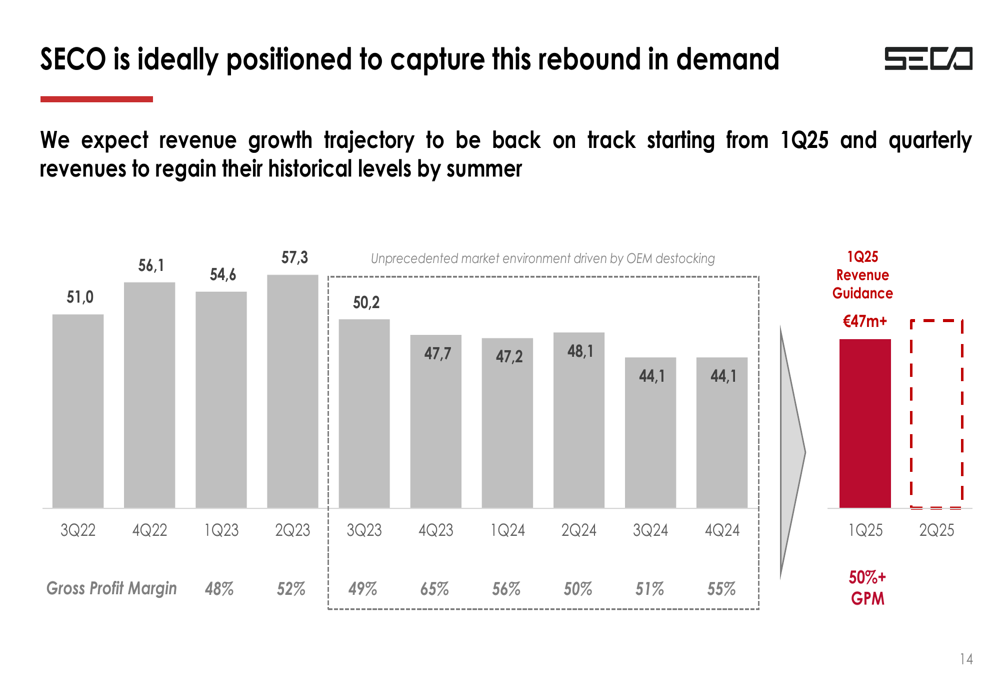

SECO’s management expressed confidence in a return to growth in 2025, pointing to encouraging signs in backlog trends and book-to-bill ratios. The company provided guidance for Q1 2025, projecting revenue of €47+ million with gross profit margins exceeding 50%.

As illustrated in the following chart, SECO expects to see a rebound in demand starting from Q1 2025, with quarterly revenues projected to return to historical levels by summer:

"We’re seeing clear signals that the inflection point has been reached," noted Mauri. "OEMs have mostly completed their inventory adjustments, as evidenced by our positive book-to-bill ratio of 1.0x and encouraging incoming backlog trend."

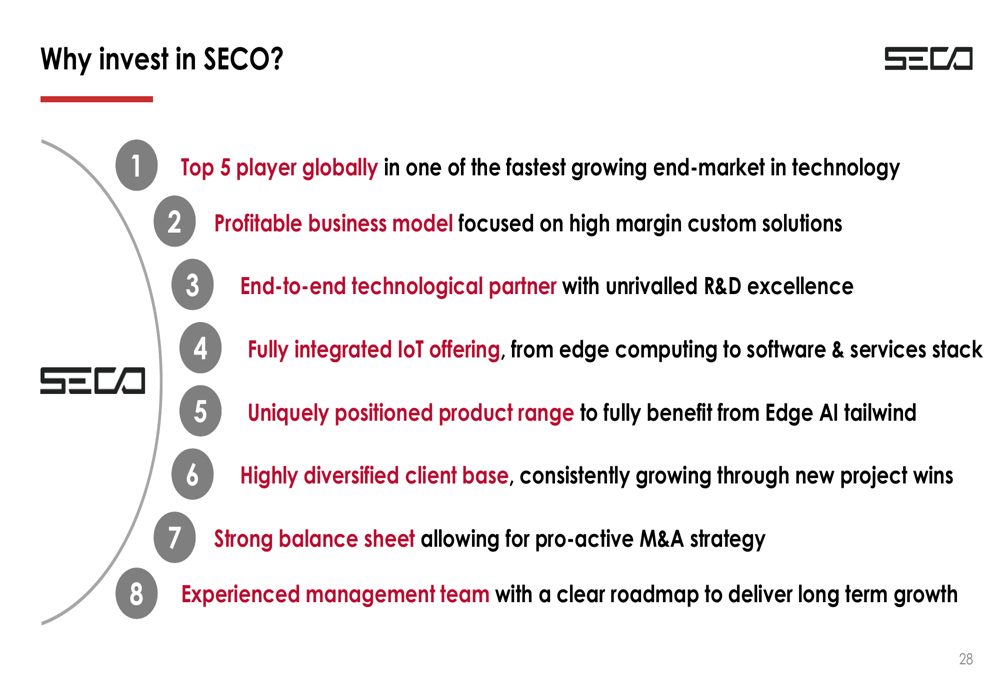

The company’s investment thesis emphasizes its position as a top 5 global player in one of technology’s fastest-growing end-markets, with a profitable business model focused on high-margin custom solutions:

With its strategic focus on AI-powered edge computing, diversified client base, and strong balance sheet, SECO appears positioned to capitalize on the anticipated market recovery in 2025, though investors will be watching closely to see if the projected rebound materializes as expected.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.