Treasury Secretary Bessent announces tariff relief on coffee, fruits

Introduction & Market Context

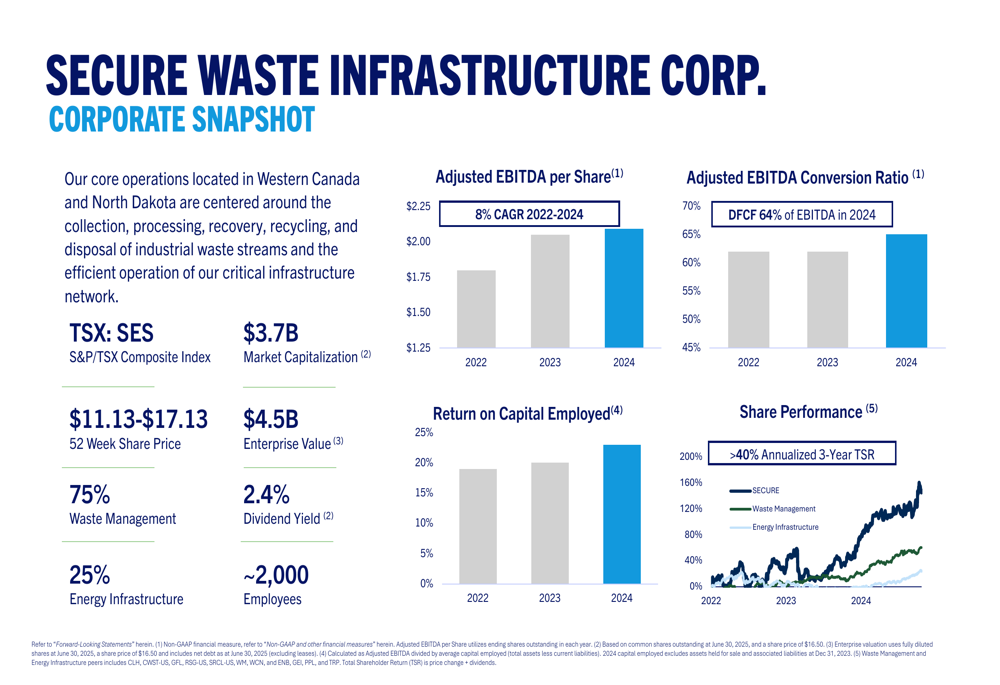

Secure Energy Services Inc . (TSX:SES) released its July 2025 investor presentation, highlighting the company’s transformation into a leading waste management and energy infrastructure provider with a significant valuation gap compared to industry peers. Operating primarily in Western Canada and North Dakota, the company has evolved from an energy services provider to a diversified waste management and infrastructure business with highly recurring cash flows.

The presentation comes after a record-breaking 2023 performance, which included $1.15 billion in asset sales to Waste Connections (NYSE:WCN) and a leadership transition from retiring CEO Rene Amirault to Allen Gransch. Currently trading at $16.72, the stock has shown strong momentum, up 0.54% in the most recent session and trading near its 52-week high of $17.13.

Executive Summary

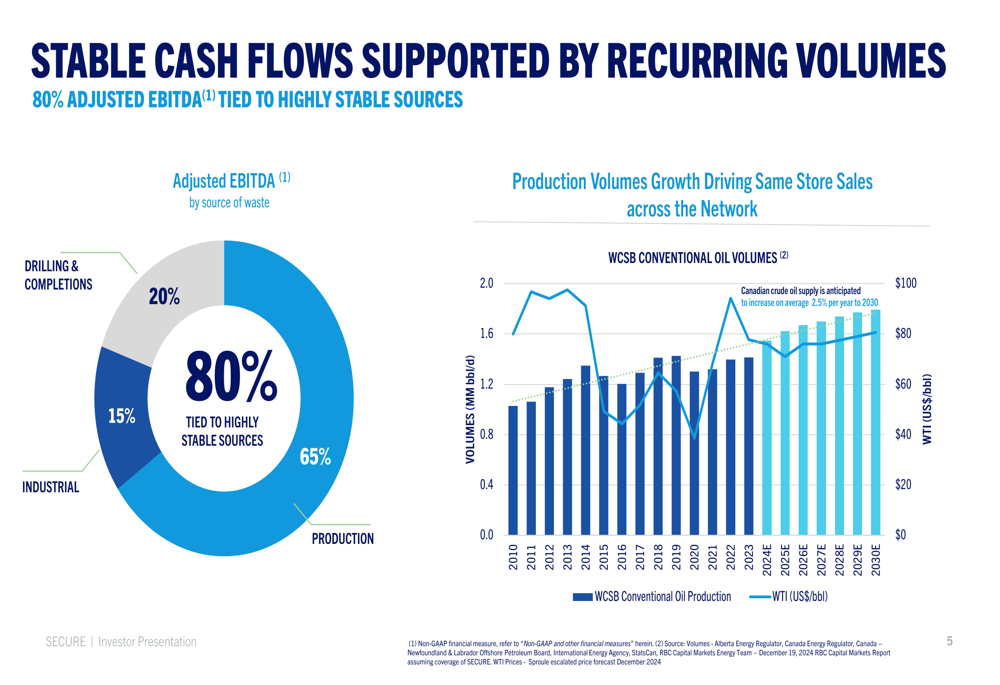

Secure Energy Services has successfully transformed its business model to focus on more stable, infrastructure-based revenue streams. The company now derives approximately 75% of its adjusted EBITDA from waste management operations and 25% from energy infrastructure, with 80% of volumes tied to production-related and recurring waste streams.

As shown in the following corporate snapshot, the company has demonstrated consistent financial improvement across key metrics:

With a market capitalization of $3.7 billion and enterprise value of $4.5 billion, Secure has delivered an 8% CAGR in adjusted EBITDA per share from 2022-2024, while improving its EBITDA conversion ratio from 65% to 70% and increasing return on capital employed from 17% to 21%. The company’s share performance has exceeded 40% annualized three-year total shareholder return, significantly outperforming its peer group.

Financial Performance Highlights

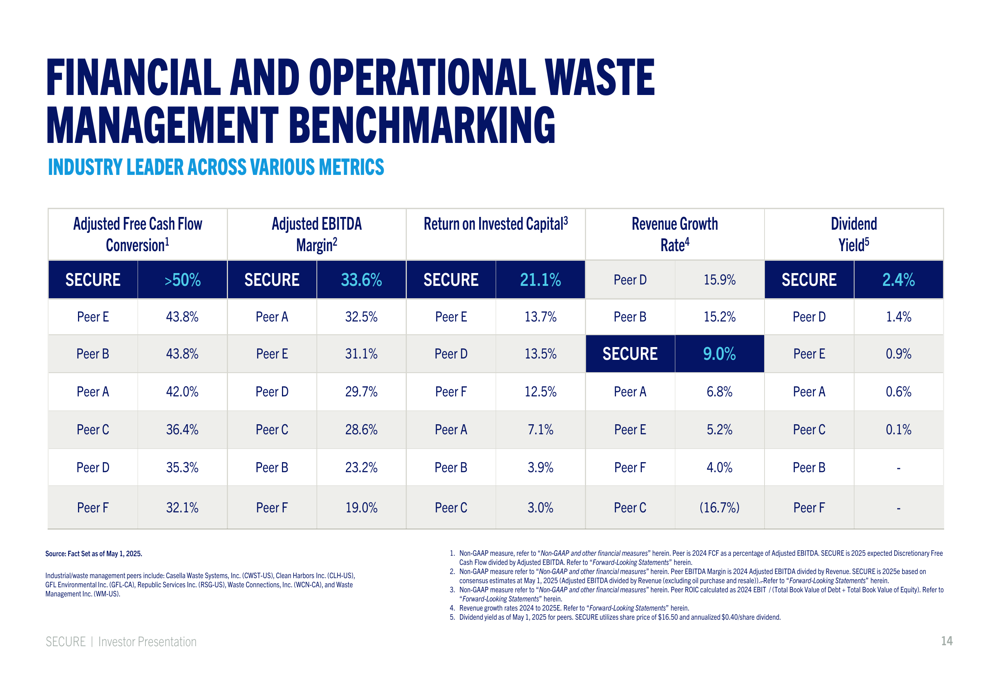

Secure Energy Services has demonstrated strong financial performance, projecting adjusted EBITDA of $510-540 million for 2025. The company maintains industry-leading metrics compared to waste management peers, including superior free cash flow conversion, EBITDA margins, and return on invested capital.

The following benchmarking data illustrates Secure’s financial outperformance relative to industry peers:

Notably, Secure leads its peer group with:

- Adjusted free cash flow conversion exceeding 50% (vs. peer average of ~39%)

- Adjusted EBITDA margin of 33.6% (vs. peer average of ~27%)

- Return on invested capital of 21.1% (vs. peer average of ~9%)

The company has maintained a strong balance sheet with total debt to EBITDA of 2.1x as of June 30, 2025, providing significant financial flexibility to execute on strategic priorities. This represents an improvement from previous years and aligns with management’s disciplined approach to capital allocation.

Strategic Positioning and Competitive Advantages

Secure has built a network of approximately 80 facilities across Western Canada and North Dakota, creating significant barriers to entry through complex regulatory requirements, high capital investment needs, and specialized operating expertise. The company processes and disposes of 136 mbbl/d of produced water and waste, recovers 1.1 million barrels of oil from waste, disposes of 3.5 million tonnes of solid waste, and handles 131 mbbl/d through its oil pipeline and terminalling operations.

The company’s business is supported by stable and recurring cash flows, with 80% of volumes tied to production-related activities rather than more cyclical drilling and completions work. This is illustrated in the following breakdown of revenue sources:

Secure’s competitive positioning is further strengthened by its extensive geographical footprint, as shown in this map of its operations:

The company’s critical infrastructure network would be difficult to replicate, providing a sustainable competitive advantage and supporting consistent growth, margin expansion, and cash flow generation.

Growth Initiatives and Capital Allocation

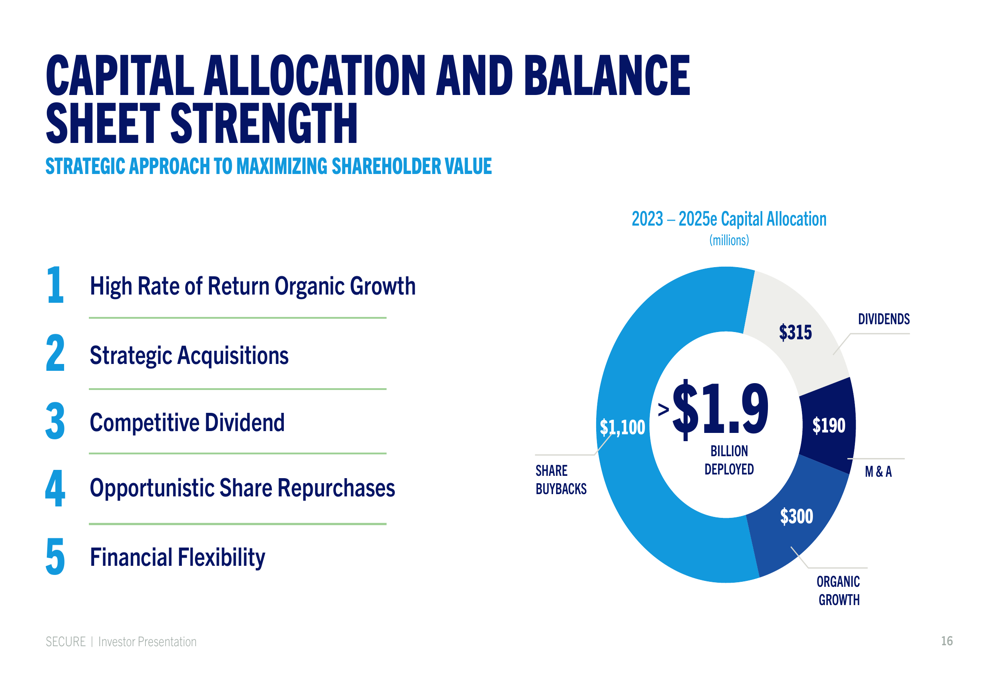

Secure has outlined a balanced capital allocation strategy focused on maximizing shareholder value. Between 2023-2025, the company expects to deploy over $1.9 billion through a combination of share buybacks ($1.1 billion), dividends ($315 million), organic growth investments ($300 million), and strategic acquisitions ($190 million).

The company’s capital deployment strategy is illustrated in the following breakdown:

For 2025 specifically, Secure plans to invest $125 million in organic growth initiatives, with approximately 90% directed toward waste management projects. Key investments include:

- Two new produced water disposal facilities with integrated pipelines, secured by 10-year contracts

- Expansion of oil terminal capacity (Clearwater Phase 3)

- Reopening and upgrading an industrial site in the Alberta Industrial Heartland

- Expanding railcar fleet to improve metals recycling transportation and distribution

- Network enhancements to increase throughput and grow same-store adjusted EBITDA

These investments are expected to generate high returns while leveraging the company’s core competencies in waste management and energy infrastructure.

Valuation and Investment Thesis

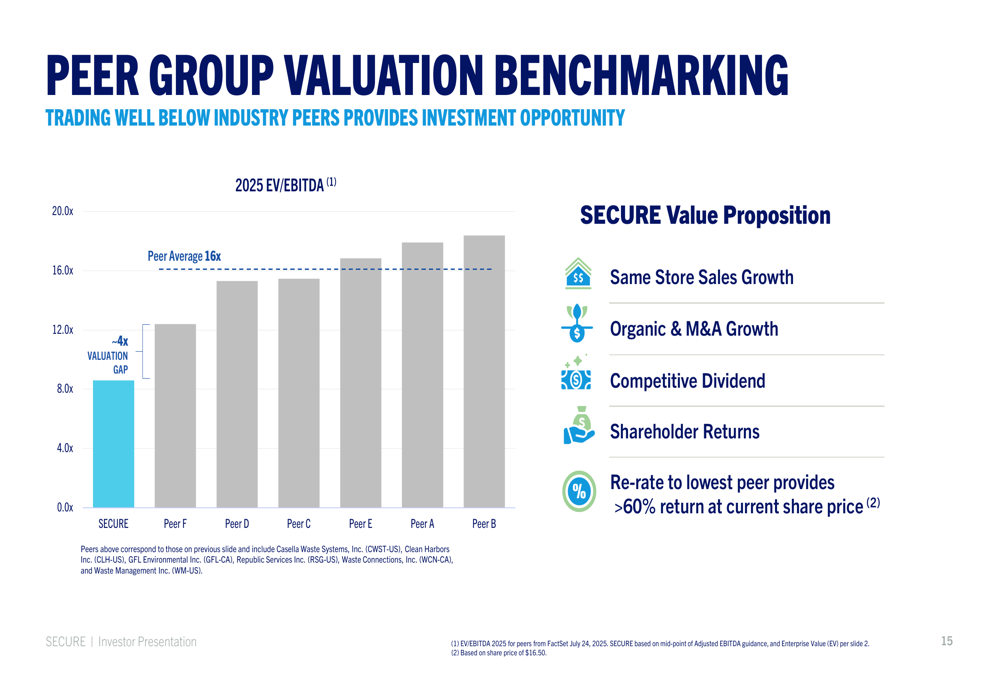

Despite its industry-leading financial metrics, Secure trades at a significant discount to waste management peers. The company’s 2025 EV/EBITDA multiple is approximately 4x below the peer average of 16x, suggesting substantial potential for share price appreciation through multiple expansion.

The valuation gap is clearly illustrated in the following peer comparison:

Management believes this valuation disconnect presents a compelling investment opportunity, with the potential for more than 60% share price appreciation if the company were to be valued at even the lowest peer multiple.

Secure’s investment thesis is supported by multiple drivers, including:

- Same store sales volume growth

- Organic expansion and strategic acquisitions

- Competitive dividend yield of 2.4%

- Significant shareholder returns through share repurchases (nearly 30% of outstanding shares repurchased over the past 2.5 years)

- Strong financial position with substantial liquidity to execute on strategic priorities

The company’s summary of key investment highlights reinforces these points:

With its critical infrastructure network, recurring revenue streams, strong financial performance, and attractive valuation relative to peers, Secure Energy Services appears well-positioned to deliver continued value to shareholders through both operational execution and potential multiple expansion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.