Stock market today: S&P 500 hits fresh record close on stronger economic growth

Introduction & Market Context

Selective Insurance Group, Inc. (NASDAQ:SIGI) released its second quarter 2025 investor presentation on July 24, showcasing improved performance metrics after a challenging first quarter. As the 34th largest property and casualty (P&C) insurer in the United States with approximately 1.5% market share in commercial lines, Selective has positioned itself as an outperformer against industry peers in key profitability metrics.

The presentation comes after a mixed Q1 2025 earnings report where the company missed EPS expectations ($1.76 vs. forecast of $1.88) but exceeded revenue projections. The latest presentation suggests a stronger second quarter performance, with half-year metrics showing significant improvement over full-year 2024 results.

Quarterly Performance Highlights

Selective reported a non-GAAP operating return on equity (ROE) of 12.5% for the first half of 2025, substantially higher than the 7.0% achieved for full-year 2024. This improvement indicates a strong rebound in Q2 after the challenging first quarter. Similarly, the combined ratio improved to 98.2% for 1H25 compared to 103.0% for full-year 2024.

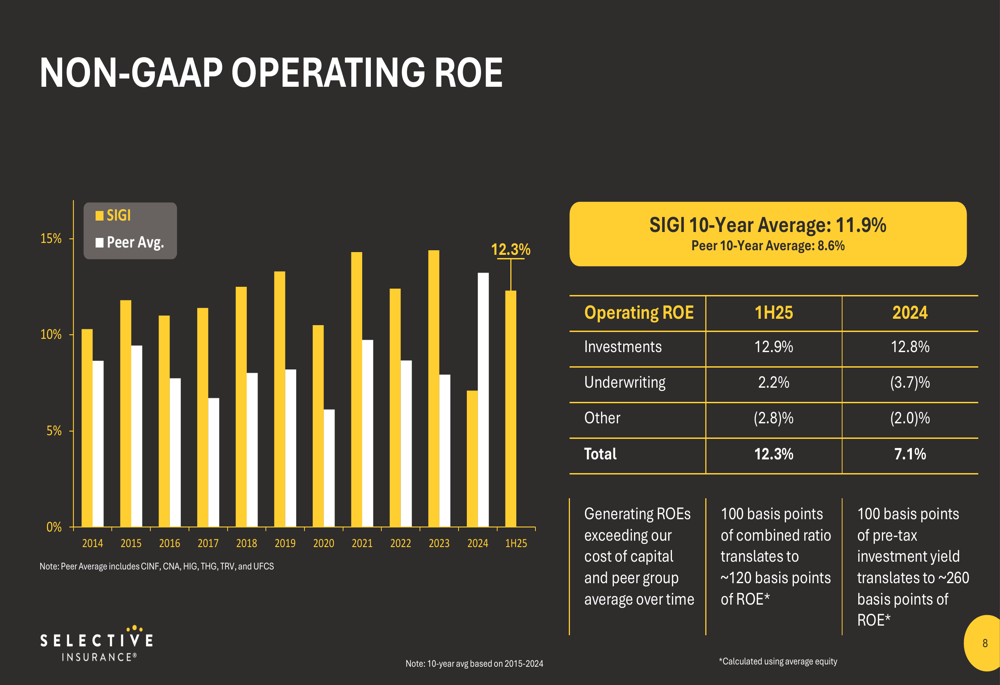

As shown in the following chart detailing Selective’s performance against peers, the company has consistently outperformed its peer group in ROE metrics over the past decade:

The company’s 10-year average ROE stands at 11.9%, significantly outpacing the peer average of 8.6%. For 1H25, the ROE breakdown shows 12.9% contribution from investments, 2.2% from underwriting, and a -2.8% impact from other factors, resulting in a total of 12.3%.

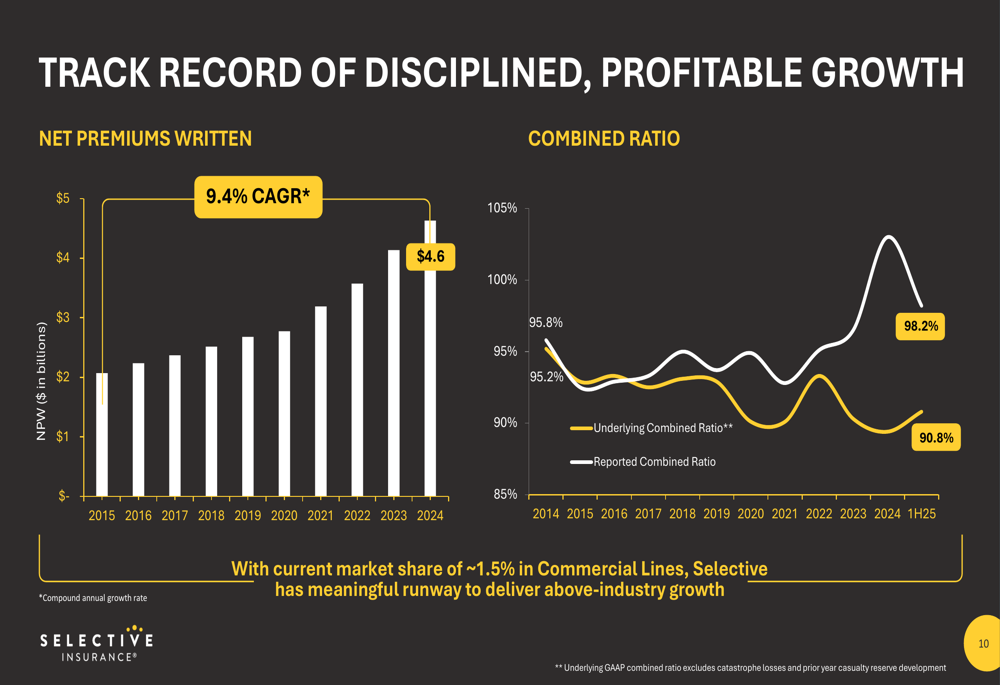

Selective has demonstrated a consistent track record of profitable growth, with net premiums written growing at a compound annual growth rate of 9.4% from 2015 to 2024, reaching $4.6 billion. The company’s combined ratio performance has also been strong relative to the industry:

Segment Performance

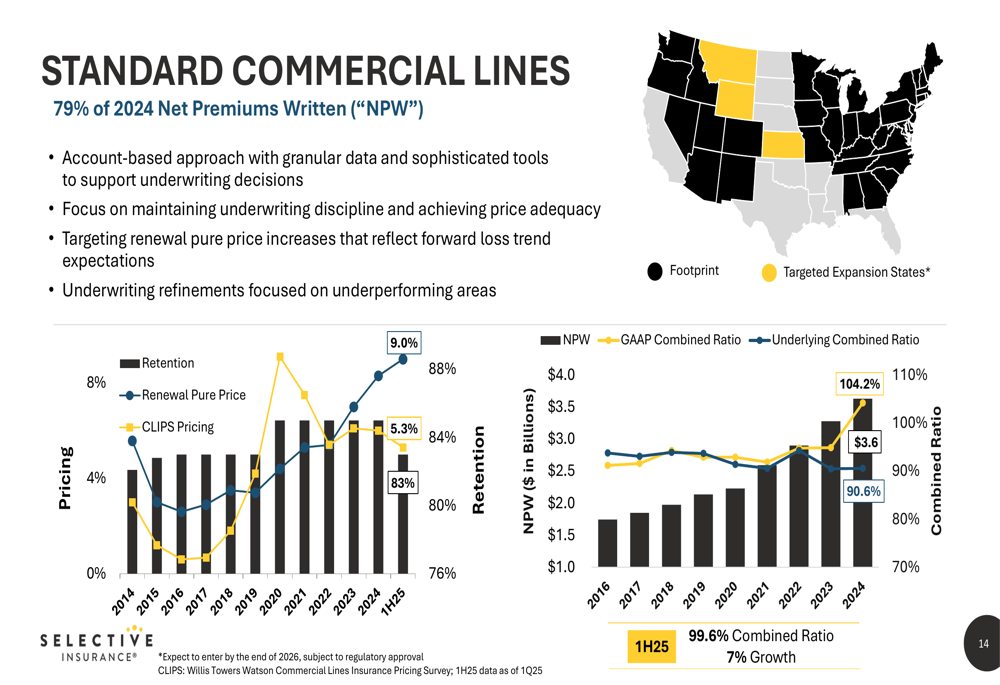

Standard Commercial Lines, representing 79% of Selective’s 2024 net premiums written, showed solid performance in 1H25 with an underlying combined ratio of 90.6% and a reported combined ratio of 99.6%. The segment achieved 5.3% renewal pure price increases while maintaining a strong retention rate of 84%.

As illustrated in the following segment overview:

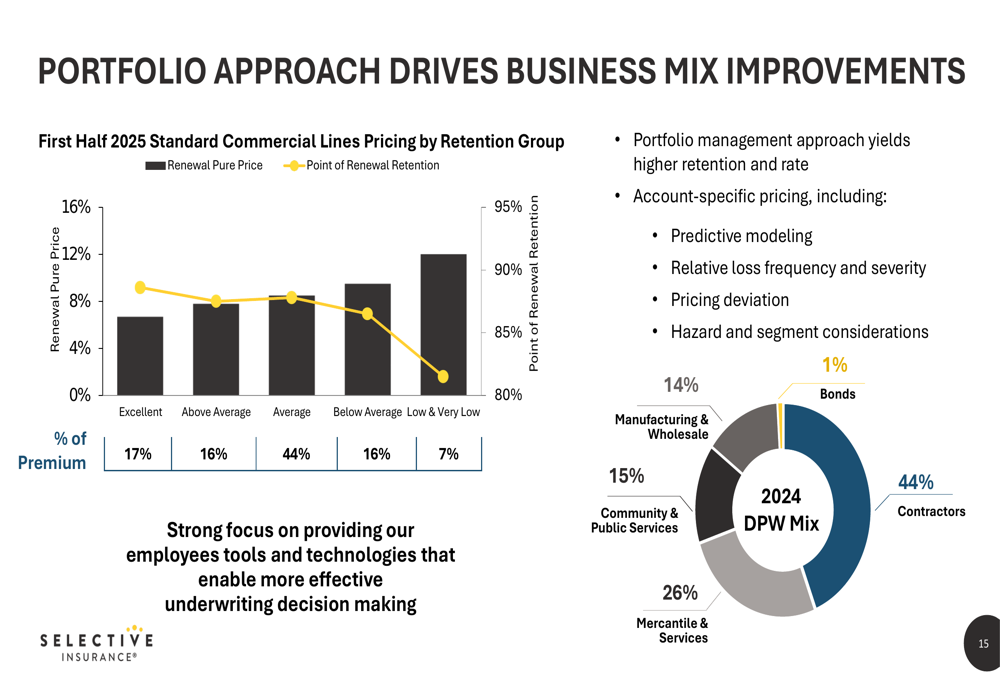

The company employs a sophisticated portfolio approach to managing its commercial business, segmenting accounts by performance quality and adjusting pricing accordingly. This strategy has allowed Selective to maintain profitability while growing selectively:

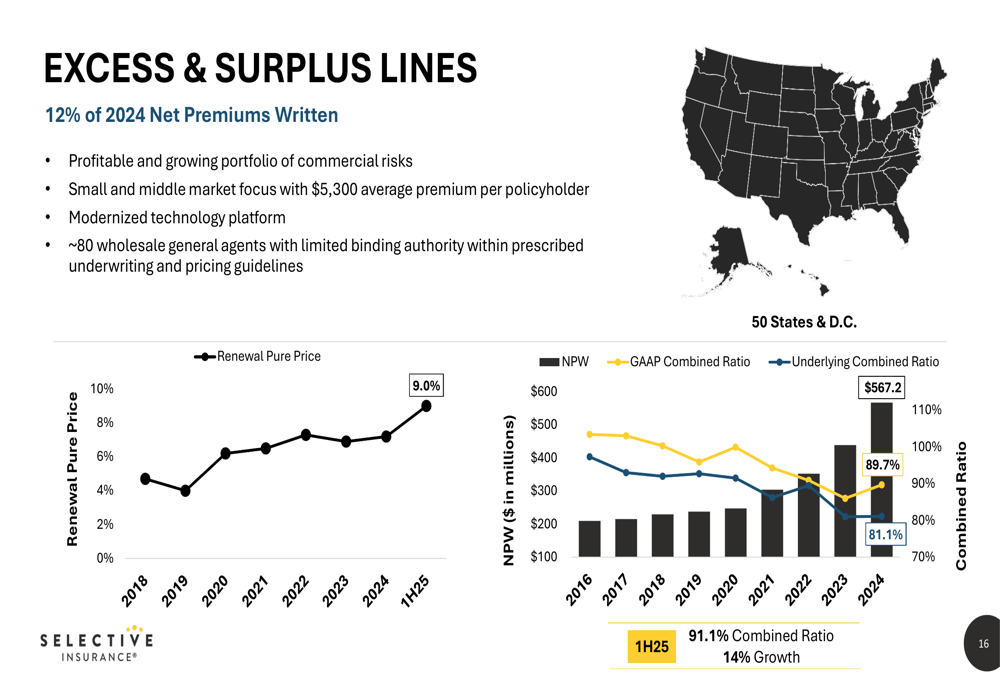

Excess and Surplus Lines, accounting for 12% of 2024 net premiums written, has been a standout performer with a combined ratio of 89.7% for 1H25 and 14% growth. The segment achieved 9.0% renewal pure price increases in the first half of 2025:

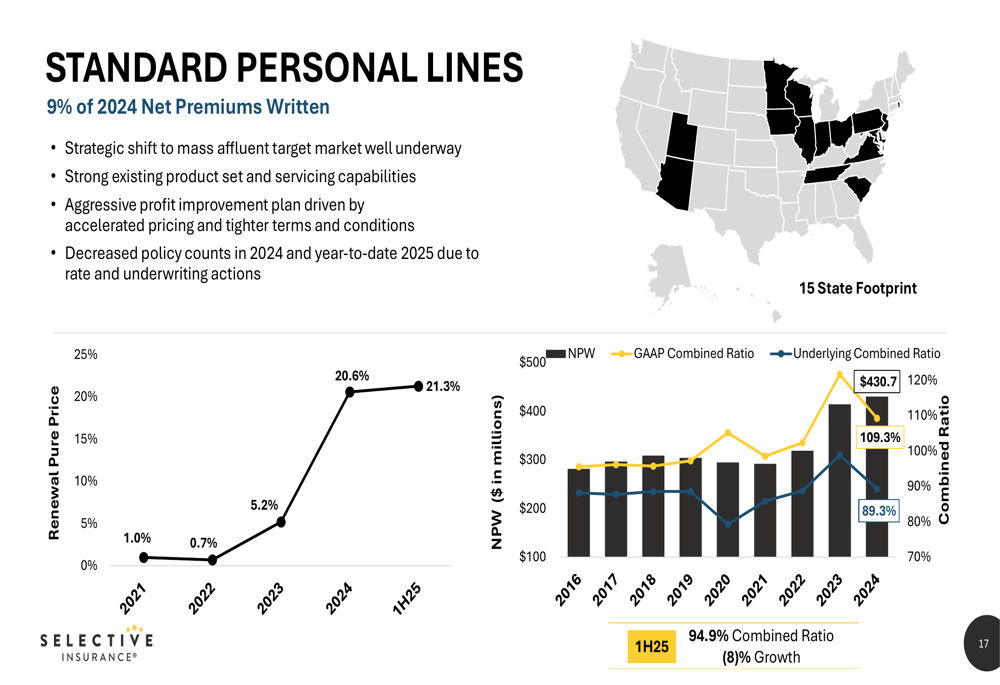

Standard Personal Lines, representing 9% of the business, is undergoing a strategic shift toward the mass-affluent market. The segment has implemented aggressive pricing actions with renewal pure price increases of 21.3% in 1H25, reflecting the company’s focus on improving profitability in this challenging line:

Strategic Initiatives

Selective outlined its path for profitable growth across all business segments, with a particular focus on geographic expansion. The company has added thirteen states to its Standard Commercial Lines footprint since 2017 and aims to achieve a near-national presence in the coming years:

The company’s strategy includes targeting 3% market share in its existing footprint over the long term, increasing share of wallet with existing distribution partners to 12%, and achieving 25% agent market share in existing markets.

For Personal Lines, Selective is focusing on the mass-affluent segment where its coverage and service capabilities are most competitive. In Excess and Surplus Lines, the company is pursuing opportunistic growth by expanding capabilities and products.

Forward-Looking Statements

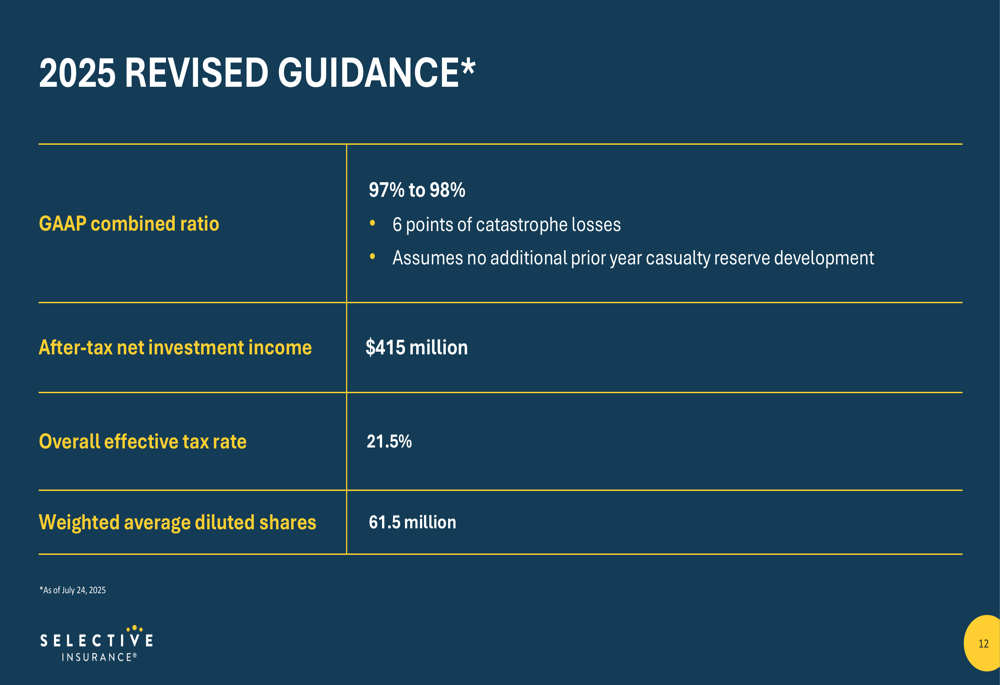

Selective provided revised guidance for 2025, projecting a GAAP combined ratio between 97% and 98%, which includes 6 percentage points of catastrophe losses and assumes no additional prior-year casualty reserve development:

The company expects after-tax net investment income of $415 million, an overall effective tax rate of 21.5%, and weighted average diluted shares of 61.5 million.

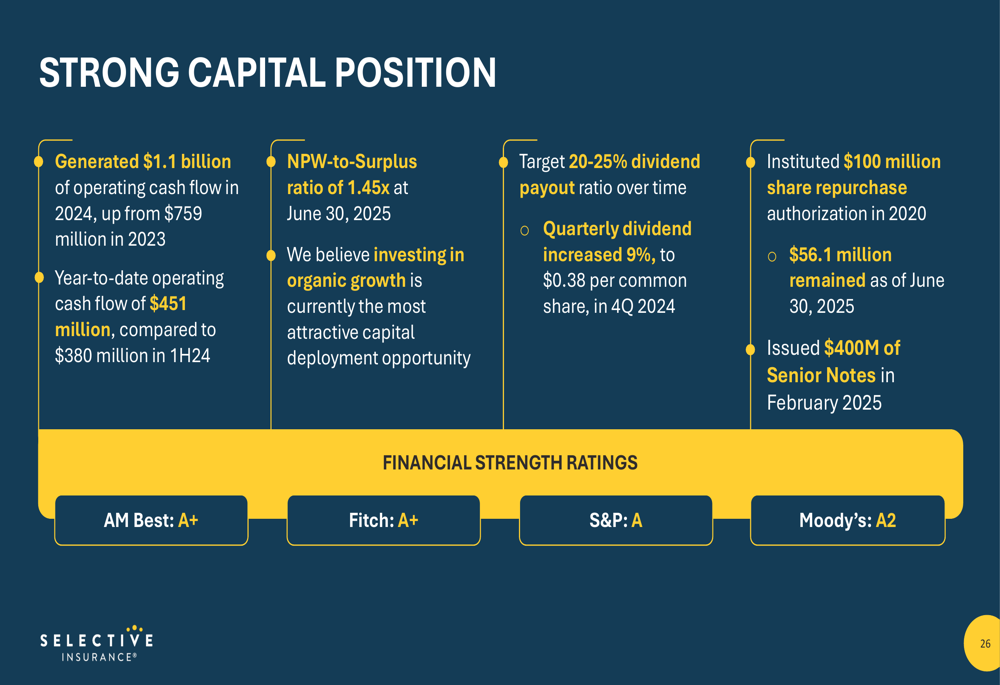

Selective maintains a strong capital position with $1.1 billion of cash flow generated and $451 million in year-to-date operating cash flow. The company’s net premiums written to surplus ratio stands at 1.45x as of June 30, 2025, and it maintains strong ratings from major agencies, including an A+ rating from AM Best:

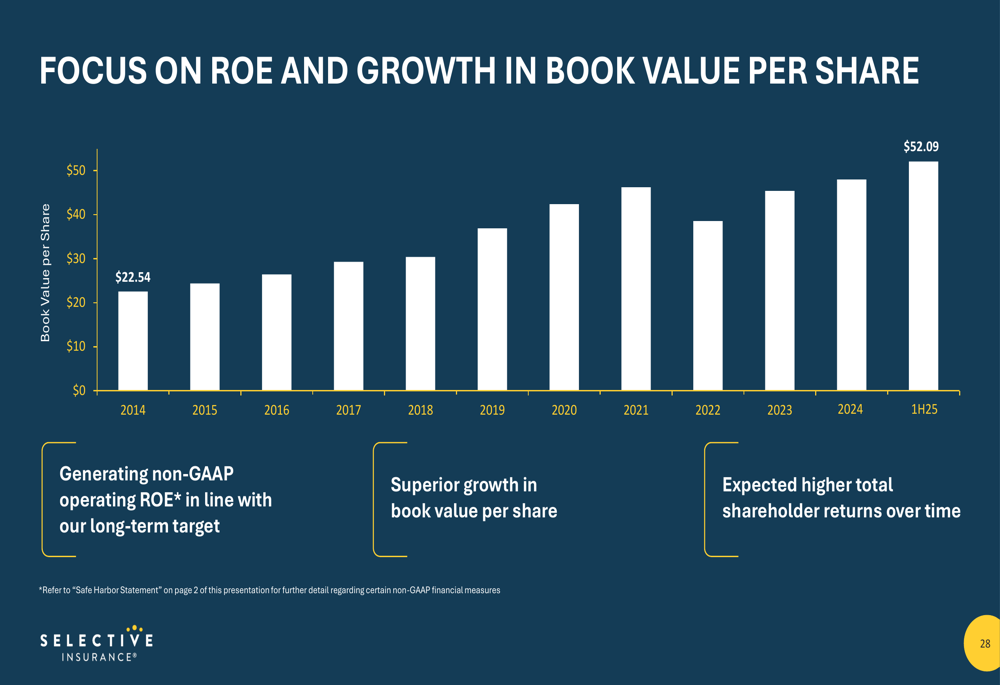

The company’s book value per share has shown consistent growth, increasing from $22 in 2014 to $52 by 1H25, reflecting Selective’s long-term focus on building shareholder value:

Selective’s presentation demonstrates a company that has rebounded strongly in Q2 2025 after a challenging first quarter, with improved profitability metrics and a clear strategy for continued growth through geographic expansion and segment-specific initiatives. The revised guidance for 2025 suggests management confidence in maintaining this positive momentum through the remainder of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.