Fed Governor Adriana Kugler to resign

SelectQuote Inc (NYSE:SLQT) presented its third-quarter fiscal 2025 earnings results on May 12, 2025, highlighting 8% revenue growth while navigating a shift in its business mix toward its rapidly expanding Healthcare Services (NASDAQ:HCSG) division.

Quarterly Performance Highlights

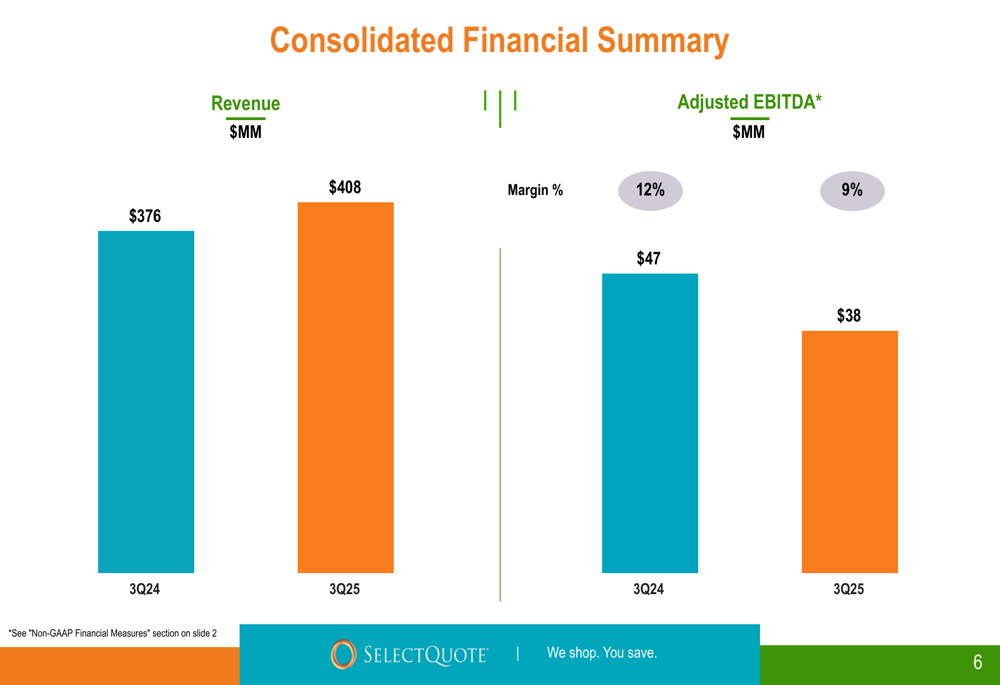

The insurance marketplace and healthcare services provider reported consolidated revenue of $408.2 million for the quarter, an 8% increase from $376.4 million in the same period last year. However, Adjusted EBITDA declined to $37.7 million from $46.6 million in Q3 FY24, reflecting a margin compression from 12% to 9%.

"We delivered solid revenue growth this quarter while continuing to optimize our operations across all segments," said Tim Danker, CEO of SelectQuote, according to the presentation materials. The company highlighted a combined Senior and Healthcare Services Rev-to-CAC (Revenue to Customer Acquisition Cost) ratio of 5.8X, demonstrating efficient customer acquisition despite challenges.

As shown in the following consolidated financial summary:

Segment Analysis

Senior Division

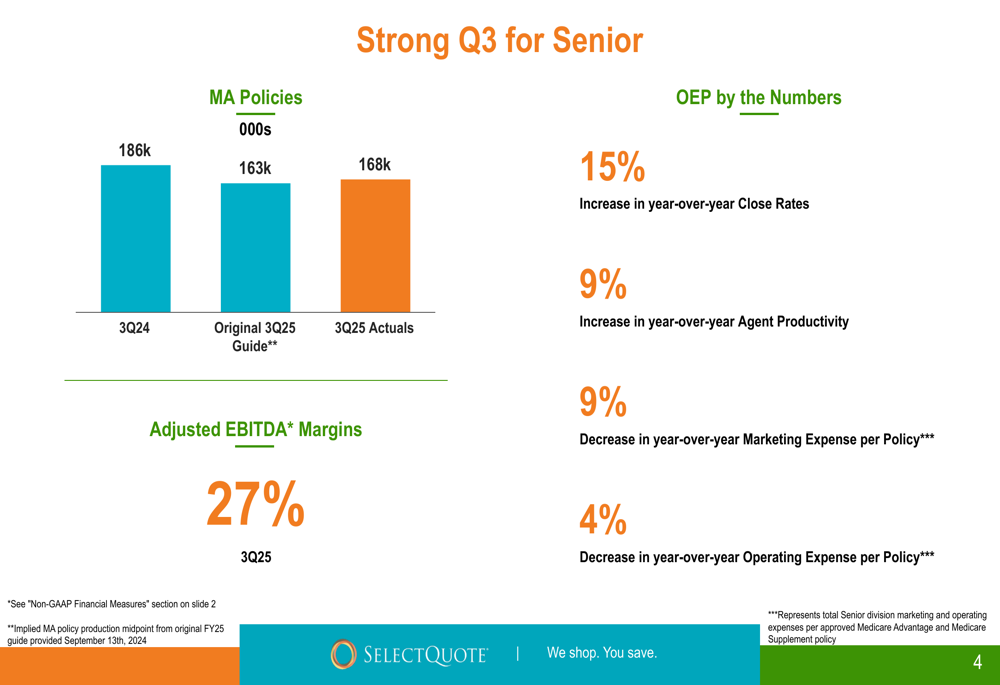

SelectQuote’s Senior division, which focuses on Medicare Advantage plans, showed operational improvements despite lower policy volumes. The segment delivered 168,000 MA policies in Q3, exceeding the original guidance of 163,000 but still below the 186,000 policies from Q3 FY24. Notably, these results were achieved with 26% fewer agents, indicating significant efficiency gains.

The Senior segment posted revenue of $169 million, down from $204 million in the prior year, with Adjusted EBITDA of $46 million (27% margin) compared to $61 million (30% margin) in Q3 FY24.

The company’s operational improvements in the Senior segment are illustrated in the following slide:

The company reported a 15% increase in year-over-year close rates, 9% increase in agent productivity, 9% decrease in marketing expense per policy, and 4% decrease in operating expense per policy. These efficiency gains helped mitigate the impact of lower policy volumes.

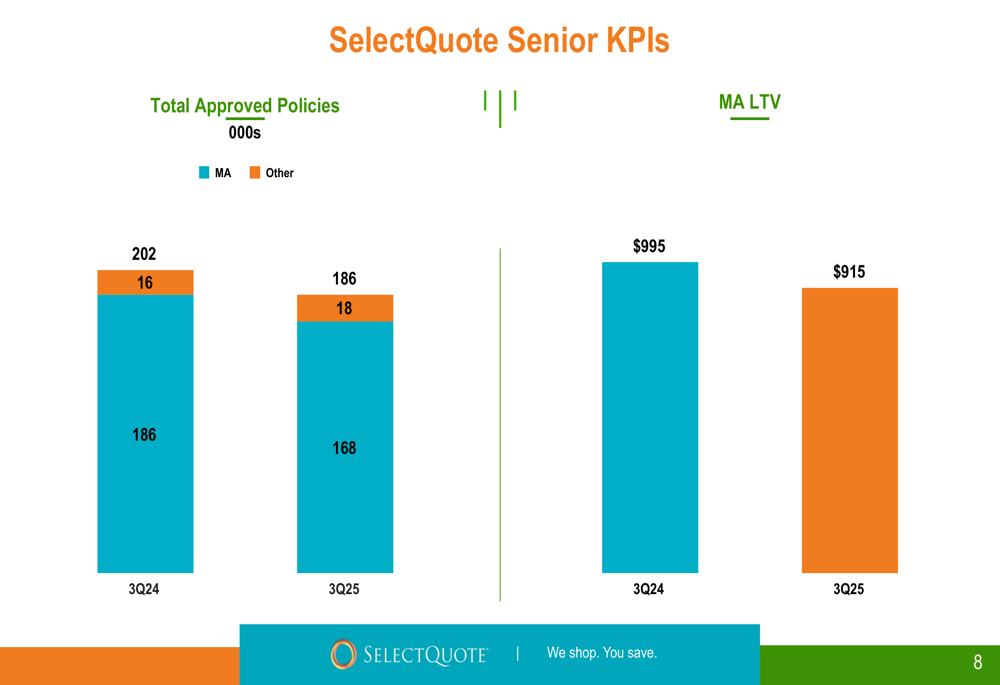

The MA Lifetime Value (LTV) metric decreased to $915 from $995 in the prior year period, as shown in the following KPI summary:

Healthcare Services

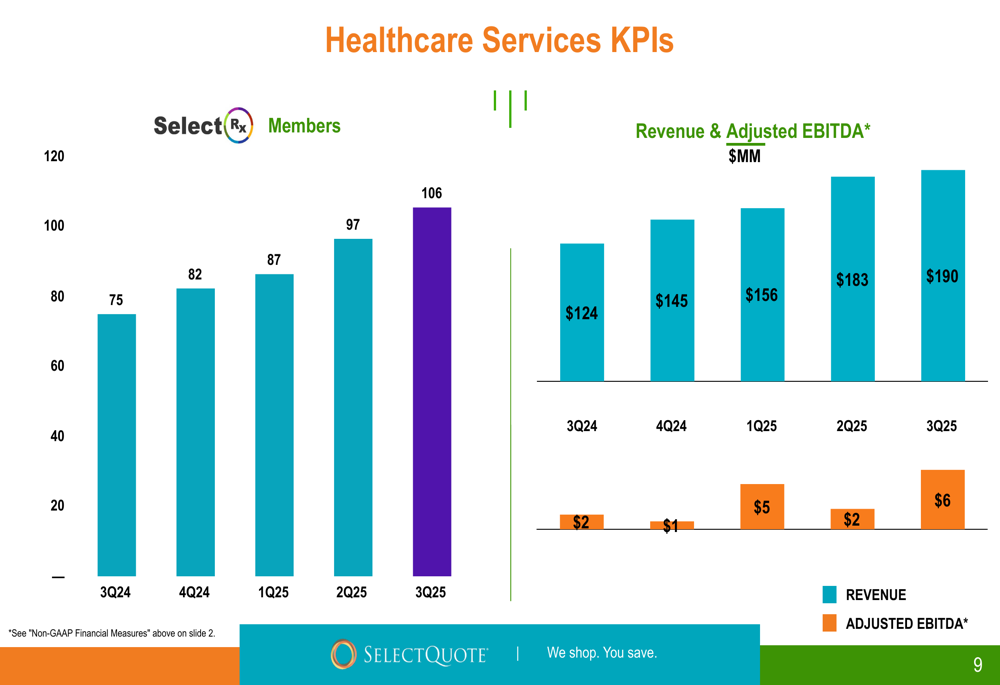

The Healthcare Services division, anchored by the SelectRx pharmacy services business, continues to be the company’s primary growth driver. SelectRx membership reached nearly 106,000 members as of Q3 FY25, representing 41% year-over-year growth. The division achieved positive Adjusted EBITDA for the eighth consecutive quarter.

The following chart illustrates the steady growth in SelectRx membership and financial performance:

Healthcare Services generated $190 million in revenue for Q3 FY25, up from $124 million in Q3 FY24, with Adjusted EBITDA of $6 million compared to $2 million in the prior year period. The division has achieved nearly $675 million in trailing 12-month revenue, establishing it as a significant component of SelectQuote’s business.

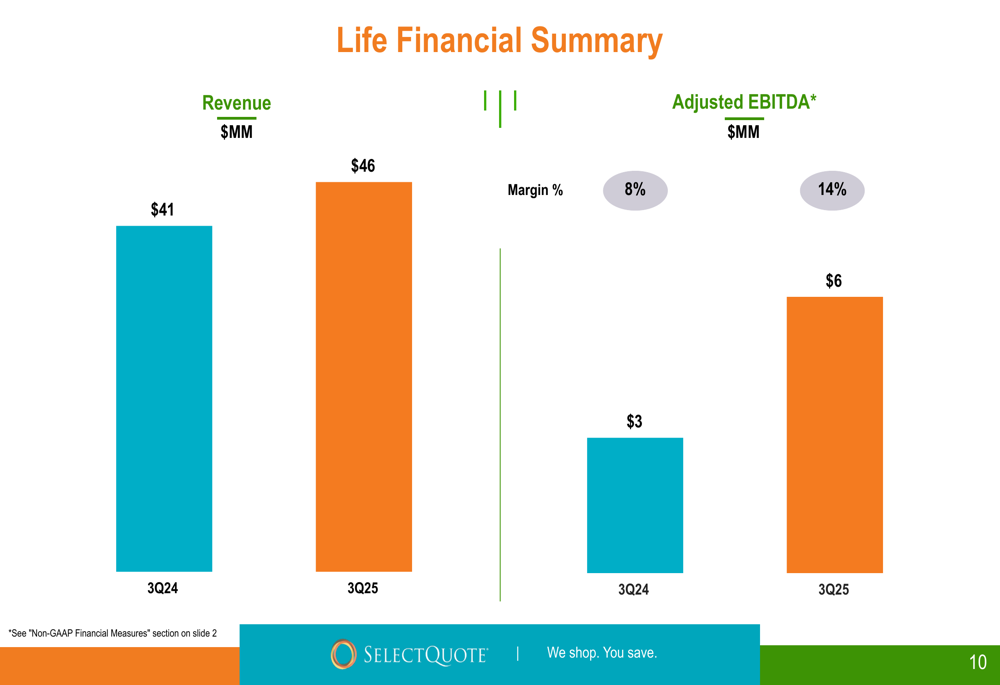

Life Segment

The Life insurance segment showed improvement, with revenue increasing to $46 million from $41 million in Q3 FY24. Adjusted EBITDA doubled to $6 million from $3 million, with margins expanding from 8% to 14%.

The Life segment’s financial performance is illustrated in the following summary:

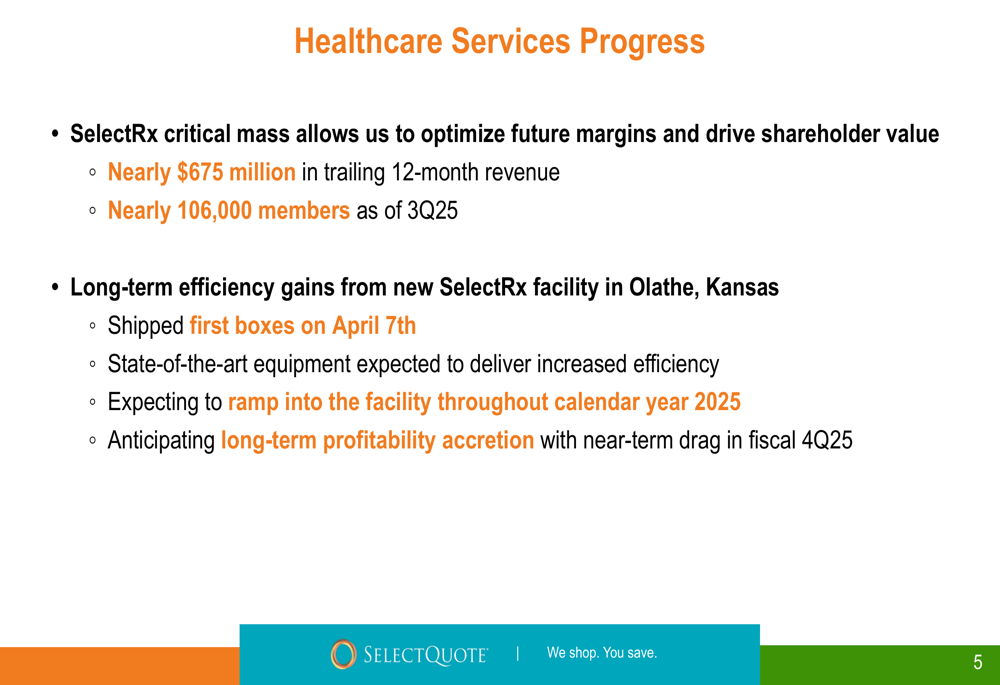

Strategic Initiatives

A key strategic focus for SelectQuote is its investment in a new SelectRx facility in Olathe, Kansas, which shipped its first prescriptions on April 7th. Management expects this state-of-the-art facility to deliver increased efficiency and drive long-term profitability for the Healthcare Services division, though it may create some near-term drag in fiscal Q4 2025.

"The new Olathe facility represents a significant investment in our future growth and operational capabilities," noted the company in its presentation. "We expect to ramp into the facility throughout calendar year 2025, with long-term profitability accretion."

The Healthcare Services progress and facility update is detailed in the following slide:

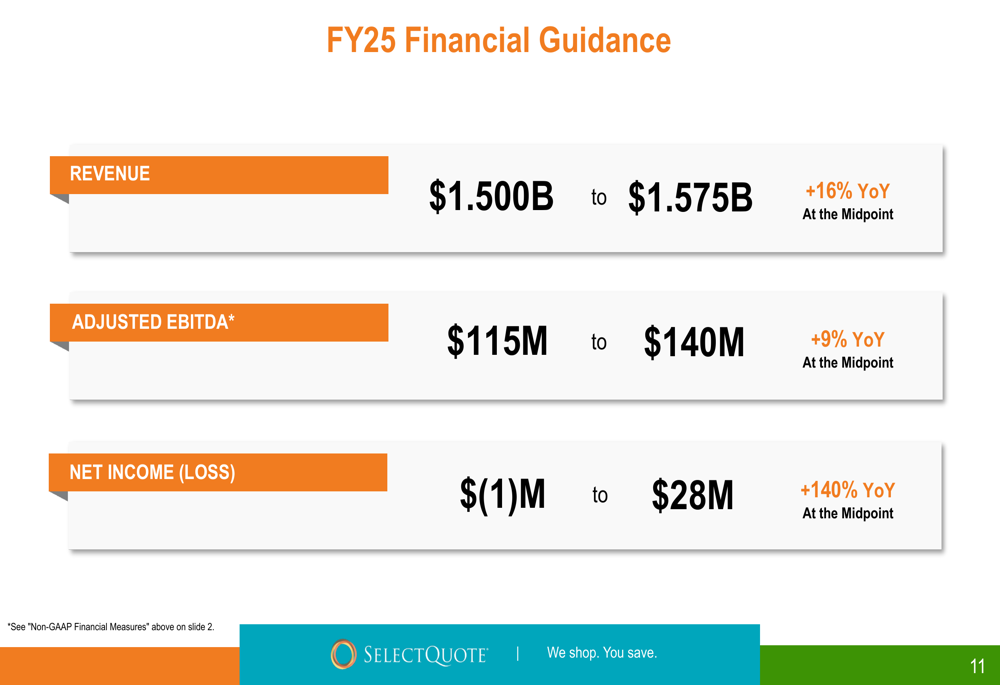

Forward-Looking Statements

SelectQuote maintained its fiscal 2025 guidance, projecting revenue between $1.500 billion and $1.575 billion, representing 16% year-over-year growth at the midpoint. The company expects Adjusted EBITDA between $115 million and $140 million, a 9% increase at the midpoint, and Net Income between a $1 million loss and $28 million profit, representing a 140% improvement at the midpoint.

The company’s full-year guidance is summarized in the following slide:

This guidance reflects continued confidence in the company’s business model despite the evolving mix between segments. The projected improvement in net income suggests management expects operational efficiencies to continue delivering results.

Market Context

SelectQuote’s Q3 results come after a strong start to fiscal 2025, where the company reported 26% revenue growth in Q1. The deceleration to 8% growth in Q3 indicates some normalization, though the Healthcare Services segment continues to show robust expansion.

The stock closed at $2.67 on May 9, 2025, down 2.2% for the session, according to market data. Year-to-date, SelectQuote shares have shown volatility, with the stock trading well below its 52-week high of $6.86 but above its 52-week low of $1.62.

The company’s strategic shift toward Healthcare Services and operational improvements in its core Senior business appear aimed at creating a more balanced and sustainable growth model, though investors will likely focus on the path to improved profitability given the Adjusted EBITDA decline in Q3.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.