Fannie Mae, Freddie Mac shares tumble after conservatorship comments

Introduction & Market Context

Sempra Energy (NYSE:SRE) presented its first quarter 2025 earnings results on May 8, 2025, showing signs of recovery after a challenging fourth quarter 2024. The company reported adjusted earnings per share (EPS) of $1.44, representing a 7.5% increase from $1.34 in the same period last year. This performance comes after Sempra’s stock dropped nearly 19% following its Q4 2024 earnings miss, when it reported EPS of $1.50 against an expected $1.58.

The utility company’s shares have partially recovered since then, with the stock closing at $75.86 on May 7, 2025, up 1.05% for the day. According to available data, Sempra is currently trading well above its 52-week low of $61.90 but remains significantly below its 52-week high of $95.77.

Quarterly Performance Highlights

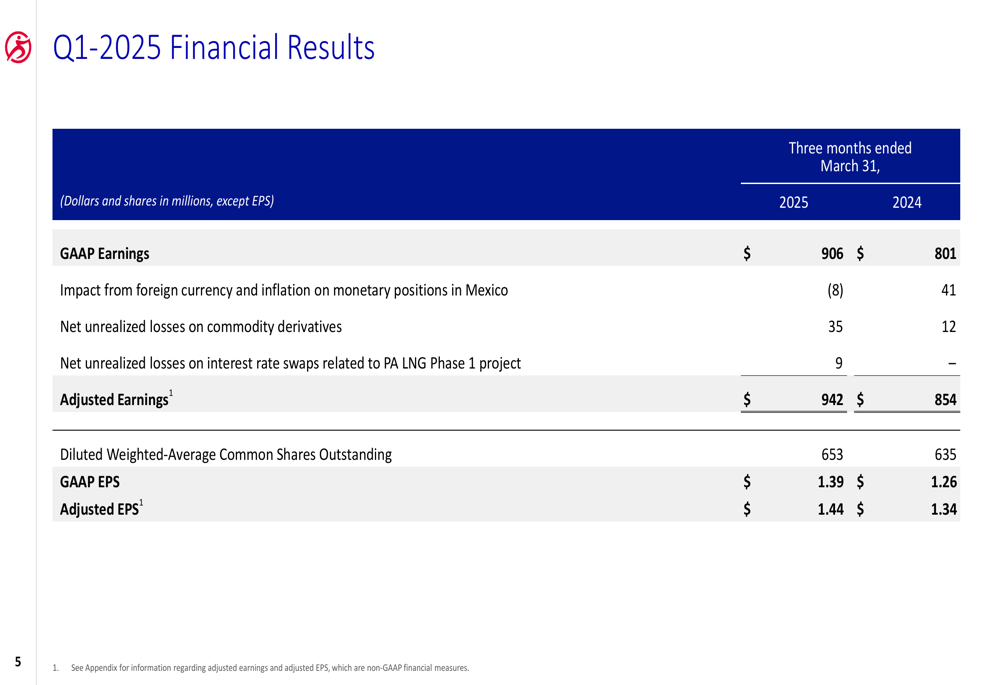

Sempra reported GAAP earnings of $906 million for Q1 2025, a 13.1% increase from $801 million in Q1 2024. On an adjusted basis, which excludes certain items such as foreign currency impacts and unrealized losses on commodity derivatives, earnings rose to $942 million from $854 million, representing a 10.3% year-over-year increase.

As shown in the following financial results comparison:

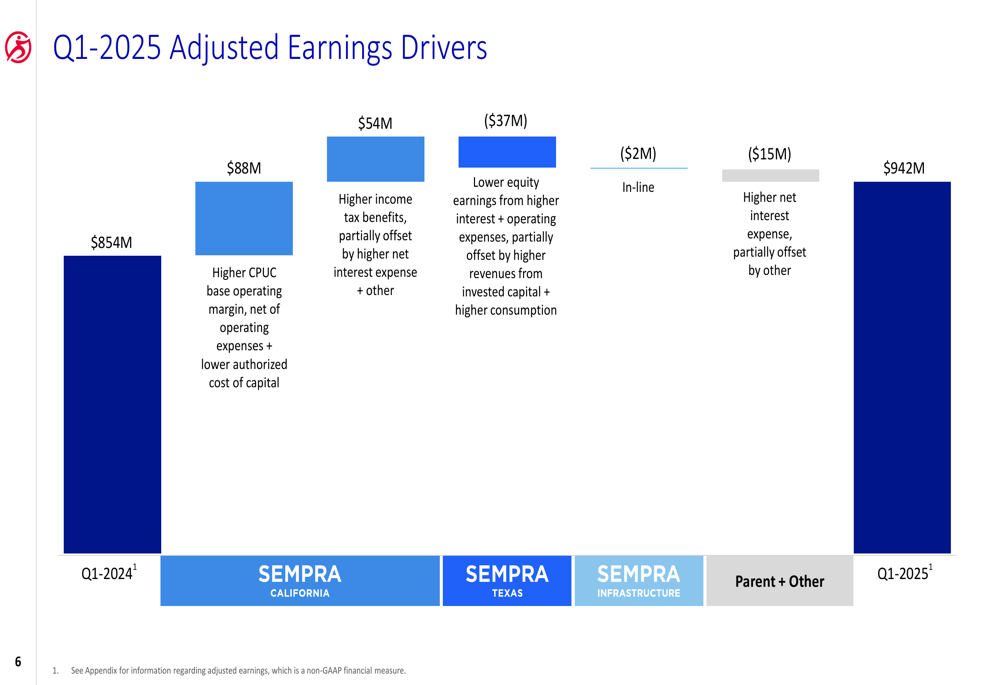

The primary drivers of the adjusted earnings growth included strong performance from Sempra California, which contributed an additional $88 million due to higher CPUC base operating margin and lower authorized cost of capital. Sempra Texas added $54 million from higher income tax benefits, partially offset by higher net interest expenses. However, Sempra Infrastructure saw a $37 million decrease due to higher interest and operating expenses, though this was partially offset by higher revenues from invested capital and increased consumption.

The following chart breaks down the contribution of each business segment to the overall earnings growth:

By business unit, Sempra California reported GAAP earnings of $724 million in Q1 2025, up from $582 million in Q1 2024. This increase was primarily driven by $88 million in higher CPUC base operating margin (net of operating expenses), $13 million in lower authorized cost of capital, and $62 million in higher income tax benefits, partially offset by $15 million in higher net interest expense.

Sempra Texas Utilities, however, saw GAAP earnings decrease to $146 million from $183 million in the prior year period, primarily due to higher interest expense and depreciation expense associated with increases in invested capital, as well as higher operations and maintenance costs.

Strategic Initiatives

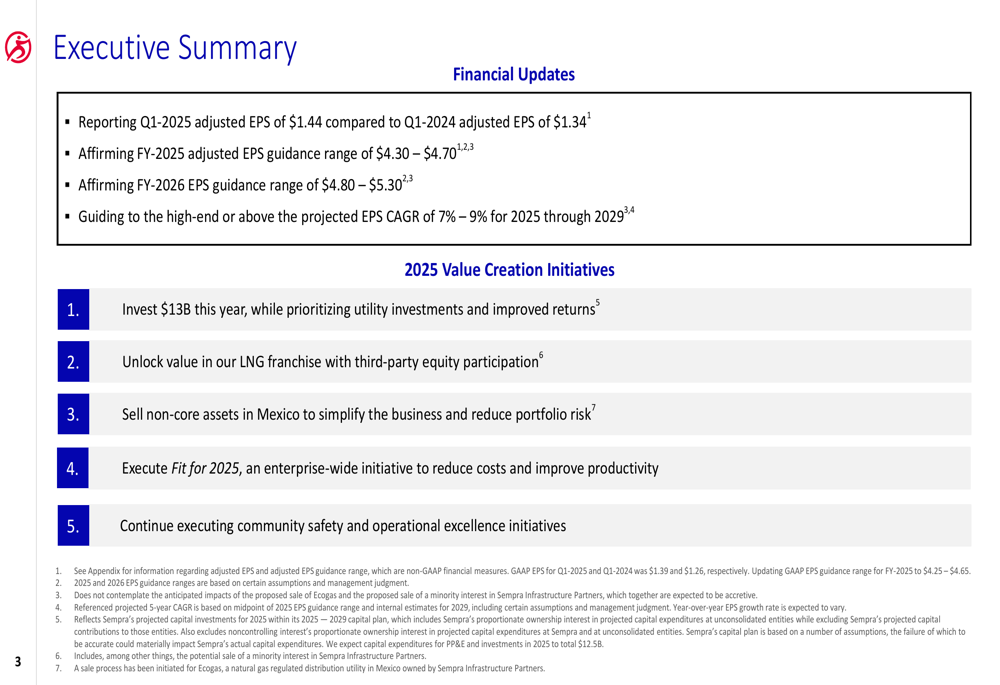

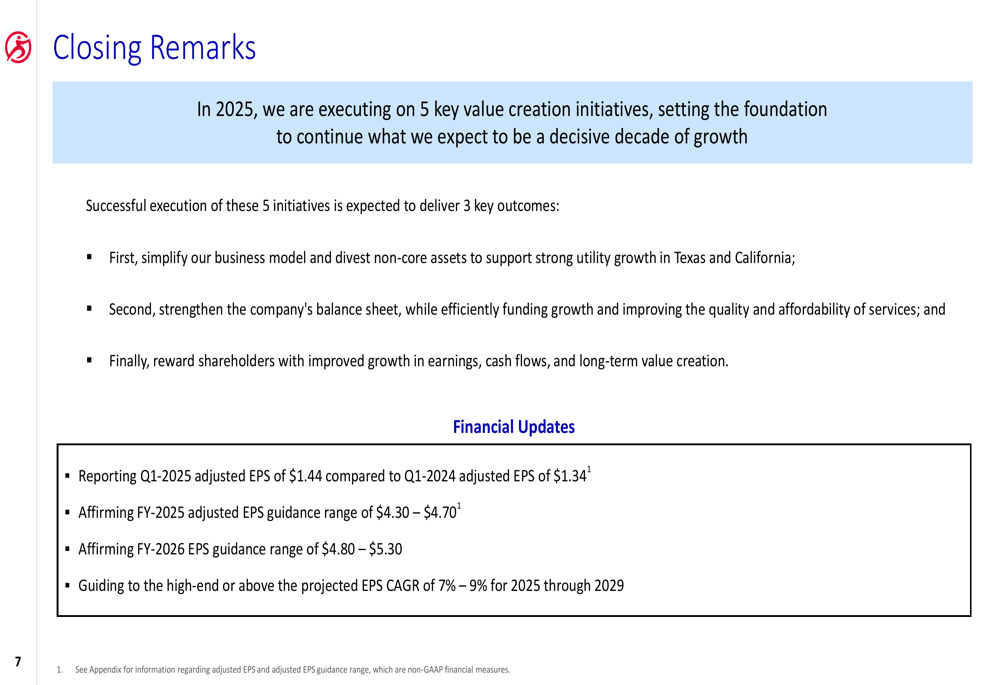

Sempra outlined five key value creation initiatives for 2025 that aim to simplify the business model, strengthen the balance sheet, and improve shareholder returns. These initiatives include investing $13 billion this year (prioritizing utility investments), unlocking value in the LNG franchise, selling non-core assets in Mexico, executing a cost reduction program, and continuing safety and operational excellence initiatives.

The company’s executive summary highlights these strategic priorities alongside financial performance:

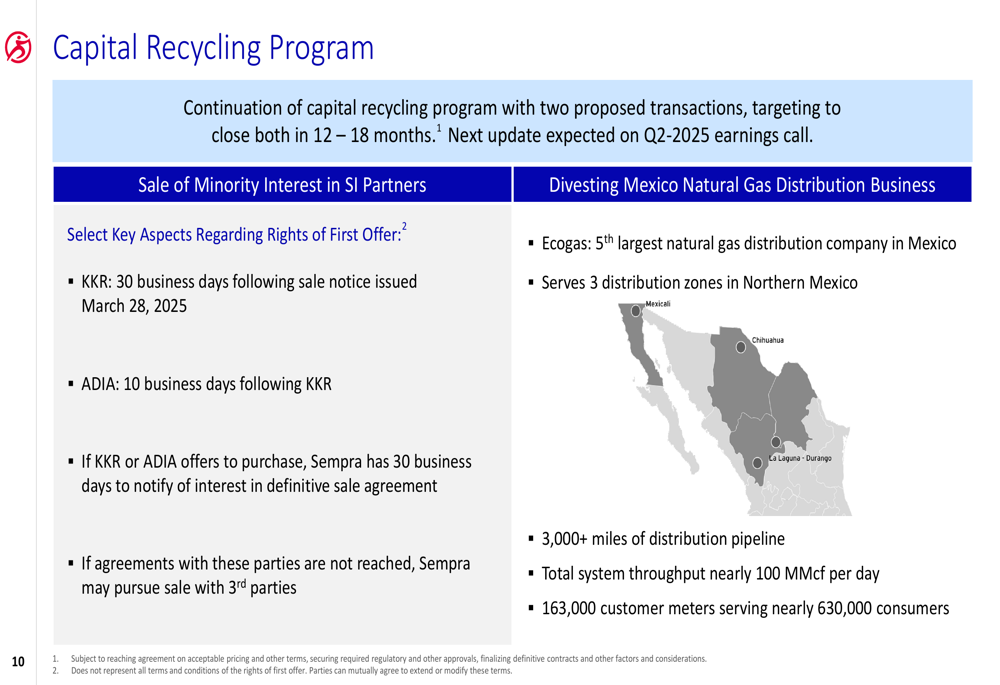

A significant component of Sempra’s strategy involves its capital recycling program, which includes two major transactions: selling a 15-30% minority interest in Sempra Infrastructure Partners and divesting Ecogas, its natural gas distribution business in Mexico. These transactions are expected to close within 12-18 months, with updates anticipated in the Q2 2025 earnings call.

The following slide details the capital recycling program and provides information about the Ecogas business:

In Texas, Sempra is positioning itself to capitalize on substantial transmission expansion opportunities driven by load growth. The company’s subsidiary Oncor expects to build a significant portion of transmission projects with total estimated costs between $32-35 billion, including Permian Basin Reliability Plan Projects, Import Paths, Local Common Projects, and additional Regional Transmission Plan projects.

Forward-Looking Statements

Sempra affirmed its full-year 2025 adjusted EPS guidance range of $4.30-$4.70 and its 2026 EPS guidance range of $4.80-$5.30. The company also indicated it expects to achieve the high-end or above its projected EPS compound annual growth rate (CAGR) of 7-9% for the period from 2025 through 2029.

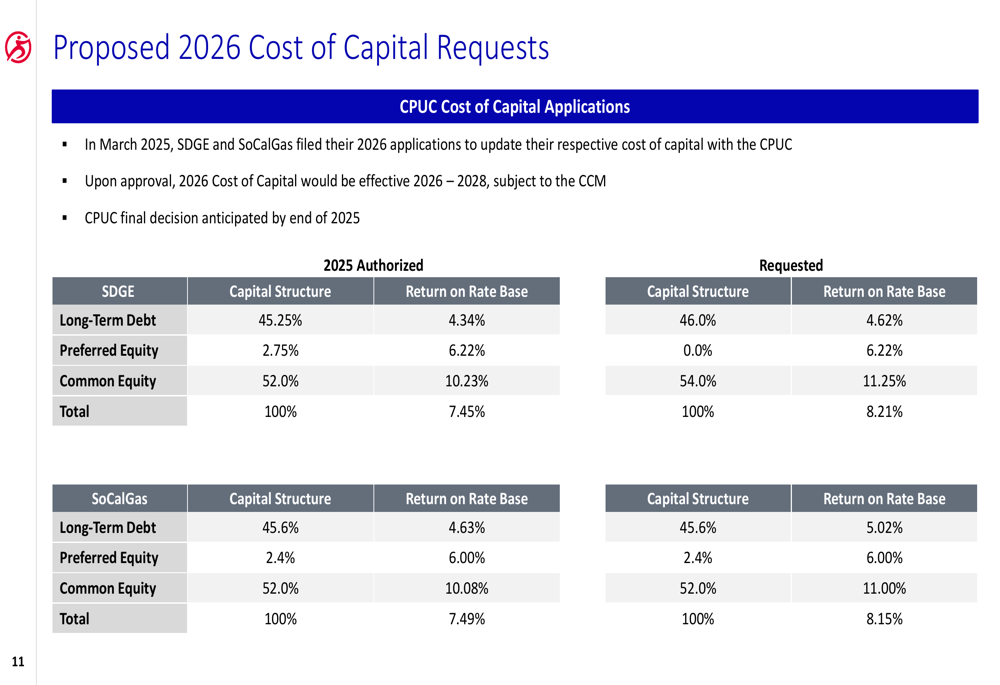

For its California utilities, Sempra has filed applications to update their cost of capital structures for 2026-2028. San Diego Gas & Electric (SDGE) is requesting an increase in its return on rate base from 7.45% to 8.21%, while Southern California Gas Company (SoCalGas) is seeking an increase from 7.49% to 8.15%. These requests include higher returns on common equity of 11.25% and 11.00%, respectively.

The proposed cost of capital structures are detailed in the following slide:

Conclusion

Sempra’s Q1 2025 results demonstrate a recovery trajectory following its disappointing Q4 2024 performance. The company’s focus on strategic initiatives, particularly its capital recycling program and investments in high-growth areas like Texas transmission, positions it for long-term growth despite near-term challenges.

While the company faces some headwinds in its Texas utilities segment due to higher expenses, strong performance in California and a clear strategic direction provide a foundation for the projected earnings growth through 2029. Sempra’s affirmation of its full-year guidance suggests management confidence in the company’s ability to execute its strategic plan and deliver value to shareholders.

As summarized in the company’s closing remarks:

Investors will be watching closely to see if Sempra can maintain this positive momentum throughout 2025 and successfully execute on its strategic initiatives, particularly as it works to optimize its portfolio through the planned divestments and strengthen its position in key growth markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.