Dollar edges higher ahead of Fed minutes; sterling gains after CPI increase

Introduction & Market Context

Sensata Technologies (NYSE:ST) released its second quarter 2025 earnings presentation on July 29, 2025, revealing a company successfully navigating challenging market conditions through operational efficiency improvements. While revenue declined year-over-year, the company exceeded guidance across key financial metrics, with particularly strong free cash flow performance.

The presentation comes amid mixed global automotive production trends, with S&P estimating flat year-over-year production globally but significant regional variations. North America and Europe markets are projected down 3-4% for the full year, offset by growth in China. Meanwhile, North America truck production faces a steeper 24% year-over-year decline, creating headwinds for Sensata’s Performance Sensing segment.

Quarterly Performance Highlights

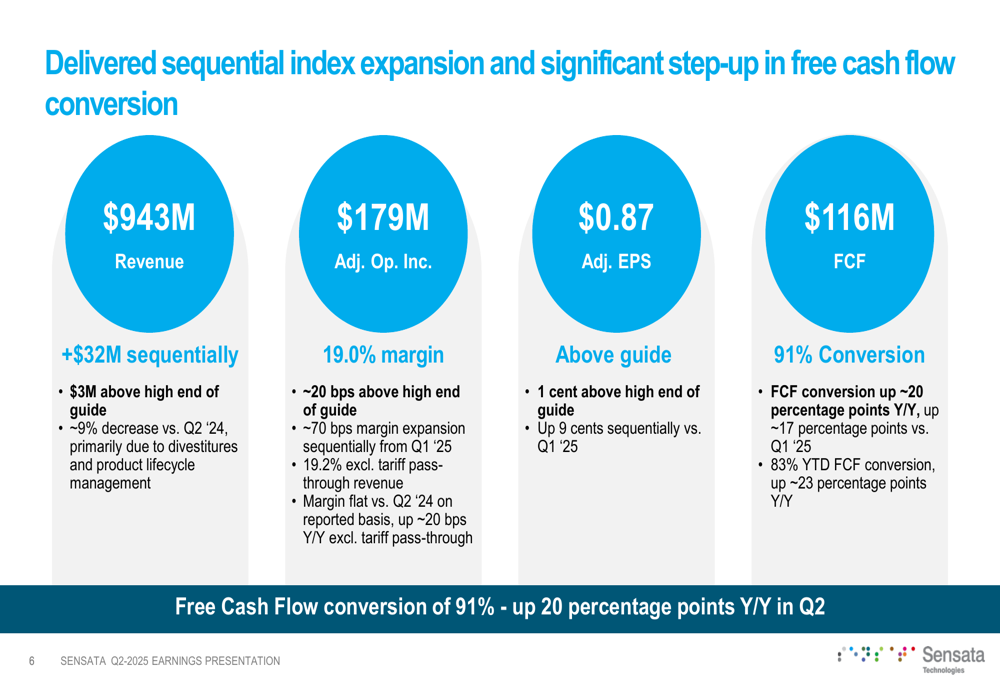

Sensata reported Q2 2025 revenue of $943 million, representing a sequential increase of $32 million from Q1 but a year-over-year decline of approximately 9%. The company attributed this decline primarily to strategic divestitures and product lifecycle management decisions rather than underlying market weakness.

As shown in the following financial performance summary, Sensata exceeded expectations across key metrics:

Despite the revenue decline, adjusted operating income reached $179 million with a 19.0% margin, approximately 20 basis points above the high end of guidance. This represents a 70 basis point margin expansion sequentially from Q1 2025. Adjusted earnings per share of $0.87 exceeded the high end of guidance by 1 cent and improved 9 cents sequentially.

CEO Stephan von Schuckmann highlighted the company’s operational progress: "Our back-to-basics approach continues to deliver. We are building resiliency in our business and we are pleased to report a strong second quarter where we exceeded our revenue and earnings commitments and significantly improved our free cash flow."

The most notable achievement was the substantial improvement in free cash flow, which reached $116 million with a 91% conversion rate. This represents an increase of approximately 20 percentage points year-over-year and 17 percentage points sequentially from Q1 2025.

Segment Analysis

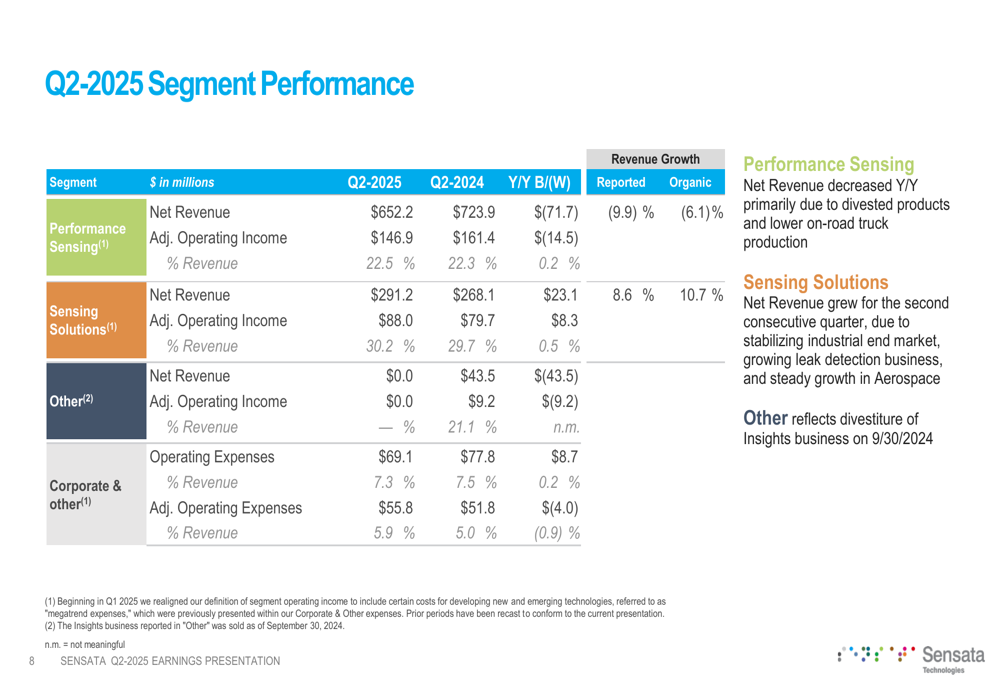

Sensata’s segment performance revealed divergent trends between its two main business units. The detailed breakdown shows the relative performance of each segment:

Performance Sensing, which represents approximately 69% of total revenue, saw a year-over-year revenue decline to $652.2 million from $723.9 million in Q2 2024. Despite this decrease, the segment’s adjusted operating margin improved slightly to 22.5% from 22.3% a year earlier, demonstrating effective cost management.

Sensing Solutions delivered a more positive story, with revenue growing to $291.2 million from $268.1 million in Q2 2024, marking the second consecutive quarter of year-over-year growth. The segment’s adjusted operating margin also improved to 30.2% from 29.7%.

The "Other" category, which contributed $43.5 million in Q2 2024, is now at zero following the divestiture of the Insights business on September 30, 2024. This strategic portfolio reshaping explains a portion of the overall revenue decline.

Capital Allocation and Balance Sheet

Sensata maintained a balanced approach to capital allocation during the quarter, as illustrated in the following summary:

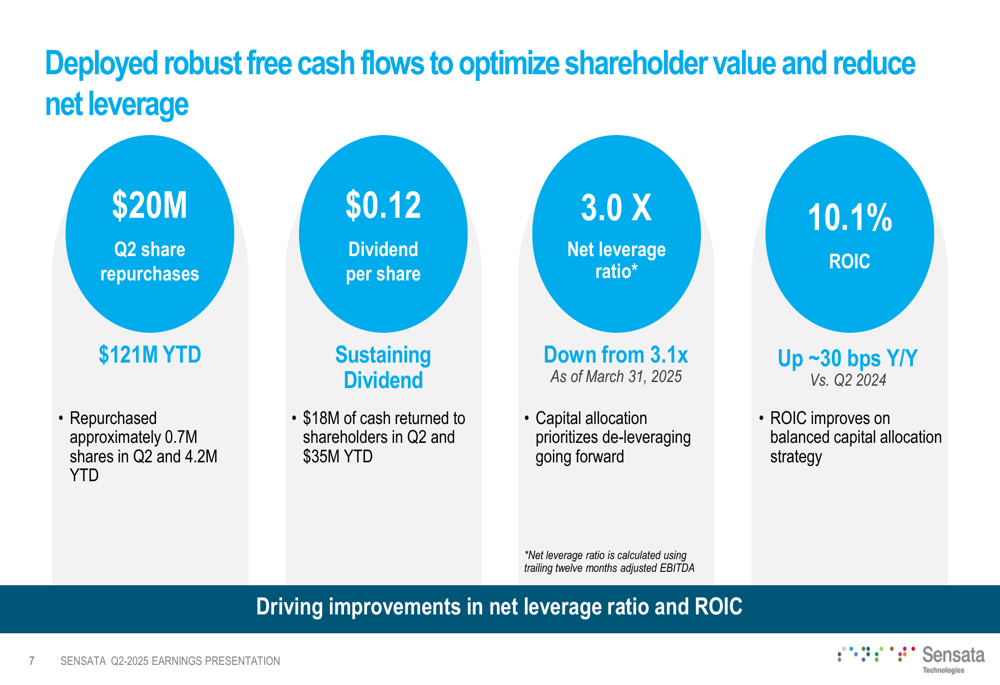

The company repurchased $20 million worth of shares in Q2 (approximately 0.7 million shares), bringing the year-to-date total to $121 million (4.2 million shares). Sensata also continued its quarterly dividend of $0.12 per share, returning $18 million to shareholders in Q2.

The net leverage ratio improved to 3.0x, down from 3.1x as of March 31, 2025, with the company stating that capital allocation will prioritize de-leveraging going forward. Return on invested capital (ROIC) reached 10.1%, up approximately 30 basis points year-over-year.

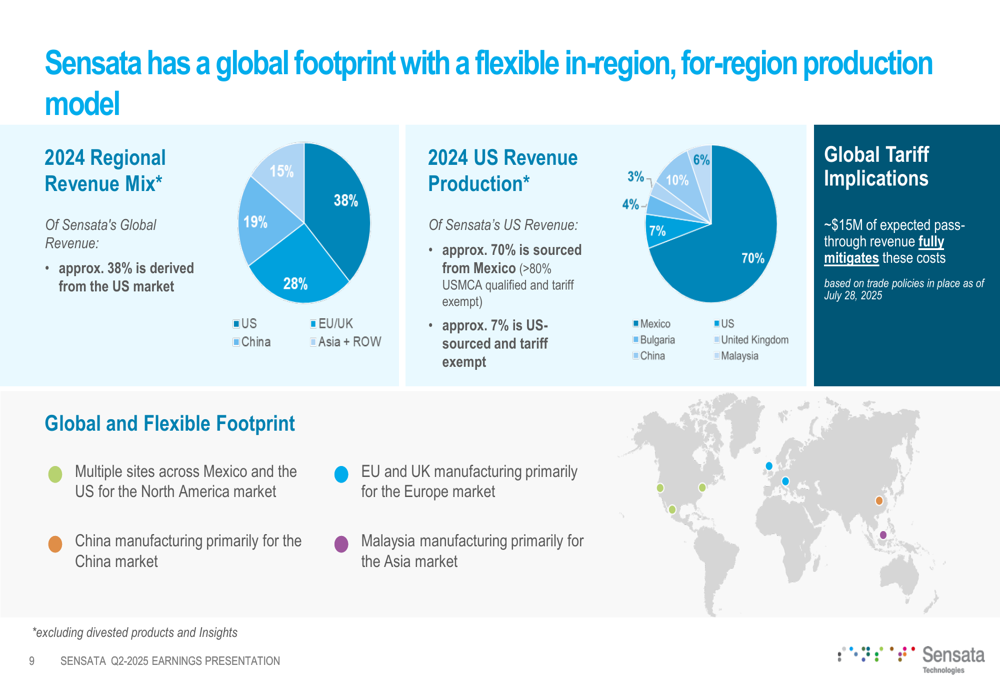

Sensata’s global manufacturing footprint provides strategic advantages in managing tariff impacts, as shown in the following breakdown:

Approximately 70% of US revenue is sourced from Mexico, which is USMCA qualified and tariff exempt, while another 7% is US-sourced. The company expects approximately $15 million of pass-through revenue to fully mitigate tariff costs based on trade policies in place as of July 28, 2025.

Guidance and Outlook

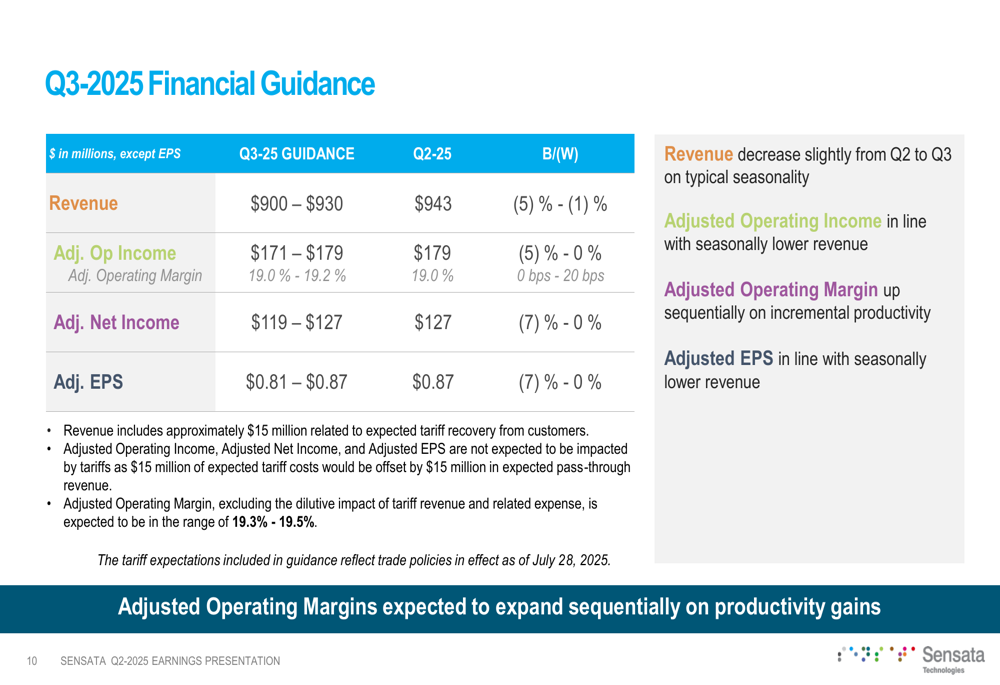

Looking ahead to Q3 2025, Sensata provided the following guidance:

The company expects Q3 2025 revenue between $900-$930 million, slightly below Q2 levels due to typical seasonality. Adjusted operating income is projected at $171-$179 million, with adjusted operating margins of 19.0%-19.2%, representing sequential margin expansion on incremental productivity.

Adjusted EPS guidance of $0.81-$0.87 aligns with the seasonally lower revenue expectations. The guidance includes approximately $15 million related to expected tariff recovery from customers.

This outlook builds on momentum from Q1 2025, when the company began showing signs of operational improvement. The Q1 earnings report had highlighted revenue of $911 million and adjusted EPS of $0.78, indicating that Q2 results represent continued progress in the company’s operational efficiency initiatives.

Sensata’s focus on its "back-to-basics" approach appears to be yielding tangible results, particularly in free cash flow generation and margin stability despite revenue challenges. With a continued emphasis on operational efficiency and strategic portfolio management, the company is positioning itself to navigate ongoing market uncertainties while maintaining financial discipline.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.