Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Service Properties Trust (NASDAQ:SVC) presented its fourth quarter 2024 financial results on February 26, 2025, highlighting the company’s ongoing strategic transformation toward becoming a net lease-focused REIT. The presentation revealed widening losses alongside significant portfolio restructuring efforts, including the sale of multiple hotel properties and a continued focus on its net lease assets.

SVC’s stock has struggled in recent months, trading near $2.53 as of August 15, 2025, well below its 52-week high of $5.00 and closer to its 52-week low of $1.71. This performance reflects ongoing investor concerns about the company’s financial health and strategic direction.

Quarterly Performance Highlights

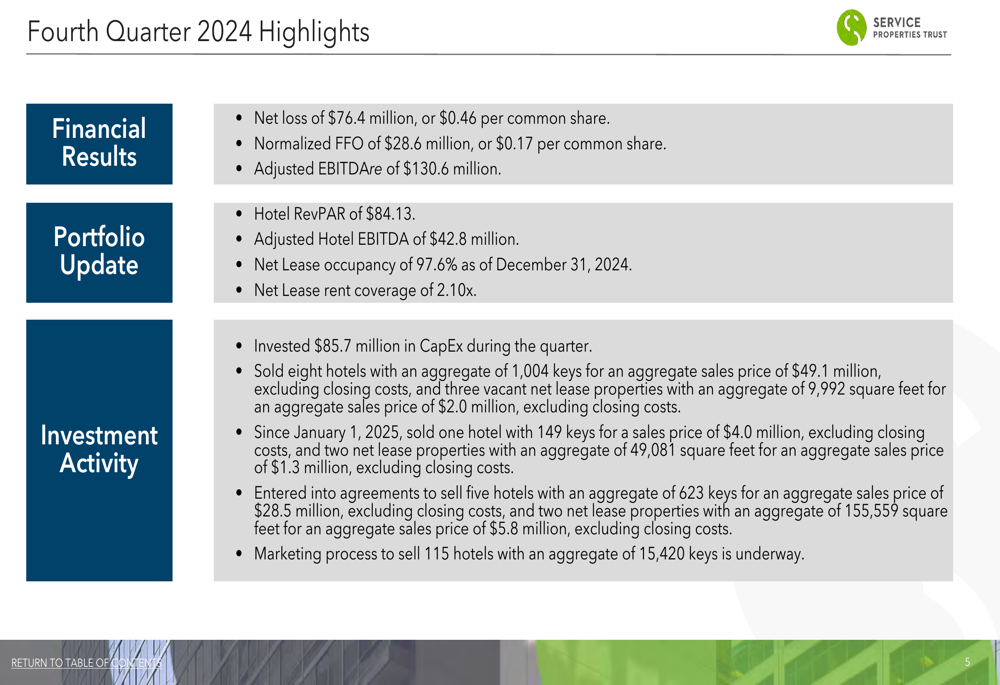

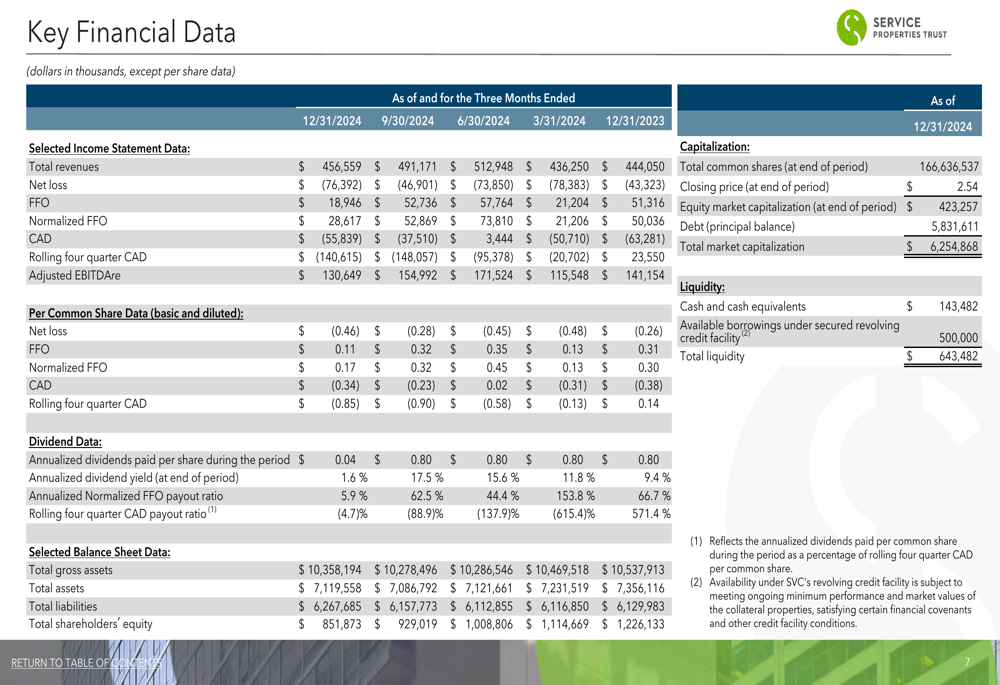

Service Properties Trust reported a net loss of $76.4 million ($0.46 per share) for Q4 2024, compared to a net loss of $43.3 million ($0.26 per share) in the same period of 2023. For the full year 2024, the net loss widened significantly to $275.5 million, compared to $32.8 million in 2023.

Despite these challenges, the company highlighted some positive operational metrics, including comparable hotel RevPAR growth of 4.2% and a strong net lease portfolio occupancy rate of 97.6%.

As shown in the following comprehensive overview of the quarter’s key metrics:

The company reported Normalized FFO (Funds From Operations) of $28.6 million ($0.17 per share) and Adjusted EBITDAre of $130.6 million for the fourth quarter. Hotel RevPAR came in at $84.13, while the company’s net lease rent coverage ratio stood at 2.10x.

A more detailed look at SVC’s financial performance over recent quarters shows the progression of key metrics:

Strategic Portfolio Transformation

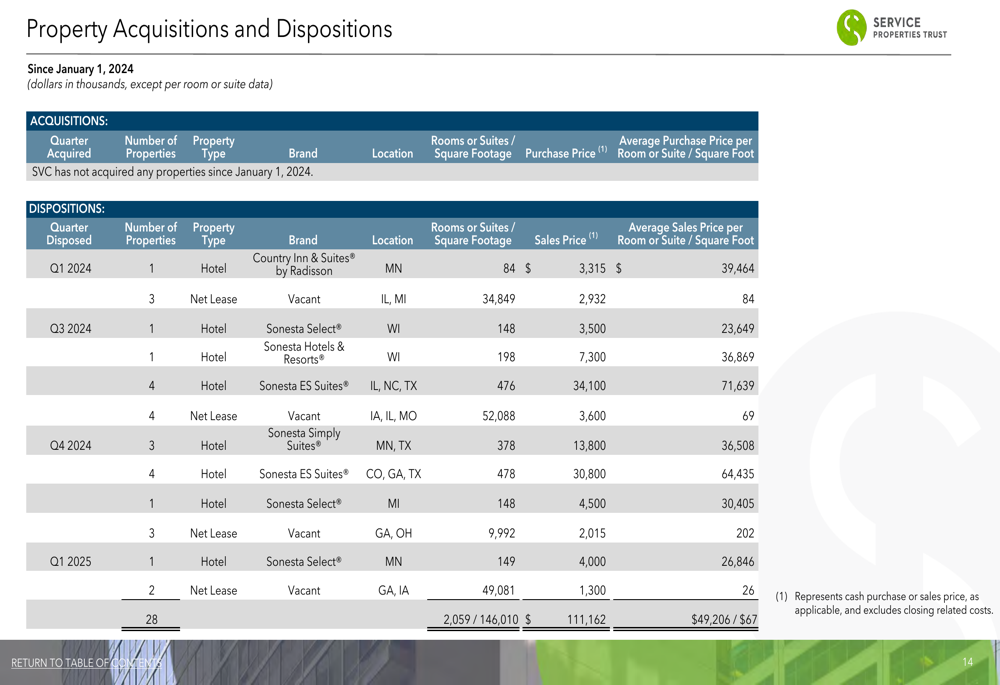

The most significant aspect of SVC’s strategy is its ongoing portfolio transformation. The company is actively reducing its hotel exposure while focusing on its net lease properties. During Q4 2024, SVC completed the sale of eight hotels for nearly $50 million and had five additional hotels under agreement to be sold for $28.5 million.

Most notably, the company disclosed that it has a marketing process underway to sell 115 hotels representing 15,420 keys, signaling an acceleration of its strategic shift.

The following chart details the company’s recent property dispositions:

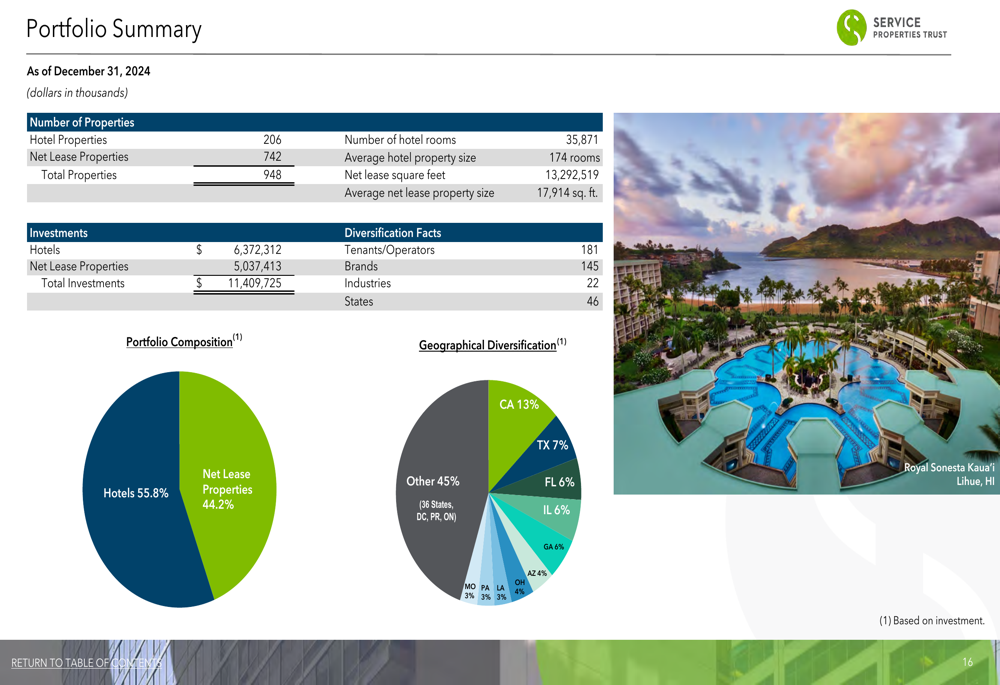

As of December 31, 2024, SVC’s portfolio consisted of 206 hotel properties and 742 net lease properties, with hotels representing 55.8% of the portfolio and net lease properties accounting for 44.2%. This balance is expected to shift significantly as the company executes its disposition strategy.

The portfolio summary provides a clear picture of the company’s current asset mix:

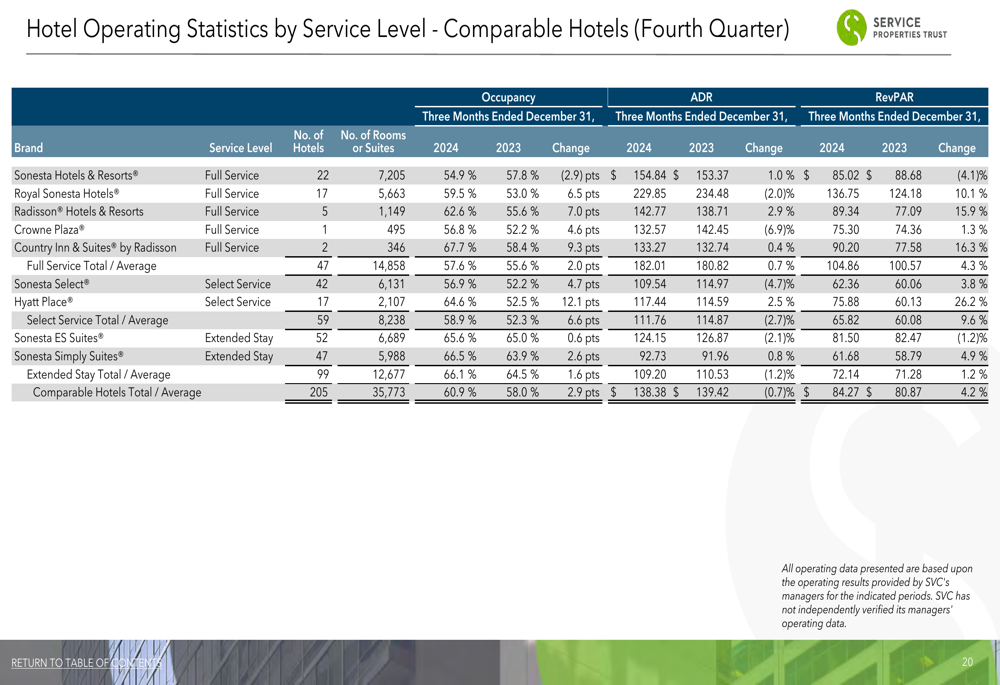

Within the hotel segment, SVC’s portfolio is diversified across several brands, with Sonesta ES Suites representing the largest portion at 25.1% of total hotels and 18.4% of total rooms. The company’s hotel operating statistics showed varying performance across brands:

On the net lease side, SVC’s portfolio is heavily concentrated in the travel center industry, with TravelCenters of America Inc. being the dominant tenant, accounting for 175 properties and $3.27 billion in investment.

Debt and Financial Position

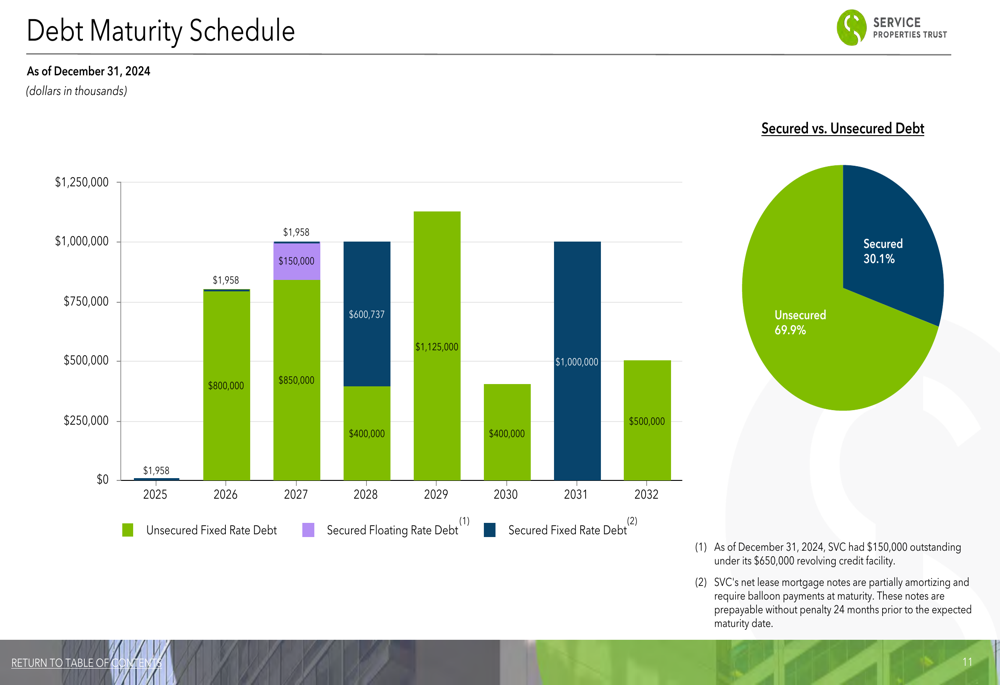

SVC’s financial position remains challenging, with total debt of $5.83 billion as of December 31, 2024, carrying a weighted average interest rate of 6.385%. The company’s debt maturity schedule shows significant obligations coming due in the next few years:

The company’s leverage metrics indicate high debt levels, with net debt to rolling four-quarter Adjusted EBITDAre at 9.9x as of December 31, 2024. This high leverage ratio suggests potential financial strain, which is consistent with the company’s strategic focus on asset sales.

SVC reported total liquidity of $643.5 million, including $143.5 million in cash and $500 million available under its secured revolving credit facility. This liquidity position provides some financial flexibility as the company executes its transformation strategy.

Forward-Looking Statements

Looking ahead, SVC’s presentation suggests a continued focus on its strategic transformation toward becoming a net lease REIT. The earnings article from Q2 2025 confirms this direction, with management indicating that "pro forma for our expected hotel sales, net lease assets are projected to account for over 70% of SVC’s pro forma Q2 adjusted EBITDAre."

However, subsequent financial results from Q2 2025 indicate that challenges have persisted, with the company reporting a larger-than-expected loss of $0.23 per share. The stock’s reaction to these results—a 5.62% drop in after-hours trading—suggests ongoing investor concerns about SVC’s transformation strategy and financial health.

Management has indicated plans to reduce capital expenditures significantly in 2026 to $150 million, down from $250 million in 2025, as it continues its hotel disposition strategy and focuses on net lease acquisitions. This capital allocation shift aligns with the company’s broader strategic direction.

The company’s debt management remains a critical focus area, with executives noting they are "evaluating different strategies to improve our credit metrics" according to the Q2 2025 earnings call. With debt covenant challenges and a high leverage ratio, addressing the debt situation will likely remain a priority for SVC in the coming quarters as it continues its strategic transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.