Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

ServiceNow Inc (NYSE:NOW) released its first quarter 2025 results on April 23, showing continued growth and improved profitability as the company positions itself as "the AI Platform for Business Transformation." The market responded positively to the results, with ServiceNow shares rising 5.98% during regular trading hours and an additional 8.88% in after-hours trading.

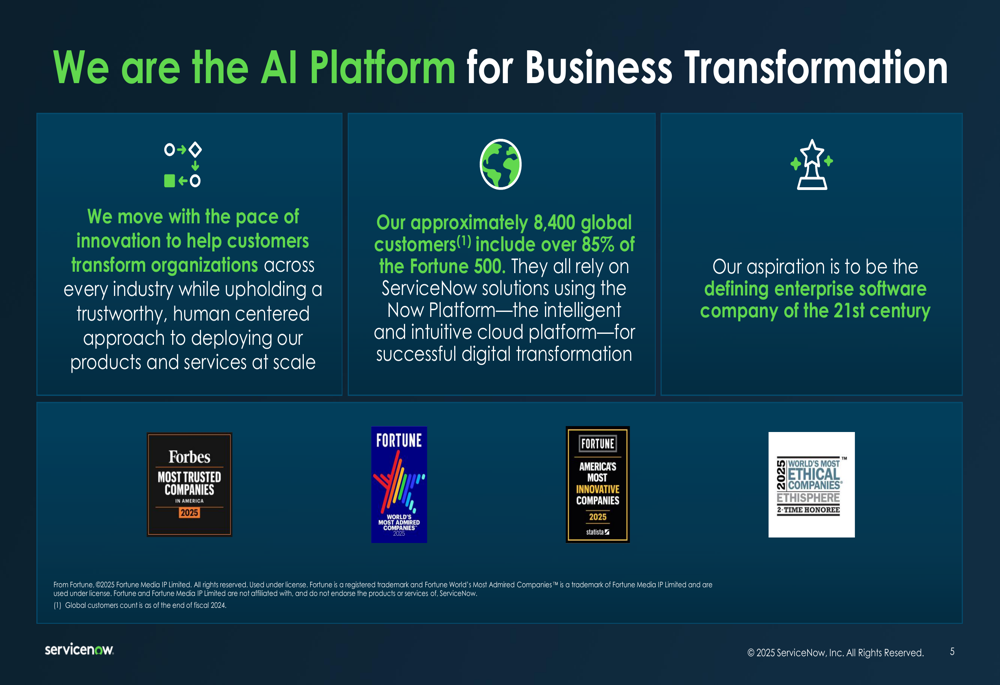

The company maintained its strong position in the enterprise software market, serving approximately 8,400 global customers including over 85% of the Fortune 500. ServiceNow continues to expand its product offerings across four main workflow categories while leveraging AI capabilities to drive business value.

Quarterly Performance Highlights

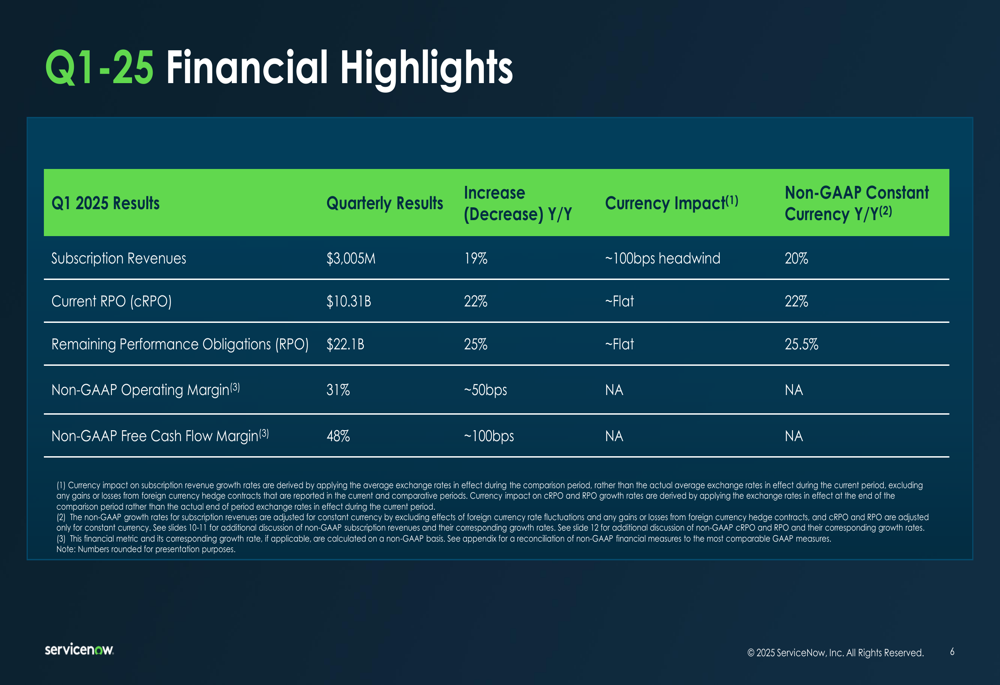

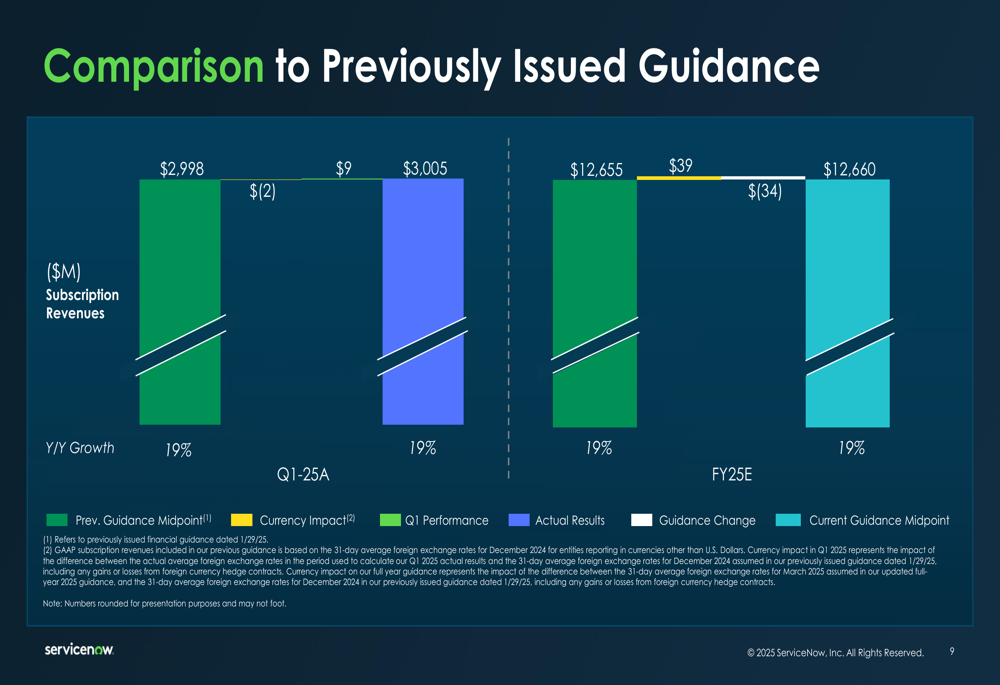

ServiceNow reported solid financial results for Q1 2025, with subscription revenues reaching $3,005 million, representing a 19% year-over-year increase (20% in constant currency). The company’s current remaining performance obligations (cRPO) grew 22% year-over-year to $10.31 billion, while total RPO increased 25% (25.5% in constant currency) to $22.1 billion.

As shown in the following financial highlights chart from the presentation:

The company also demonstrated improved profitability, with non-GAAP operating margin reaching 31%, up approximately 50 basis points year-over-year. Free cash flow margin showed even stronger improvement, increasing by approximately 100 basis points to 48%.

This performance translated into substantial bottom-line growth, with non-GAAP net income increasing from $707 million in Q1 2024 to $846 million in Q1 2025, and non-GAAP diluted earnings per share growing from $3.41 to $4.04 over the same period.

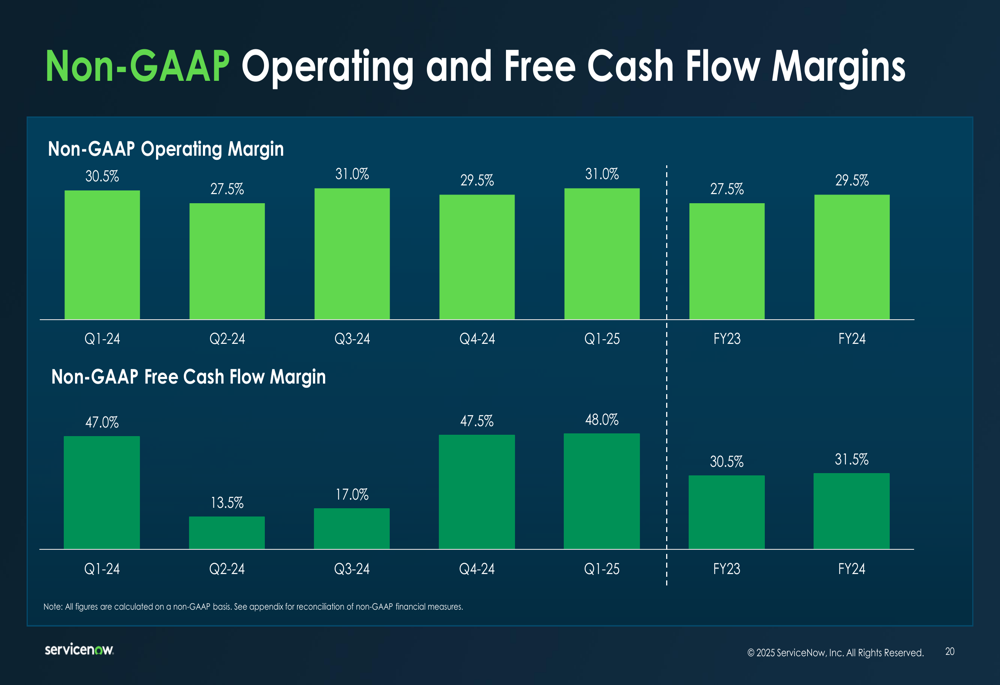

The company’s operating and free cash flow margins have shown consistent improvement over recent quarters, as illustrated in this chart:

Customer Growth and Business Mix

ServiceNow continues to expand its customer relationships, with the number of customers having annual contract values (ACV) exceeding $5 million growing to 508 in Q1 2025, up from 425 in Q1 2024. The average ACV for these large customers also increased from $13.2 million to $14.2 million over the same period.

The company maintained its impressive 98% renewal rate for the fifth consecutive quarter, demonstrating strong customer satisfaction and the mission-critical nature of its offerings.

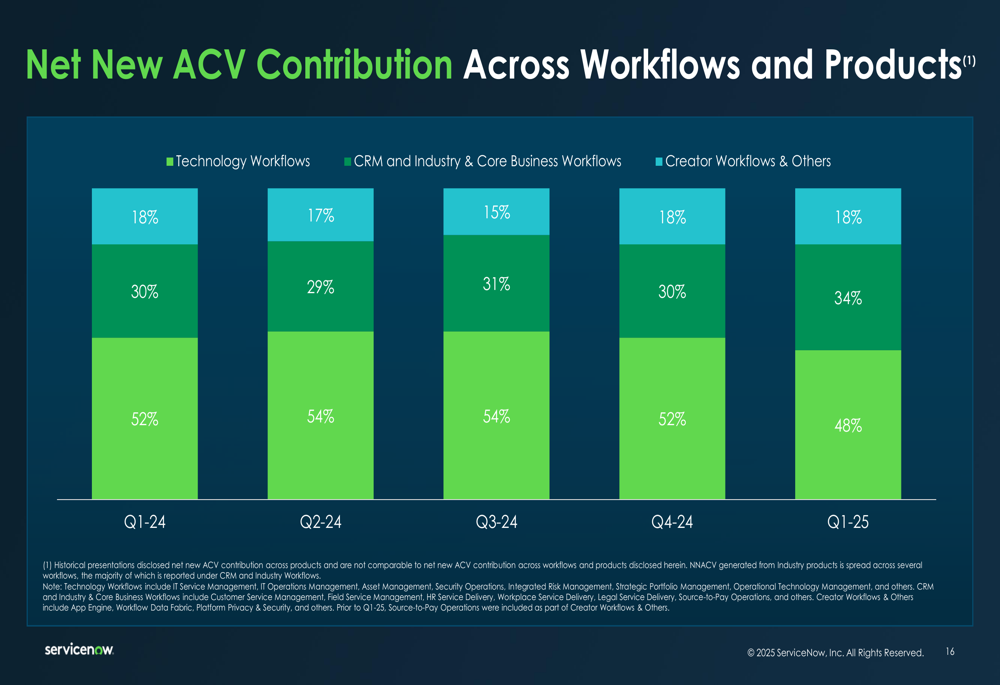

An interesting shift is occurring in ServiceNow’s business mix, with Technology Workflows contributing 48% of net new ACV in Q1 2025 (down from 52% in Q1 2024), while CRM, Industry, and Core Business Workflows increased their contribution to 34% (up from 30%). This suggests the company is successfully expanding beyond its IT service management roots into broader enterprise workflows.

This business mix evolution is clearly visible in the following chart:

The company’s platform strategy centers around four main workflow categories, as illustrated in this slide:

Forward Guidance

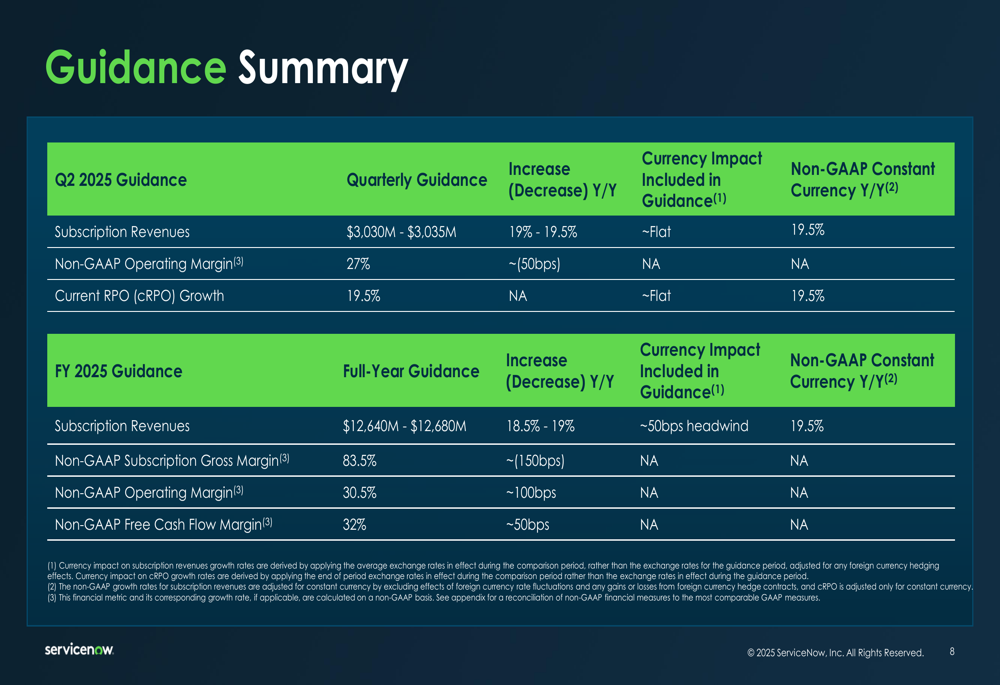

Looking ahead, ServiceNow provided guidance for Q2 2025 and updated its full-year outlook. For Q2, the company expects subscription revenues of $3,030-$3,035 million, representing 19-19.5% year-over-year growth, with a non-GAAP operating margin of 27% (down approximately 50 basis points).

For the full year 2025, ServiceNow slightly raised its subscription revenue guidance to $12,640-$12,680 million (up 18.5-19% year-over-year, or 19.5% in constant currency). The company expects non-GAAP subscription gross margin of 83.5% (down approximately 150 basis points), non-GAAP operating margin of 30.5% (down approximately 100 basis points), and non-GAAP free cash flow margin of 32% (down approximately 50 basis points).

The guidance summary is presented in detail here:

ServiceNow noted that while the U.S. dollar weakened during Q1, providing a currency tailwind, and the company exceeded the high end of its subscription revenue guidance for the quarter, its updated guidance only reflects a portion of these benefits. This cautious approach allows the company to factor in potential risks related to the current geopolitical environment.

The comparison between actual results, previous guidance, and updated guidance is illustrated in this chart:

Strategic Positioning

ServiceNow continues to position itself as "the AI Platform for Business Transformation," emphasizing how its platform connects AI, data, and workflows to maximize the value of existing technology investments, cut costs, and improve core business processes.

The company’s strategic vision is captured in this slide:

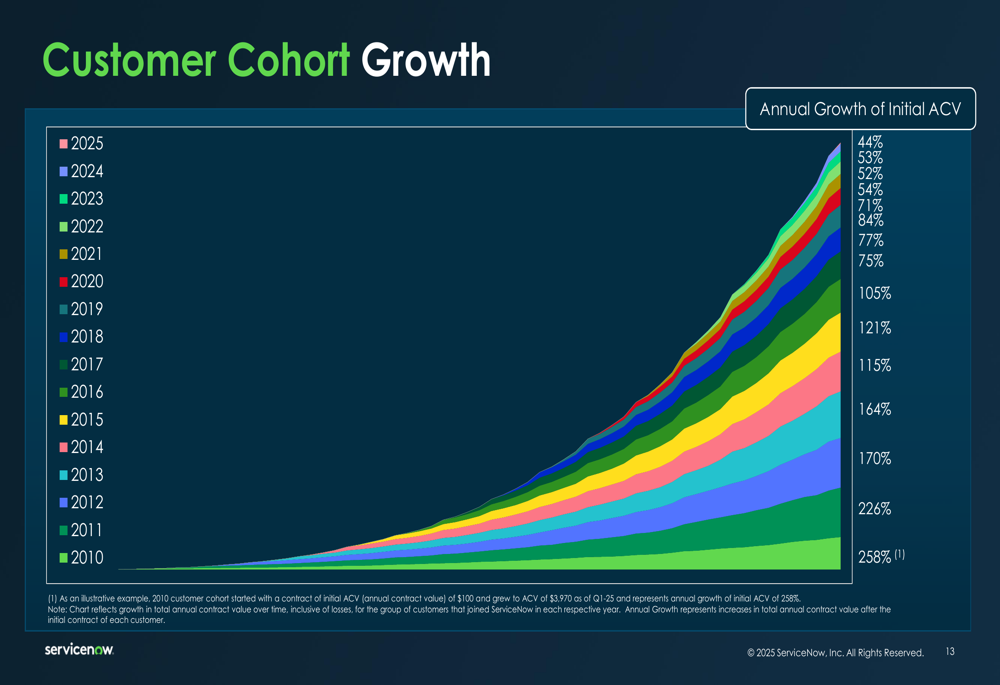

ServiceNow’s long-term growth strategy is further validated by the strong performance of its customer cohorts over time. Customers that joined in earlier years continue to significantly expand their ServiceNow investments, with the 2010 cohort growing its initial annual contract value by 258% as of Q1 2025.

This customer cohort growth pattern demonstrates the platform’s expanding value proposition:

ServiceNow’s geographic revenue distribution remained relatively stable, with North America accounting for 64% of GAAP revenues in Q1 2025, EMEA contributing 25%, and APAC and other regions representing 11%. This global footprint provides the company with diversified growth opportunities while maintaining a strong base in its core North American market.

As ServiceNow continues its journey toward becoming "the defining enterprise software company of the 21st century," its Q1 2025 results demonstrate solid execution against this ambitious vision, with steady growth, improving profitability, and expanding customer relationships across its workflow portfolio.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.