Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

ServiceNow (NYSE:NOW) released its second quarter 2025 investor presentation on July 23, showcasing continued strong performance while positioning itself as "the AI platform for business transformation." The enterprise software company reported solid growth across key metrics while raising its full-year guidance, despite flagging some near-term headwinds expected in the third quarter.

ServiceNow continues to expand its customer base, now serving approximately 8,400 global customers including over 85% of the Fortune 500, as it pursues its stated aspiration to become "the defining enterprise software company of the 21st century."

As shown in the following slide, ServiceNow positions its AI platform across four key workflow areas, targeting comprehensive enterprise transformation:

Quarterly Performance Highlights

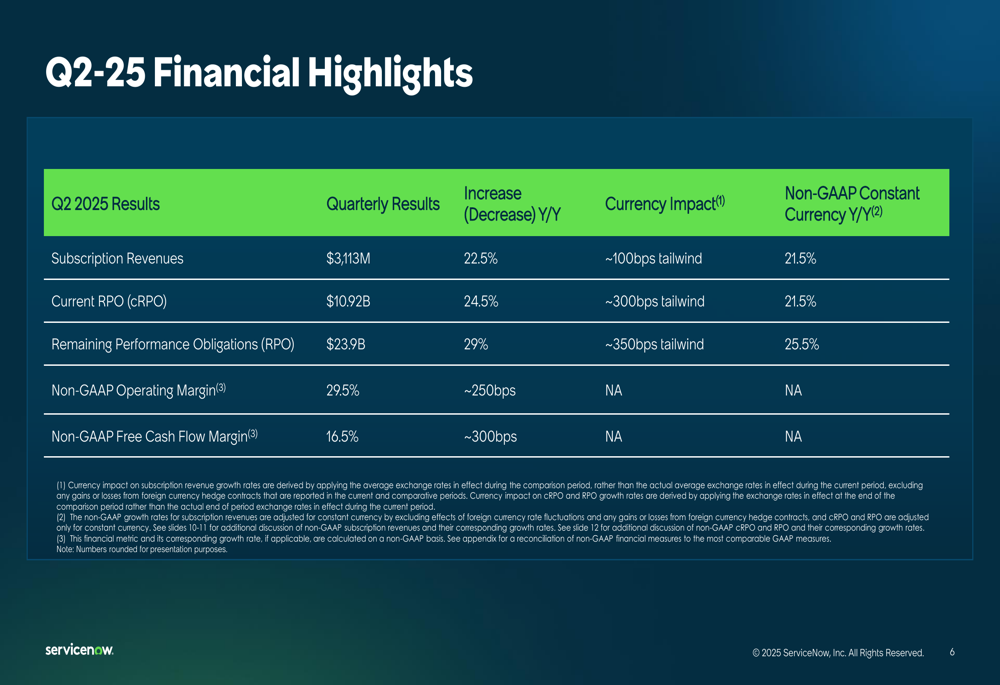

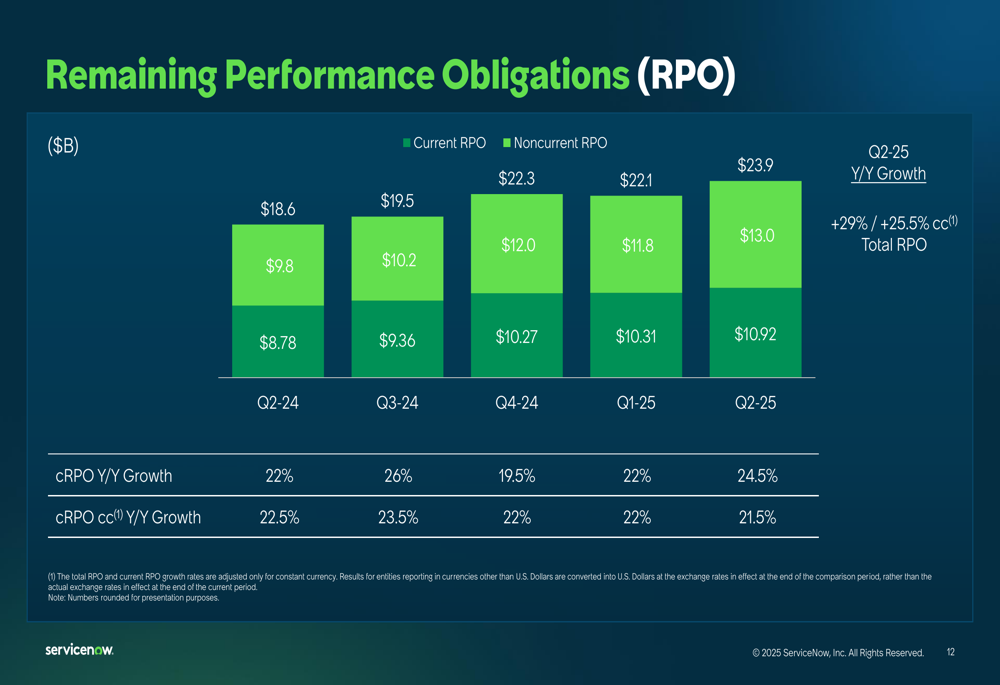

ServiceNow delivered strong financial results in Q2 2025, with subscription revenues reaching $3.11 billion, representing a 22.5% year-over-year increase, or 21.5% in constant currency. The company’s current remaining performance obligations (cRPO) grew to $10.92 billion, up 24.5% year-over-year, while total RPO expanded to $23.9 billion, a 29% increase from the prior year.

The following financial highlights table details the company’s Q2 2025 performance:

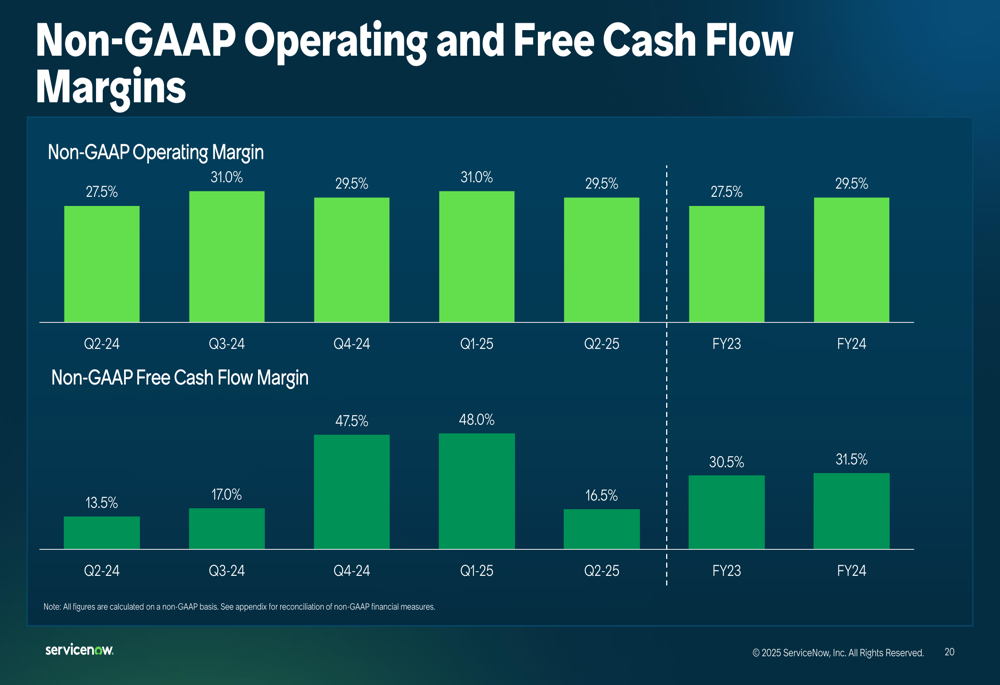

Profitability metrics also showed improvement, with non-GAAP operating margin reaching 29.5%, an increase of approximately 250 basis points year-over-year. Non-GAAP free cash flow margin stood at 16.5%, up about 300 basis points from the prior year.

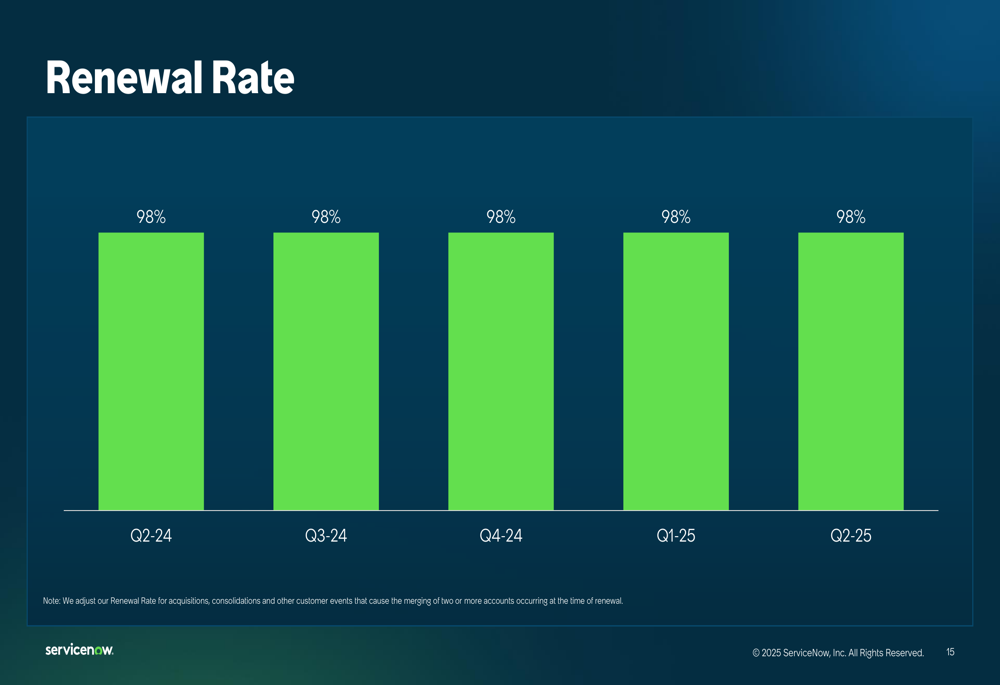

The company maintained its impressive customer renewal rate at 98% for the fifth consecutive quarter, demonstrating strong customer satisfaction and product stickiness:

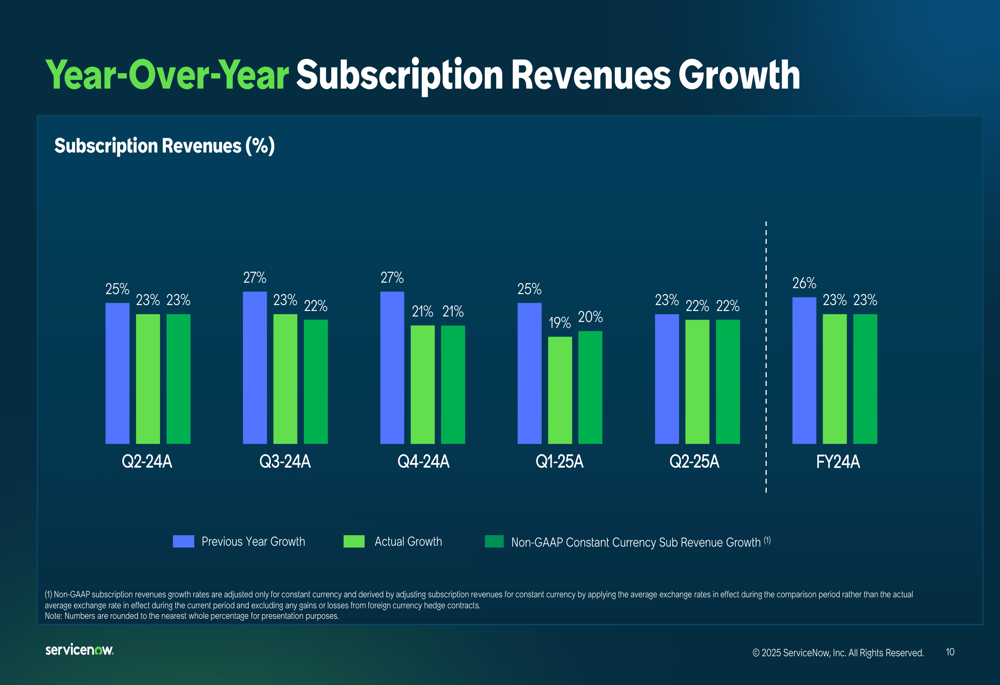

ServiceNow’s revenue growth has remained consistent in the low-to-mid 20% range over recent quarters, as illustrated in the following chart:

Guidance and Forward-Looking Statements

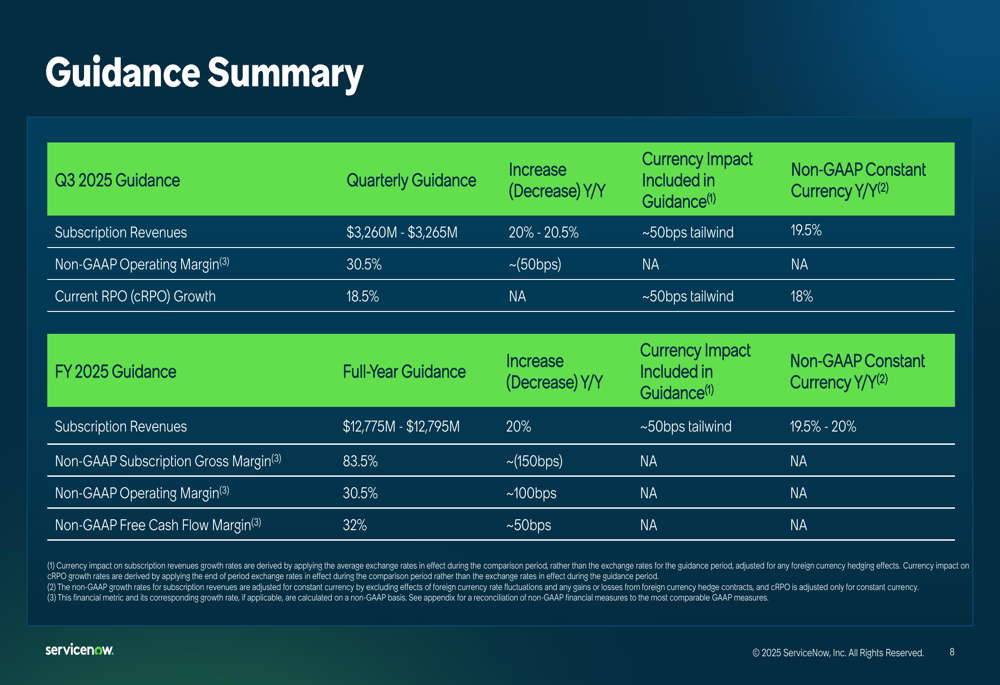

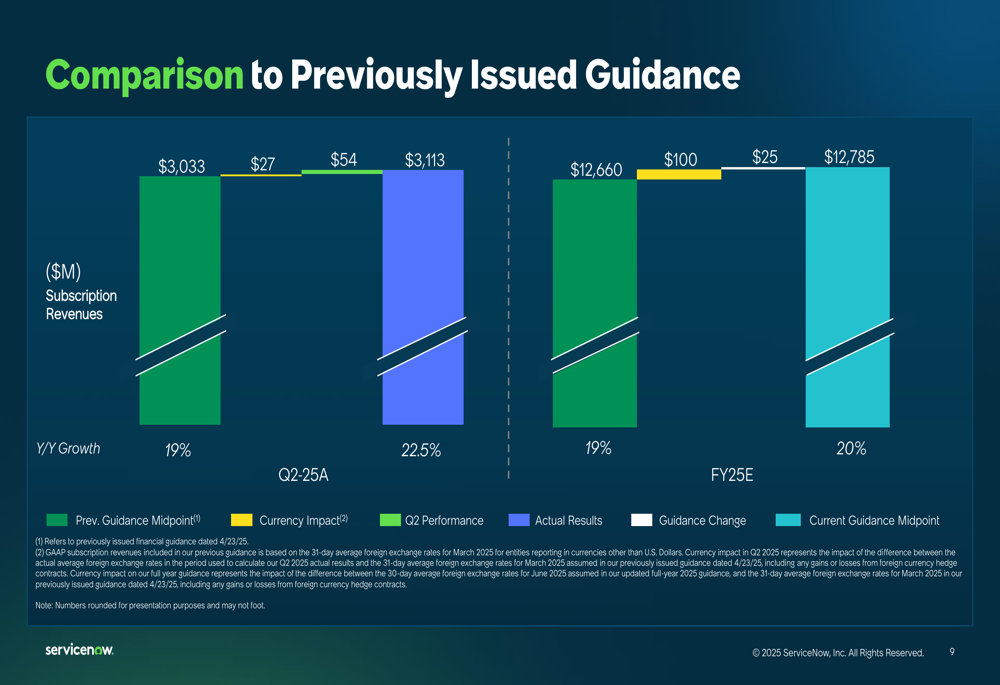

While raising its full-year 2025 guidance, ServiceNow cautioned investors about potential headwinds in the third quarter. The company now expects fiscal year 2025 subscription revenues between $12.78 billion and $12.80 billion, representing 20% year-over-year growth, up from its previous guidance of $12.66 billion.

For Q3 2025, ServiceNow projects subscription revenues between $3.26 billion and $3.27 billion, reflecting 20-20.5% year-over-year growth. However, the company expects cRPO growth to slow to 18.5% in Q3, before rebounding in Q4.

The complete guidance summary is presented in the following slide:

ServiceNow attributed the expected Q3 deceleration to two specific factors: a larger-than-average customer cohort scheduled to renew in Q4 2025, creating approximately 2 percentage points of headwind to cRPO growth in Q3, and U.S. federal agencies navigating budget tightening and evolving mission demands.

The company’s guidance revision from previous projections is visualized below:

Business Segment Performance

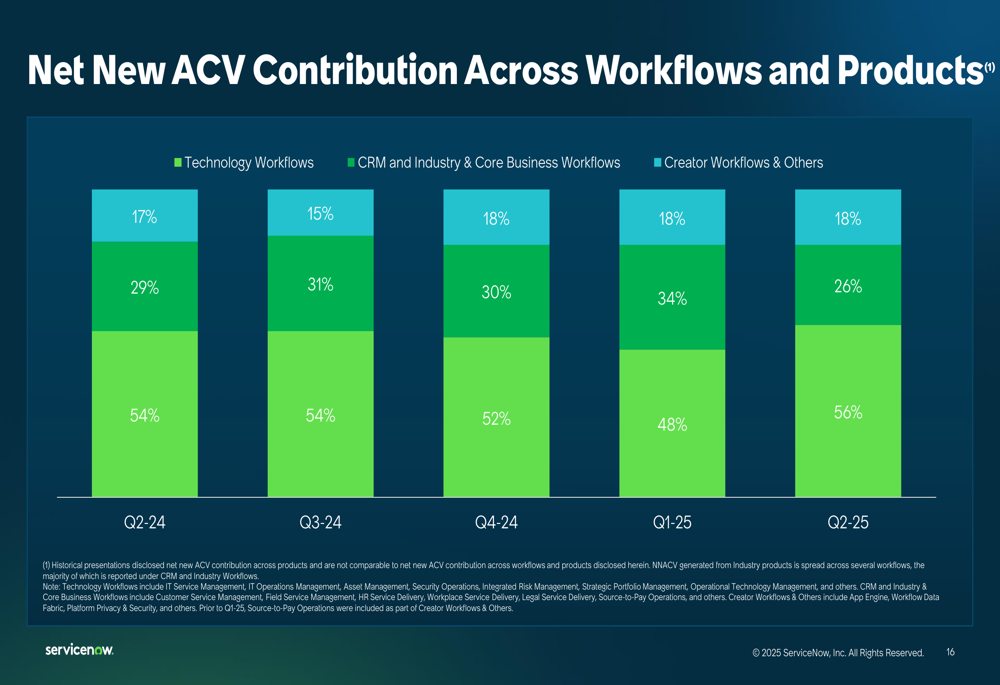

ServiceNow’s business continues to be driven by its Technology Workflows segment, which contributed the largest portion of net new annual contract value (ACV) in Q2 2025. However, the company is seeing growing contributions from its CRM, Industry & Core Business Workflows, as well as Creator Workflows segments.

The following chart breaks down the net new ACV contribution across ServiceNow’s workflow categories:

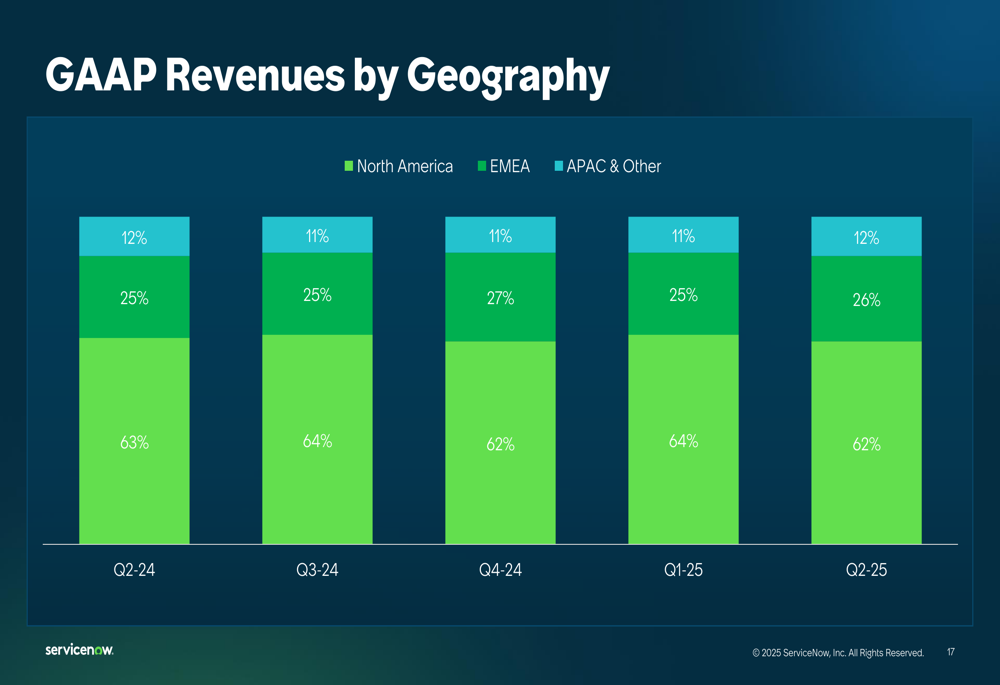

From a geographic perspective, North America remains ServiceNow’s largest market, accounting for approximately 62-64% of total revenues, followed by EMEA at 25-27% and APAC & Other regions at 11-12%. This distribution has remained relatively stable over recent quarters:

Financial Health and Margins

ServiceNow continues to demonstrate strong financial health with expanding margins and growing profitability. The company’s non-GAAP subscription gross margin remains robust at around 83.5% for fiscal year 2025 guidance.

The company’s remaining performance obligations (RPO), a key indicator of future revenue, show healthy growth across both current and non-current components:

ServiceNow’s operating margin and free cash flow margin have shown different trajectories, with operating margin steadily improving while free cash flow margin has fluctuated significantly:

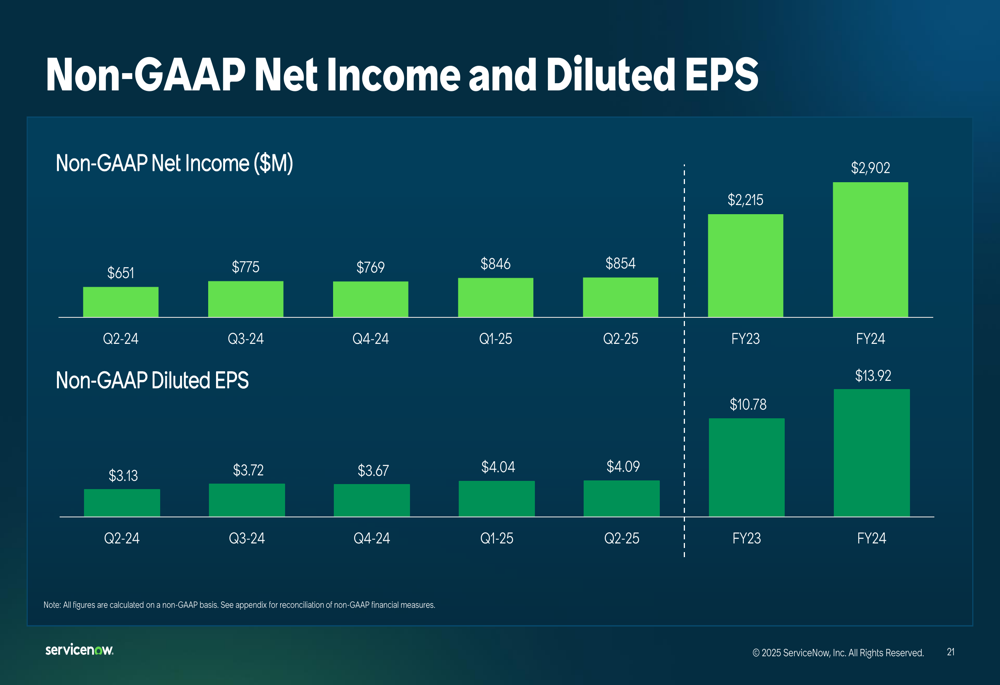

The company’s non-GAAP net income and diluted earnings per share have maintained an upward trend, reflecting improved operational efficiency:

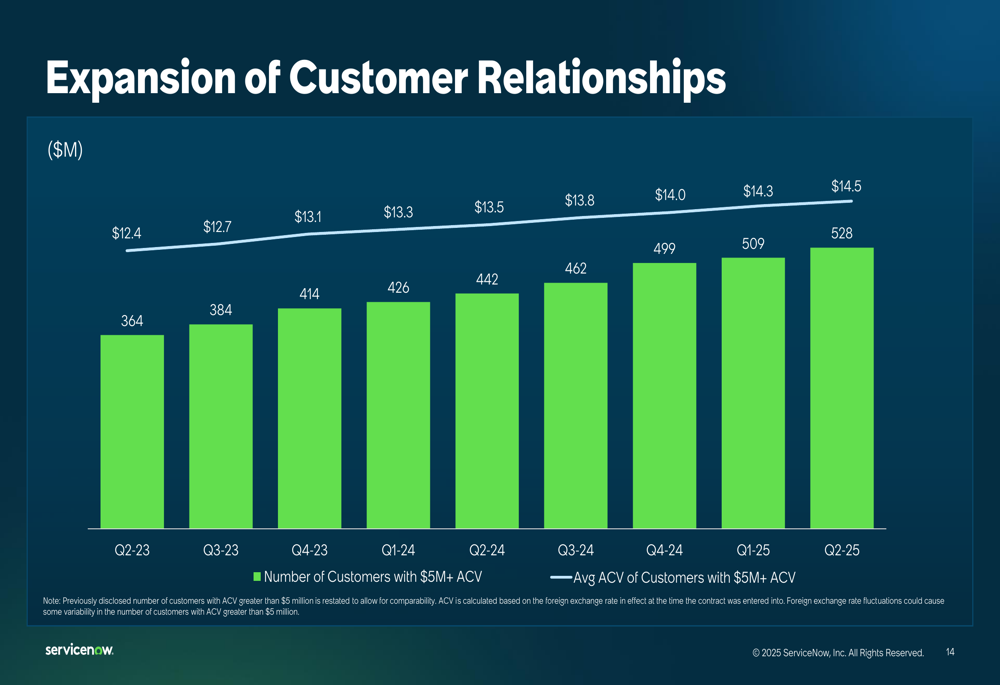

ServiceNow’s continued investment in customer relationships is yielding results, with an increasing number of customers exceeding $5 million in annual contract value (ACV) and growing average ACV among these large customers:

As ServiceNow navigates temporary headwinds in the coming quarter, its strong Q2 performance and raised full-year guidance suggest management remains confident in the company’s long-term growth trajectory and its positioning as a leading enterprise AI platform provider.

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.