Procore stock price target raised to $90 from Goldman Sachs on stabilizing growth

Introduction & Market Context

Seven & i Holdings Co., Ltd. (TYO:3382) presented its second quarter fiscal year 2025 results on October 9, 2025, revealing significant profit growth despite revenue challenges. The Japanese retail conglomerate, which operates 7-Eleven stores globally, saw its stock decline 3.58% following the announcement as investors reacted to revenue figures that fell short of expectations despite impressive bottom-line performance.

The company’s presentation highlighted substantial year-over-year profit improvements amid ongoing business transformation initiatives designed to enhance profitability in both domestic and international operations. Seven & i continues to navigate a challenging Japanese retail environment characterized by inflation pressures and changing consumer behaviors.

Quarterly Performance Highlights

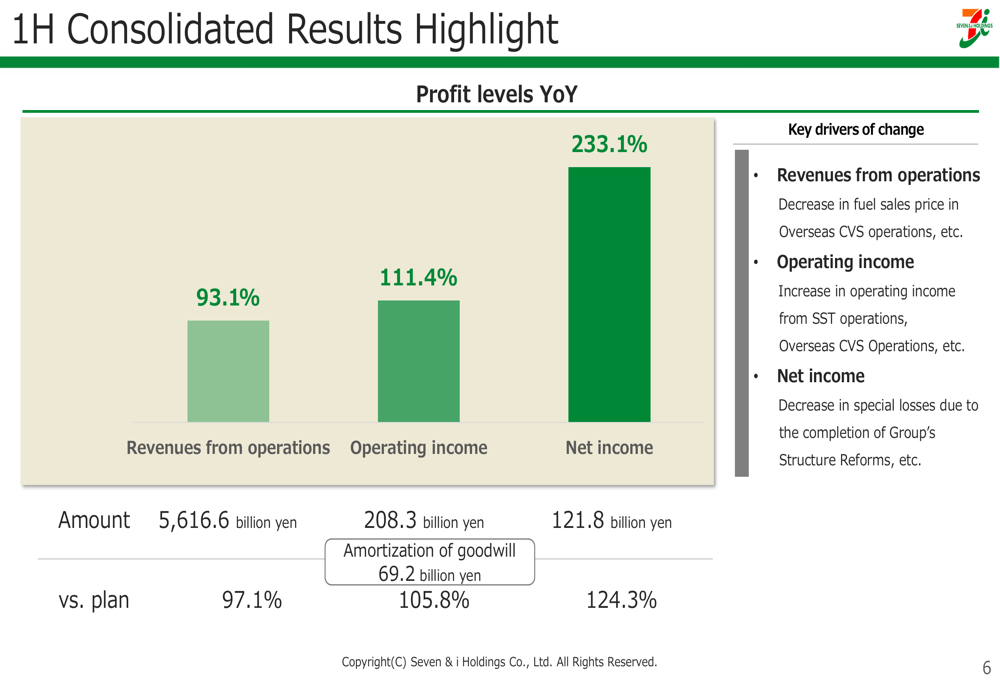

Seven & i Holdings reported operating income of 208.3 billion yen for the first half of FY2025, representing 111.4% year-over-year growth and exceeding the company’s plan by 5.8%. Most notably, net income attributable to owners surged to 121.8 billion yen, a remarkable 233.1% increase compared to the same period last year.

As shown in the following chart detailing profit performance year-over-year:

This impressive bottom-line growth came despite revenues from operations declining to 5,616.6 billion yen, representing 93.1% of the previous year’s figure. The company attributed this revenue decrease primarily to lower fuel sales prices in overseas convenience store operations.

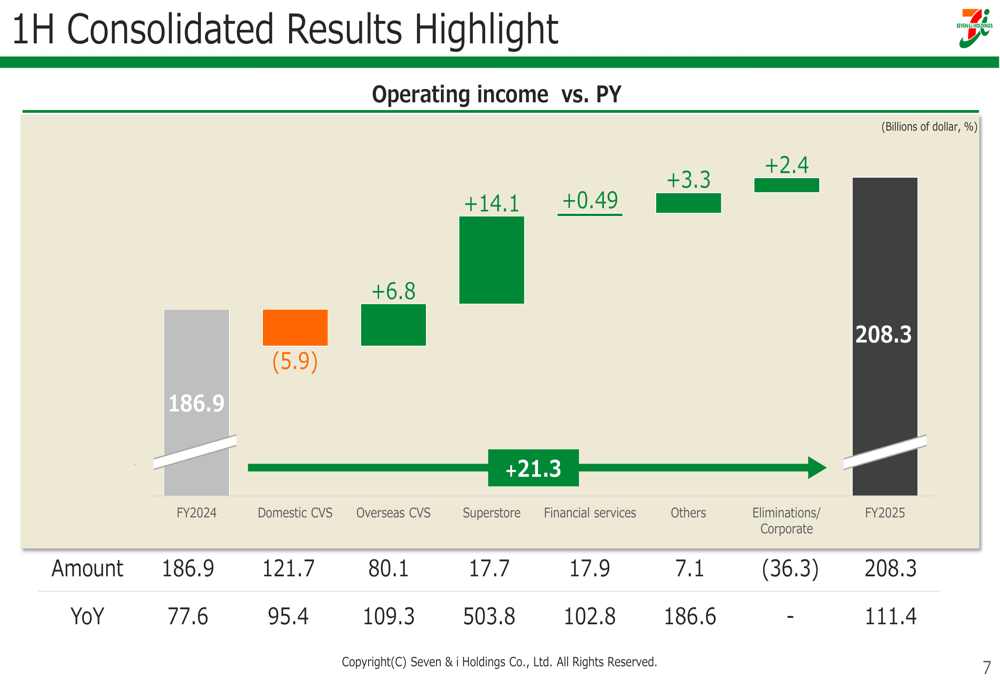

The operating income improvement was driven by multiple segments, with particularly strong contributions from superstore operations and overseas convenience stores, as illustrated in this breakdown:

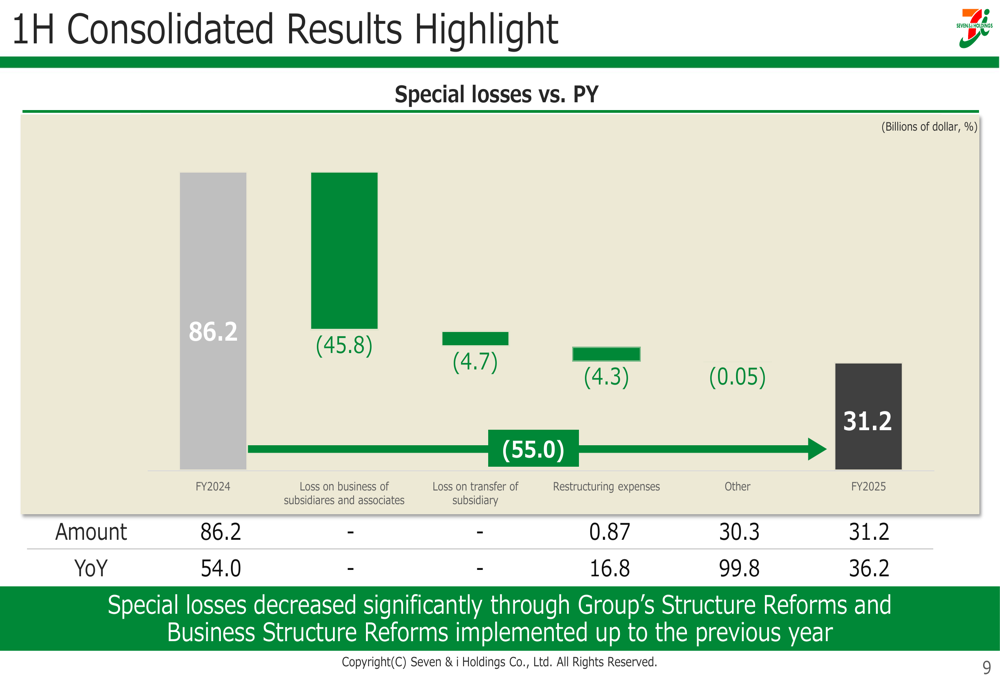

A significant factor in the company’s improved profitability was the substantial reduction in special losses, which decreased from 86.2 billion yen in FY2024 to 31.2 billion yen in FY2025. This reduction primarily resulted from the completion of the Group’s Structure Reforms initiatives.

Segment Performance Analysis

Seven-Eleven Japan (SEJ) reported operating income of 121.4 billion yen, down from 127.6 billion yen in the previous year. Despite this decline, existing store sales showed modest growth of 0.8%, with customer traffic increasing 0.5% in the second quarter. The company’s merchandise gross profit margin decreased slightly to 31.8%, down 0.3 percentage points year-over-year.

Seven-Eleven Inc. (SEI), the company’s North American operation, delivered stronger results with operating income increasing from 858 million dollars to 905 million dollars. However, same-store sales declined 0.9% compared to the previous year, though merchandise gross profit margin improved by 0.2 percentage points to 33.2%.

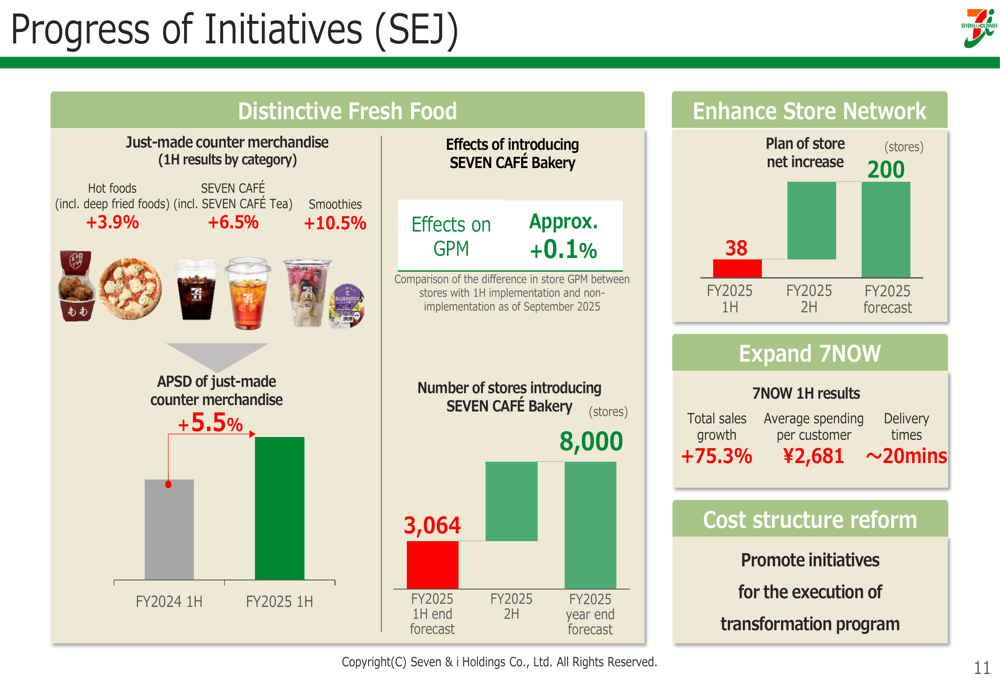

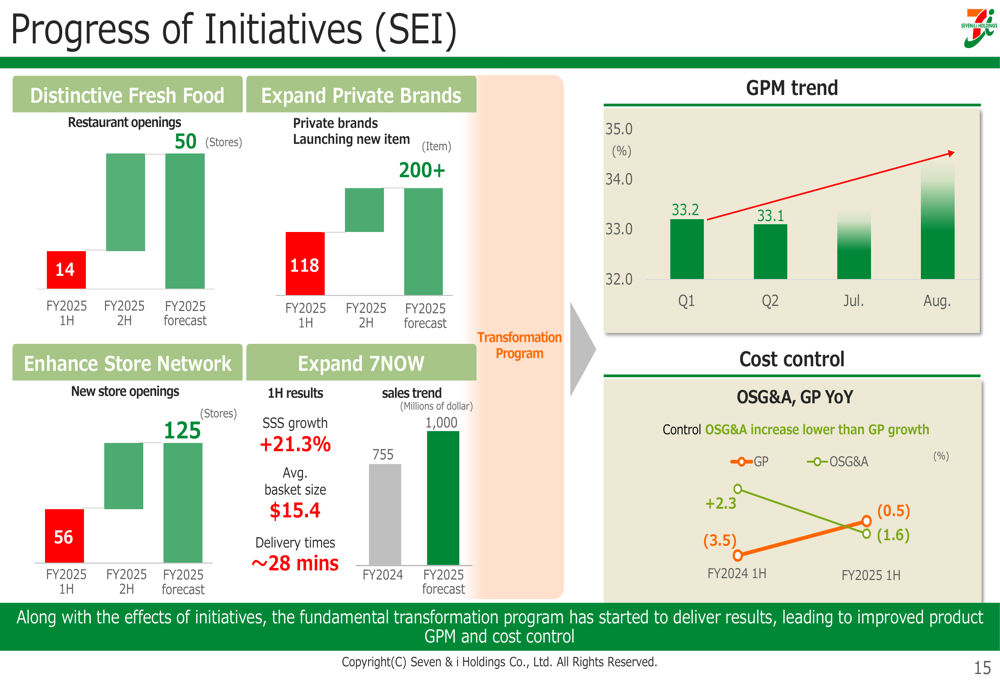

The company’s progress in key initiatives for both SEJ and SEI shows promising developments in fresh food offerings, which are central to the company’s strategy:

For SEI, the expansion of restaurant concepts and private brand products remains a strategic priority:

Strategic Initiatives

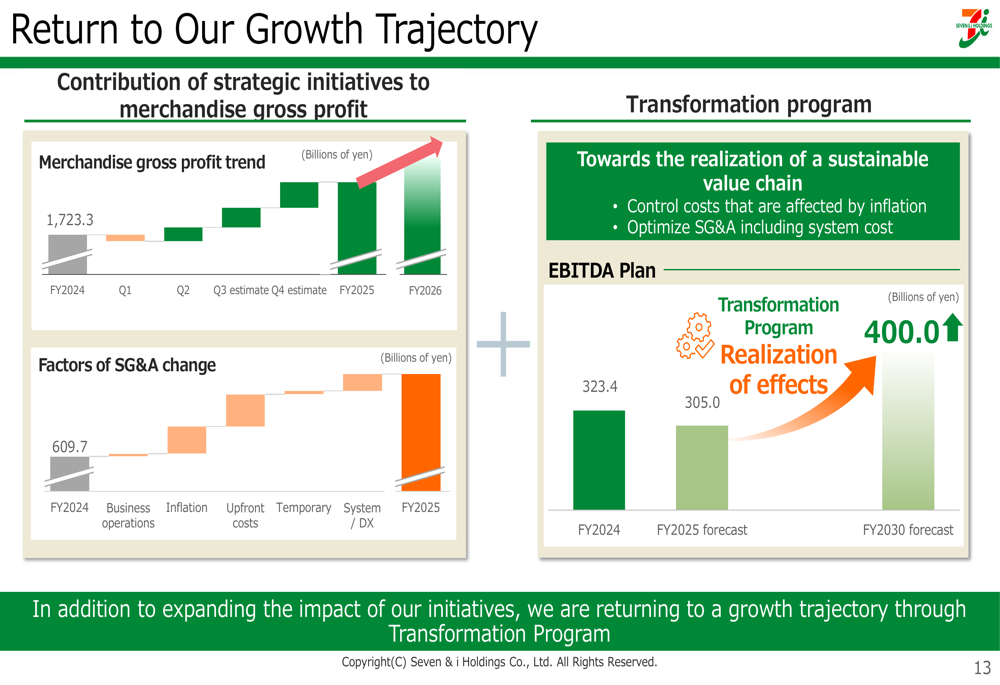

Seven & i Holdings outlined its transformation program aimed at returning to a sustainable growth trajectory. The company is focusing on controlling costs affected by inflation and optimizing SG&A expenses to improve profitability across operations.

As shown in the following chart, the company has established a clear path toward its EBITDA target of 400 billion yen by FY2030:

For Seven-Eleven Japan, the company is emphasizing "just-made counter merchandise" with categories like hot foods, SEVEN CAFÉ, and smoothies showing growth of 3.9%, 6.5%, and 10.5% respectively. The average per store per day (APSD) of just-made counter merchandise increased by 5.5%.

The company is also strengthening high-value-added merchandise with initiatives like "Umasa-Aimori" and "Oyogase-men," while expanding SEVEN CAFÉ Bakery to 817 additional stores and SEVEN CAFÉ Tea to 776 more locations.

For Seven-Eleven Inc., the focus remains on restaurant openings (projected 50 new locations), expanding private brands (200+ new items), and enhancing digital capabilities including delivery services that currently average 28-minute delivery times.

Revised Financial Forecasts

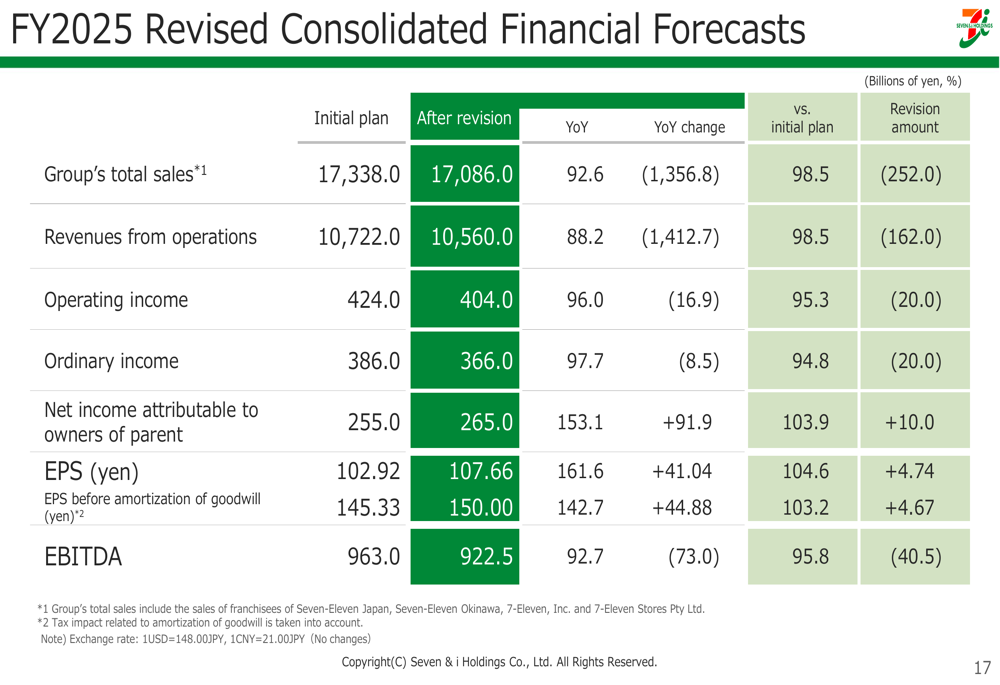

Seven & i Holdings revised its full-year financial forecasts, adjusting several key metrics as shown in the following table:

While the company reduced its revenue and operating income forecasts, it notably increased its net income projection from 255.0 to 265.0 billion yen, representing a substantial 153.1% year-over-year growth. Similarly, EPS forecasts were revised upward from 102.92 to 107.66 yen, a 161.6% increase from the previous year.

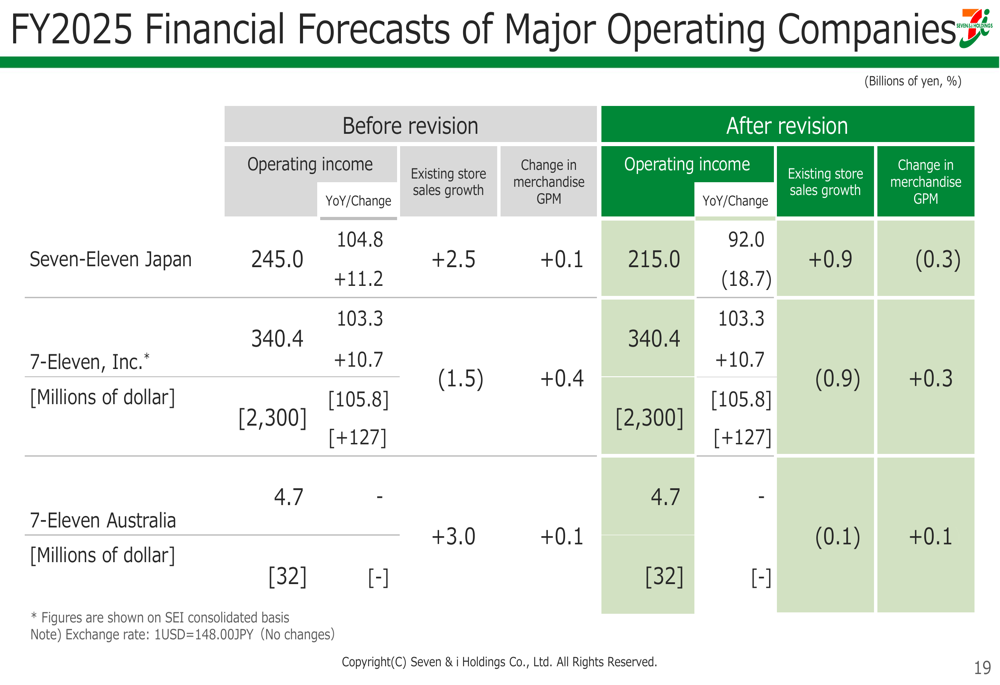

The company also provided segment-specific forecasts for its major operating companies:

Seven-Eleven Japan’s operating income forecast was maintained at 215.0 billion yen with existing store sales growth projected at 0.9%. Seven-Eleven Inc.’s forecast remained unchanged with a focus on improving merchandise gross profit margin by 0.3%.

Forward-Looking Statements

Seven & i Holdings reaffirmed its commitment to several strategic initiatives, including the planned IPO of Seven-Eleven Inc. by the second half of 2026. According to the presentation, practical preparations for this significant corporate event are progressing as scheduled.

The company also highlighted its ongoing share repurchase program, which has reached 58.8% completion, and announced an interim dividend of 25.0 yen per share with payments scheduled for November 14, 2025. The total dividend for the fiscal year is forecast to be 50 yen per share.

The key takeaways from the presentation emphasize the company’s focus on transformation programs to drive sustainable growth:

CEO Davis emphasized the company’s commitment to returning Seven-Eleven Japan to growth in the next fiscal year, primarily through the nationwide rollout of freshly prepared items. "Our objective is clear: to deliver visible results, starting with increased customer traffic," Davis stated during the earnings call.

Despite the positive profit trajectory, Seven & i Holdings faces several challenges, including inflationary pressures, declining consumer spending in Japan, reduced shopping frequency, and competitive pressures in the ready-to-eat market. The company’s transformation initiatives are designed to address these challenges while positioning the business for sustainable long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.