Joby Aviation closes $591 million stock offering with full underwriter option

Introduction & Market Context

Sherritt International Corporation (TSX:S) presented its Q1 2025 financial results on May 14, 2025, highlighting improved EBITDA performance despite ongoing challenges in the nickel and cobalt markets. The Canadian mining company continues to navigate a global oversupply environment while making progress on strategic initiatives including debt restructuring and the Moa Joint Venture expansion.

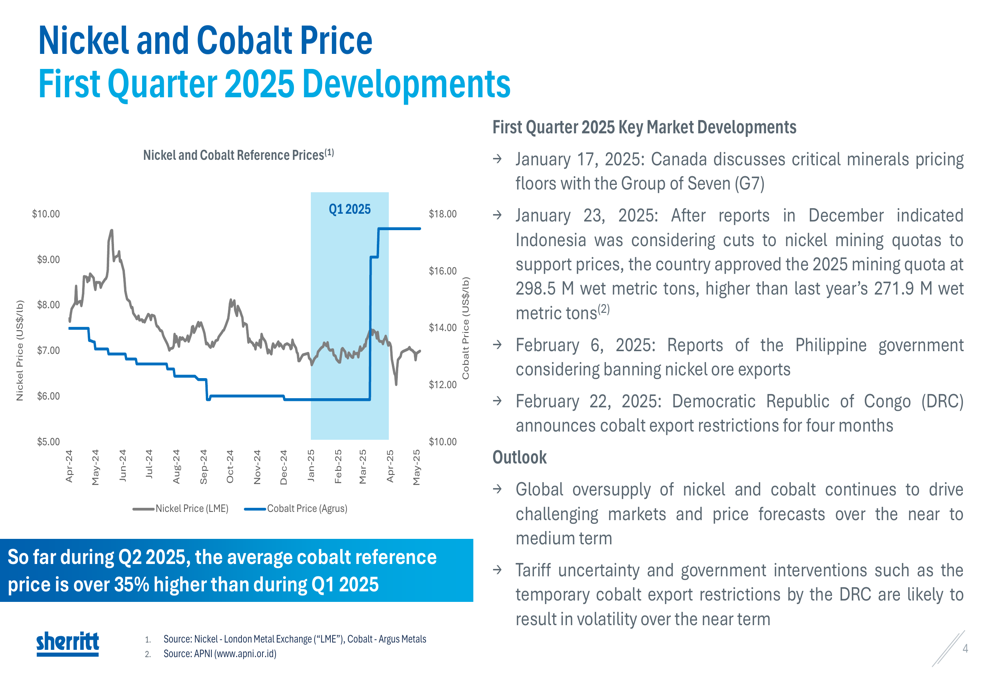

Market conditions remain challenging for Sherritt, with nickel and cobalt prices under pressure due to global oversupply. However, the company noted several key market developments that could impact future pricing, including Canada’s discussions with G7 partners about critical minerals pricing floors and the Democratic Republic of Congo’s announcement of temporary cobalt export restrictions.

As shown in the following chart of nickel and cobalt price developments, cobalt reference prices are trending upward, with Q2 2025 prices over 35% higher than Q1 2025:

Quarterly Performance Highlights

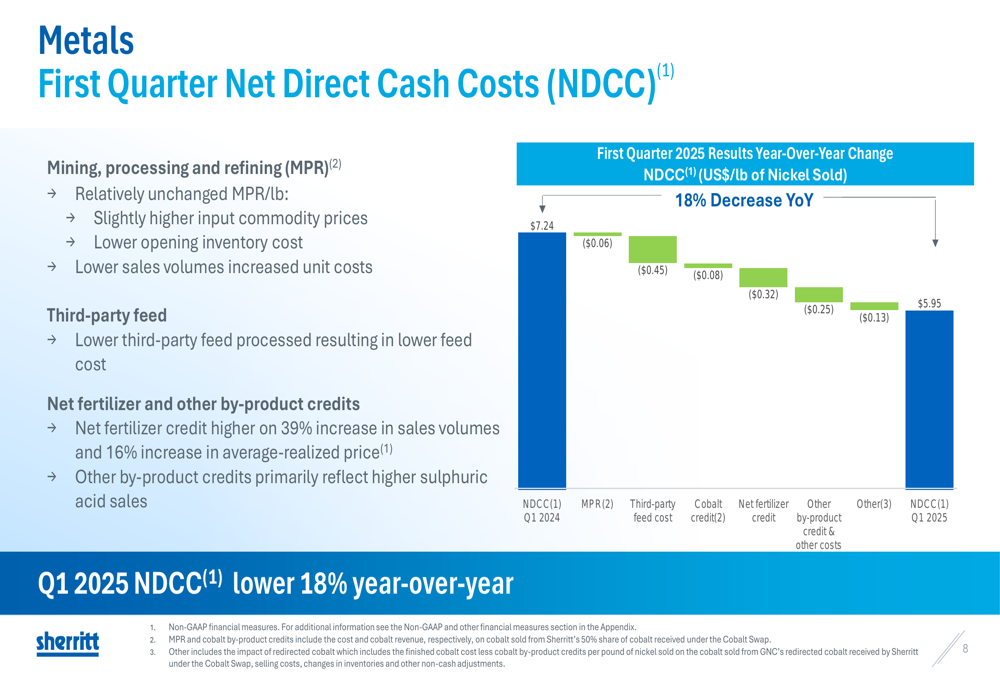

Sherritt reported mixed operational results for Q1 2025. Nickel production reached 2,947 tonnes and cobalt production totaled 323 tonnes, while sales volumes were 3,439 tonnes and 456 tonnes respectively. The company’s Net Direct Cash Cost (NDCC) decreased significantly by 18% year-over-year to $5.95 per pound, primarily driven by higher net fertilizer and other by-product credits, as well as lower third-party feed costs.

The following table summarizes Sherritt’s metals production and sales performance:

The company’s NDCC improvement represents a significant achievement in the current market environment. The following waterfall chart illustrates the key factors contributing to the 18% year-over-year reduction in NDCC:

In the Power segment, electricity production was lower at 170 GWh compared to 210 GWh in Q1 2024, primarily due to frequency control at the Varadero facility (at the request of the Cuban utility) and reduced gas supply. Despite lower production, Sherritt noted that Energas was fully compensated for lost production in Q1 and expects to be fully compensated throughout 2025.

Financial Analysis

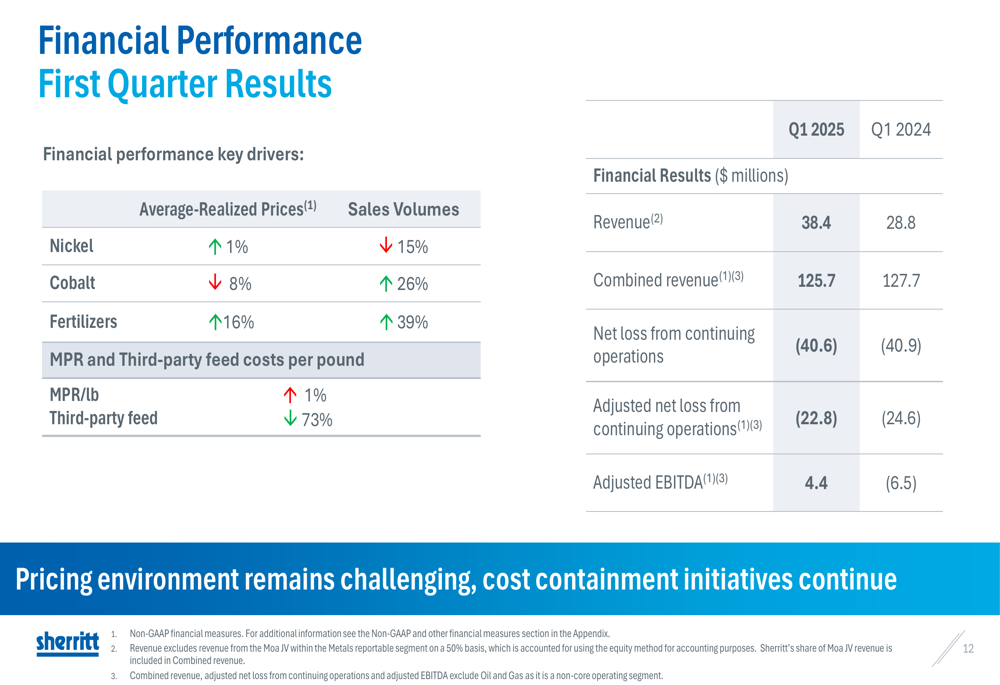

Sherritt’s financial performance showed improvement in key metrics despite market challenges. Revenue increased to $38.4 million in Q1 2025 from $28.8 million in Q1 2024, while combined revenue (including the Moa JV) remained relatively stable at $125.7 million compared to $127.7 million in the prior-year period.

The company reported a net loss from continuing operations of $40.6 million, slightly improved from $40.9 million in Q1 2024. Notably, adjusted EBITDA turned positive at $4.4 million, compared to negative $6.5 million in the prior-year period, demonstrating progress in operational efficiency despite challenging market conditions.

The following table provides a detailed breakdown of Sherritt’s financial performance:

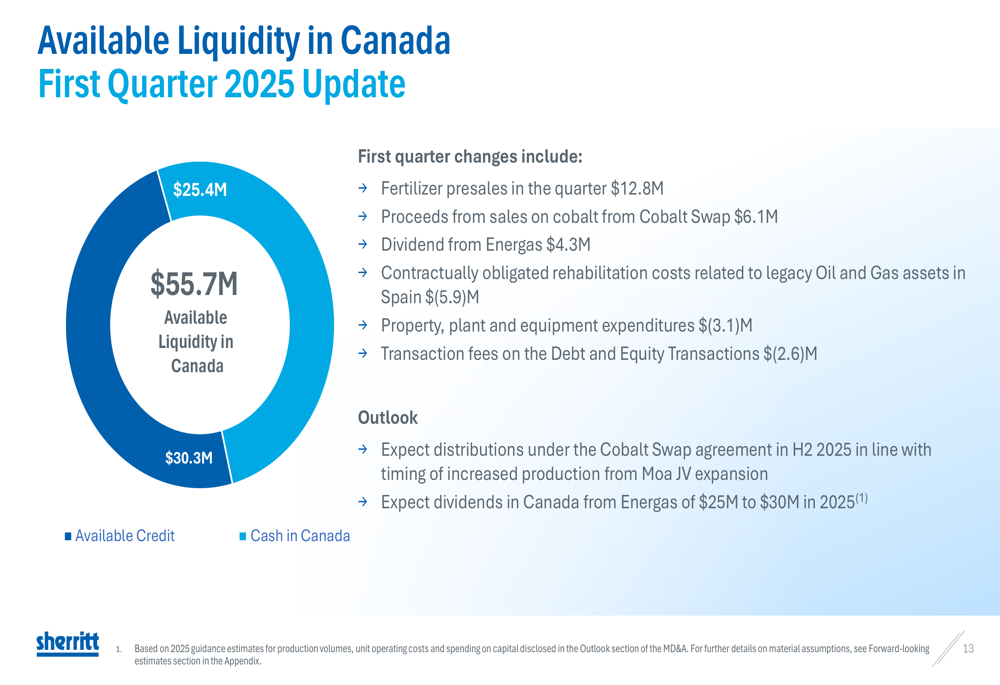

Sherritt maintained a solid liquidity position with total available liquidity in Canada of $55.7 million as of Q1 2025, consisting of $25.4 million in available credit and $30.3 million in cash. Key contributors to the company’s liquidity included $12.8 million from fertilizer presales, $6.1 million from cobalt sales under the Cobalt Swap agreement, and $4.3 million in dividends from Energas.

Strategic Initiatives

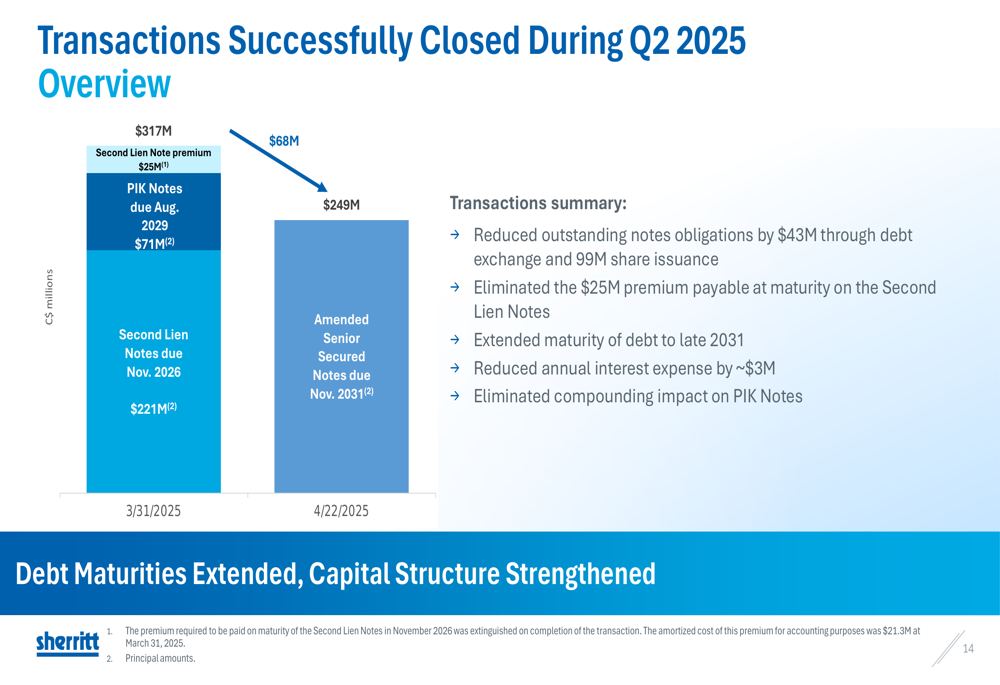

A major highlight of Sherritt’s Q1 presentation was the successful completion of strategic debt restructuring transactions in April 2025. The company reduced its outstanding notes obligations by $43 million through a debt exchange and 99 million share issuance, eliminated a $25 million premium payable at maturity on Second Lien Notes, extended debt maturities to late 2031, and reduced annual interest expense by approximately $3 million.

The following chart illustrates the transformation of Sherritt’s debt structure:

Progress continues on the Moa JV expansion, with commissioning of phase two (the processing plant) beginning during the quarter. The company expects additional mixed sulphides precipitate from the expansion to begin processing at the refinery in the fourth quarter of 2025, with full ramp-up anticipated in the second half of the year.

The interior of the Moa processing plant in Cuba is shown below:

Forward-Looking Statements

Looking ahead, Sherritt maintained its 2025 guidance for Metals and Power segments. The company expects stronger production in the second half of 2025, coinciding with the ramp-up of phase two of the Moa JV expansion. Management anticipates distributions under the Cobalt Swap agreement in the second half of 2025, aligned with increased production from the expansion.

Sherritt continues to advance its midstream MHP (Mixed Hydroxide Precipitate) Project, engaging with federal and provincial governments, potential customers, and funding partners. The company’s focus for 2025 includes securing external partners and funding support, including offtake partners for refinery products and by-products.

The following slide summarizes Sherritt’s key strategic initiatives and outlook:

Despite the challenging pricing environment, Sherritt’s management expressed confidence in the company’s positioning to drive significant long-term value through its strategic initiatives, cost containment efforts, and production expansion plans. With debt maturities extended and capital structure strengthened, the company appears better positioned to navigate market volatility while pursuing growth opportunities.

Sherritt International Corporation closed at C$0.145 on May 14, 2025, down 3.45% from the previous close.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.