IREN proposes $875 million convertible notes offering due 2031

Introduction & Market Context

Sherwin-Williams (NYSE:SHW) released its first quarter 2025 results on April 29, showing the paint and coatings giant navigating a challenging environment with improved profitability despite slight revenue declines. The company’s stock traded up 0.91% in premarket at $335.21, following a previous close of $332.20.

The results come amid what management previously described as a "choppy" demand environment, with the company demonstrating resilience through margin expansion and strategic initiatives despite facing headwinds in some segments. Sherwin-Williams continues to operate within a market characterized by mixed signals across residential, commercial, and industrial sectors.

Quarterly Performance Highlights

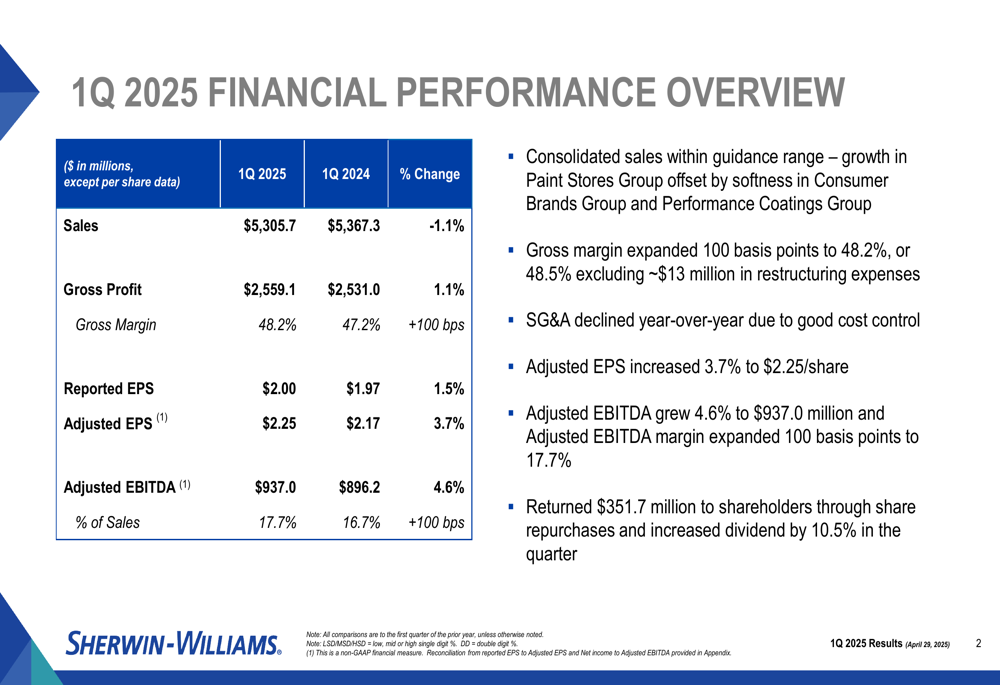

Sherwin-Williams reported Q1 2025 sales of $5,305.7 million, representing a 1.1% decrease compared to $5,367.3 million in the same period last year. Despite this revenue dip, the company improved its profitability metrics across the board, with gross profit increasing 1.1% to $2,559.1 million and gross margin expanding 100 basis points to 48.2%.

As shown in the following financial overview, the company delivered adjusted earnings per share of $2.25, a 3.7% increase from $2.17 in Q1 2024, while adjusted EBITDA grew 4.6% to $937.0 million:

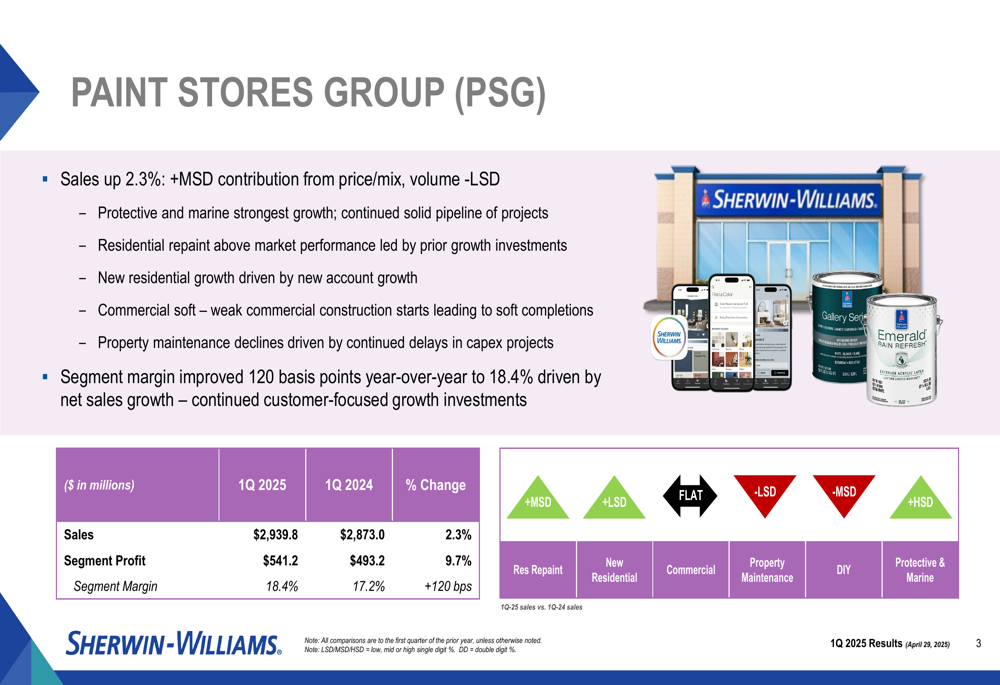

Segment performance varied significantly, with the Paint Stores Group (PSG) emerging as the strongest performer. PSG sales increased 2.3%, driven by positive price/mix contributions, though partially offset by lower volumes. The segment’s margin improved 120 basis points year-over-year to 18.4%, with protective and marine coatings showing the strongest growth.

The following chart illustrates the Paint Stores Group’s performance across different product categories:

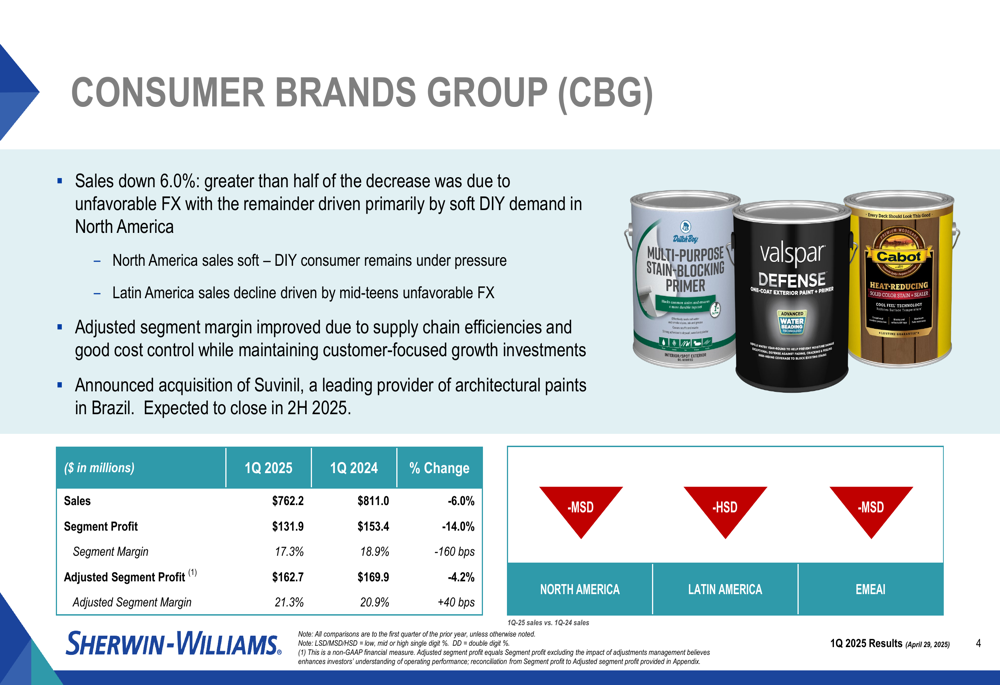

In contrast, the Consumer Brands Group (CBG) faced more significant challenges, with sales decreasing 6.0%. This decline was primarily attributed to unfavorable foreign exchange impacts and soft DIY demand in North America. Despite these headwinds, the segment’s adjusted margin improved due to supply chain efficiencies and cost control measures.

The Consumer Brands Group performance breakdown by geography shows the challenges across different regions:

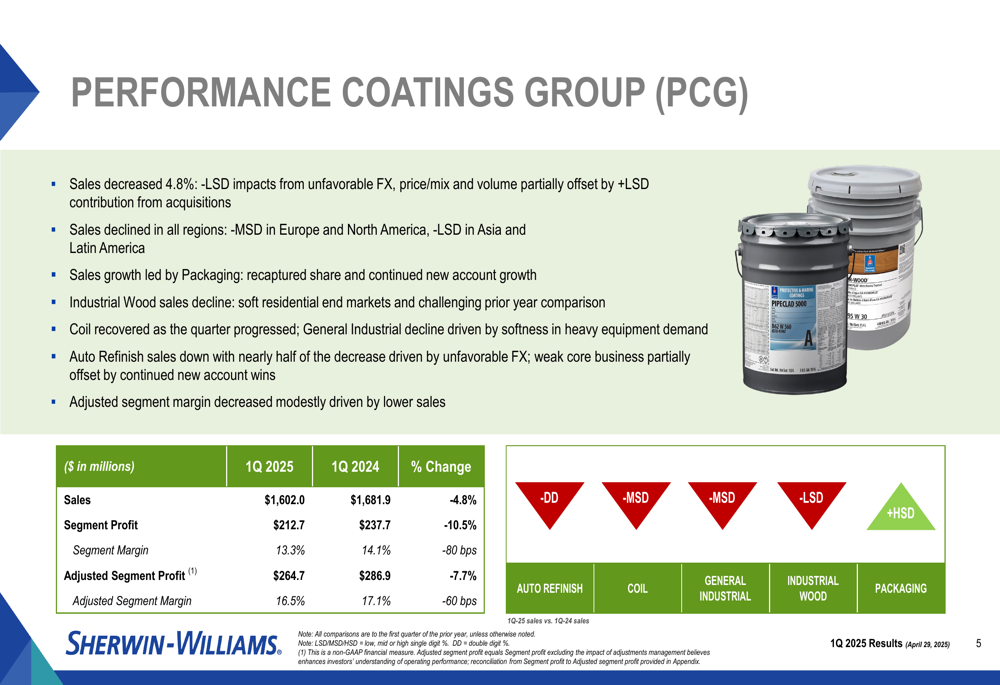

Similarly, the Performance Coatings Group (PCG) experienced a 4.8% sales decrease, affected by unfavorable foreign exchange, price/mix, and volume. Sales declined across all regions, though packaging coatings showed high single-digit growth. The segment’s adjusted margin decreased modestly due to lower sales.

The Performance Coatings Group’s mixed results across different sectors are illustrated in this breakdown:

Detailed Financial Analysis

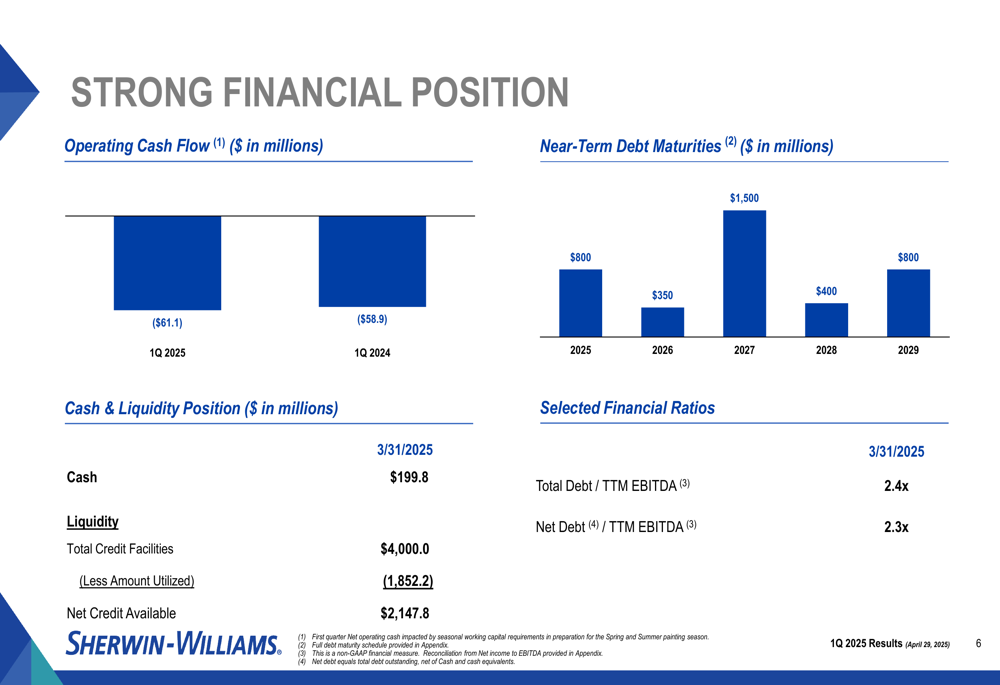

Sherwin-Williams maintained a strong financial position despite reporting negative operating cash flow of $61.1 million for Q1 2025, slightly worse than the negative $58.9 million reported in Q1 2024. This is not unusual for the first quarter due to seasonal patterns in the paint and coatings industry.

The company’s debt profile shows manageable near-term maturities, with $800 million due in 2025. As of March 31, 2025, Sherwin-Williams reported total debt to TTM EBITDA of 2.4x and net debt to TTM EBITDA of 2.3x, indicating a healthy leverage position. The company maintained substantial liquidity with $199.8 million in cash and $2,147.8 million in available credit.

The following chart details the company’s financial position, including debt maturities and key financial ratios:

Sherwin-Williams returned $351.7 million to shareholders during the quarter, continuing its commitment to shareholder returns. The company’s debt structure remains well-balanced with 83% fixed-rate debt and 17% floating-rate debt, providing stability in the current interest rate environment.

Strategic Initiatives

During the quarter, Sherwin-Williams announced the acquisition of Suvinil in Brazil, expected to close in the second half of 2025. This strategic move expands the company’s presence in Latin America and aligns with its global growth strategy.

Capital expenditures for 2025 are projected at approximately $900 million, including $200 million allocated for new buildings. This investment underscores the company’s commitment to long-term growth despite near-term market uncertainties.

Forward-Looking Statements

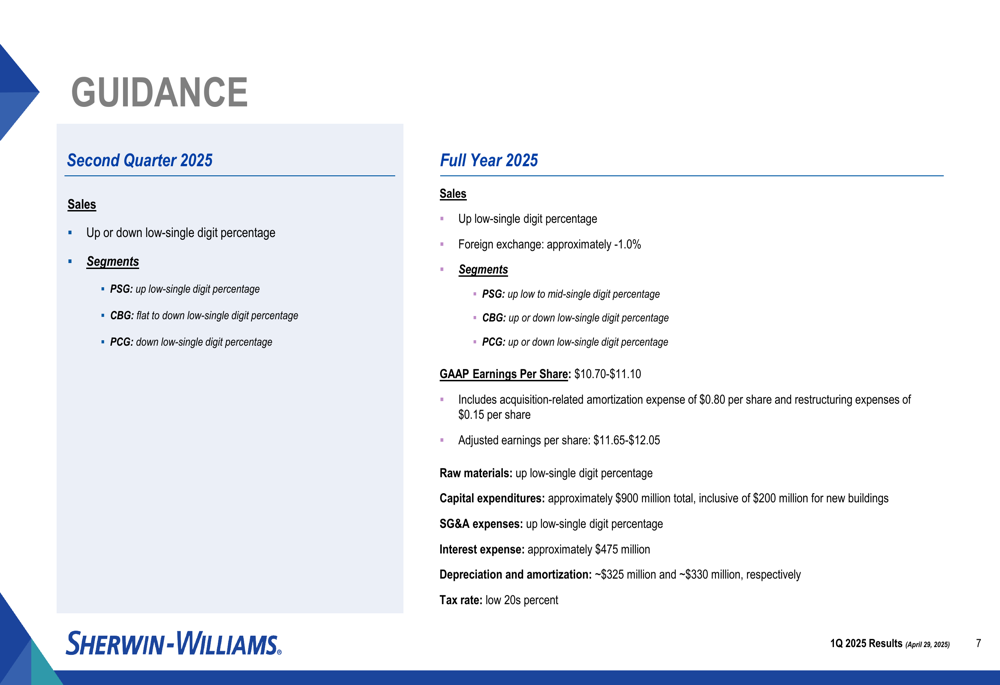

Looking ahead, Sherwin-Williams provided guidance for both the second quarter and full year 2025. For Q2, the company expects sales to be up or down by a low-single-digit percentage, with mixed performance across segments. The Paint Stores Group is projected to show low-single-digit growth, while Consumer Brands Group and Performance Coatings Group are expected to be flat to down by low-single digits.

For the full year 2025, Sherwin-Williams maintained its outlook for low-single-digit percentage sales growth, with foreign exchange expected to have a negative 1.0% impact. The company projects GAAP earnings per share of $10.70-$11.10 and adjusted earnings per share of $11.65-$12.05.

The detailed guidance for both Q2 and full-year 2025 is presented in the following chart:

This guidance reflects management’s cautious optimism about gradual market improvement throughout 2025, balanced against ongoing challenges in certain segments and regions. The company’s focus on margin expansion and operational efficiency appears designed to offset potential revenue volatility in a still-uncertain market environment.

Sherwin-Williams continues to demonstrate its ability to navigate challenging market conditions through disciplined cost management and strategic pricing, even as it invests in long-term growth initiatives. The company’s performance in Q1 2025 suggests it remains well-positioned to capitalize on eventual market recovery while maintaining profitability in the current environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.