Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

Sherwin-Williams Co (NYSE:SHW) released its second quarter 2025 financial results on July 22, revealing modest sales growth but declining profitability metrics. The paint and coatings giant reported results largely within its guidance range, though higher costs weighed on earnings. The stock traded down 3.02% in premarket to $331.00, reflecting investor concerns about profitability despite maintained full-year guidance.

The company’s performance comes amid continued challenges in the housing market, with mortgage rates and consumer confidence impacting DIY demand, while professional segments showed more resilience. This follows a stronger first quarter when the company beat EPS expectations.

Quarterly Performance Highlights

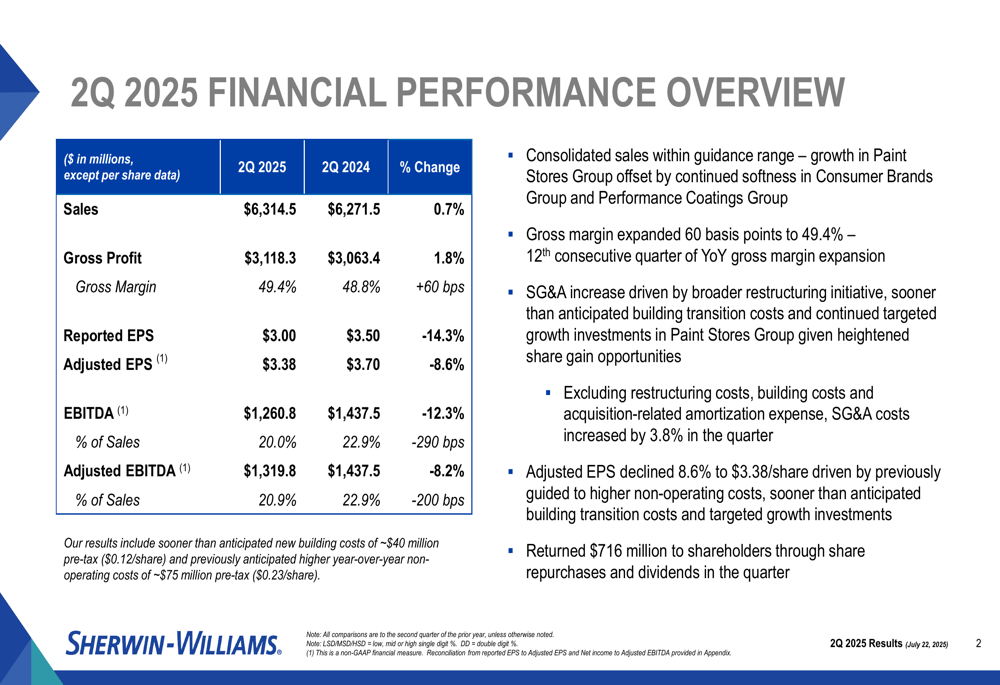

Sherwin-Williams reported second quarter sales of $6,314.5 million, a slight increase of 0.7% year-over-year. While gross profit rose 1.8% to $3,118.3 million and gross margin expanded by 60 basis points to 49.4%, profitability metrics declined significantly.

As shown in the company’s financial overview:

Reported earnings per share fell 14.3% to $3.00, while adjusted EPS decreased 8.6% to $3.38. The company noted that results were impacted by approximately $40 million in sooner-than-anticipated new building costs ($0.12 per share) and previously anticipated higher year-over-year non-operating costs of approximately $75 million ($0.23 per share).

Despite these challenges, Sherwin-Williams returned $716 million to shareholders through share repurchases and dividends during the quarter, demonstrating confidence in its long-term financial position.

Segment Analysis

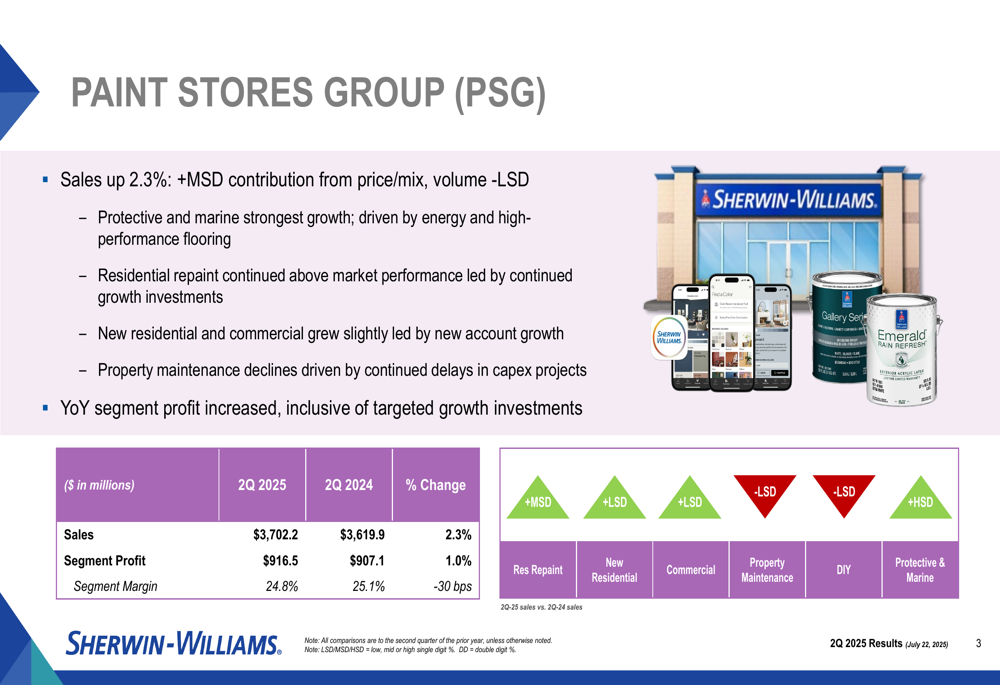

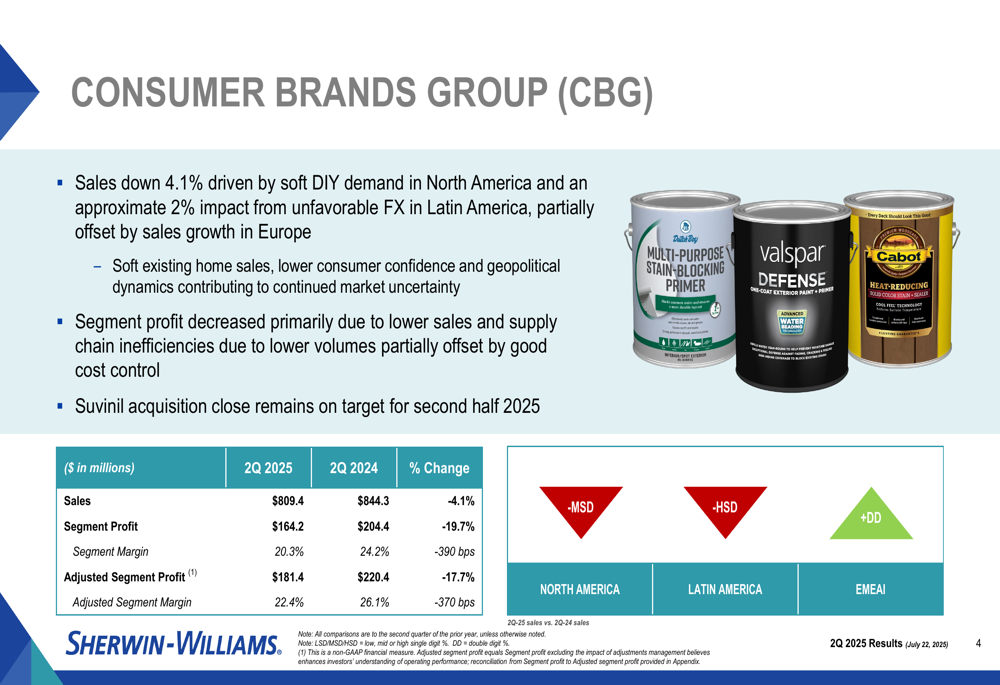

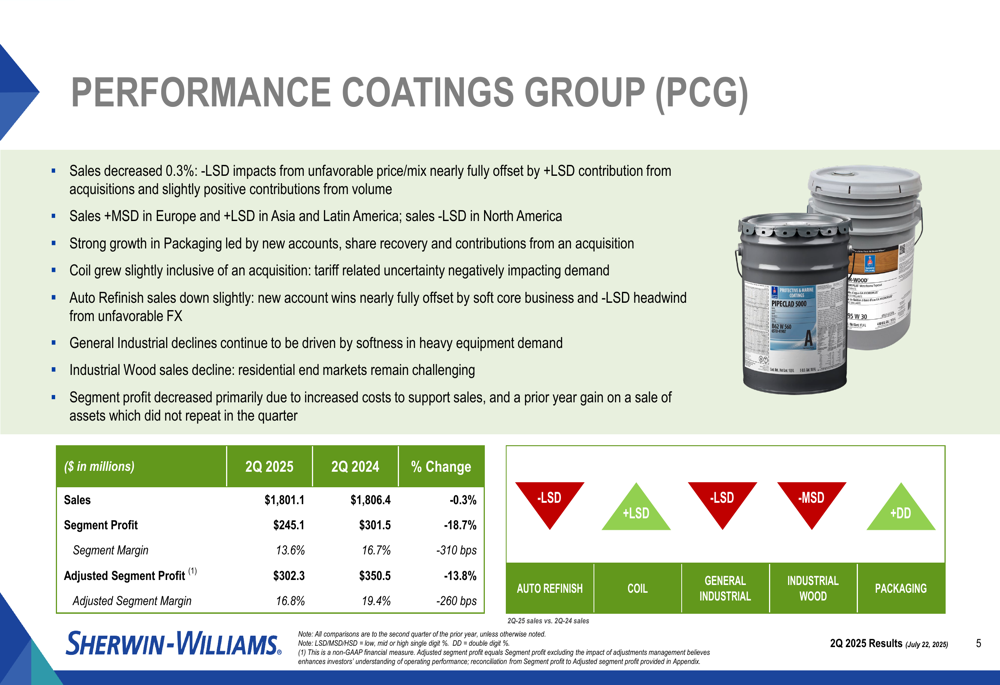

The company’s three operating segments showed divergent performance, with the Paint Stores Group (PSG) delivering growth while the Consumer Brands Group (CBG) and Performance Coatings Group (PCG) experienced declines.

The Paint Stores Group, which represents the largest segment, posted sales of $3,702.2 million, increasing 2.3% year-over-year. This growth was driven by price/mix improvements (mid-single digits) that offset volume declines (low-single digits). Segment profit increased 1.0% to $916.5 million, though margin contracted slightly to 24.8%.

The Consumer Brands Group faced more significant challenges, with sales declining 4.1% to $809.4 million. The segment was impacted by soft DIY demand in North America and unfavorable foreign exchange in Latin America. Segment profit decreased 19.7% to $164.2 million, with margin contracting 390 basis points to 20.3%.

The Performance Coatings Group saw a slight sales decline of 0.3% to $1,801.1 million. While packaging showed double-digit growth led by new accounts and share recovery, this was offset by declines in general industrial and industrial wood segments. Segment profit fell 18.7% to $245.1 million, with margin contracting 310 basis points to 13.6%.

Financial Position & Outlook

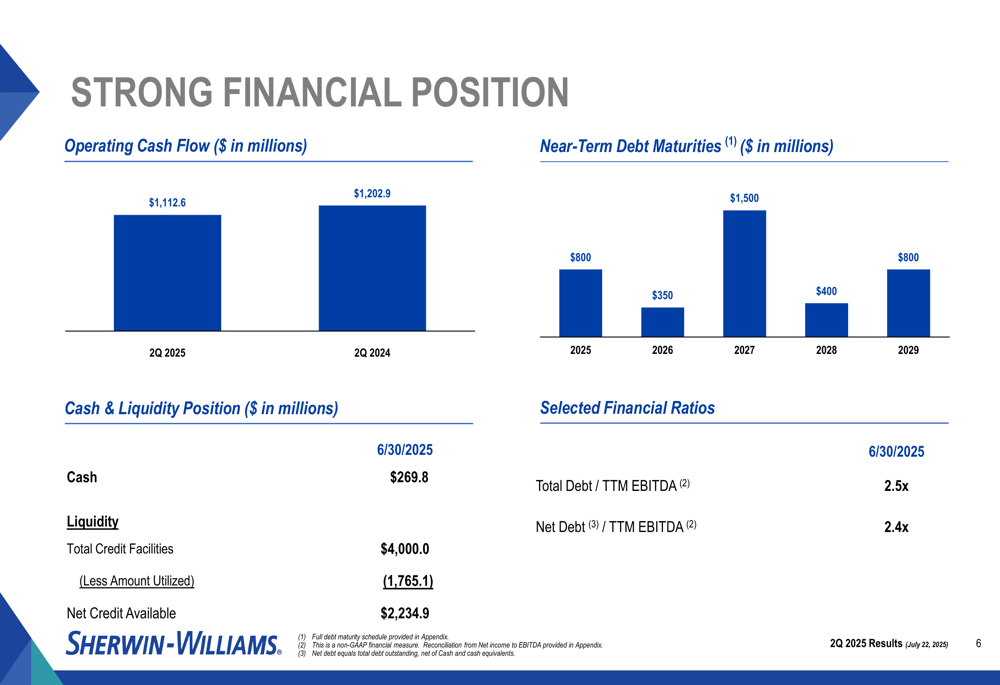

Despite the profitability challenges, Sherwin-Williams maintained a strong financial position with operating cash flow of $1,112.6 million, slightly down from $1,202.9 million in the same period last year. The company reported total debt to trailing twelve-month EBITDA of 2.5x and net debt to TTM EBITDA of 2.4x, indicating a manageable leverage position.

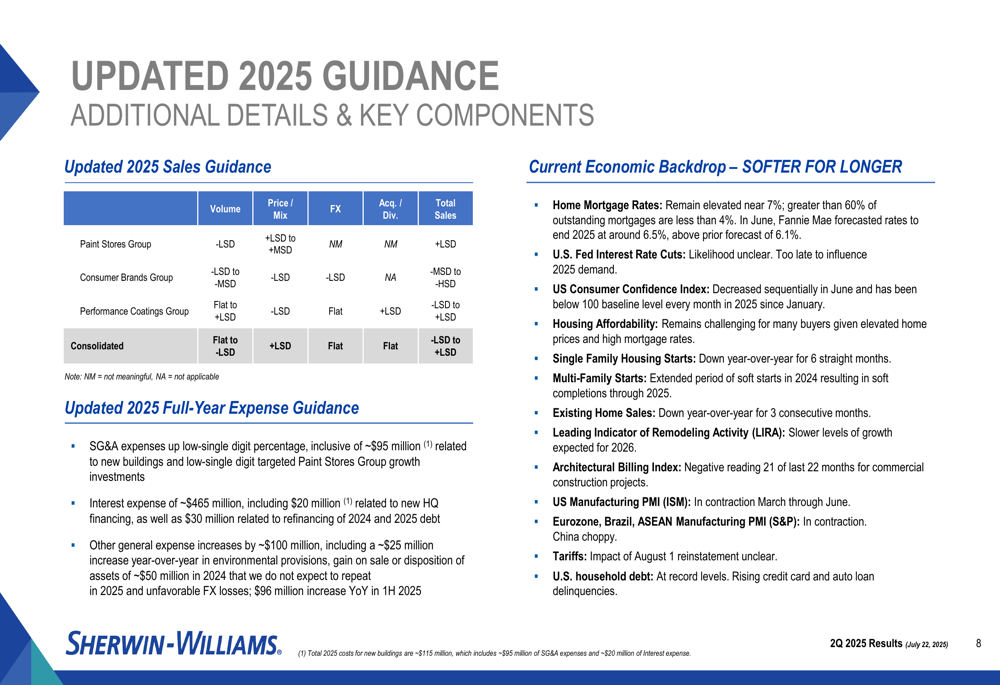

For the third quarter of 2025, Sherwin-Williams expects sales to be up or down by a low-single digit percentage, with the Paint Stores Group projected to grow by a low-single digit percentage, Consumer Brands Group expected to decline by mid to high-single digits, and Performance Coatings Group anticipated to be flat to up low-single digits.

The company maintained its full-year 2025 sales guidance of up or down low-single digit percentage, with foreign exchange impact expected to be less than -1.0%. Full-year GAAP earnings per share guidance was set at $10.11-$10.41, with adjusted earnings per share of $11.20-$11.50.

Forward-Looking Statements

Sherwin-Williams’ guidance incorporates several key economic assumptions, including expectations for home mortgage rates, U.S. Federal Reserve interest rate cuts, consumer confidence, housing affordability, and manufacturing activity. The company also factored in potential tariff impacts, which could affect its cost structure.

The planned acquisition of Suvinil in Brazil remains on target for closing in the second half of 2025, which should strengthen the company’s position in Latin America despite current challenges in that region.

Capital expenditures are projected at approximately $730 million for the year, including $300 million for new buildings. Raw material costs are expected to remain flat compared to the prior year, while SG&A expenses are anticipated to increase by a low-single digit percentage.

As Sherwin-Williams navigates a challenging economic environment, the company’s ability to maintain sales growth in its Paint Stores Group while addressing profitability concerns in other segments will be crucial for meeting its full-year targets. The market reaction suggests investors remain cautious about the company’s ability to overcome these near-term headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.