Asia stocks surge as tech extends rebound, Dec rate cut bets grow

Introduction & Market Context

Sherwin-Williams (NYSE:SHW) presented its third quarter 2025 results on October 28, showing solid overall performance despite mixed results across business segments. The company reported better-than-expected earnings and revenue, driving its stock up 5.81% in pre-market trading to $355.62, and continuing to rise 4.18% during regular trading hours.

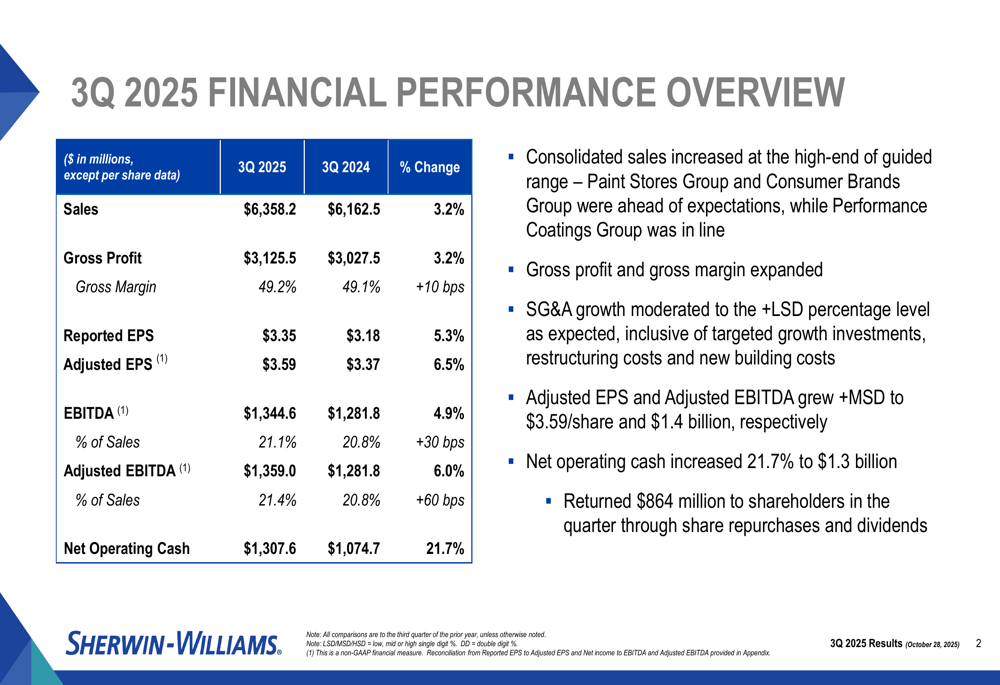

The paint and coatings manufacturer demonstrated resilience in a challenging environment, with consolidated sales increasing 3.2% year-over-year to $6.36 billion, exceeding analyst expectations of $6.2 billion. Adjusted earnings per share of $3.59 surpassed forecasts of $3.45, representing a 6.5% increase from the prior year.

Quarterly Performance Highlights

Sherwin-Williams delivered solid financial results across key metrics in Q3 2025, with particular strength in its Paint Stores Group and significant improvement in cash flow generation.

As shown in the following comprehensive financial overview:

The company's gross margin expanded slightly to 49.2%, up 10 basis points year-over-year. More impressively, adjusted EBITDA grew 6.0% to $1.36 billion, representing 21.4% of sales – a 60 basis point improvement from Q3 2024. Net operating cash flow showed remarkable growth of 21.7%, reaching $1.31 billion for the quarter.

Sherwin-Williams returned $864 million to shareholders through a combination of share repurchases and dividends, underscoring its commitment to shareholder returns even while investing in growth initiatives.

Detailed Financial Analysis

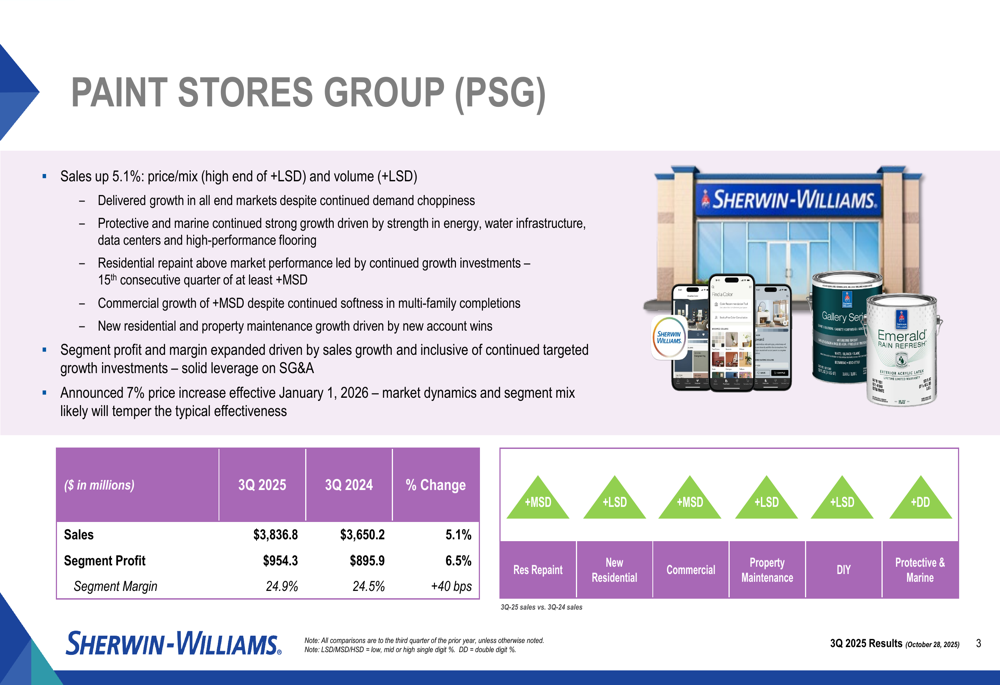

Performance varied significantly across Sherwin-Williams' three main business segments, with the Paint Stores Group delivering the strongest results.

The Paint Stores Group, which represents approximately 60% of total sales, showed robust growth across all end markets:

PSG sales increased 5.1% to $3.84 billion, driven by both price/mix improvements and volume growth. Segment profit rose 6.5% to $954.3 million, with margins expanding 40 basis points to 24.9%. Particularly strong performance was seen in the protective and marine coatings category, which achieved double-digit growth, while residential repaint, commercial, and property maintenance segments all delivered positive results.

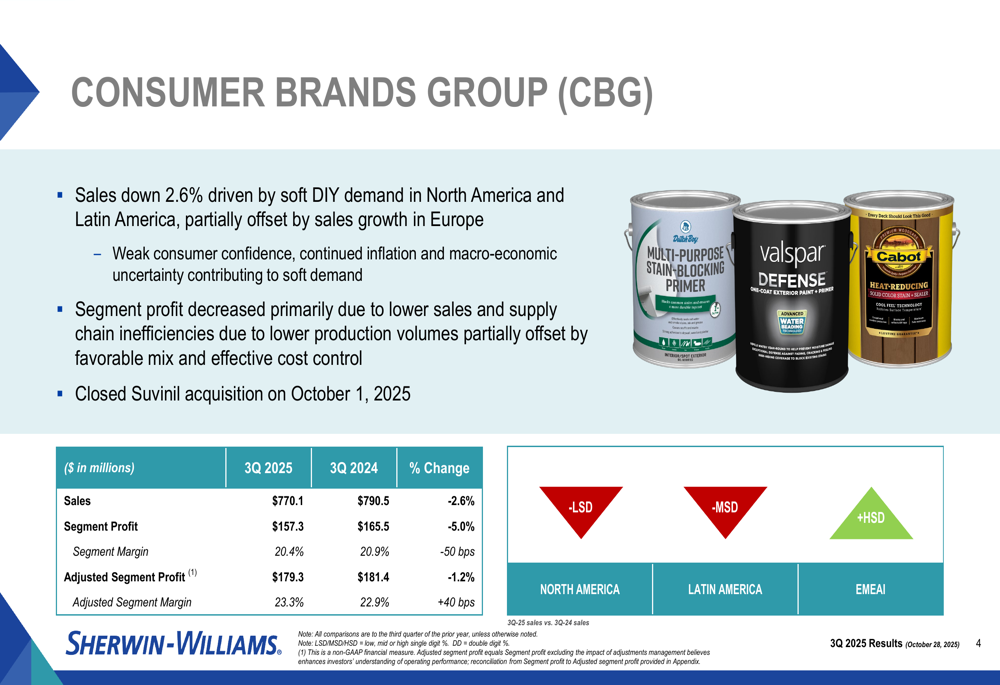

The Consumer Brands Group faced more challenging conditions:

CBG sales declined 2.6% to $770.1 million, primarily due to soft DIY demand in North America and Latin America, though this was partially offset by high-single-digit growth in Europe, Middle East, Africa, and India (EMEAI). While reported segment profit decreased 5.0% to $157.3 million, adjusted segment profit showed a smaller decline of 1.2%, with adjusted margins actually improving 40 basis points to 23.3%.

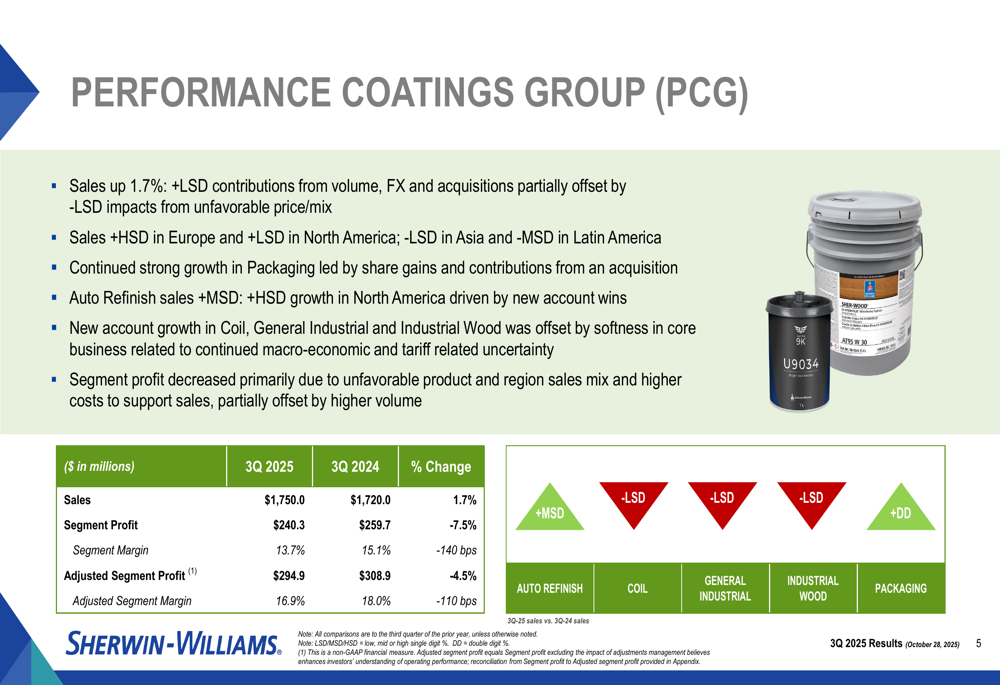

The Performance Coatings Group delivered mixed results:

PCG sales grew modestly at 1.7% to $1.75 billion, with positive contributions from volume, foreign exchange, and acquisitions partially offset by unfavorable price/mix. However, segment profit declined 7.5% to $240.3 million, with margins contracting 140 basis points to 13.7%. On an adjusted basis, segment profit decreased 4.5% to $294.9 million. The packaging coatings business was a bright spot, achieving double-digit growth, while auto refinish showed mid-single-digit growth.

Financial Position & Capital Allocation

Sherwin-Williams maintained a strong financial position in Q3 2025, with substantial cash flow generation and a manageable debt profile:

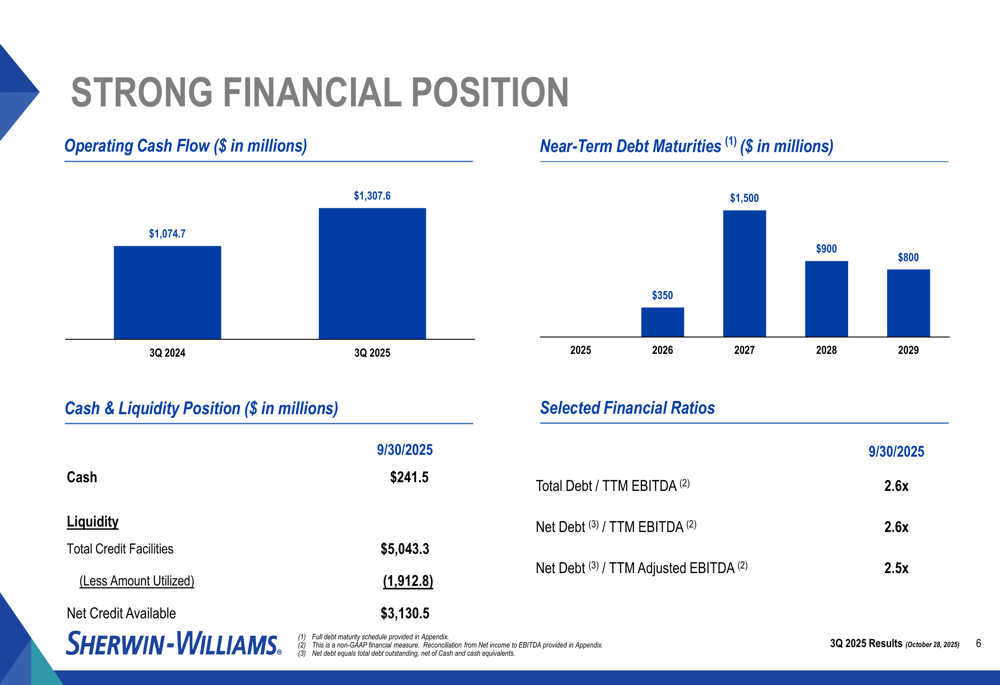

The company's operating cash flow increased dramatically from $1.07 billion in Q3 2024 to $1.31 billion in Q3 2025, representing a 21.7% improvement. This robust cash generation provides Sherwin-Williams with significant financial flexibility.

The company's debt maturity profile is well-structured, with limited near-term maturities. As of September 30, 2025, Sherwin-Williams had $241.5 million in cash and $3.13 billion in available credit, providing ample liquidity. The company's leverage ratio (Net Debt/TTM Adjusted EBITDA) stood at a comfortable 2.5x.

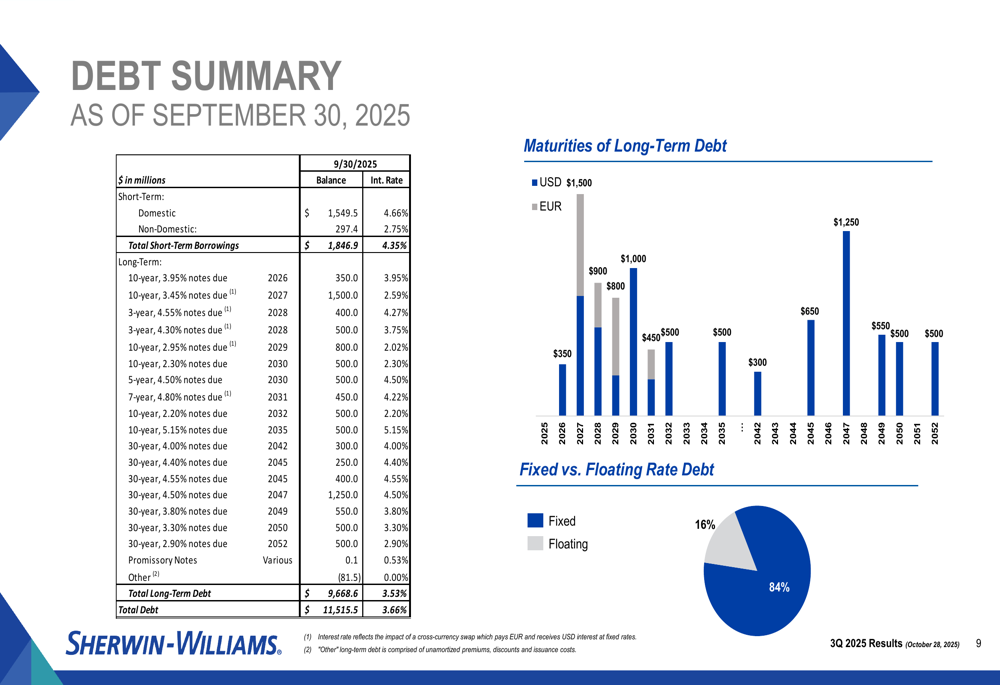

A more detailed breakdown of the company's debt structure reveals:

Sherwin-Williams maintains a prudent approach to debt management with 84% fixed-rate debt and 16% floating-rate debt, helping to insulate the company from interest rate volatility. The debt maturities are well-distributed across future years, with significant amounts not coming due until 2027 and beyond.

Strategic Initiatives

Sherwin-Williams is implementing several strategic initiatives to drive future growth and improve profitability:

1. Pricing Actions: The company announced a 7% price increase for the Paint Stores Group effective January 1, 2026, which should help offset any potential raw material cost increases and support margin expansion.

2. Strategic Acquisitions: The Suvinil acquisition closed on October 1, 2025, strengthening Sherwin-Williams' position in Latin America despite current softness in that market.

3. Restructuring Initiatives: The company is undertaking restructuring efforts that are expected to save approximately $40 million in 2025, according to the earnings call transcript.

4. Supply Chain Optimization: Management is addressing supply chain inefficiencies in the Consumer Brands Group to improve profitability in that segment.

Forward-Looking Statements

Sherwin-Williams provided updated guidance for the remainder of 2025 and offered some perspective on 2026:

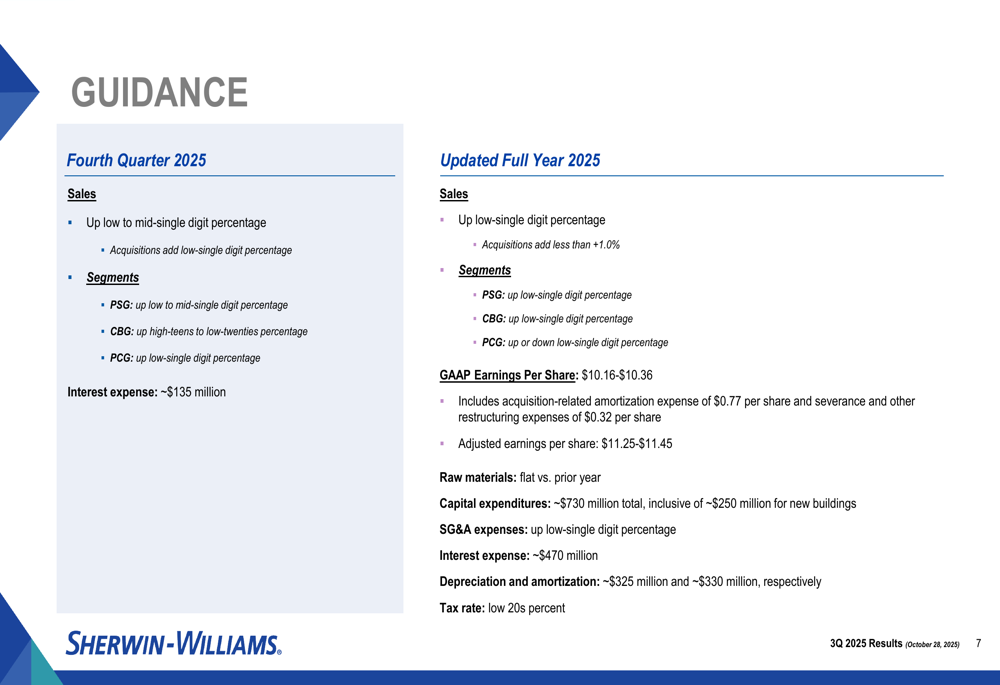

For the fourth quarter of 2025, the company expects sales to increase by low to mid-single digit percentages, with acquisitions adding a low-single digit percentage. The Paint Stores Group is projected to grow by low to mid-single digits, while the Consumer Brands Group is expected to see a significant boost of high-teens to low-twenties percentage growth, likely benefiting from the Suvinil acquisition.

For the full year 2025, Sherwin-Williams narrowed its adjusted earnings per share guidance to $11.25-$11.45, reflecting confidence in its fourth-quarter outlook. The company expects raw material costs to remain flat for the remainder of 2025.

Looking further ahead, President and CEO Heidi Petz indicated during the earnings call that the company expects the demand environment to remain soft well into 2026. Despite these challenges, management emphasized their proactive approach, stating, "Don't let a downturn go to waste. There's a lot of self-help that we can do to make sure we're continuing to improve our cost position."

Conclusion

Sherwin-Williams' Q3 2025 results demonstrate the company's ability to deliver growth and margin expansion despite challenges in certain segments and markets. The strong performance of the Paint Stores Group, coupled with robust cash flow generation and strategic initiatives, positions the company well to navigate the anticipated soft demand environment in the coming quarters.

Investors responded positively to the results and outlook, with the stock trading higher following the announcement. While management remains cautious about market conditions extending into 2026, their focus on operational efficiency, strategic pricing, and targeted acquisitions suggests a disciplined approach to creating long-term shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.