These are top 10 stocks traded on the Robinhood UK platform in July

Shimmick Corp (NASDAQ:SHIM) released its first quarter 2025 earnings presentation on May 14, showing signs of financial improvement despite ongoing challenges. The infrastructure solutions provider reported a net loss of $10 million but demonstrated progress in its turnaround strategy with improved gross margins and reduced losses in its legacy projects. The stock rose 6.19% in after-hours trading to $1.80, rebounding from near its 52-week low.

Quarterly Performance Highlights

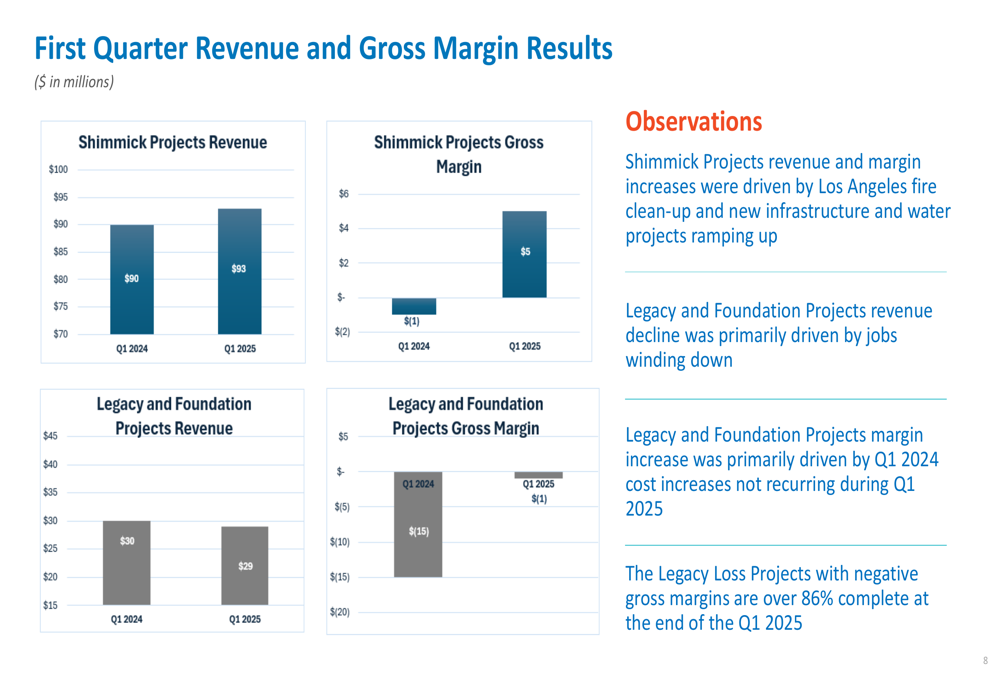

Shimmick reported total revenue of $122 million for Q1 2025, with $93 million coming from its core Shimmick Projects segment. The company achieved a gross margin of $5 million, a significant improvement compared to a negative $16 million gross margin in the same quarter last year. Selling, general, and administrative expenses decreased by 11% year-over-year to $14 million, reflecting the company’s cost control efforts.

As shown in the following quarterly results chart, Shimmick Projects revenue increased slightly from $90 million in Q1 2024 to $93 million in Q1 2025, while gross margin for this segment improved substantially from a $1 million loss to a $5 million gain:

The company’s Legacy and Foundation Projects segment, which has been a drag on overall performance, showed improvement with gross margin losses narrowing from $15 million in Q1 2024 to just $1 million in Q1 2025. Revenue from this segment declined slightly from $30 million to $29 million as these projects continue to wind down.

Strategic Initiatives

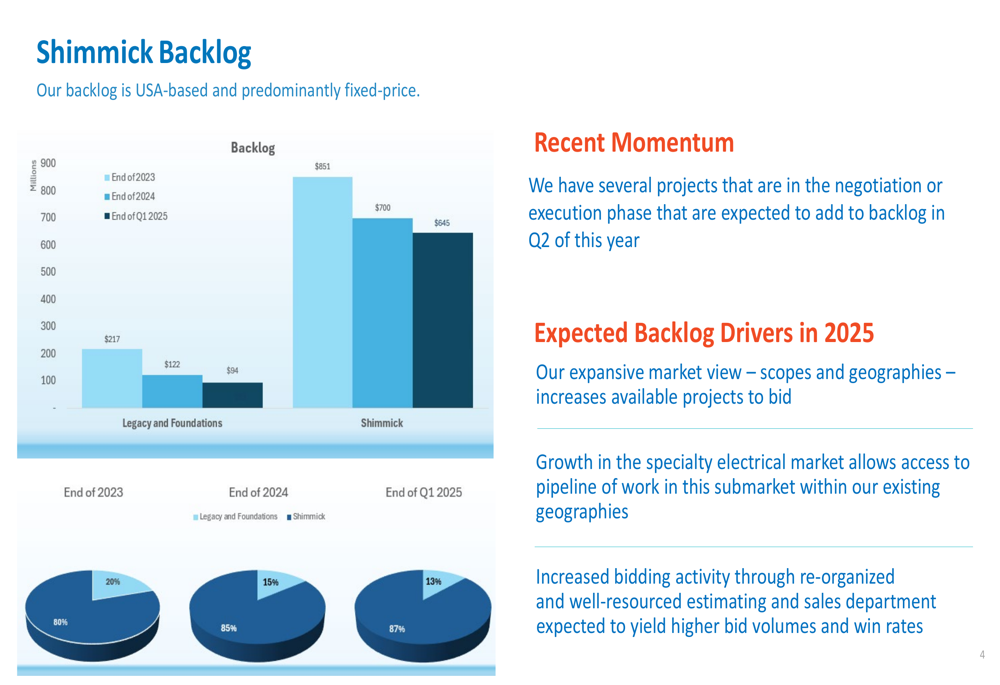

Shimmick’s presentation highlighted its strategic focus on shifting its business mix toward higher-margin Shimmick Projects while reducing exposure to problematic Legacy Projects. This transition is evident in the company’s backlog composition, which now consists of 87% Shimmick Projects compared to 80% at the end of 2023.

The following chart illustrates this strategic shift in the company’s backlog composition:

The company is also expanding its electrical business, targeting industrial, water, technology, and energy markets. Recent contract wins include the Orange County J-98 Electrical Power Distribution System Improvements, Sunol Valley Water Treatment Plant Electrical Sub Package, and Redwood (NYSE:RWT) Materials Battery Recycling Facility CAM2 Project.

Shimmick’s growth strategy focuses on three key areas: building a sustainable, risk-balanced backlog; achieving operational excellence through improved cost controls and risk management; and strengthening its people and culture with enhanced benefits and retention programs.

Financial Analysis

Despite the improved gross margins, Shimmick still reported a net loss of $10 million and Adjusted EBITDA of negative $3 million for Q1 2025. However, the company maintained a solid liquidity position of $71 million as of April 4, 2025, providing financial flexibility as it continues its turnaround efforts.

This performance represents a step forward from the company’s challenging Q4 2024, when it reported a significant earnings miss with an EPS of -0.91 compared to the forecasted 0.11, and revenue of $104 million against expectations of $173.7 million.

The company’s backlog stood at approximately $740 million as of April 4, 2025, providing visibility for future revenue. According to the presentation, Shimmick is seeing increased bidding activity with nearly $2 billion in projects anticipated to come to market.

Forward-Looking Statements

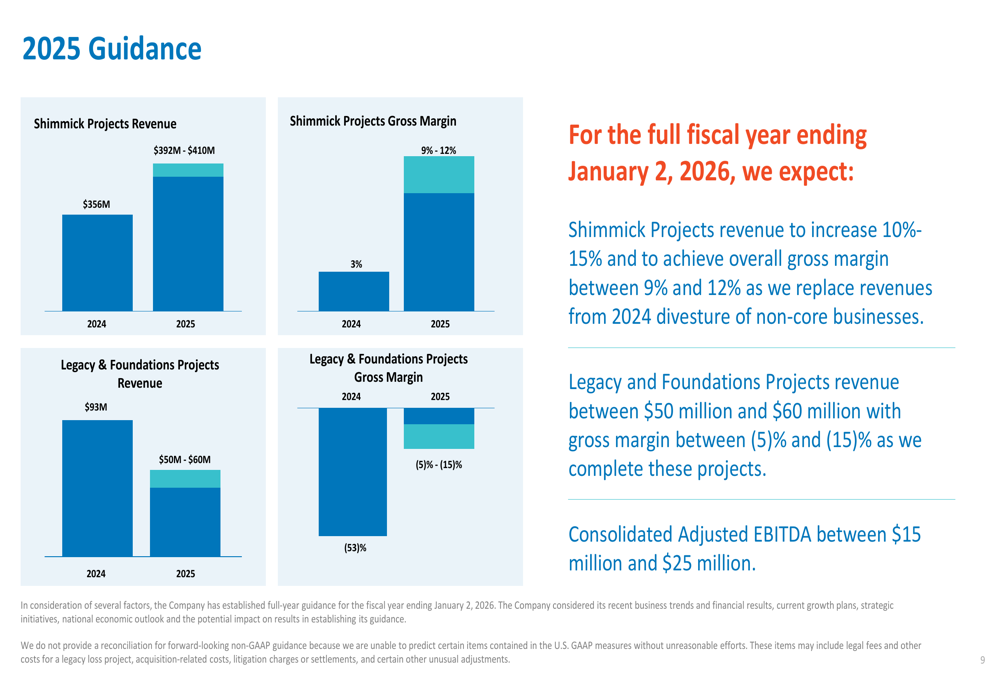

Shimmick reaffirmed its guidance for fiscal year 2025, projecting Shimmick Projects revenue between $392 million and $410 million, representing a 10-15% increase from $356 million in 2024. The company expects gross margins for this segment to improve significantly to between 9% and 12%, compared to 3% in 2024.

The following chart details the company’s 2025 guidance compared to 2024 performance:

For Legacy and Foundations Projects, Shimmick forecasts revenue to decline to between $50 million and $60 million in 2025, down from $93 million in 2024, as these projects continue to wind down. Gross margins for this segment are expected to improve to between negative 5% and negative 15%, compared to negative 53% in 2024.

Overall, the company projects consolidated Adjusted EBITDA between $15 million and $25 million for fiscal year 2025, suggesting confidence in its ability to continue improving financial performance.

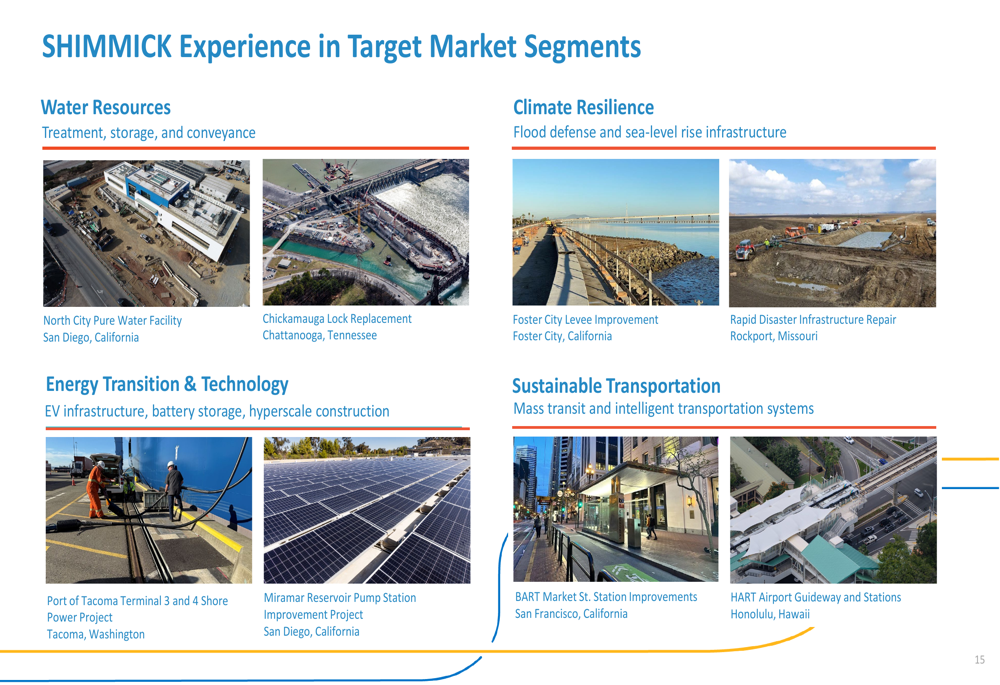

Shimmick is targeting four major end markets with a combined addressable market exceeding $100 billion: Water Resources, Climate Resilience, Energy Transition & Technology, and Sustainable Transportation. The company’s experience across these segments is illustrated in the following image:

While Shimmick’s Q1 2025 results show progress in its turnaround strategy, the company still faces challenges in achieving consistent profitability. Investors will be watching closely to see if management can deliver on its ambitious 2025 guidance and complete the transition away from problematic legacy projects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.