China smartphone shipments slumped in June on inventory overhang: Jefferies

Introduction & Market Context

Siemens AG (OTC:SIEGY) (ETR:SIE) presented its second quarter fiscal year 2025 results on May 15, highlighting robust performance despite increasing economic uncertainties. The German industrial technology giant reported 6% revenue growth and confirmed its full-year outlook, positioning itself as effectively navigating geopolitical shifts, protectionism concerns, and supply chain complexities while capitalizing on long-term growth drivers.

The company’s stock closed at €223.35 on May 14, near its 52-week high of €260, reflecting continued investor confidence in Siemens (ETR:SIEGn)’ strategic direction. The Q2 results follow a solid first quarter that saw 3% revenue growth, indicating accelerating momentum in the company’s performance.

Quarterly Performance Highlights

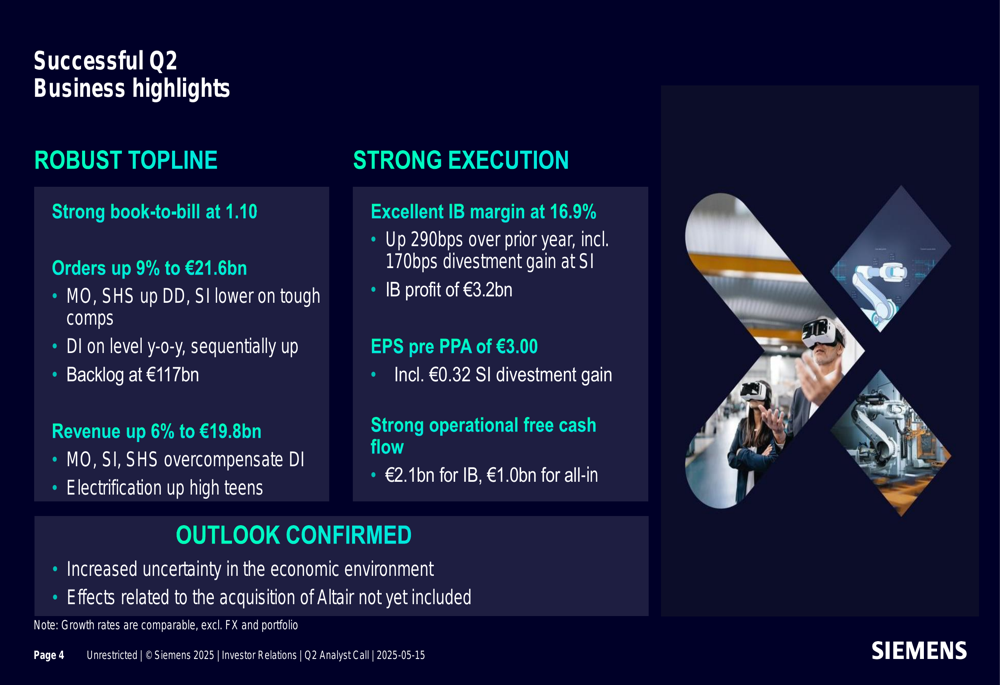

Siemens delivered strong Q2 results with orders up 9% to €21.6 billion and revenue increasing 6% to €19.8 billion. The book-to-bill ratio stood at a healthy 1.10, with total order backlog reaching €117 billion. The Industrial Business segment achieved an impressive 16.9% profit margin, generating €3.2 billion in profit and earnings per share (pre PPA) of €3.00.

As shown in the following comprehensive overview of Siemens’ Q2 performance:

Free cash flow remained robust, with the Industrial Business generating €2.1 billion and total free cash flow reaching €1.0 billion. This strong cash generation supports Siemens’ strategic investments and shareholder returns, including its progressive dividend policy and share buyback program.

The company maintained a strong balance sheet despite completing the Altair acquisition, with pension deficit at a historic low of €0.8 billion. Management emphasized that the capital structure remains well within target corridors following the acquisition.

Strategic Initiatives and Acquisitions

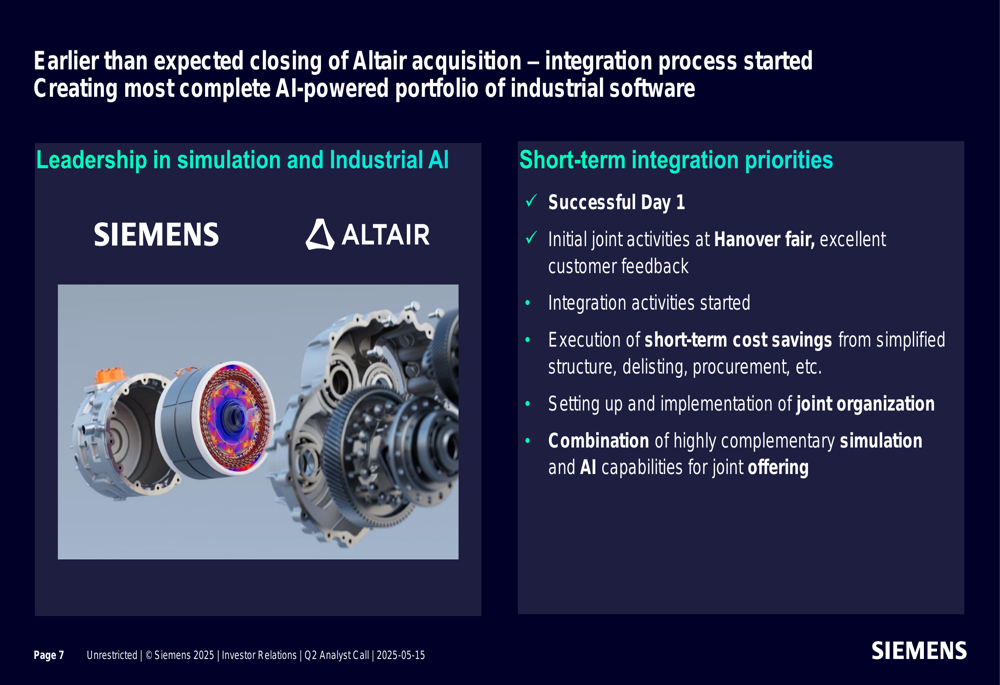

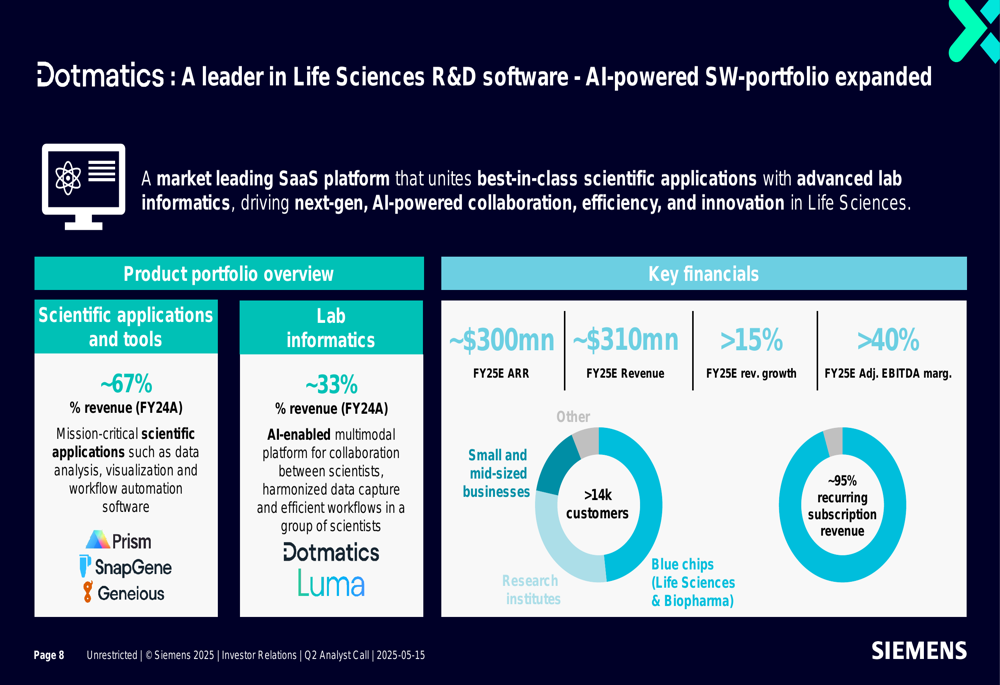

Siemens is advancing its "ONE Tech Company" program, focusing on stronger customer focus, faster innovations, and higher profitable growth. The company highlighted several strategic moves during the quarter, including the earlier-than-expected closing of the Altair acquisition and the signing of Dotmatics, a leader in Life Sciences R&D software.

The Altair acquisition strengthens Siemens’ simulation and AI capabilities, with integration activities already underway. The companies demonstrated initial joint activities at the Hanover Fair, showcasing the potential of their combined offerings.

The Dotmatics acquisition expands Siemens’ digital twin capabilities in life sciences, with key financial highlights including €300-310 million in annual recurring revenue (ARR), over 15% revenue growth, and over 40% EBITDA margin. This acquisition creates an end-to-end digital thread and positions Siemens as a leading player in life sciences PLM software.

At the Hanover Fair, Siemens showcased partnerships with industry leaders including Audi for automation, Microsoft (NASDAQ:MSFT) and NVIDIA (NASDAQ:NVDA) for XCELERATOR, and Accenture (NYSE:ACN) for Business Group. The company’s Industrial Copilot won the prestigious HERMES award, underscoring its innovation leadership.

Digital Business Transformation

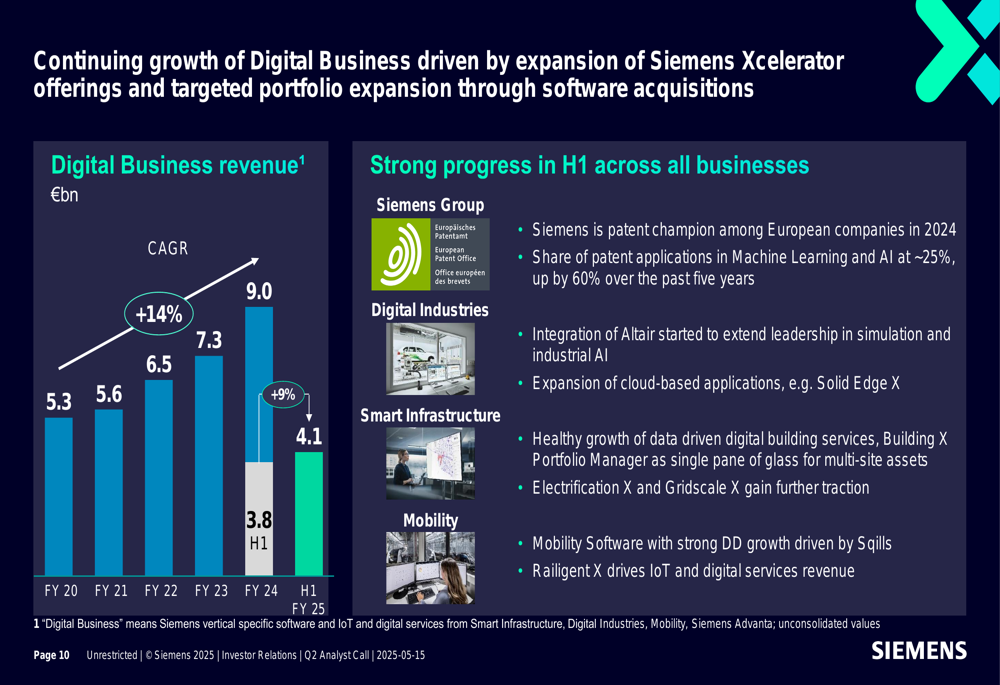

Siemens continues to make significant progress in its transformation into a technology company, with digital business revenue growing from €5.3 billion in FY20 to €9.0 billion in FY24, representing approximately 14% year-over-year growth.

The following chart illustrates this impressive digital business growth trajectory:

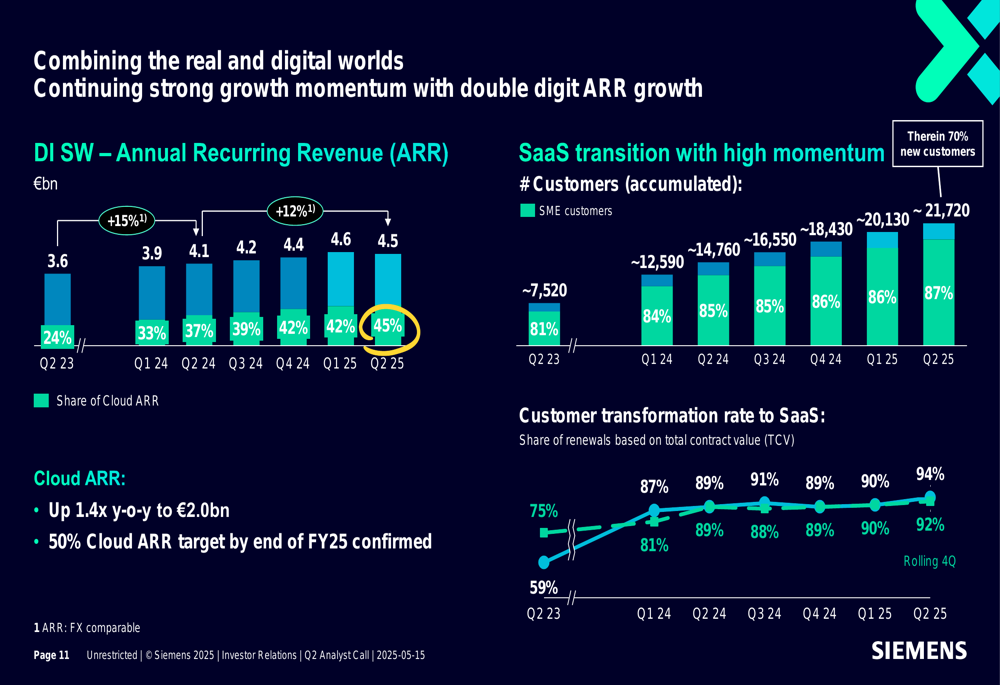

In the Digital Industries software business, annual recurring revenue (ARR) has increased from €3.6 billion to €4.5 billion, with the share of cloud ARR growing dramatically from 24% to 45%. The customer transformation rate to Software (ETR:SOWGn) as a Service (SaaS) has reached an impressive 94%, demonstrating strong customer adoption of Siemens’ cloud offerings.

Business Segment Performance

The performance across Siemens’ business segments showed varying results in Q2 FY2025:

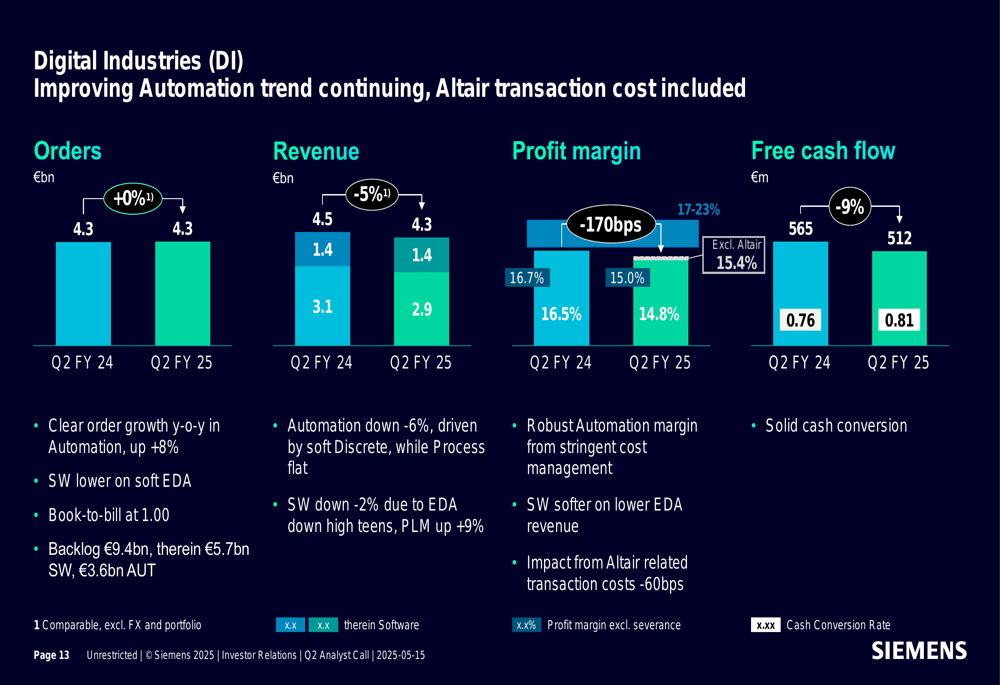

Digital Industries (DI) reported flat orders at €4.3 billion and a 5% revenue decline to €4.3 billion, with profit margin between 17-23%. The segment showed clear order growth and robust automation margins but was impacted by the Altair transaction. Free cash flow for DI was €512 million.

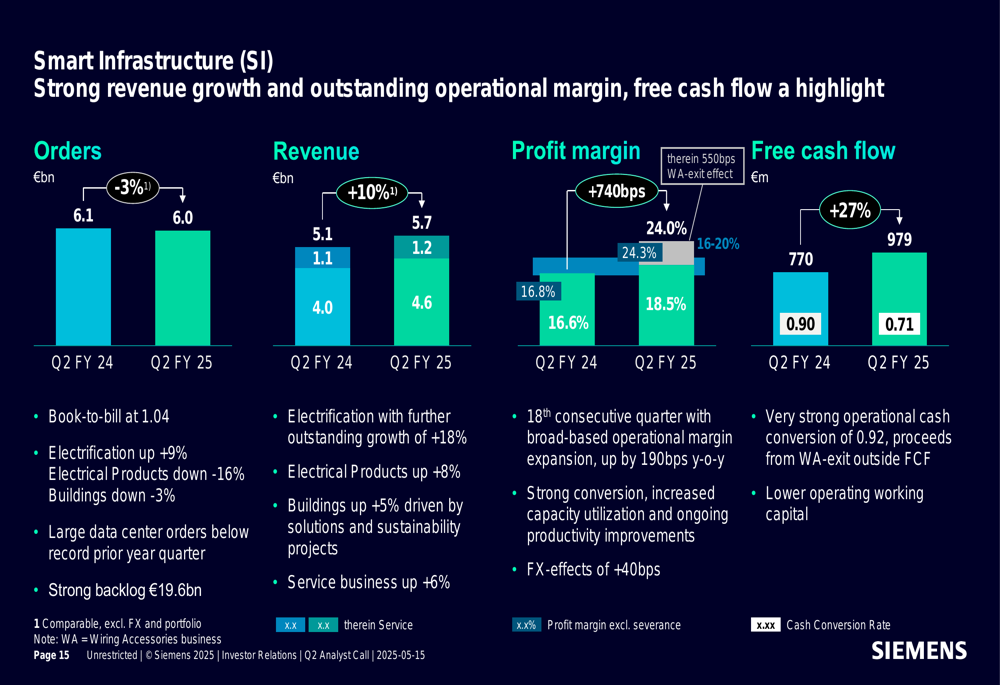

Smart Infrastructure (SI) delivered exceptional results with orders of €6.0 billion (-3%) but strong revenue growth of 10% to €5.7 billion. The profit margin improved by 740 basis points, with electrification showing outstanding growth of 18% and electrical products increasing by 8%. The segment’s backlog stands at €19.6 billion.

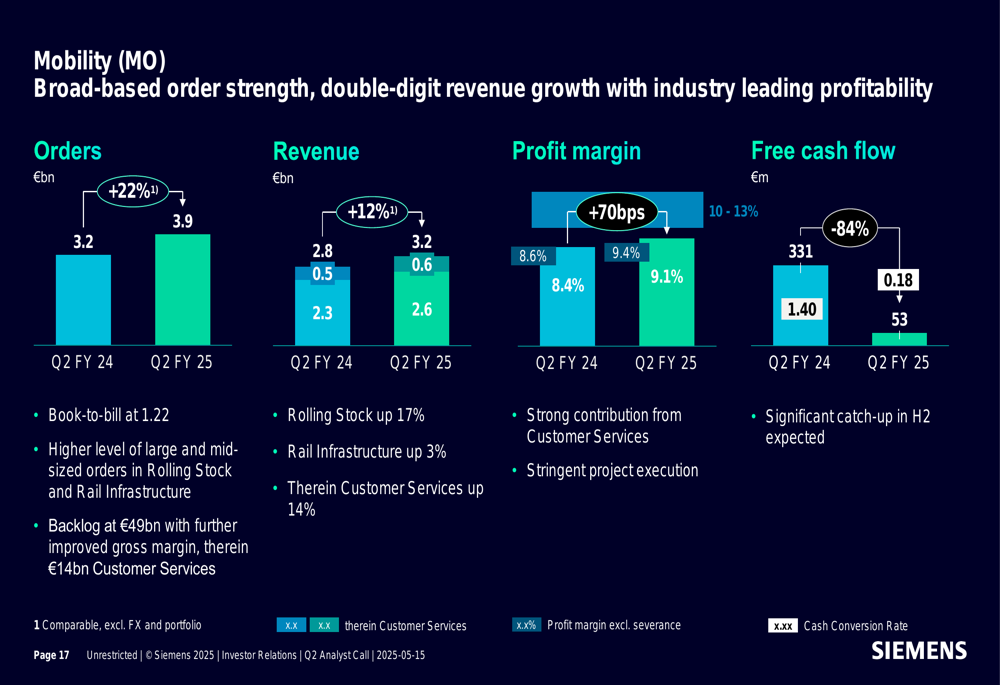

Mobility (MO) demonstrated strong performance with orders up 22% to €3.9 billion and revenue increasing 12% to €3.2 billion. The profit margin improved by 70 basis points, with a substantial backlog of €49 billion providing long-term visibility.

Regional Performance

Regional performance varied significantly across Siemens’ businesses. In Digital Industries, China showed remarkable order growth of 41%, while Germany declined by 16%. Italy grew by 12%, and the U.S. remained flat. Global software orders increased by 2%.

For Smart Infrastructure, the U.S. saw orders decline by 17%, while Germany and China grew by 13% and 15%, respectively. Europe overall showed modest growth of 2%, with global service revenue increasing by 6%.

Siemens emphasized its well-balanced global footprint as a strategic advantage in navigating tariff uncertainties. The company highlighted its strong U.S. presence with 28 factories and 48,000 employees, with 80% of its U.S. cost base sourced from within North America, limiting direct impact from potential tariff changes.

Forward-Looking Statements

Siemens confirmed its outlook for FY2025, projecting a book-to-bill ratio greater than 1, revenue growth of 3-7%, and EPS pre PPA of €10.40-€11.00. This guidance does not yet include effects related to the Altair acquisition.

The detailed outlook by business segment is illustrated in the following table:

For Digital Industries, Siemens expects revenue growth between -6% and 1% with a profit margin of 15-19%. Smart Infrastructure is projected to achieve 6-9% revenue growth with a 17-18% profit margin, while Mobility is expected to deliver 8-10% revenue growth with an 8-10% profit margin.

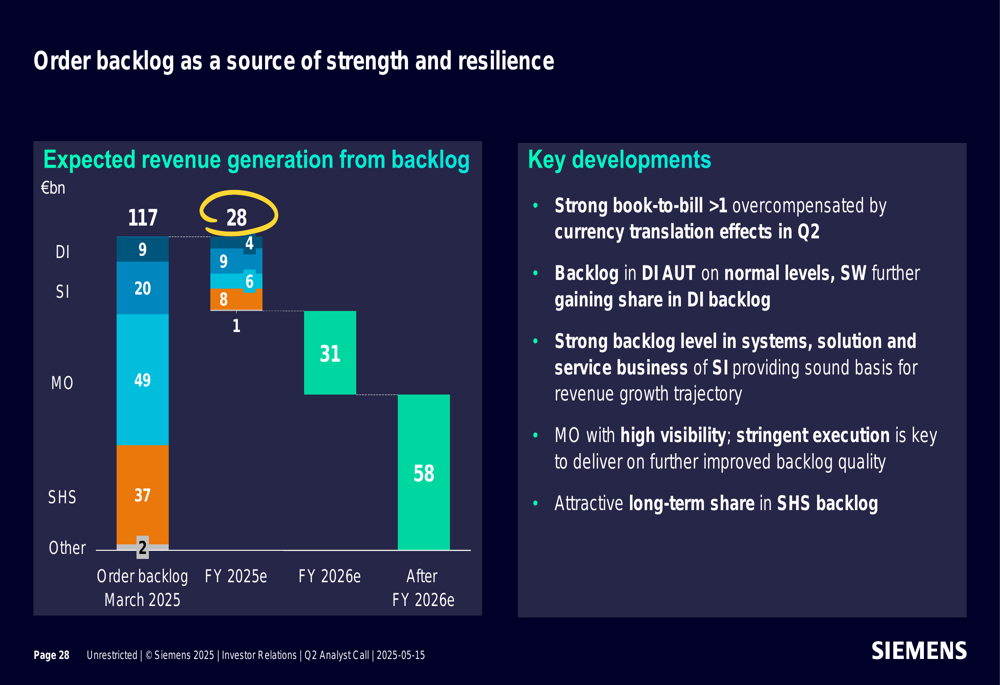

Management noted increased uncertainty in the economic environment but expressed confidence in the company’s ability to navigate these challenges. The company’s substantial order backlog of €117 billion provides a source of strength and visibility for future performance.

Siemens’ strategic positioning, strong financial performance, and continued investment in digital transformation and acquisitions demonstrate its commitment to long-term growth despite near-term economic uncertainties. With its balanced global footprint, robust digital business momentum, and strategic acquisitions, Siemens appears well-positioned to maintain its leadership in industrial technology and digital transformation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.