NVIDIA launches Jetson Thor robotics computers for physical AI systems

Introduction & Market Context

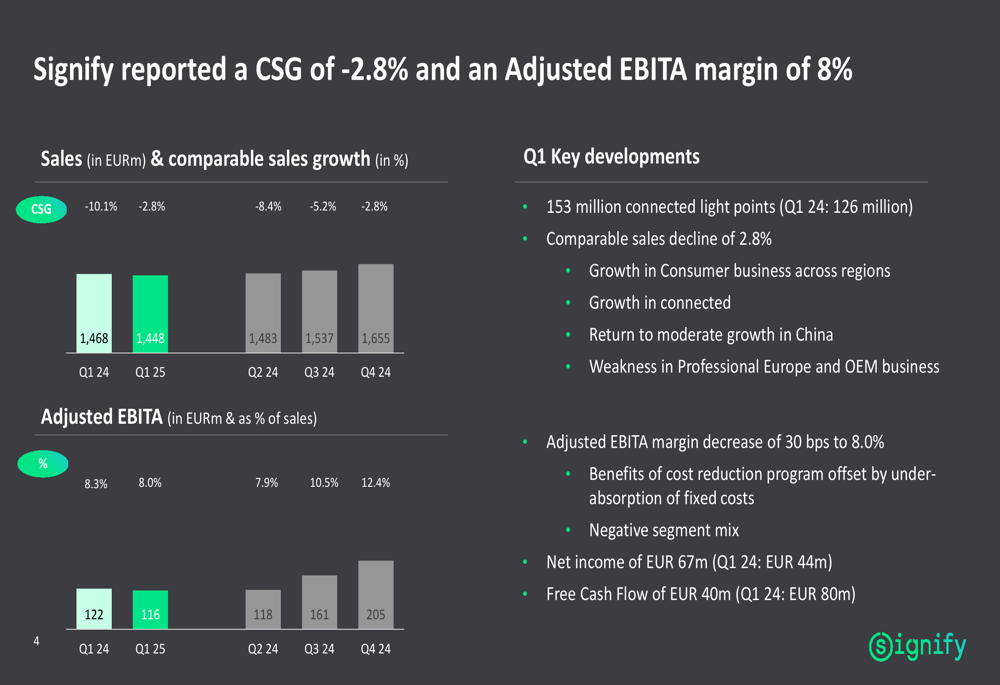

Signify NV ( AMS (VIE:AMS2):LIGHT) released its first quarter 2025 results on April 25, showing signs of gradual recovery despite an overall sales decline. The lighting manufacturer reported a comparable sales decline of 2.8%, a significant improvement from the 10.1% drop in the same period last year. Shares fell 1.47% to €19.03 following the announcement, as investors digested the mixed results across business segments.

The company highlighted sequential improvement in its Professional business and a return to growth in its Consumer segment, while the OEM business faced continued challenges. Signify maintained its full-year guidance, suggesting confidence in its recovery trajectory despite ongoing market headwinds.

Quarterly Performance Highlights

Signify reported Q1 2025 sales of €1,448 million, down slightly from €1,466 million in Q1 2024. The comparable sales decline of 2.8% represents a substantial improvement from the 10.1% decline in the same period last year. Adjusted EBITA reached €116 million with a margin of 8.0%, down 30 basis points from 8.3% in Q1 2024.

As shown in the following comprehensive results overview:

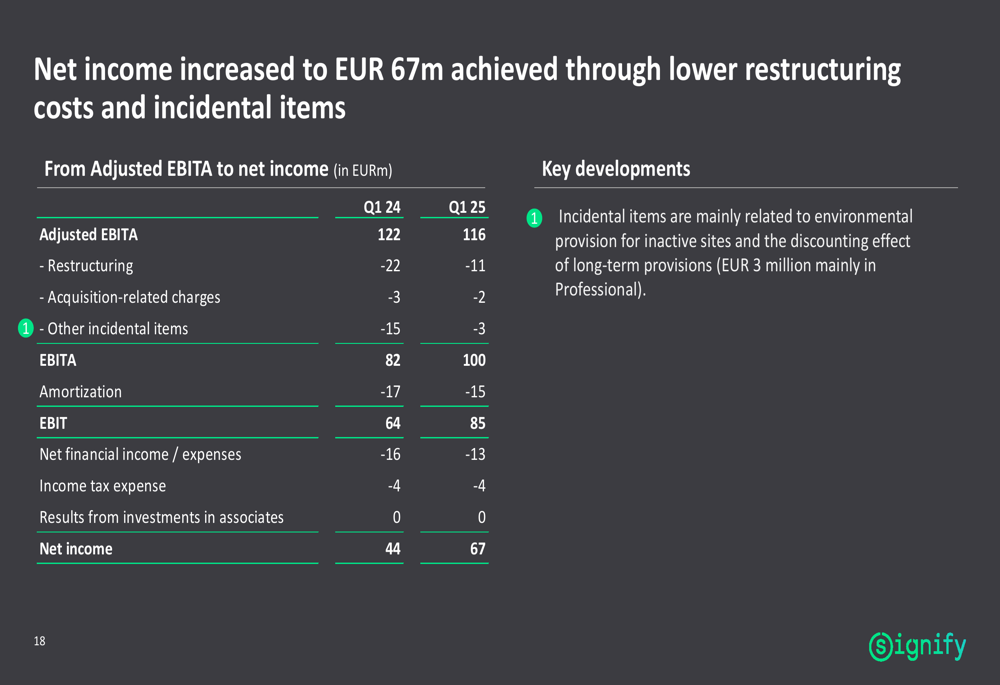

Net income increased significantly to €67 million, up from €44 million in Q1 2024, while free cash flow decreased to €40 million from €80 million in the prior year period. The company also reported reaching 153 million connected light points, underscoring its continued focus on digital lighting solutions.

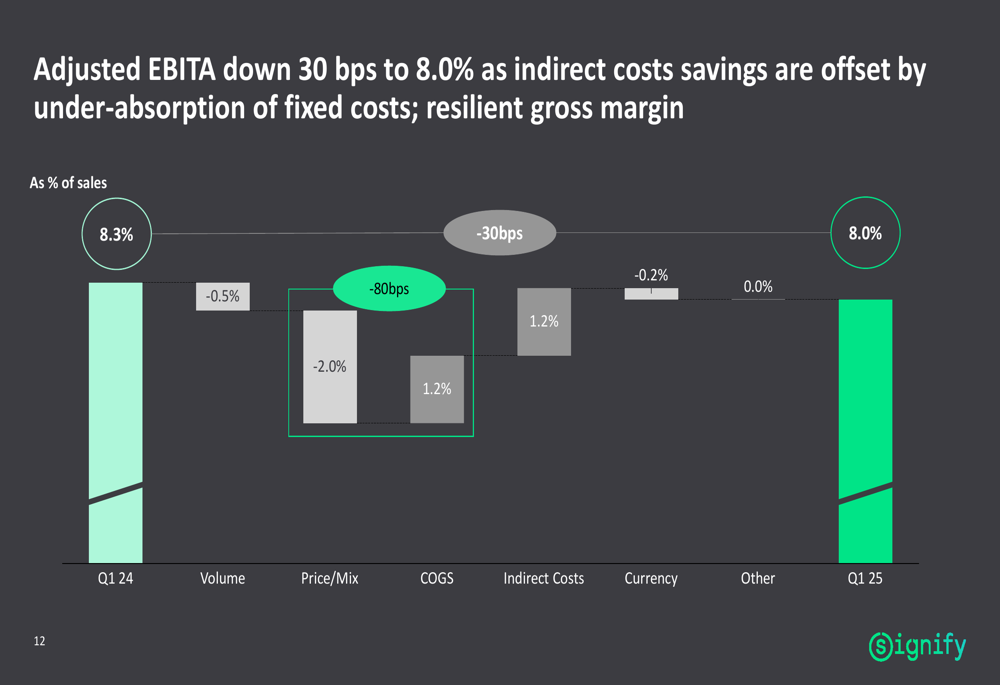

The Adjusted EBITA margin decline was primarily attributed to under-absorption of fixed costs and negative segment mix, partially offset by benefits from the company’s cost reduction program. The following bridge analysis illustrates the key factors affecting the margin:

Segment Performance Analysis

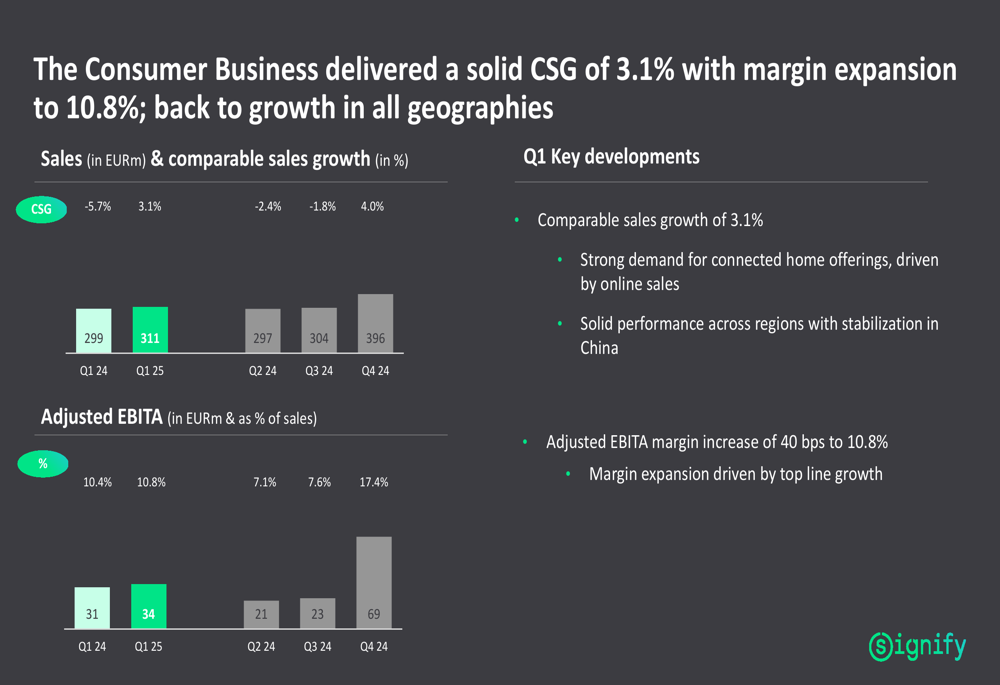

Signify’s Consumer business was the standout performer, delivering 3.1% comparable sales growth with an improved Adjusted EBITA margin of 10.8%. The segment benefited from strong demand for connected home offerings, particularly through online sales channels, and showed solid performance across all regions.

The following chart illustrates the Consumer segment’s return to growth:

The Professional business showed sequential improvement with a comparable sales decline of 1.8%, compared to a 7.6% decline in Q1 2024. The segment reported robust performance in agricultural lighting but continued to face softness in trade and public segments in Europe. Adjusted EBITA margin decreased slightly to 7.1% due to negative segment mix.

The OEM business faced the most significant challenges, with comparable sales declining by 10.7% and Adjusted EBITA margin dropping to 4.2% from 8.8% in Q1 2024. The company attributed half of this decline to two major customers and noted intensified pricing pressure in the component business.

The Conventional business continued its expected decline with comparable sales down 23.9%, yet maintained a strong Adjusted EBITA margin of 18.4%, actually improving from 17.6% in Q1 2024 due to positive price contributions.

Financial Analysis

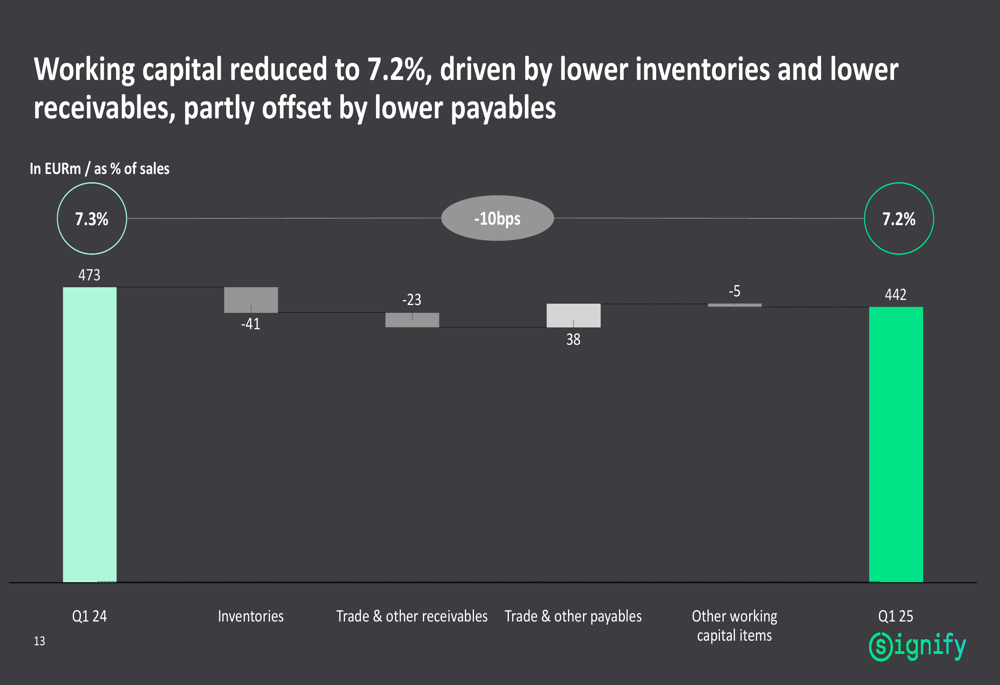

Signify’s working capital improved slightly to 7.2% of sales from 7.3% in Q1 2024, driven by lower inventories and receivables, partially offset by lower payables. The following chart shows this evolution:

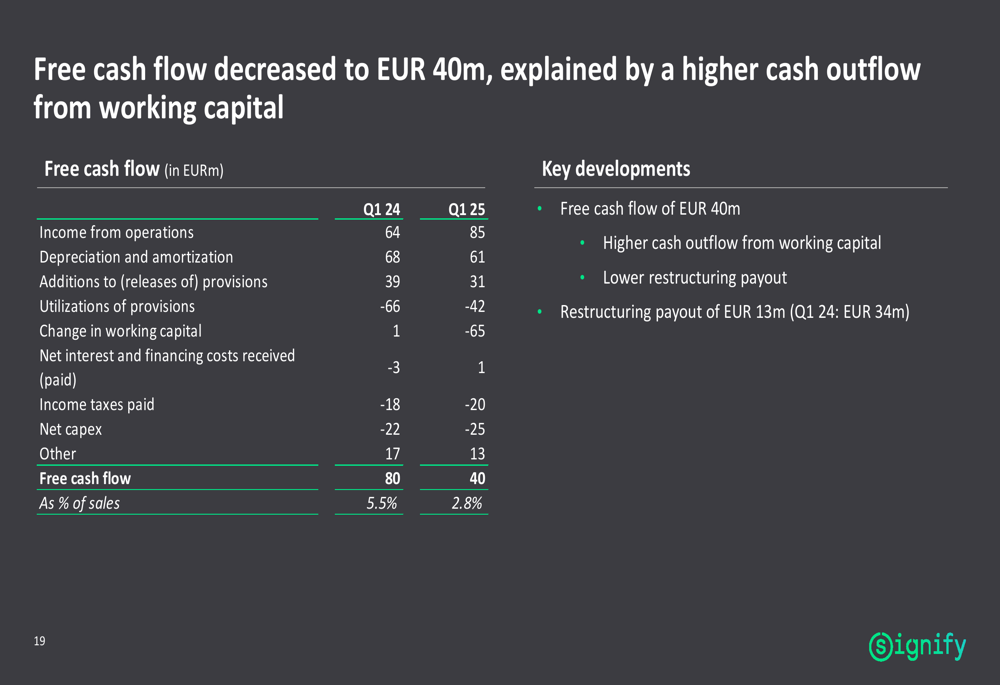

Free cash flow decreased to €40 million (2.8% of sales) from €80 million (5.5% of sales) in Q1 2024, primarily due to higher cash outflow from working capital, though this was partially offset by lower restructuring payouts.

The reconciliation from Adjusted EBITA to net income shows significant improvement in EBITA and EBIT compared to the previous year, primarily due to lower restructuring and other incidental costs:

The detailed free cash flow breakdown reveals the main factors affecting cash generation:

Sustainability Progress

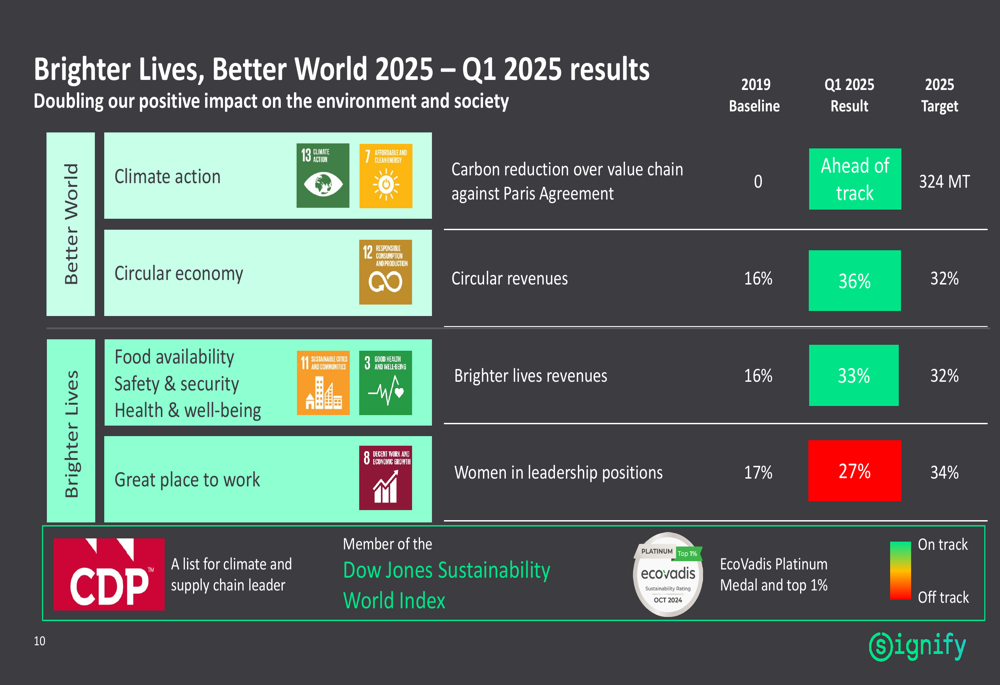

Signify continued to make progress on its "Brighter Lives, Better World 2025" sustainability program, reporting that it is ahead of track on carbon reduction across its value chain. The company achieved 36% circular revenues against a 2025 target of 32%, and 33% brighter lives revenues against the same target.

The following chart details Signify’s sustainability performance:

The company also highlighted its 15th rank among the Global 100 most sustainable corporations, reinforcing its commitment to environmental and social responsibility.

Outlook and Guidance

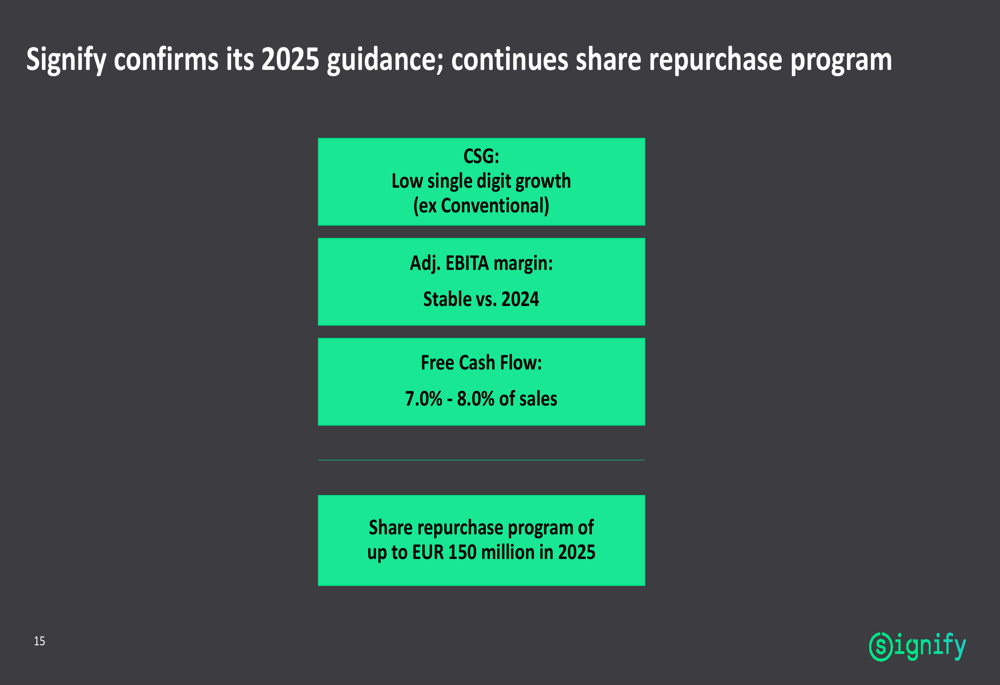

Signify confirmed its guidance for 2025, projecting low single-digit comparable sales growth (excluding the Conventional business), a stable Adjusted EBITA margin compared to 2024, and free cash flow of 7.0-8.0% of sales. The company also announced the continuation of its share repurchase program of up to €150 million in 2025.

The following slide outlines the company’s guidance for 2025:

While the first quarter showed mixed results across segments, management expressed confidence in the company’s trajectory, pointing to sequential improvements in sales performance and the return to growth in the Consumer business. The continued challenges in the OEM segment and the gradual recovery in Professional business will be key areas to watch in the coming quarters as Signify works toward achieving its full-year targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.