Gold bars to be exempt from tariffs, White House clarifies

Sila Realty Trust Inc (NYSE:SILA) has released its Q2 2025 supplemental information package, revealing stable performance across its healthcare real estate portfolio with continued high occupancy rates and modest growth in same-store cash NOI.

Quarterly Performance Highlights

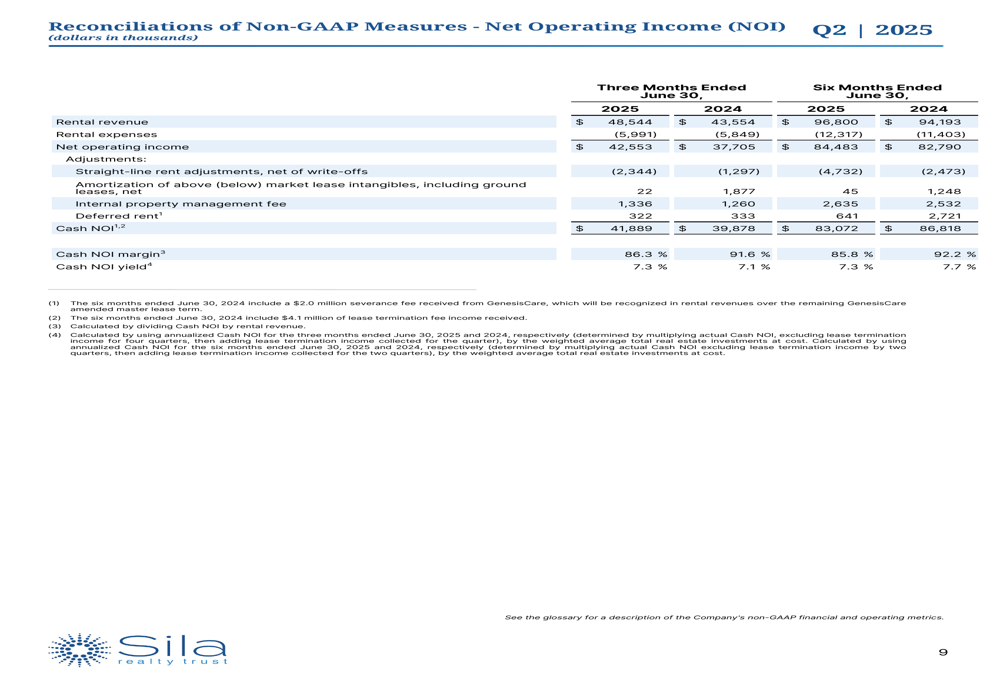

For the quarter ended June 30, 2025, Sila Realty Trust reported rental revenue of $48.54 million and net income attributable to common stockholders of $8.60 million. The company’s Funds From Operations (FFO) reached $30.01 million, while Core FFO and Adjusted FFO (AFFO) came in at $30.11 million and $29.56 million, respectively.

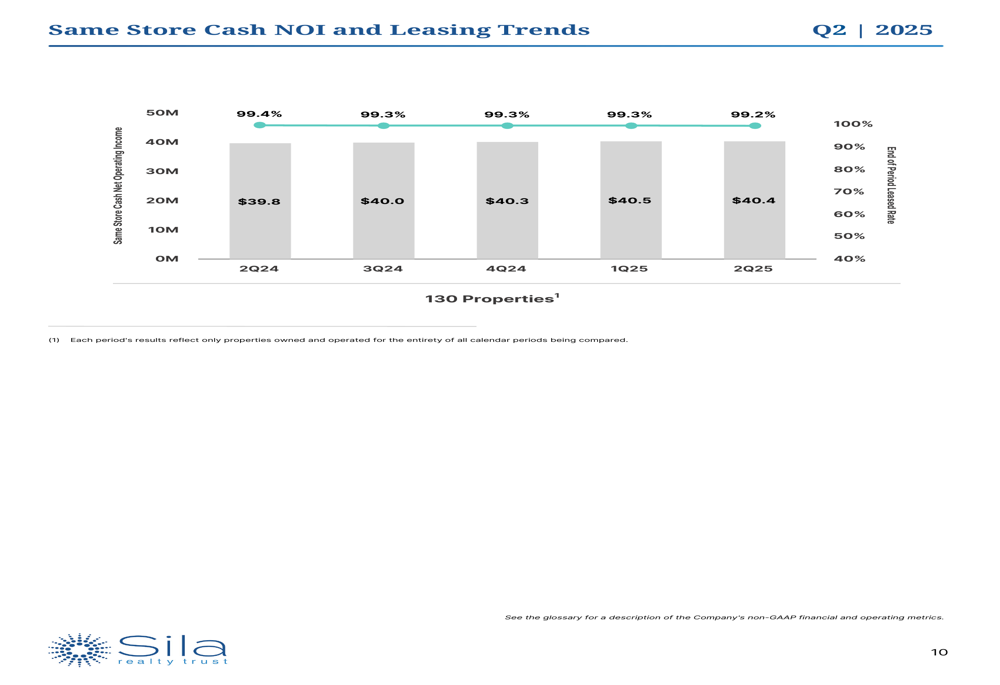

The REIT maintained its strong occupancy with a weighted average leased rate of 99.2%, only slightly down from 99.4% in the same quarter last year. Same-store cash NOI showed improvement, increasing from $39.8 million in Q2 2024 to $40.4 million in Q2 2025.

As shown in the following chart tracking same-store performance and occupancy rates:

The company’s cash NOI for Q2 2025 was $41.89 million with an impressive cash NOI margin of 86.3% and a cash NOI yield of 7.3%, demonstrating efficient property management and strong operational performance.

Portfolio Composition and Strategy

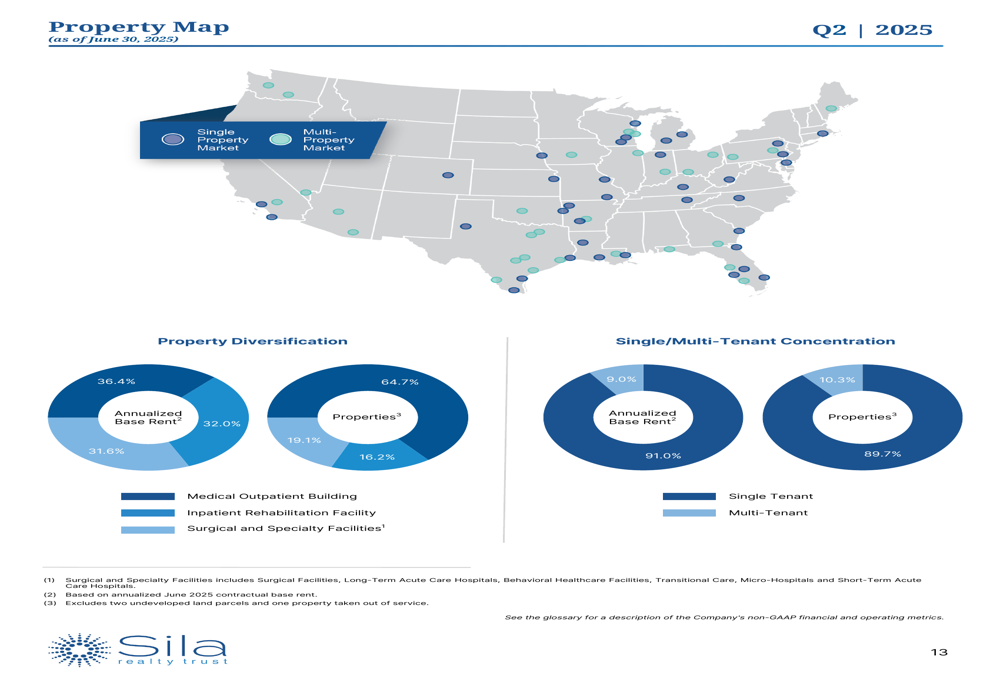

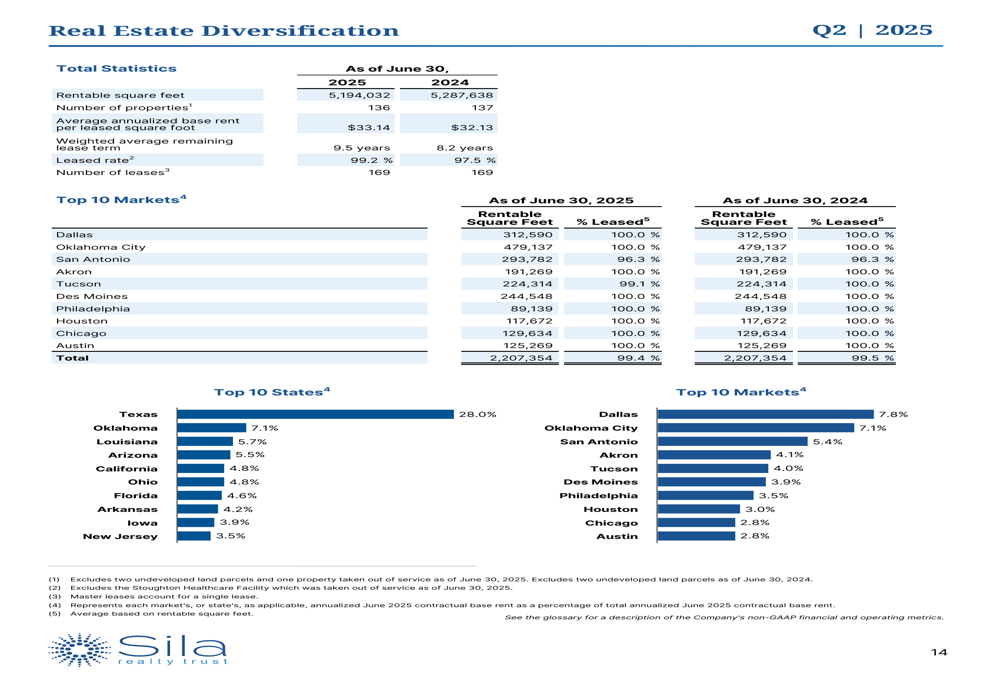

Sila Realty Trust’s portfolio comprised 136 properties as of June 30, 2025, with a well-balanced mix of healthcare facility types. The company’s annualized base rent is distributed across three main property categories: 36.4% from medical outpatient buildings, 31.6% from inpatient rehabilitation facilities, and 32.0% from surgical and specialty facilities.

The company’s geographic diversification and property type breakdown is illustrated in this comprehensive map:

The REIT maintains a strategic focus on single-tenant properties, which account for 91.0% of annualized base rent, while multi-tenant properties represent the remaining 9.0%. This approach aligns with the company’s emphasis on stable, long-term leases, as evidenced by its weighted average remaining lease term of 8.8 years.

Texas represents the company’s largest market concentration at 28% of assets, with Dallas specifically accounting for 7.8%. This geographic distribution is shown in the following visualization:

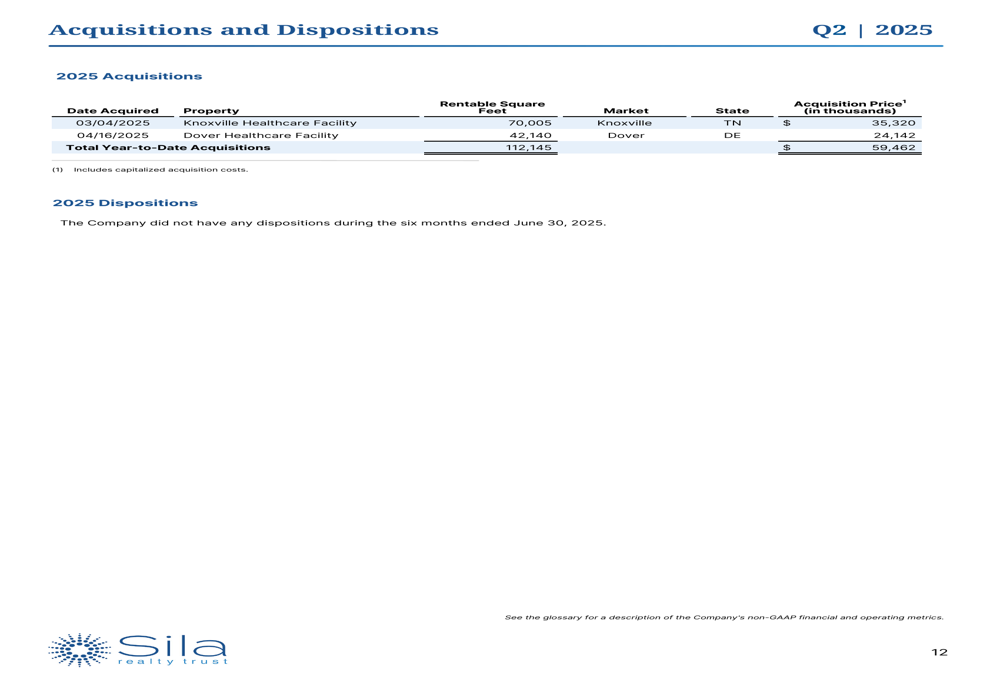

Year-to-date, Sila has completed two strategic acquisitions totaling $59.46 million: a 70,005 square foot healthcare facility in Knoxville, Tennessee for $35.32 million (acquired March 4, 2025) and a 42,140 square foot healthcare facility in Dover (NYSE:DOV), Delaware for $24.14 million (acquired April 16, 2025).

Financial Position and Debt Management

Sila Realty Trust maintains a disciplined approach to financial leverage. As of June 30, 2025, the company reported total debt of $581 million with a weighted average interest rate of 4.6%. The debt consists of $525 million in credit facility term loans and $56 million in revolving line of credit borrowings.

The REIT’s net debt to EBITDAre ratio stands at a conservative 3.6x, with a strong interest coverage ratio of 6.07x, indicating substantial capacity to meet its debt obligations.

The company’s debt maturity schedule and key financial ratios are presented in the following summary:

Total (EPA:TTEF) assets reached $2.02 billion as of June 30, 2025, with total stockholders’ equity of $1.36 billion. The company’s annualized distribution per share was $1.60, based on a stock price of $23.67 as reported in the presentation.

Tenant Quality and Lease Structure

The stability of Sila’s portfolio is further reinforced by the financial strength of its tenants. The company reports strong EBITDARM (Earnings Before Interest, Taxes, Depreciation, Amortization, Rent, and Management fees) coverage ratios across its property types, with medical outpatient buildings showing particularly robust tenant financial health.

The following chart illustrates the EBITDARM coverage ratios across different property types:

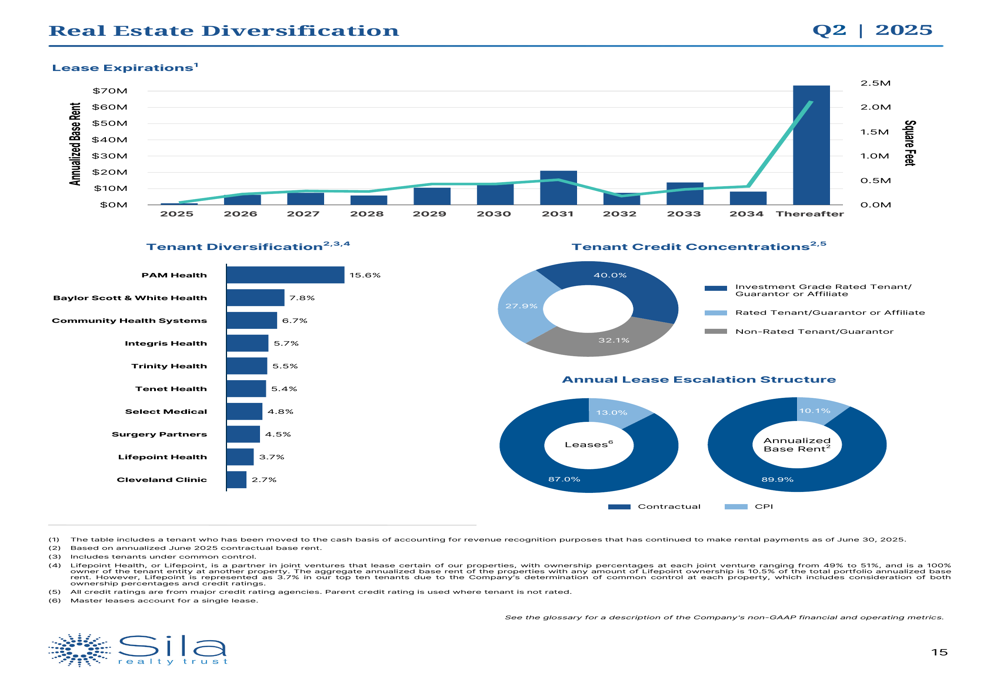

The company’s lease expiration schedule shows a well-staggered maturity profile, providing visibility into future rental income streams and limiting near-term re-leasing risk:

Market Context and Forward Outlook

Sila Realty Trust’s Q2 2025 performance follows a mixed Q1, where the company reported an EPS of $0.13, missing analyst expectations of $0.19, while revenue exceeded forecasts at $48.26 million versus an expected $45.41 million.

The current stock price of $25.41 represents a slight increase from the Q1 earnings report when it closed at $25.31, suggesting stable investor confidence in the company’s performance and strategy. The stock has traded between $21.29 and $27.50 over the past 52 weeks.

In previous guidance, the company targeted $150-$250 million in acquisitions for 2025, with $59.46 million already completed in the first half of the year. Management has emphasized a disciplined capital allocation strategy and cautious approach to leverage until stock prices recover further.

The company’s focus on healthcare real estate positions it to benefit from demographic trends, particularly the aging population, which CEO Michael Seaton previously described as "the silver tsunami" that "should drive the success of our tenants for decades to come."

With its high occupancy rates, diversified portfolio of necessity-based healthcare properties, and conservative financial management, Sila Realty Trust appears well-positioned to maintain stable performance in the healthcare REIT sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.