SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

Icelandic fishing company Sildarvinnslan hf (ICE:SVN) released its first quarter 2025 results on May 22, showing improved operational efficiency despite lower catch volumes. The company reported higher EBITDA margins even as it navigated challenges including a smaller-than-expected capelin fishing season, higher energy costs, and concerns about increased fishing taxes.

Sildarvinnslan’s stock closed at 79.00 ISK on the presentation date, trading near the lower end of its 52-week range of 77.50-102.00 ISK, reflecting investor caution about the mixed results and industry headwinds.

Quarterly Performance Highlights

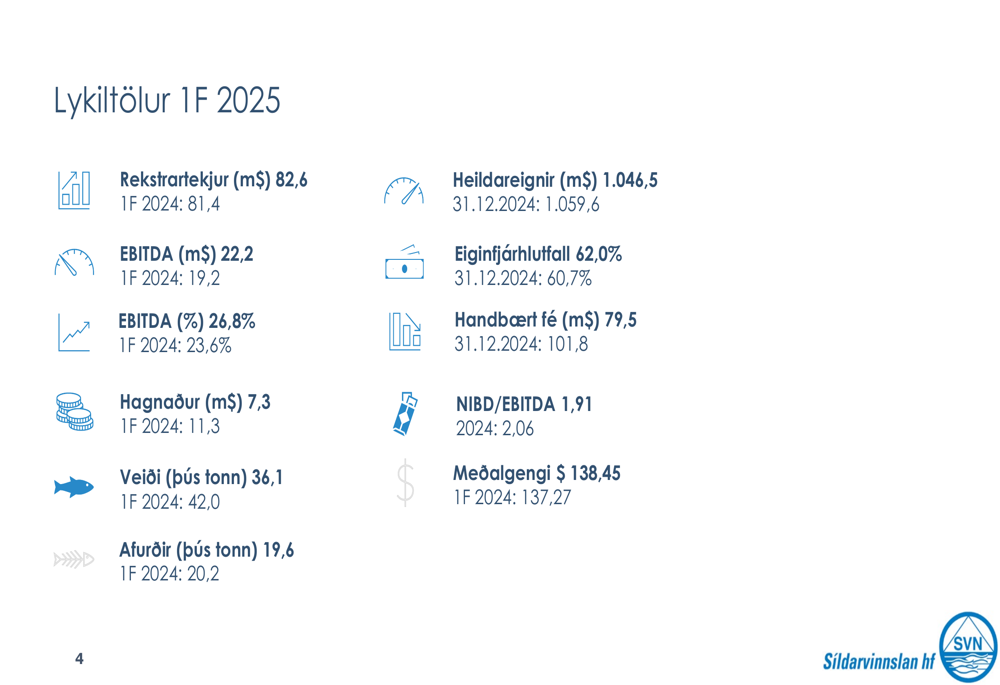

Sildarvinnslan reported Q1 2025 operating revenue of $82.6 million, a slight increase from $81.4 million in the same period last year. More significantly, EBITDA rose to $22.2 million (26.8% margin) from $19.2 million (23.6% margin) in Q1 2024, demonstrating improved operational efficiency despite challenges.

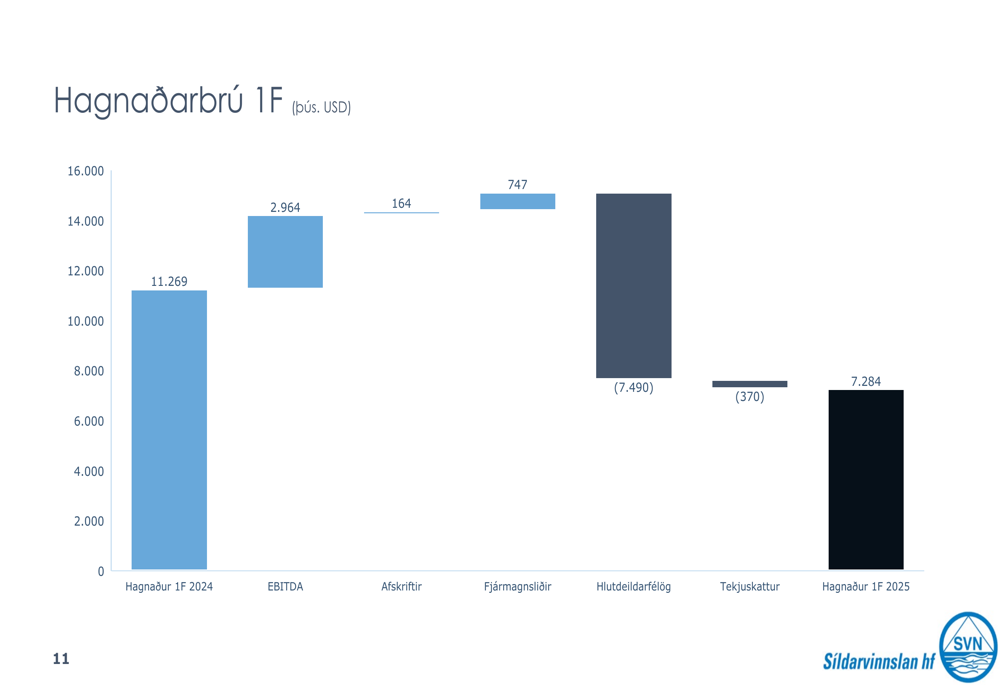

As shown in the following key figures chart, net profit declined to $7.3 million from $11.3 million in the prior-year period, primarily due to negative impacts from equity method investments:

The company maintained a strong balance sheet with an equity ratio of 62.0%, up from 60.7% at the end of 2024, while cash on hand decreased to $79.5 million from $101.8 million, partly due to investments made during the quarter.

Total (EPA:TTEF) catch volume declined to 36.1 thousand tons from 42.0 thousand tons in Q1 2024, while production volume decreased slightly to 19.6 thousand tons from 20.2 thousand tons.

Detailed Financial Analysis

The income statement reveals that while operating revenue increased slightly, the company managed to reduce cost of goods sold by $1.8 million compared to Q1 2024, contributing to the improved EBITDA:

The profit bridge analysis clearly illustrates how the $3.0 million EBITDA improvement was more than offset by a $7.5 million negative impact from equity investments, resulting in the overall profit decline:

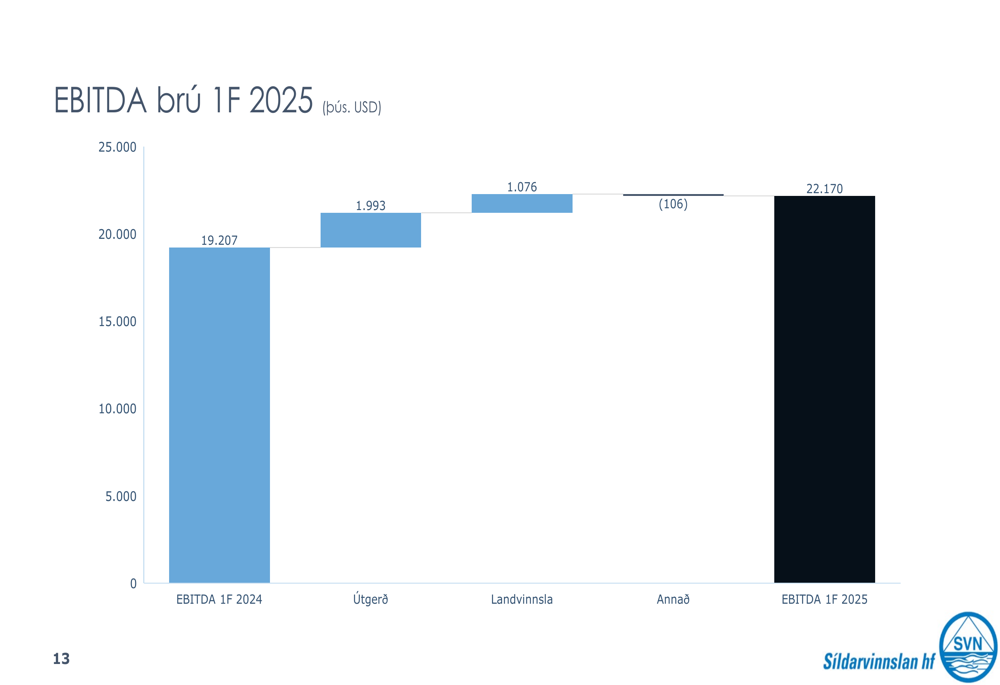

Breaking down EBITDA by segment shows that both the Outward and Land Based segments contributed positively to the EBITDA improvement, while the "Other" segment had a slight negative impact:

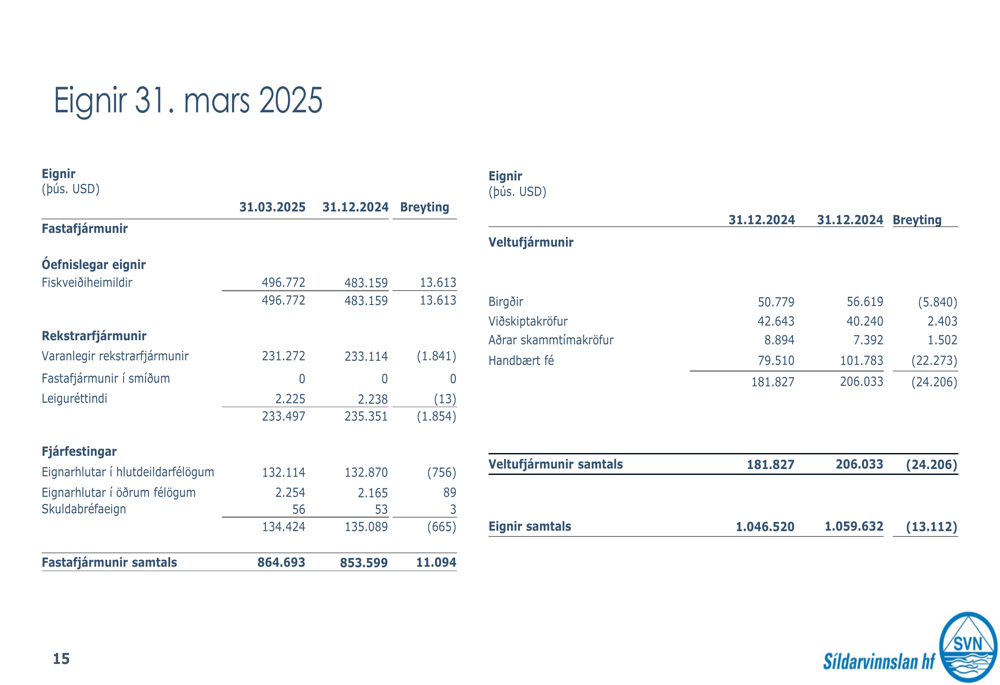

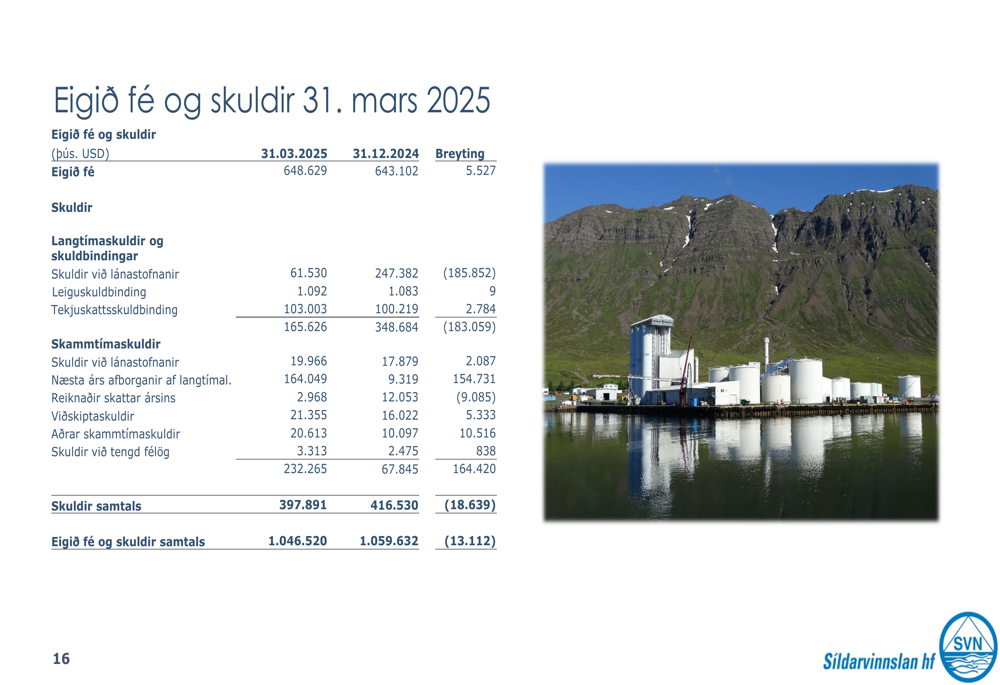

The company’s asset position remained strong at $1.05 billion, with a slight decrease from $1.06 billion at the end of 2024:

The equity and liabilities side shows an increase in equity to $648.6 million from $643.1 million, while total liabilities decreased to $397.9 million from $416.5 million:

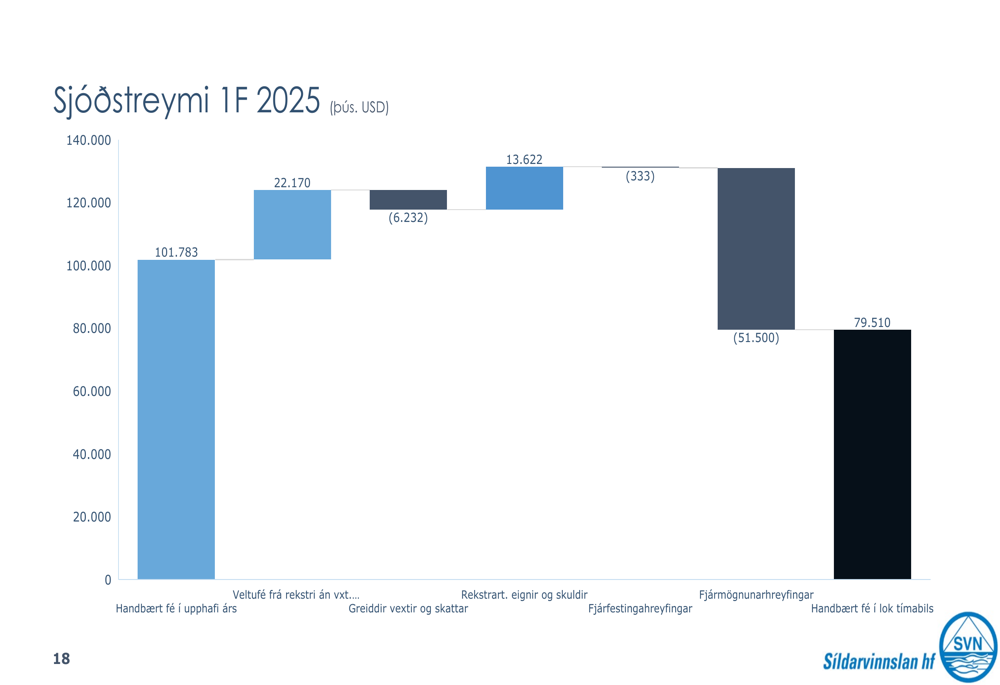

Cash flow analysis shows that strong operational cash generation of $22.2 million was offset by investments of $51.5 million, interest and taxes of $6.2 million, resulting in the cash position declining to $79.5 million:

Strategic Initiatives & Market Outlook

Sildarvinnslan highlighted several positive market developments in its presentation. The mackerel outlook is described as "very good" with empty markets and high demand ahead of the season starting in July. Herring sales have performed well, though with increased competition from Norwegian and Faroese producers.

The company noted that capelin sales have been successful despite prices nearly tripling, with two-thirds of produced roe already delivered. However, at less than 4,000 tons produced, this was "the smallest season seen."

In the demersal (groundfish) segment, the company is benefiting from high demand for cod products due to quota reductions in the Barents Sea. Sea-frozen cod and haddock products are achieving record prices in the UK market, while Greenland halibut prices are rising in Asia.

Forward-Looking Statements

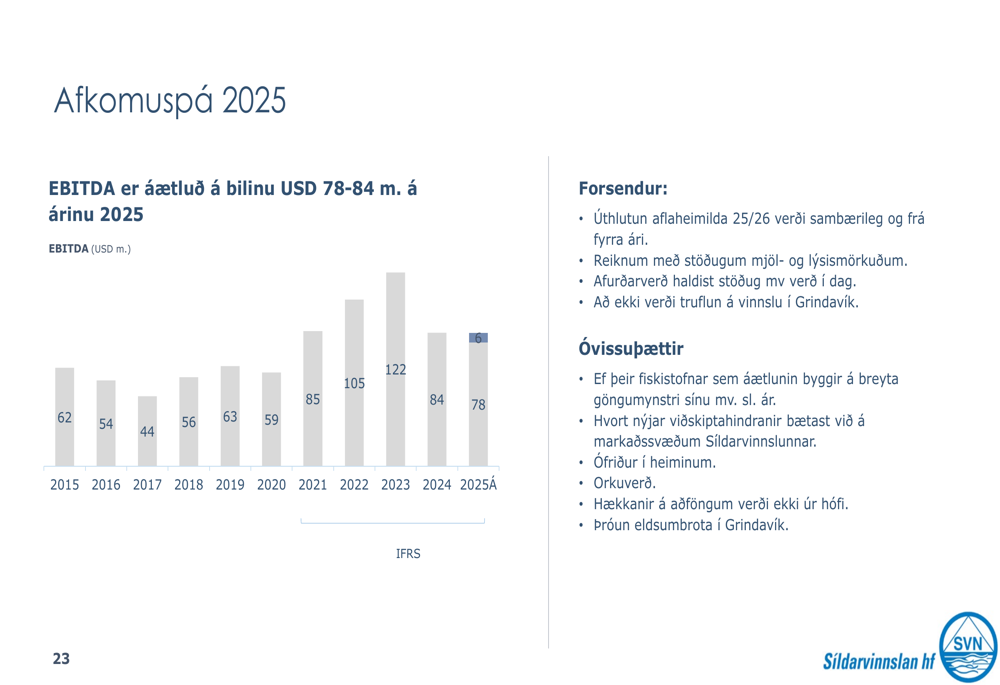

For the full year 2025, Sildarvinnslan projects EBITDA between $78-84 million, as illustrated in the following forecast:

This guidance is based on assumptions including steady quotas, stable commodity prices, and no disruptions in Grindavik. The company identified several uncertainty factors, including fishing area stability, potential trade barriers, geopolitical conflicts, energy prices, and volcanic activity in Grindavik.

Management expressed concerns about announced increases in fishing taxes that they claim will "hurt the company badly," while also highlighting that the return on equity of 6.9% in 2024 and return on market value of 3.5% were "far below the return on risk-free bank deposits."

Despite these challenges, Sildarvinnslan’s improved operational efficiency and strong market conditions for key products suggest the company is positioned to navigate the complex industry environment, though external factors continue to present significant headwinds to bottom-line performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.