Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Silicon Laboratories Inc (NASDAQ:SLAB) presented its Q1 2025 investor update on May 13, 2025, showcasing accelerating revenue growth and significant year-over-year improvements across key business segments. The company, which positions itself as "The Leading Innovator in Low-Power Connectivity," has demonstrated strong momentum in its targeted Internet of Things (IoT) markets.

The presentation revealed that Silicon Labs’ strategic focus on embedded wireless technology is yielding substantial results, with total revenue reaching $178 million in Q1 2025, representing a 68% increase from the $106 million reported in Q1 2024. This growth comes amid what the company describes as an accelerating IoT adoption environment, with projections of more than 10 billion devices per year by 2035.

As shown in the following financial performance chart, Silicon Labs has maintained consistent sequential revenue growth over five consecutive quarters:

Quarterly Performance Highlights

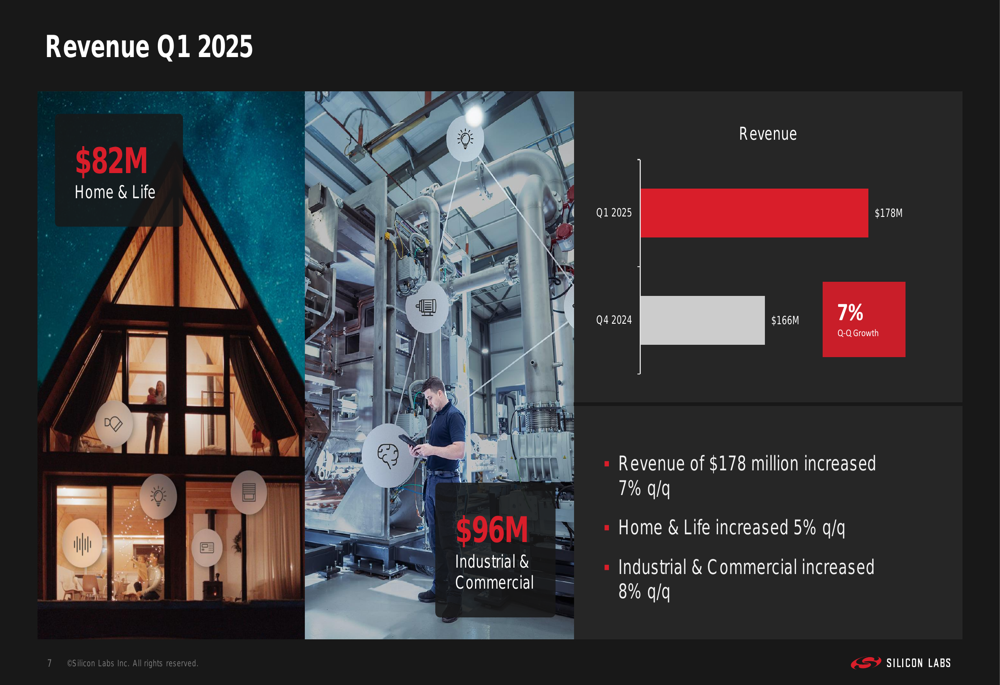

Silicon Labs reported Q1 2025 revenue of $178 million, a 7% increase quarter-over-quarter and a 68% jump year-over-year. This performance was driven by strong results in both of the company’s primary business segments.

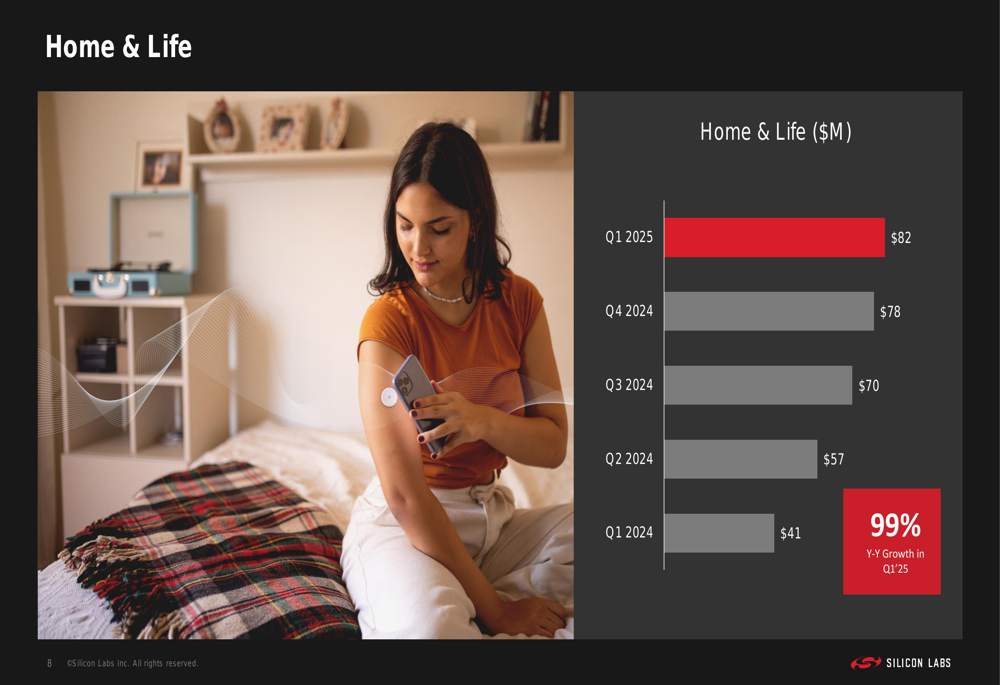

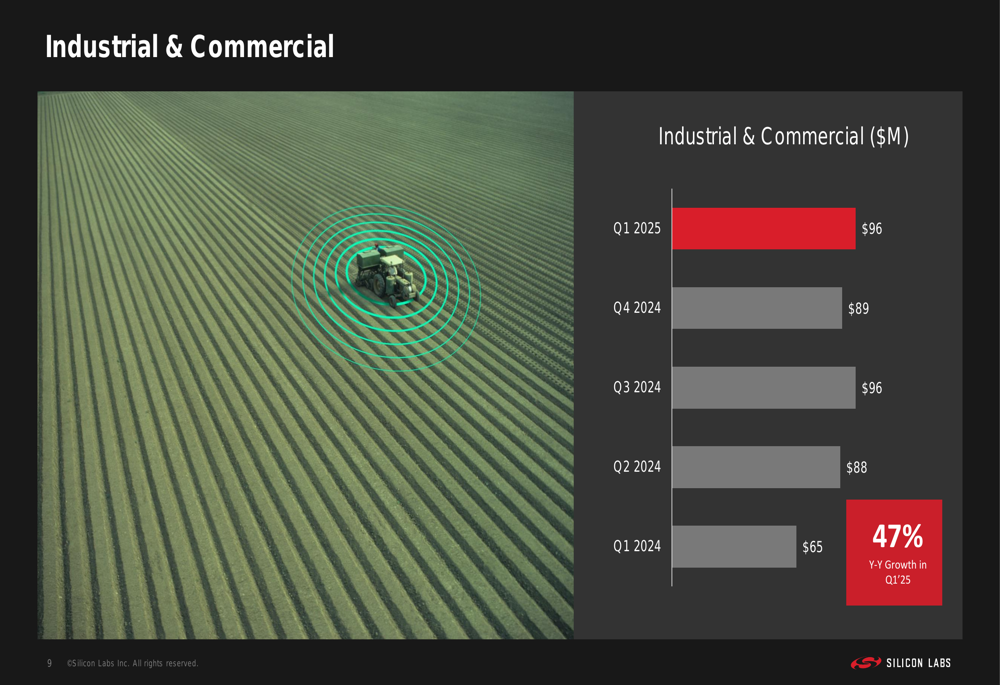

The Home & Life segment generated $82 million in revenue, up 5% sequentially and an impressive 99% year-over-year. Meanwhile, the Industrial & Commercial segment contributed $96 million, increasing 8% from the previous quarter and 47% compared to the same period last year.

The following chart illustrates the company’s Q1 2025 revenue breakdown by segment:

The exceptional year-over-year growth in the Home & Life segment demonstrates Silicon Labs’ successful penetration of consumer-oriented IoT markets:

Similarly, the Industrial & Commercial segment has shown robust performance, reflecting the company’s strong position in industrial IoT applications:

Detailed Financial Analysis

Silicon Labs reported improvements in its gross margin during Q1 2025. GAAP gross margin increased to 55.0%, up from 54.3% in the previous quarter, while non-GAAP gross margin rose to 55.4% from 54.6% in Q4 2024. These margin improvements occurred despite the significant scaling of revenue, indicating effective cost management and operational efficiency.

On the earnings front, the company reported a GAAP loss per share of $(0.94) in Q1, compared to $(0.73) in Q4. However, on a non-GAAP basis, the loss per share improved by 27% to $(0.08) from $(0.11) in the previous quarter, suggesting progress toward profitability as revenue continues to scale.

The company’s balance sheet showed significant strength, with cash and short-term investments increasing to $425 million from $382 million in the previous quarter. Silicon Labs maintains zero debt, providing substantial financial flexibility for future investments and growth initiatives.

Notably, Silicon Labs has made remarkable progress in inventory management, with days of inventory on hand reduced to 94 days in Q1 2025, down from 125 days in the previous quarter and a dramatic improvement from 407 days in Q4 2023. This inventory optimization reflects both improved demand and more efficient supply chain management.

The following slide details the company’s balance sheet highlights:

Forward-Looking Statements

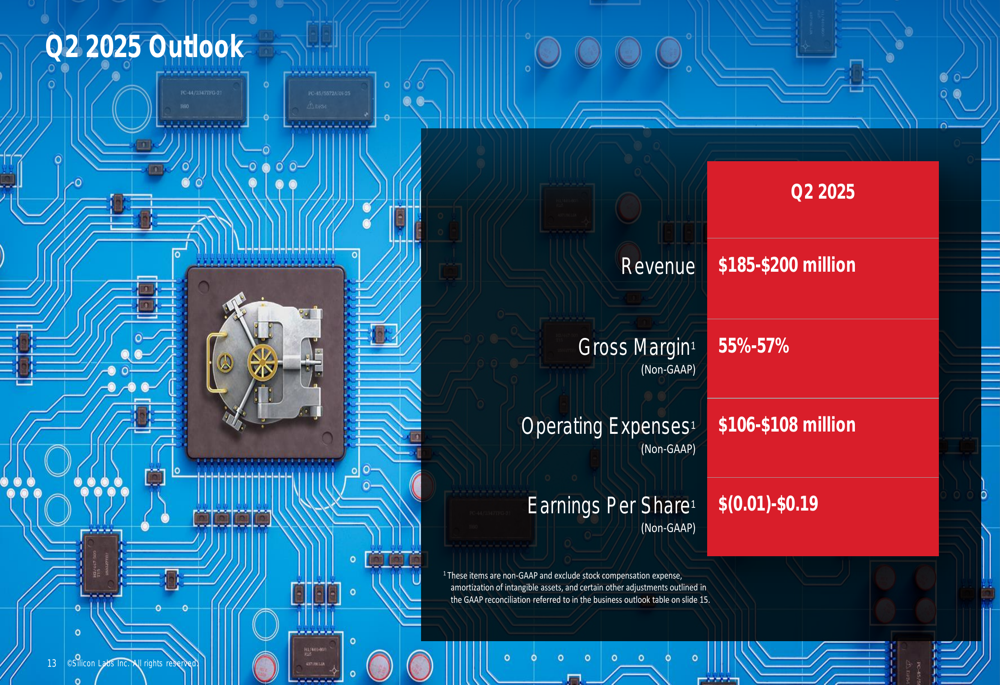

For Q2 2025, Silicon Labs provided guidance that suggests continued strong performance. The company expects revenue between $185 million and $200 million, with the midpoint of $192.5 million representing a 32% year-over-year increase. Non-GAAP gross margin is projected to be between 55% and 57%, indicating potential further improvement from Q1 levels.

Operating expenses on a non-GAAP basis are expected to be between $106 million and $108 million, while non-GAAP earnings per share are forecast to range from a loss of $(0.01) to a profit of $0.19, potentially marking the company’s return to profitability.

The detailed Q2 2025 outlook is presented in the following slide:

Strategic Initiatives

Silicon Labs’ presentation emphasized its strategic focus on high-growth IoT markets, targeting a 15-25% revenue growth rate, which it claims is approximately three times the broader semiconductor market growth rate. This strategy is built on the company’s track record of outperformance and market share gains in specific IoT segments.

The company highlighted that it has captured approximately $10 billion in design wins, which are expected to drive future revenue growth. Silicon Labs identified several high-potential growth areas, including continuous glucose monitoring (CGM), electronic shelf labels (ESL), smart meters, Matter-enabled devices, and Bluetooth applications.

The following slide outlines Silicon Labs’ market selection strategy and growth opportunity:

Silicon Labs also emphasized its customer diversification, noting that its largest customer represents less than 10% of revenue, and the company has approximately 125 customers generating more than $1 million in annual revenue. Geographically, the largest region accounts for 36% of revenue, with China representing approximately 15%.

The company’s innovation efforts have been recognized through multiple industry awards, including the 2024 IoT Evolution Product of the Year Award and Embedded World 2025 Best in Show for its MG26 SoC, demonstrating its technological leadership in the IoT connectivity space.

Market Reaction

Silicon Labs’ stock (NASDAQ:SLAB) closed at $126.31 on May 12, 2025, and was trading up 2.53% at $129.50 in pre-market trading following the presentation. The stock has shown significant volatility over the past year, with a 52-week range of $82.82 to $160.00.

The strong financial results and positive outlook presented in the investor slides appear to be supporting investor confidence in the company’s growth strategy and execution. With its focus on high-growth IoT markets, improving operational efficiency, and strong balance sheet, Silicon Labs is positioning itself to capitalize on the accelerating adoption of IoT technologies across both consumer and industrial applications.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.