InvestingPro’s Fair Value model captures 63% gain in Steelcase ahead of acquisition

Introduction & Market Context

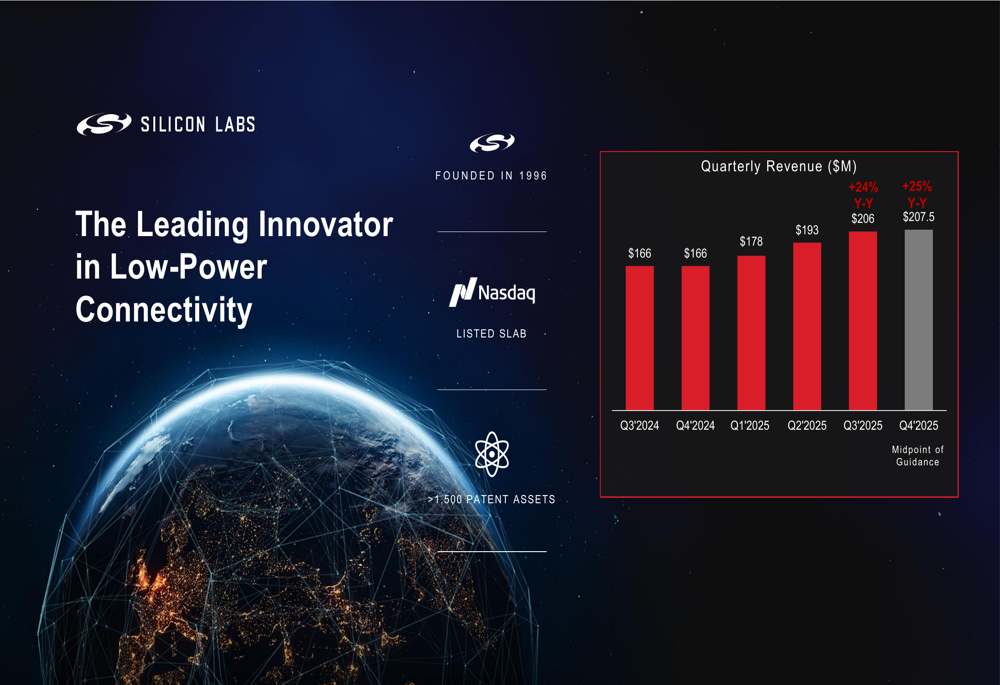

Silicon Laboratories Inc (NASDAQ:SLAB), a leading innovator in low-power connectivity solutions, presented its Q3 2025 investor presentation on November 4, 2025, highlighting strong financial performance despite a challenging market environment. The company, founded in 1996, has positioned itself as a key player in the rapidly expanding Internet of Things (IoT) market, which is forecast to reach over 10 billion devices annually by 2035.

As shown in the following revenue chart, Silicon Labs has demonstrated consistent quarterly growth throughout 2025:

Quarterly Performance Highlights

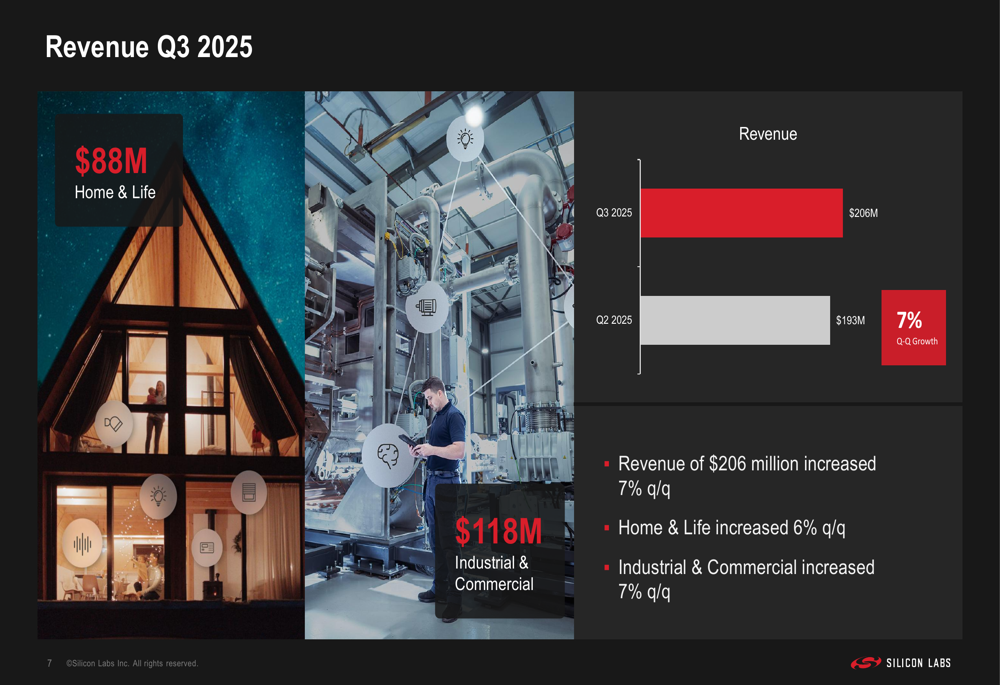

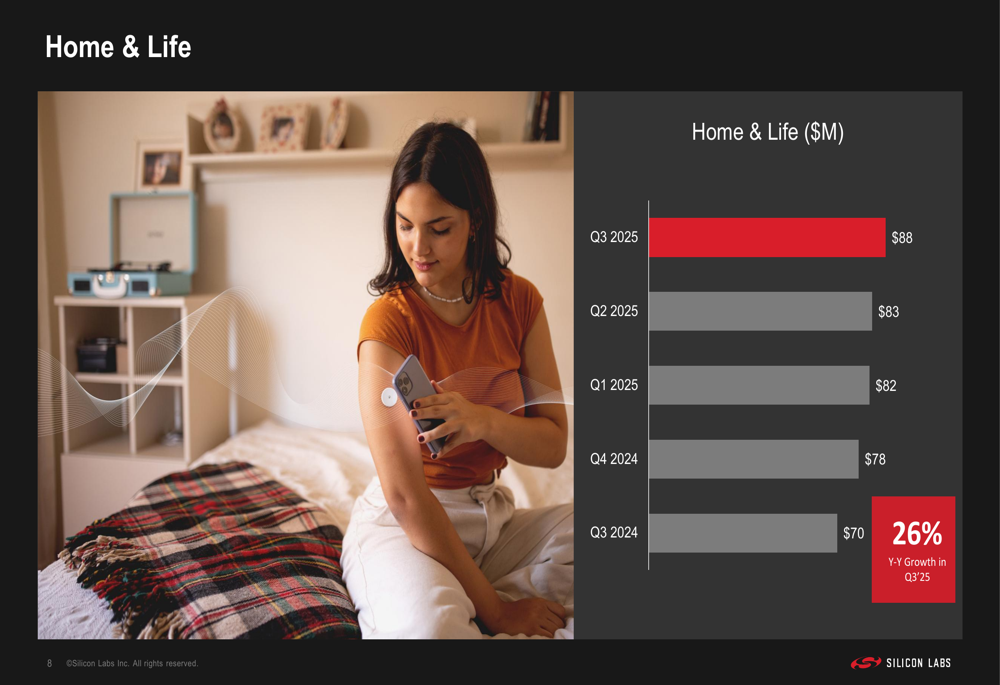

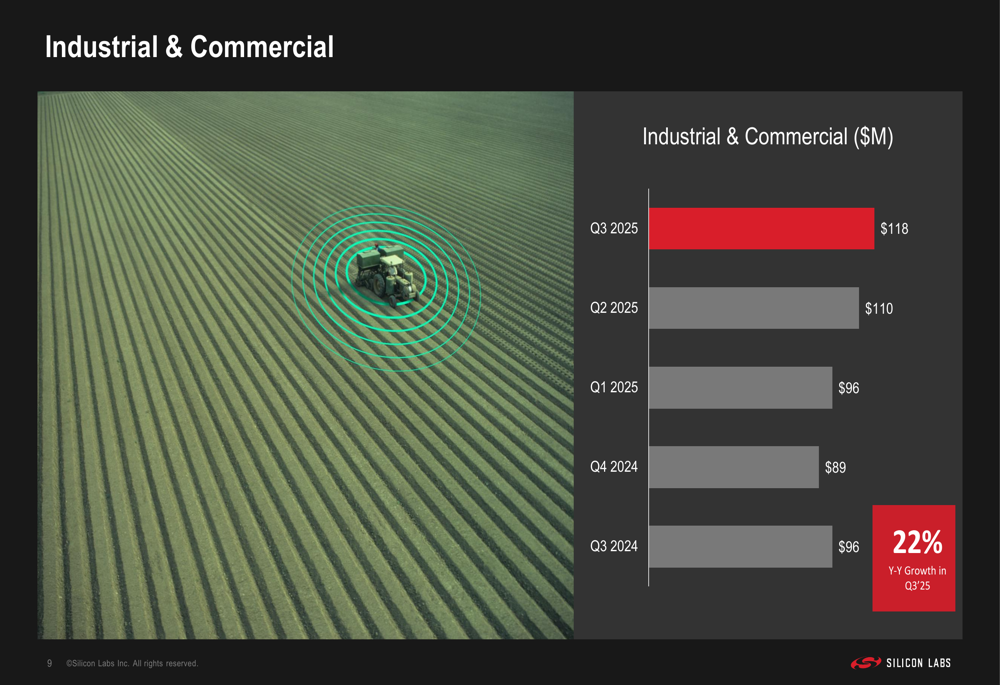

Silicon Labs reported Q3 2025 revenue of $206 million, representing a 7% increase quarter-over-quarter and an impressive 24% growth year-over-year. This performance slightly exceeded analyst expectations of $205.34 million. The company's revenue growth was balanced across its two main business segments, as illustrated in this breakdown:

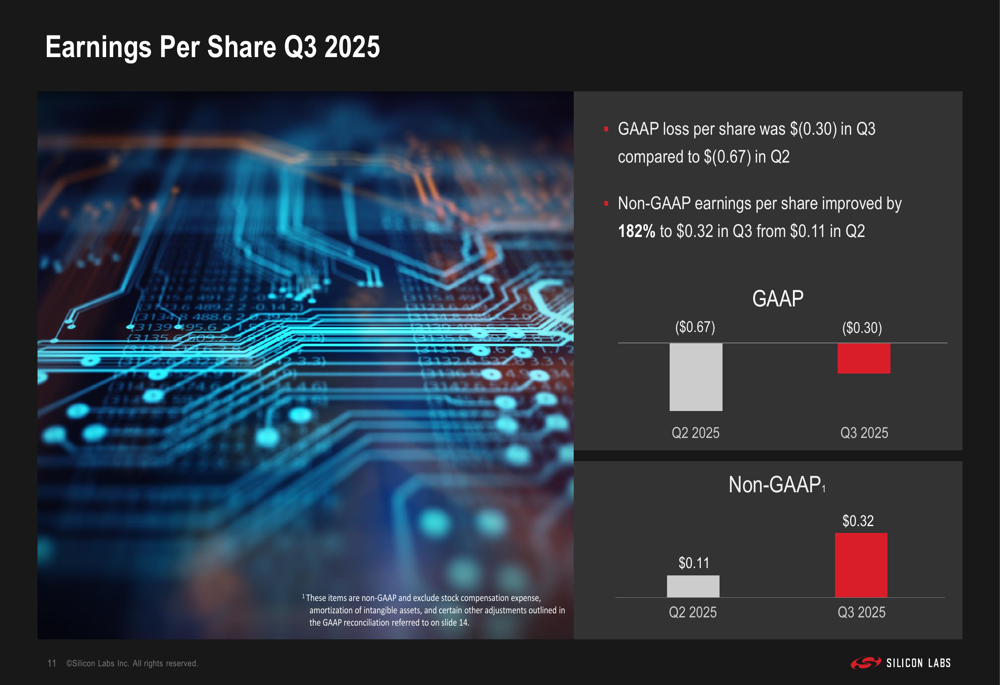

Non-GAAP earnings per share reached $0.32, exceeding forecasts by $0.02 and showing a remarkable 182% improvement from $0.11 in Q2 2025. Meanwhile, GAAP loss per share narrowed significantly to $(0.30) from $(0.67) in the previous quarter.

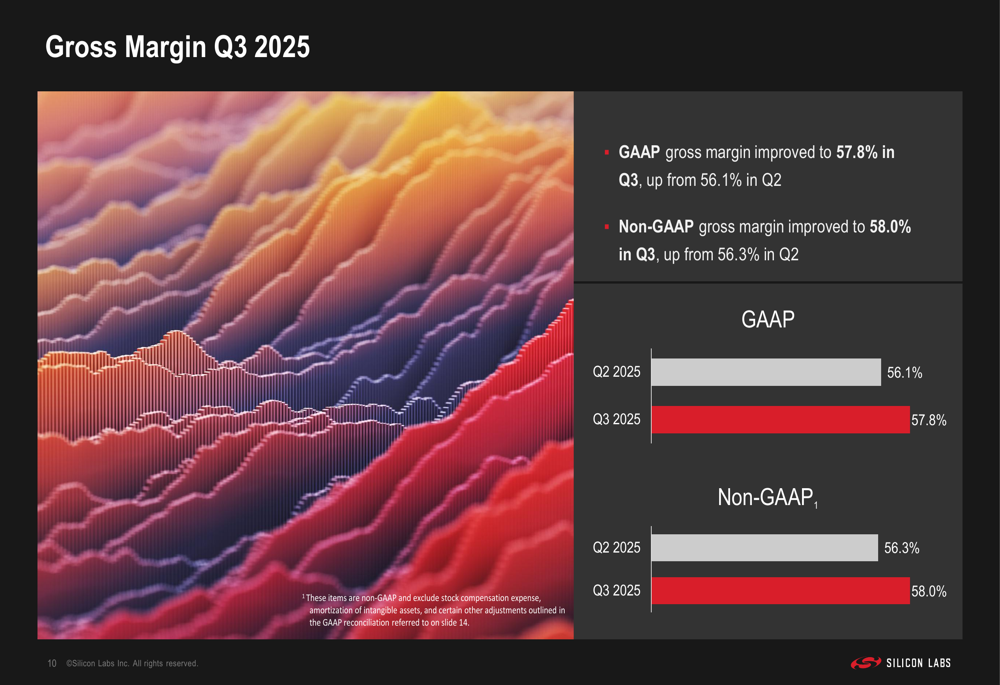

The company also achieved substantial margin expansion, with non-GAAP gross margin improving to 58.0% in Q3 from 56.3% in Q2, a 170 basis point increase. GAAP gross margin similarly improved to 57.8% from 56.1% quarter-over-quarter.

This earnings improvement reflects the company's operational efficiency and strategic focus, as shown in the EPS comparison:

Segment Analysis

Silicon Labs' business is divided into two primary segments: Home & Life and Industrial & Commercial, both of which demonstrated strong performance in Q3 2025.

The Home & Life segment generated $88 million in revenue, up 6% quarter-over-quarter and 26% year-over-year. This segment focuses on consumer applications, smart home devices, and healthcare solutions such as continuous glucose monitoring (CGM).

The Industrial & Commercial segment, which includes applications for smart metering, industrial automation, and commercial IoT deployments, contributed $118 million in revenue. This represents a 7% increase quarter-over-quarter and 22% growth year-over-year, demonstrating the company's strong position in industrial markets.

Financial Position and Outlook

Silicon Labs maintains a strong financial position with $439 million in cash, cash equivalents, and short-term investments, up from $416 million in Q2 2025. The company operates with zero debt and has maintained efficient inventory management with 85 days of inventory on hand, slightly improved from 86 days in the previous quarter.

For Q4 2025, Silicon Labs provided guidance for:

- Revenue between $200-$215 million

- Non-GAAP gross margin of 62-64%

- Non-GAAP operating expenses of $110-$112 million

- Non-GAAP earnings per share of $0.40-$0.70

This guidance suggests continued strong performance with potential for further margin expansion. The company's diversified customer base, with no single customer representing more than 10% of revenue and approximately 125 customers each contributing over $1 million in revenue, provides stability and growth potential.

Strategic Initiatives and Market Positioning

Silicon Labs has articulated a clear vision to become the "undisputed leader in embedded wireless" technology. The company's strategic market selection and focus on IoT connectivity position it for above-industry growth, as detailed in this strategic overview:

The company projects a 15-25% revenue growth rate, significantly outpacing the broader semiconductor market's expected 6-7% growth. This acceleration is driven by several factors, including:

- $10 billion in design wins now converting to revenue

- Growth opportunities in continuous glucose monitoring (CGM)

- Expansion in electronic shelf labels (ESL) and smart meters

- Market share gains in Bluetooth connectivity

- New expansion into Wi-Fi technologies

Silicon Labs' industry leadership is further validated by numerous awards and recognitions received in 2025:

Market Reaction and Analyst Perspectives

Despite the strong financial results and positive outlook, Silicon Labs' stock experienced a 2.37% decline following the presentation, closing at $127.96. This contrasts with a pre-market increase of 1.99%, suggesting that investor concerns may have outweighed the positive earnings report.

During the earnings call, CEO Matt Johnson emphasized the company's strategic position, stating, "We see a path to doing better than the market and taking continued market share." He also highlighted growth opportunities, noting, "We have the largest opportunity funnel as a company we've ever had."

Analysts have focused on Silicon Labs' alignment with end-customer demand and potential for active asset tracking. While the company's performance and outlook remain strong, market participants may be weighing potential challenges including supply chain disruptions, market saturation in certain segments, macroeconomic pressures, and intense competition in the IoT and wireless sectors.

With its strong financial performance, strategic market positioning, and robust product portfolio, Silicon Labs appears well-positioned to capitalize on the growing demand for IoT and wireless connectivity solutions despite the tepid market reaction to its latest results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.