Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Simon Property Group (NYSE:SPG), one of the largest retail REITs, reported strong third-quarter 2025 results, highlighted by accelerating net operating income (NOI) growth and an upward revision to its full-year guidance. The company's supplemental presentation, released alongside its November 3, 2025 earnings announcement, reveals a retail real estate portfolio that continues to demonstrate resilience and growth despite ongoing challenges in the broader retail sector.

Quarterly Performance Highlights

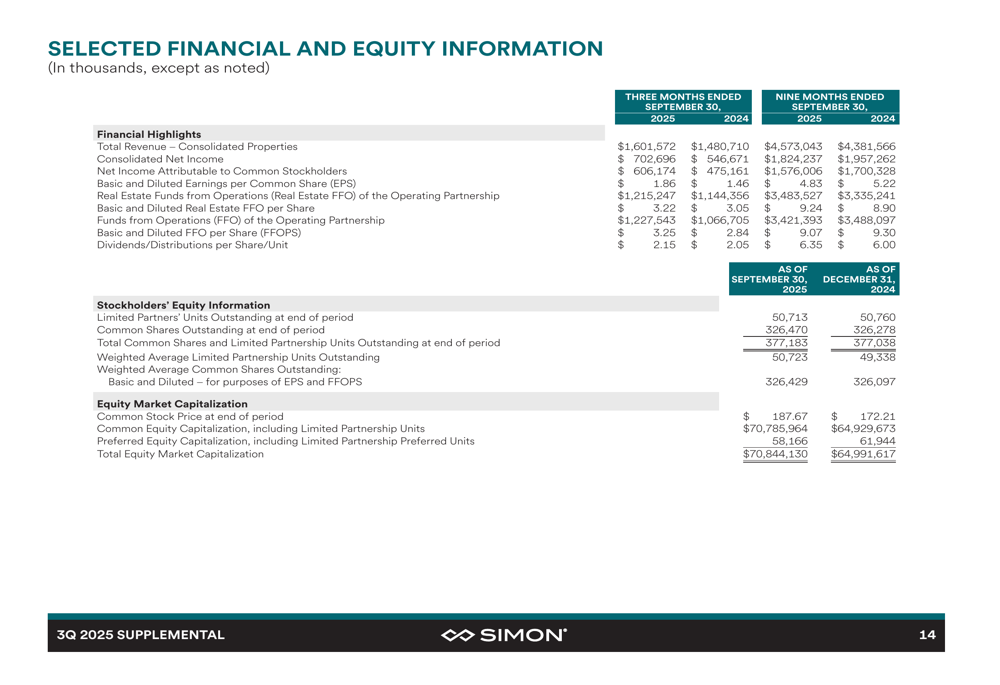

Simon Property Group reported net income attributable to common stockholders of $606.2 million, or $1.86 per diluted share, for the third quarter of 2025. The company's Funds From Operations (FFO) reached $1.228 billion, or $3.25 per diluted share, while Real Estate FFO totaled $1.215 billion, or $3.22 per diluted share.

Notably, Simon's domestic property NOI increased by 5.1% year-over-year, while total portfolio NOI grew by 5.2% compared to the prior year period. This performance exceeded analysts' expectations, with EPS coming in at $1.86 versus a forecast of $1.61, representing a 15.53% positive surprise.

The company's consolidated statements of operations provide a comprehensive view of its financial performance, showing total revenue of $1.6 billion for the three months ended September 30, 2025:

However, it's worth noting that the reported revenue figures appear to differ between Simon's presentation and some external analyses. While the presentation shows total revenue of $1.6 billion, some earnings reports cite revenue of $868.25 million, which may reflect different accounting methodologies or specific revenue segments.

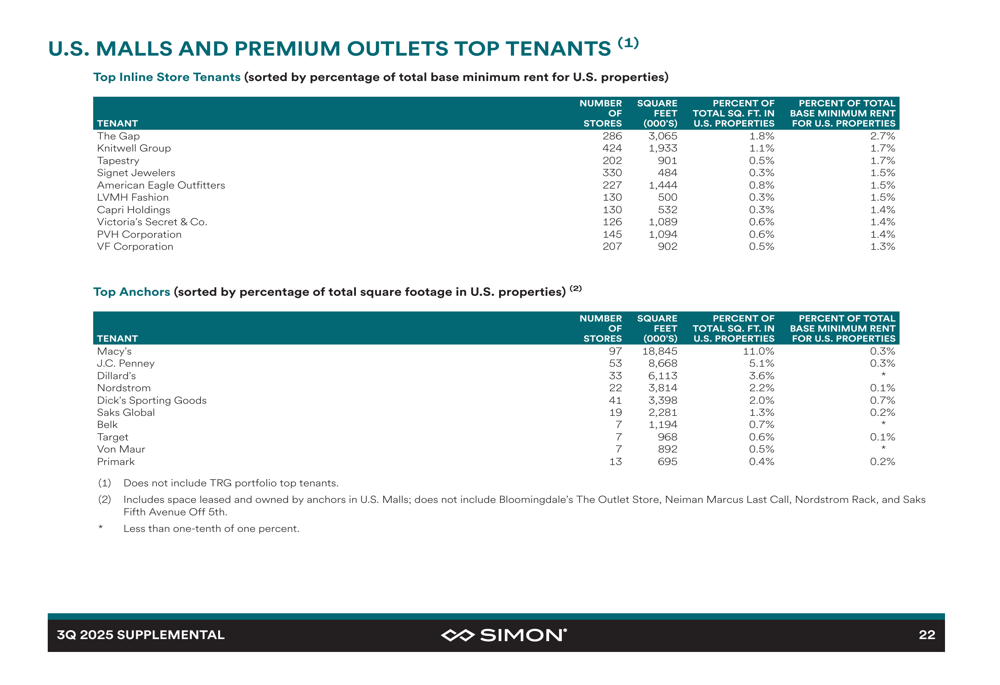

Portfolio Composition and Strategy

Simon's portfolio continues to demonstrate strong occupancy rates, with U.S. Malls and Premium Outlets reaching 96.4% occupancy as of September 30, 2025. This high occupancy rate reflects the company's ability to attract and retain tenants despite ongoing evolution in the retail landscape.

The company's NOI composition reveals a strategically diversified portfolio across different property types and geographic regions. U.S. Malls and Premium Outlets contribute the largest portion of NOI at 70.6%, followed by The Mills at 11.2%, TRG at 8.2%, and International properties at 10.0%. Geographically, Florida (19.5%), California (13.7%), and Texas (10.2%) represent the largest contributors to U.S. portfolio NOI:

This geographic diversification provides Simon with exposure to some of the strongest retail markets in the United States while limiting concentration risk in any single region. The company's international presence, particularly through its 22.4% ownership stake in European retail property company Klépierre, further enhances its diversification strategy.

Financial Strength and Capital Allocation

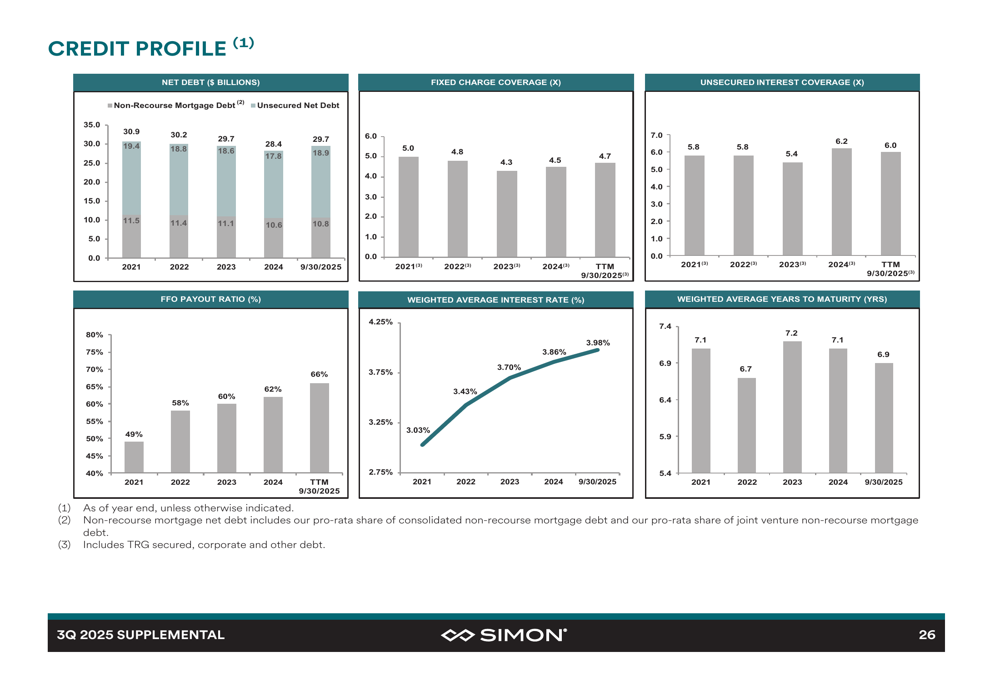

Simon's balance sheet remains robust, with a disciplined approach to leverage and strong credit metrics. The company's credit profile shows healthy fixed charge coverage and interest coverage ratios around 5x, with a weighted average interest rate of approximately 4.0% and a weighted average maturity of about 7 years:

The company's indebtedness summary further demonstrates its prudent approach to financial management, with a significant portion of debt structured at fixed rates to minimize interest rate risk:

This financial strength has enabled Simon to enhance shareholder returns through a 4.8% year-over-year increase in its quarterly dividend to $2.20 per share. Additionally, the company completed the acquisition of the remaining 12% interest in The Taubman Realty Group during the quarter, consolidating its ownership of this premium retail portfolio.

Strategic Initiatives and Development Activity

Simon continues to invest in its portfolio through targeted development and redevelopment activities. The company's capital expenditures for the nine months ended September 30, 2025, reflect its commitment to maintaining and enhancing the quality of its properties:

These investments are designed to ensure Simon's properties remain attractive destinations for both retailers and consumers, with a focus on creating experiential retail environments that cannot be replicated online.

Forward Outlook

Based on its strong performance through the first three quarters of 2025, Simon has increased its full-year 2025 Real Estate FFO guidance to a range of $12.60 to $12.70 per diluted share, up from previous estimates:

This upward revision reflects management's confidence in the company's operational performance and growth prospects for the remainder of the year. The guidance reconciliation provides a clear path from estimated net income to the projected Real Estate FFO, offering investors transparency into the company's financial projections.

Market Reaction and Analyst Perspectives

Following the earnings announcement, Simon's stock closed up 0.63% at $175.76, reflecting positive investor sentiment despite mixed reactions to the revenue figures. The stock remains within its 52-week range of $136.34 to $190.14, demonstrating relative stability in a volatile market environment.

Analysts have noted Simon's ability to navigate the evolving retail landscape through strategic tenant selection and property enhancements. The company's focus on premium retail locations and diversification across property types appears to be resonating with both tenants and investors.

In summary, Simon Property Group's Q3 2025 presentation reveals a company that continues to execute effectively on its strategic priorities, delivering solid financial results and returning value to shareholders through dividend growth and prudent capital allocation. While challenges remain in the retail sector, Simon's portfolio quality, financial strength, and management expertise position it well to continue delivering value in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.