Senate Republicans to challenge auto safety mandates in January - WSJ

Introduction & Market Context

SIMPAR SA (B3:SIMH3) reported its third-quarter 2025 results on November 13, showing improved operational performance despite posting a net loss. The Brazilian logistics and transportation conglomerate saw its stock close at R$5.27, up 0.95% on the day of the announcement, reflecting investor confidence in the company's strategic direction despite bottom-line challenges.

The company's presentation highlighted significant progress in operational efficiency and cost reduction initiatives, which helped drive a 14% year-over-year increase in adjusted EBITDA to R$3.1 billion, despite recording a net loss of R$119 million for the quarter.

Quarterly Performance Highlights

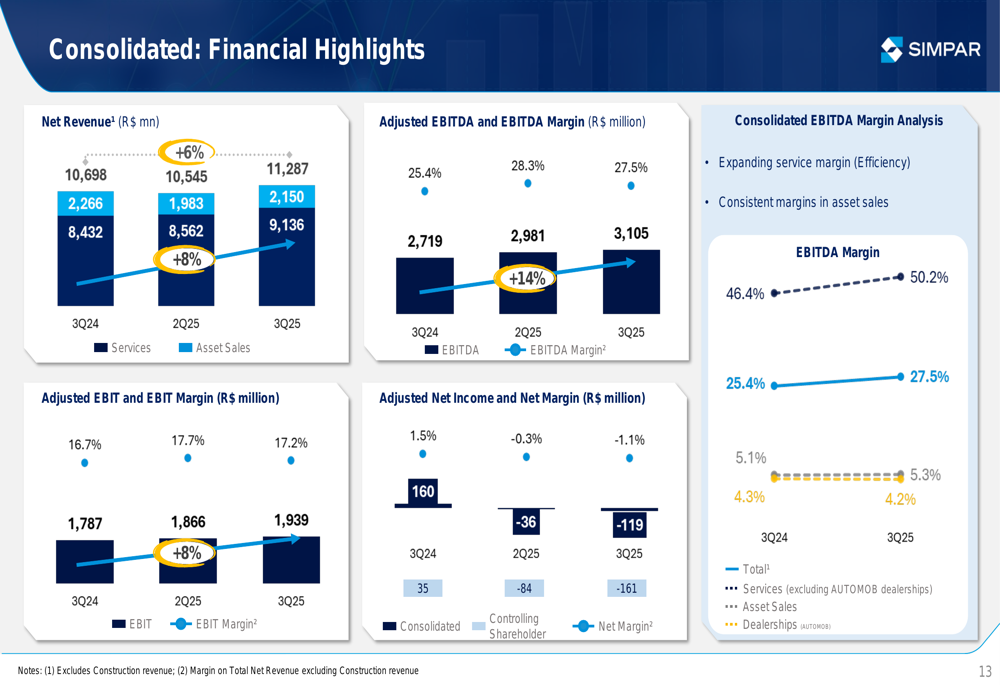

SIMPAR reported total gross revenue of R$12.4 billion in Q3 2025, representing a 5% increase compared to the same period last year. Service revenue, a key component of the business, grew by 8% year-over-year to R$10.2 billion, while sales of heavy assets surged by 82%.

The company's adjusted EBITDA margin expanded by 2.1 percentage points to reach 27.5%, demonstrating improved operational efficiency. However, adjusted net income turned negative at -R$119 million, compared to a positive R$160 million in Q3 2024.

As shown in the following consolidated financial highlights:

The company's ROIC (Return on Invested Capital) for the last twelve months reached 13.9%, a 1.5 percentage point improvement compared to the same period last year, indicating better capital allocation efficiency despite the net loss.

Operational Efficiency Initiatives

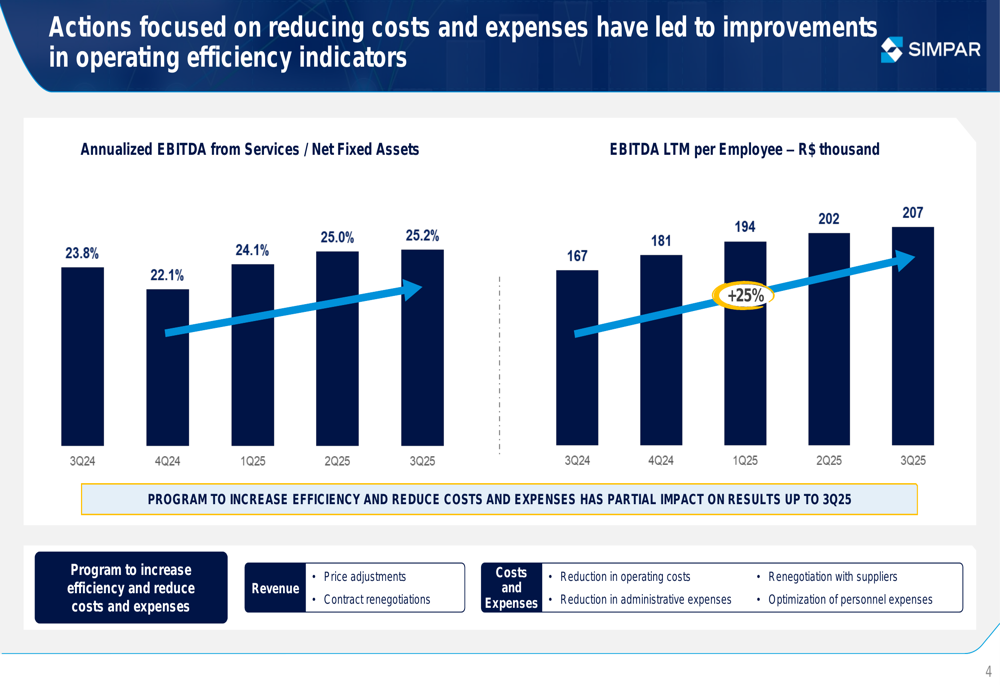

A key focus for SIMPAR has been improving operational efficiency through various cost reduction initiatives. The company reported a 25% increase in EBITDA per employee, which grew from R$167,000 in Q3 2024 to R$207,000 in Q3 2025. Additionally, the ratio of annualized EBITDA from services to net fixed assets improved from 23.8% to 25.2% year-over-year.

These improvements were achieved through several initiatives, including price adjustments, contract renegotiations, reduction in operating and administrative expenses, renegotiation with suppliers, and optimization of personnel expenses.

As illustrated in the following operational efficiency indicators:

Segment Performance

SIMPAR's diversified business model showed mixed results across its various segments:

JSL, the company's logistics arm, reported a 5.6% increase in net revenue to R$2.5 billion and a 12.8% increase in adjusted EBITDA to R$526 million. However, adjusted net income declined by 50.7% to R$36 million.

Movida, the car rental business, saw a slight 0.3% decrease in net revenue to R$3.8 billion, but achieved an 18.5% increase in EBITDA to R$1.5 billion, with EBITDA margin expanding by 6.3 percentage points to 39.3%. Net income decreased by 10.5% to R$70 million.

Vamos, the heavy equipment rental division, delivered strong revenue growth of 25.2% to R$1.5 billion, with a 3.7% increase in EBITDA to R$895 million. However, net income fell by 72.7% to R$50 million.

AUTOMOB, the automotive retail segment, reported an 11.4% increase in net revenue to R$3.5 billion, but saw a 5.6% decrease in adjusted EBITDA to R$144 million.

Capital Allocation and Debt Management

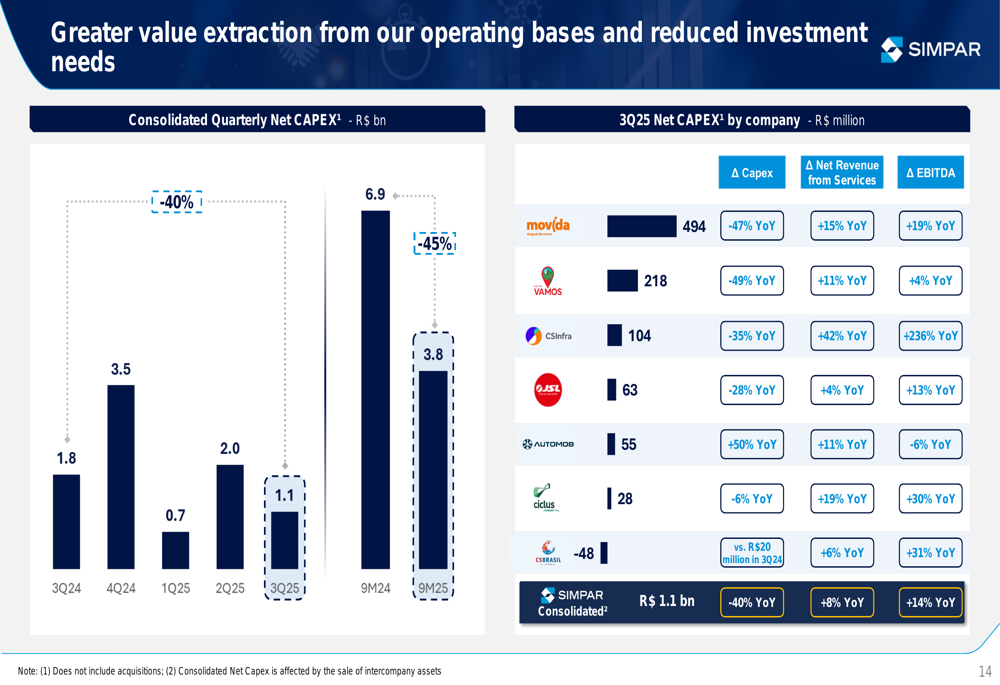

One of the most significant improvements in SIMPAR's financial performance was the 40% reduction in net capital expenditures, which decreased to R$1.1 billion in Q3 2025. This reduction was observed across most of the company's business units, with Movida (-47% YoY) and Vamos (-49% YoY) leading the way.

The following chart illustrates the breakdown of net CAPEX by company:

This reduction in capital expenditures, combined with EBITDA growth, resulted in an EBITDA to Net CAPEX ratio of 2.4x, indicating that the company is generating significantly more cash from operations than it is investing in growth.

SIMPAR also made progress in strengthening its balance sheet, reducing net debt by approximately R$828 million compared to the previous quarter. The company maintained a strong cash position of R$14.5 billion and extended its debt profile to an average term of 4.0 years.

The debt profile and amortization schedule demonstrate the company's focus on long-term financial stability:

Strategic Outlook

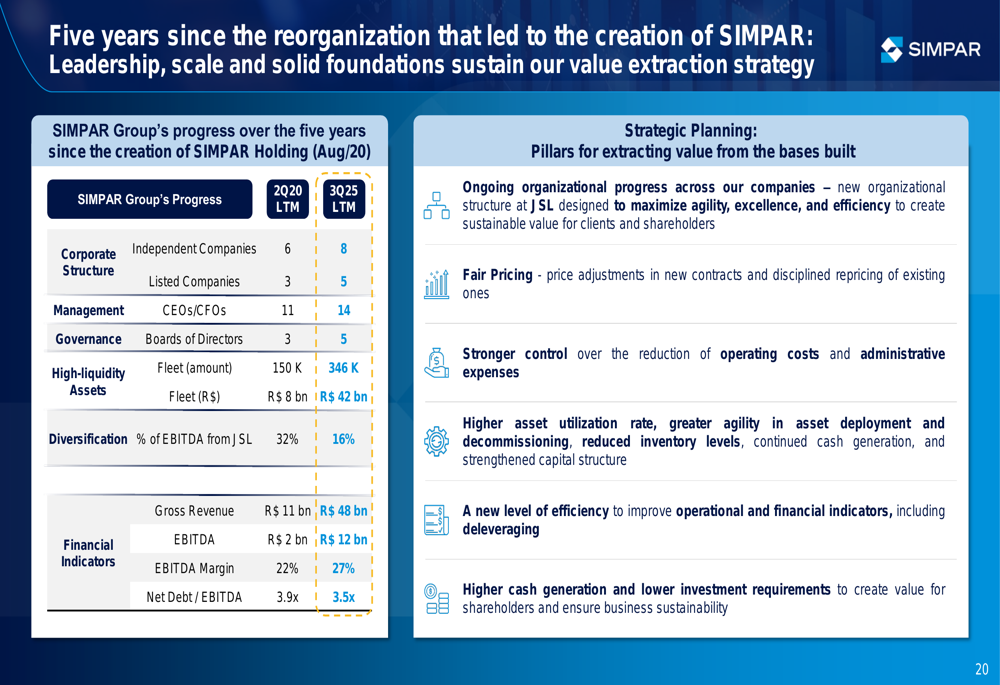

Looking ahead, SIMPAR's strategic planning is focused on five key pillars: ongoing organizational progress, fair pricing, stronger control, higher asset utilization, and higher cash generation. The company is targeting zero debt for its holding company and anticipates continued growth with reduced capital expenditures.

The company also completed the sale of 100% of Ciclus Rio for R$1.1 billion (equity value), demonstrating its commitment to portfolio optimization and value extraction.

As outlined in the company's strategic planning:

During the earnings call, CEO Fernando Simões emphasized the essential nature of SIMPAR's services, stating, "Our businesses offer essential services. They are highly liquid because people can live without our company, but they cannot live without the types of services we provide." He also highlighted the company's growth strategy, noting, "We are going to extract a lot of efficient zero debt, grow and transform our companies in size."

Despite the net loss in Q3 2025, SIMPAR's focus on operational efficiency, cost reduction, and strategic capital allocation positions the company to navigate the challenging market environment while building a foundation for future profitability.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.