Gold is 2025’s best performer. UBS sees more upside

Introduction & Market Context

Simpson Manufacturing Co., Inc. (NYSE:SSD) recently presented its investor outlook for April 2025, highlighting the company’s 30-year journey as a public company and its strategy to continue outperforming the housing market. The presentation comes after Simpson reported mixed Q4 2024 results, with revenue exceeding expectations but EPS falling short of forecasts.

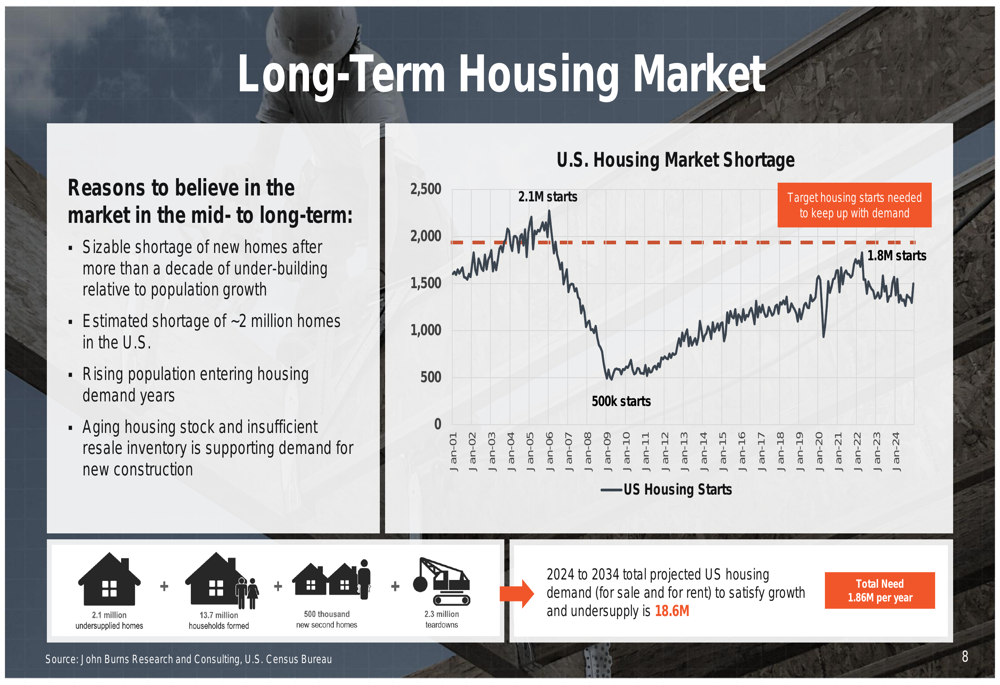

The company operates in a housing market facing both challenges and long-term opportunities. Despite current market headwinds, Simpson emphasizes the substantial housing shortage in the U.S., estimated at approximately 2 million homes, with projected housing demand of 18.6 million units from 2024 to 2034.

As shown in the following chart, Simpson highlights the significant housing shortage and demand projections that underpin its long-term market opportunity:

Executive Summary

Simpson Manufacturing is celebrating 30 years as a public company, having grown from $150 million in revenue in 1994 to $2.2 billion in 2024, representing a 15x increase. During the same period, earnings per share grew from $0.14 to $7.60, a remarkable 54x increase, reflecting a compound annual growth rate of approximately 14%.

The company’s business model centers on being an innovation leader with a broad portfolio of solutions, comprehensive service, and unparalleled product availability. Simpson maintains a strong market position across its three core addressable markets: Wood Connectors, Fastening Systems, and Concrete & Steel Connections.

The following slide illustrates Simpson’s impressive 30-year growth trajectory since its IPO:

Financial Performance Highlights

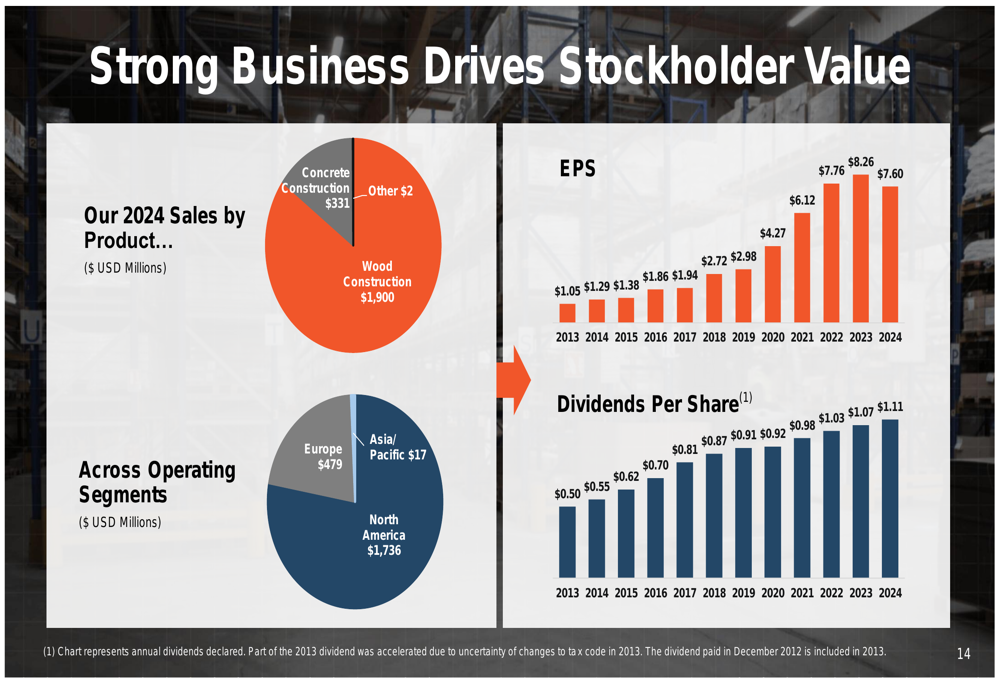

Simpson’s financial performance demonstrates consistent growth and profitability. The company reported 2024 sales of $2.23 billion, with Wood Construction products accounting for $1.9 billion, Concrete Construction contributing $331 million, and Other products adding $2 million. Geographically, North America remains the dominant market with $1.74 billion in sales, followed by Europe at $479 million and Asia/Pacific at $17 million.

The company has maintained strong profitability metrics, with operating income reaching $430 million in 2024, up from $250 million in 2020, despite flat U.S. housing starts of approximately 1.4 million in both years. This performance highlights Simpson’s ability to grow through market share gains, pricing strategies, and acquisitions like ETANCO.

However, recent earnings results reveal some challenges. In Q4 2024, Simpson reported EPS of $1.31, missing forecasts of $1.55, while gross margin decreased to 46% from 47.1% in 2023. Despite these headwinds, the company continues to outperform the broader housing market.

The following chart illustrates Simpson’s sales distribution and financial performance:

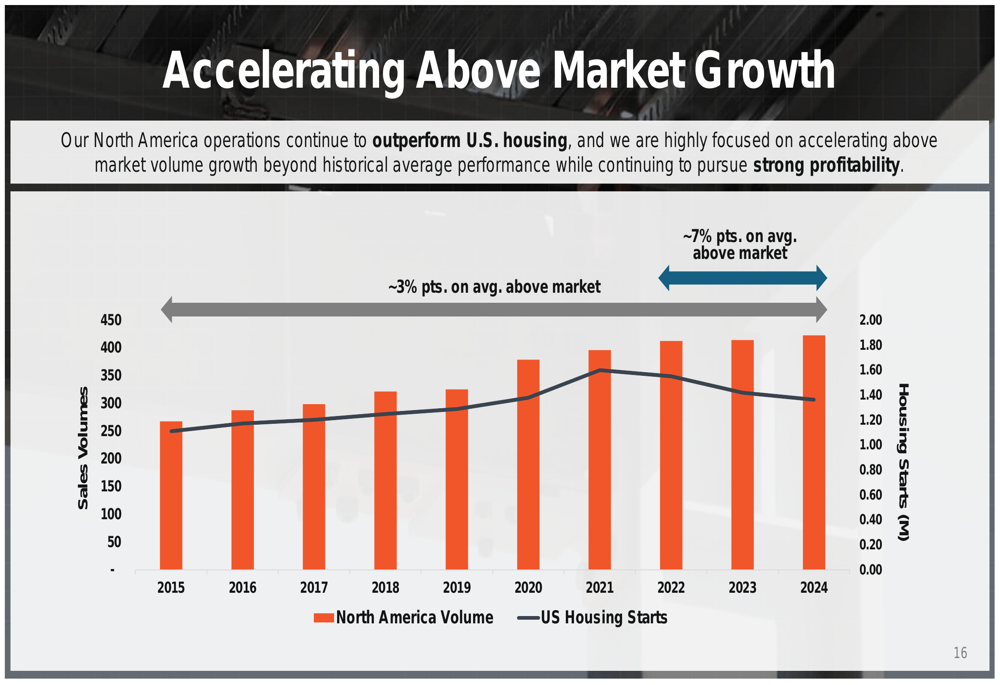

Simpson has consistently outperformed U.S. housing starts, with North American operations growing approximately 3-7 percentage points above the market, as shown in this comparative analysis:

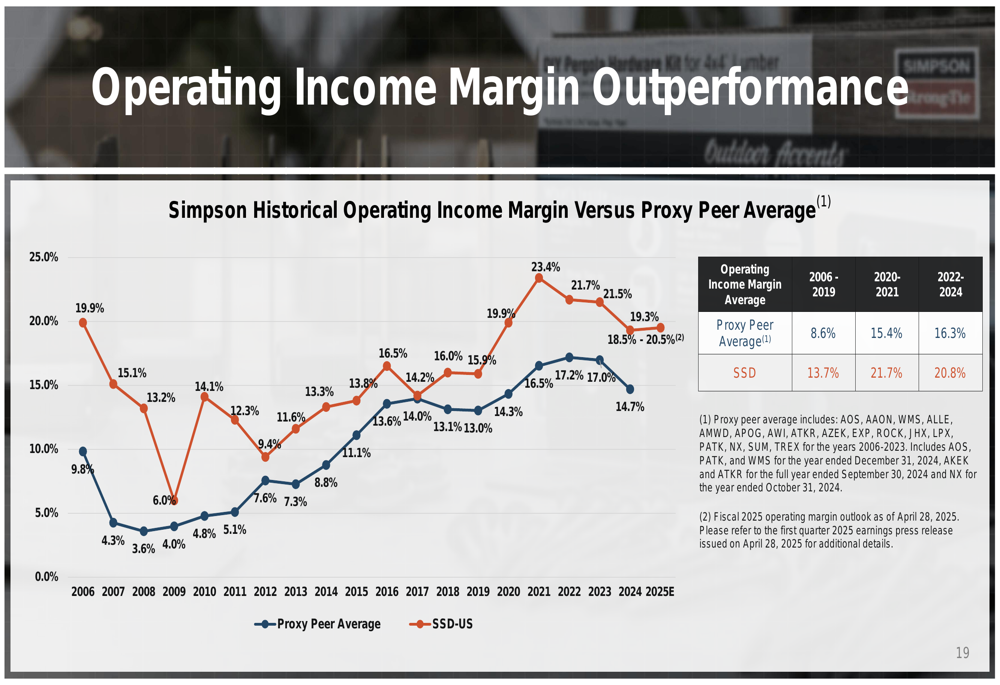

The company also maintains an operating income margin advantage over its peers, though this advantage has narrowed in recent years:

Strategic Initiatives

Simpson is pursuing several strategic initiatives to drive future growth. The company is expanding its manufacturing footprint with facility expansions in Columbus (WA:CLC), Ohio (opened in H1 2025) and a new greenfield facility in Gallatin, Tennessee (expected in H2 2025). These investments aim to support growth, maintain safety standards, improve production costs, and reduce dependence on imported products.

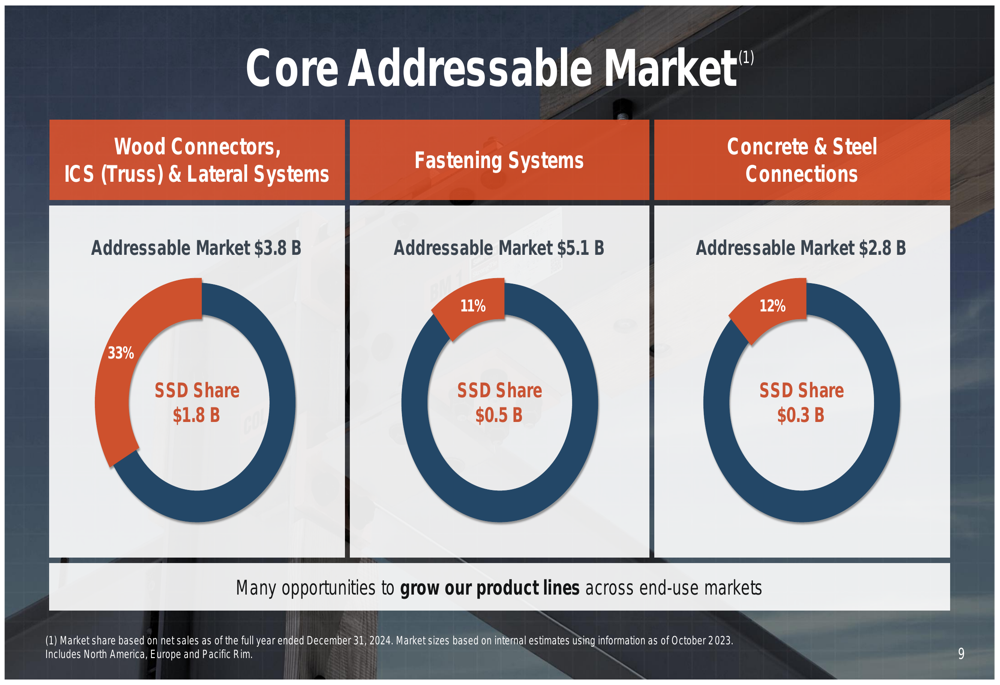

The company’s core addressable markets present significant opportunities, with Simpson currently holding a 33% share in the $3.8 billion Wood Connectors market, 11% in the $5.1 billion Fastening Systems market, and 12% in the $2.8 billion Concrete & Steel Connections market.

As illustrated in the following market share breakdown, Simpson has substantial room for growth across its core segments:

Simpson’s diverse portfolio of solutions spans multiple product categories and applications, providing a solid foundation for continued growth:

The company’s capital allocation strategy prioritizes facility expansions, growth initiatives, and shareholder returns. Simpson targets returning 35% of free cash flow to shareholders through dividends and share repurchases, with the board approving a $100 million share repurchase authorization through December 2025. From 2021 to 2025, the company has returned approximately 52% of free cash flow to stockholders, exceeding its target.

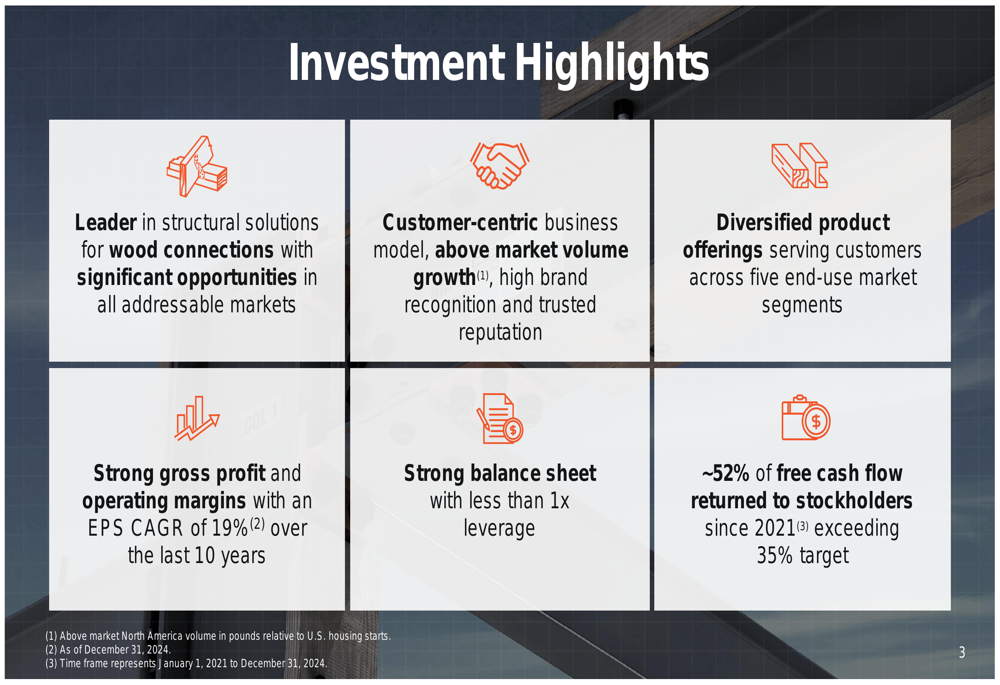

The following slide highlights Simpson’s key investment attributes:

Forward-Looking Statements

Looking ahead, Simpson has outlined several ambitious goals, including strengthening its values-based culture, becoming the business partner of choice, maintaining its position as an innovative leader, continuing above-market volume growth relative to U.S. housing starts, maintaining an operating income margin above 20%, and achieving EPS growth ahead of net revenue growth.

For 2025, the company has provided guidance for an operating margin between 18.5% and 20.5%, with capital expenditures projected at $150-170 million. Management remains cautious but optimistic about the housing market’s long-term prospects, citing the significant housing shortage and demographic trends supporting demand.

In Europe, Simpson is focusing on strengthening its position in wood connectors, increasing structural fasteners, building on strong positions in facades, and targeting expansion in pavement reinforcement. The company is prioritizing countries where it already operates and exploiting the growing mass timber trend.

Simpson’s stock closed at $153.54 on April 28, 2025, up 0.19% for the day, with aftermarket trading showing a 0.89% increase to $155.19. The stock is currently trading above its 52-week low of $137.35 but well below its 52-week high of $197.82, suggesting potential upside if the company can execute on its strategic initiatives and navigate current market challenges.

As Simpson Manufacturing enters its fourth decade as a public company, it remains focused on leveraging its strong foundation to build an even stronger future through innovation, market expansion, and disciplined capital allocation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.