Bitcoin price today: dips to $92k as Fed cut doubts spark risk-off mood

Introduction & Market Context

Sinch AB (SINCH) presented its Q3 2025 results on November 5, revealing a complex financial picture that sent shares tumbling 15.82% despite some positive operational metrics. The communications platform provider reported improved margins and organic growth in key areas, but these achievements were overshadowed by an earnings miss that disappointed investors.

The company's presentation highlighted strategic initiatives in AI-powered communications and conversational messaging, positioning these as key growth drivers amid competitive pressures in traditional messaging services. However, the market's negative reaction reflected concerns about Sinch's ability to meet revenue expectations in an increasingly competitive landscape.

Quarterly Performance Highlights

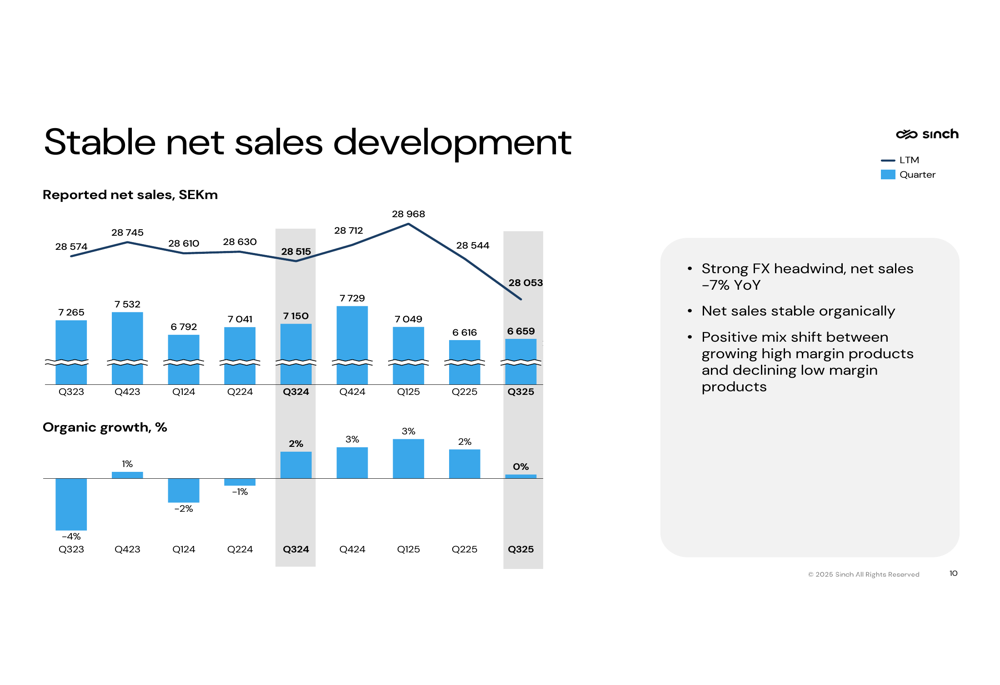

Sinch reported stable organic gross profit growth of 5% year-over-year, consistent with the previous quarter's performance. However, net sales amounted to SEK 6,659 million, with currency effects having a significant negative impact of 7%.

As shown in the following chart of quarterly net sales development:

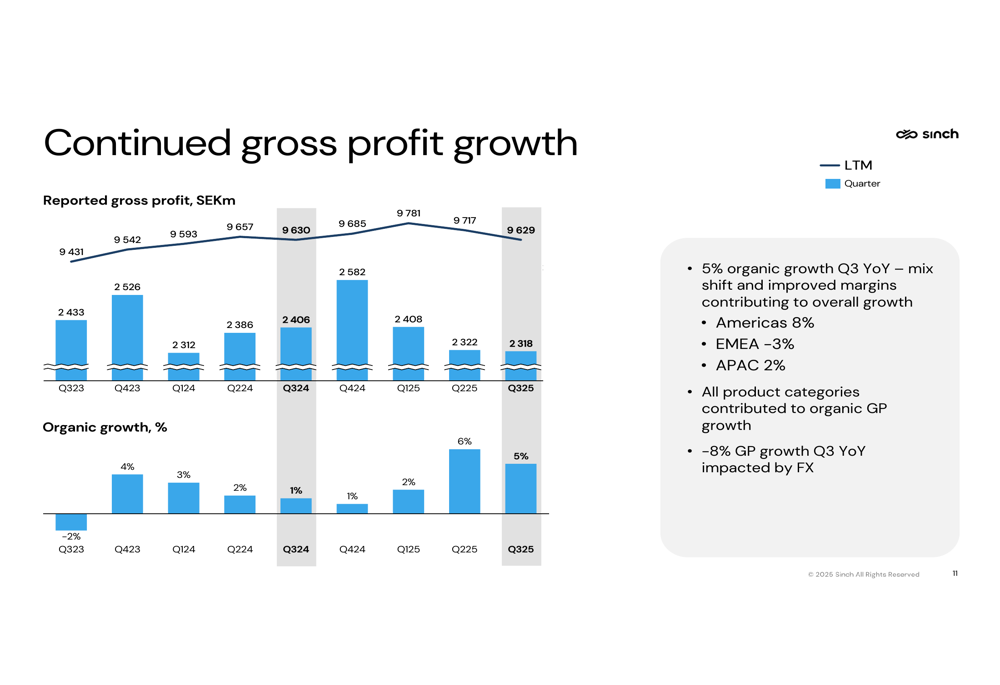

The company's gross profit showed continued organic growth despite currency headwinds, with the Americas region leading at 8% organic growth, while EMEA declined by 3% and APAC grew by 1%.

The following chart illustrates the gross profit trajectory:

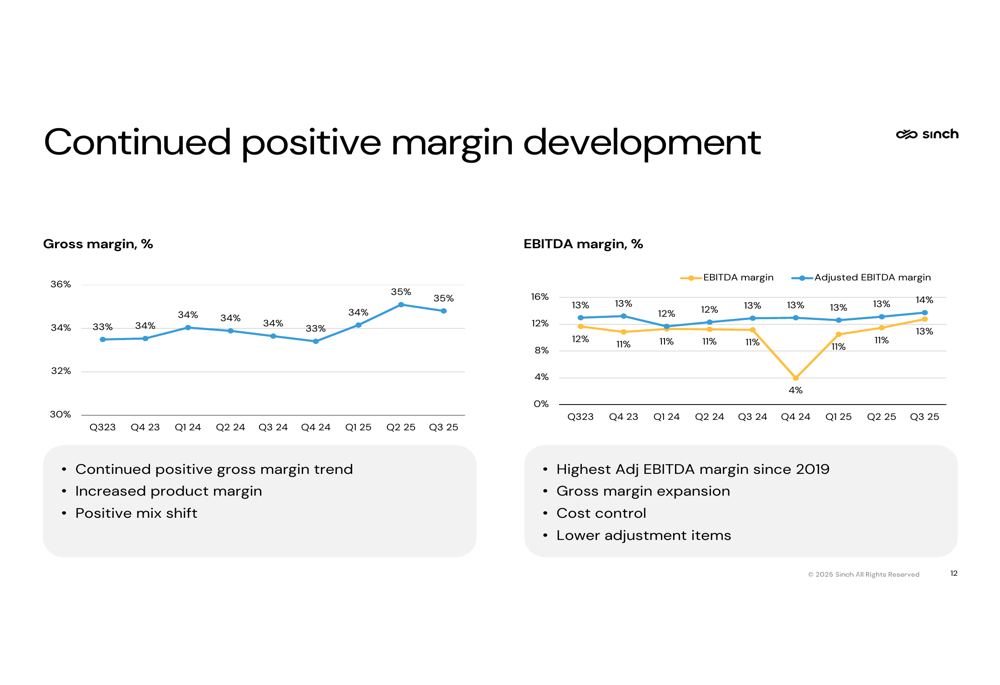

A key bright spot in Sinch's results was margin improvement, with gross margin increasing to 35%, up 1 percentage point year-over-year, while adjusted EBITDA increased 8% organically to reach a record high margin of 14% since 2019.

The margin development is illustrated in this chart:

Detailed Financial Analysis

Despite the positive margin development, Sinch's Q3 results fell significantly short of market expectations. The company posted an earnings per share (EPS) of -0.01 USD, missing the forecast of 0.55 USD by 101.82%. Revenue also missed expectations at 6.66 billion USD against a forecast of 6.86 billion USD.

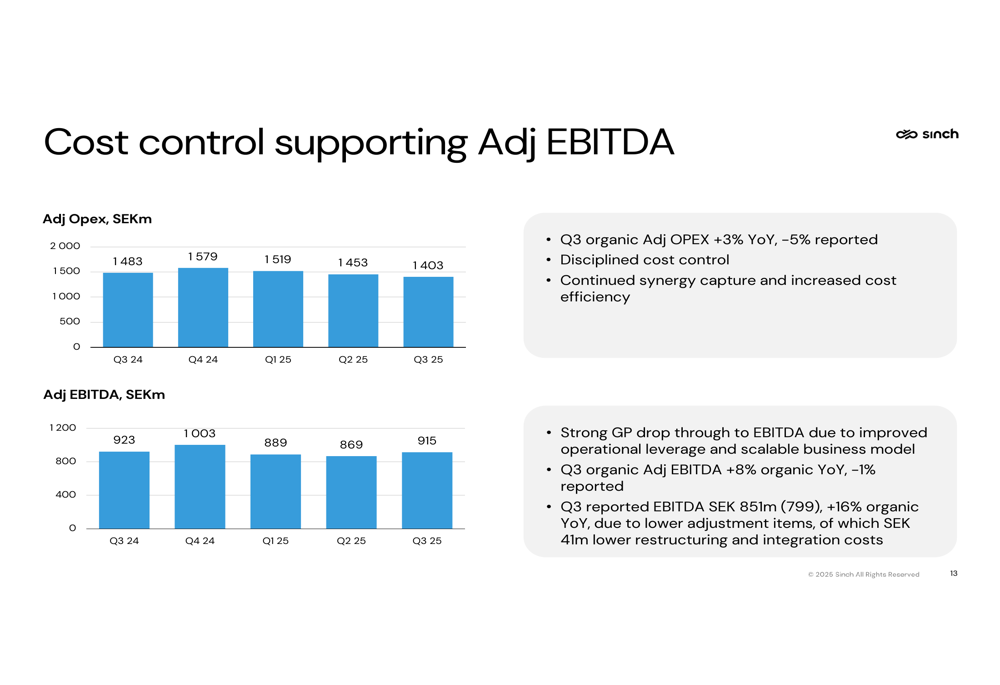

Cost control measures have supported the improved adjusted EBITDA performance, as shown in the following chart:

The company reported that Q3 organic Adjusted OPEX increased 3% year-over-year, though it decreased 5% on a reported basis. This disciplined cost control, combined with continued synergy capture and increased cost efficiency, contributed to strong gross profit drop-through to EBITDA.

Sinch's balance sheet remains relatively strong, with net debt/Adjusted EBITDA increasing slightly to 1.4x, primarily due to share repurchases. The company has repurchased 15.3 million shares for SEK 519 million, representing 1.8% of outstanding shares, while also allocating SEK 241 million for LTIP equity swap.

Cash flow from operating activities after investments was SEK 1,397 million over the past 12 months, corresponding to a 38% cash conversion rate, slightly below the company's guidance range of 40-50%.

Strategic Initiatives

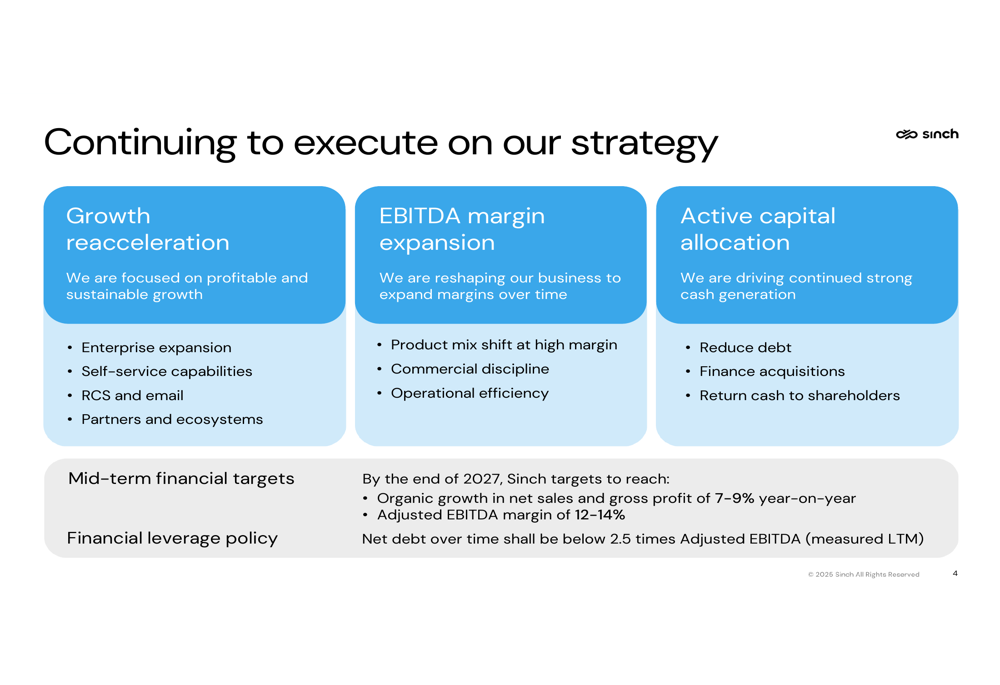

Sinch's presentation emphasized its strategic focus on three key areas: growth reacceleration, EBITDA margin expansion, and active capital allocation. The company is prioritizing profitable and sustainable growth through enterprise expansion, self-service capabilities, RCS and email, and partners and ecosystems.

The company's strategic roadmap is outlined in this slide:

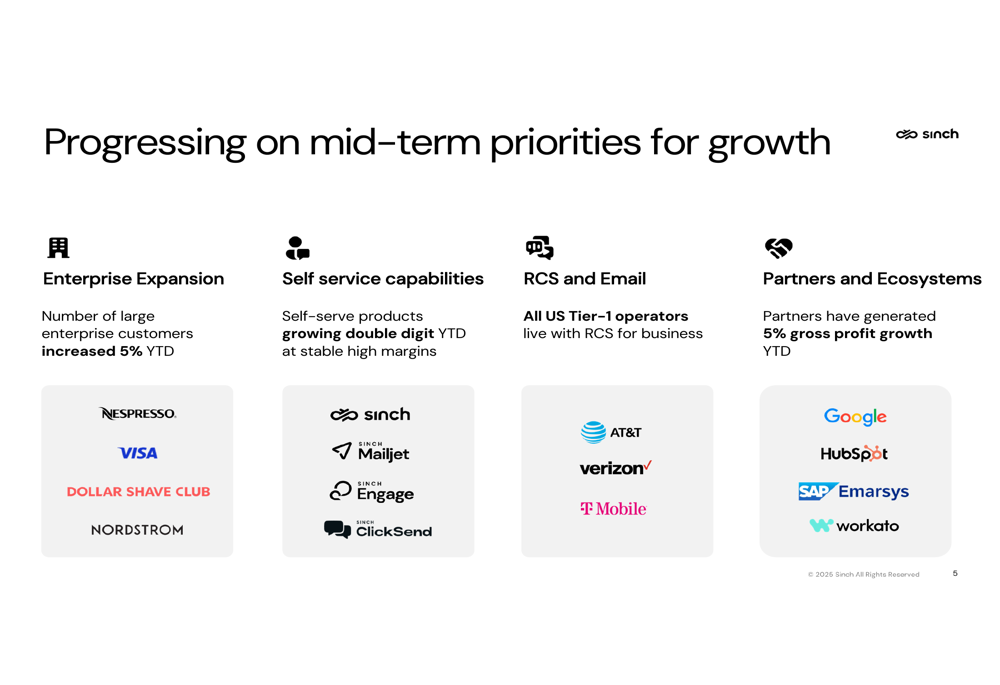

Sinch highlighted progress in its mid-term priorities for growth, noting that the number of large enterprise customers increased 5% year-to-date, while self-serve products are growing at double-digit rates with stable high margins.

The company's progress on growth priorities is illustrated here:

A significant focus of Sinch's strategy is the development of AI-powered communications and conversational messaging. The company reported that RCS for Business message volumes have tripled year-over-year, and it has launched WhatsApp Upscale to complement its RCS offerings.

CEO Lorinda Pang emphasized Sinch's role as a critical communications layer in the AI economy, stating, "More AI adoption means more traffic, generating more revenue in our existing core business." The company is positioning itself to benefit from what it calls a "dual inflection point" of conversational messaging and generative AI.

Forward-Looking Statements

Sinch reaffirmed its mid-term financial targets, anticipating 7-9% organic growth in net sales and gross profit year-on-year and an adjusted EBITDA margin of 12-14% by the end of 2027. The company's financial leverage policy states that net debt over time shall be below 2.5 times adjusted EBITDA.

However, these forward-looking statements come against a backdrop of challenges, including competitive pressures in traditional messaging, particularly in the Americas and India, potential market saturation in established communication channels, and macroeconomic pressures affecting customer spending.

The significant stock drop following the earnings announcement suggests investors remain skeptical about Sinch's ability to achieve these targets in the face of current headwinds. With the stock now trading near its 52-week low of 15.7 USD, the company faces pressure to demonstrate that its strategic initiatives can translate into improved financial performance that meets market expectations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.