Gold prices edge higher on raised Fed rate cut hopes

SiteOne Landscape Supply Inc (NYSE:SITE) reported improved profitability in its second quarter 2025 presentation despite flat organic daily sales, as the company continues to execute on its acquisition strategy and operational initiatives.

Quarterly Performance Highlights

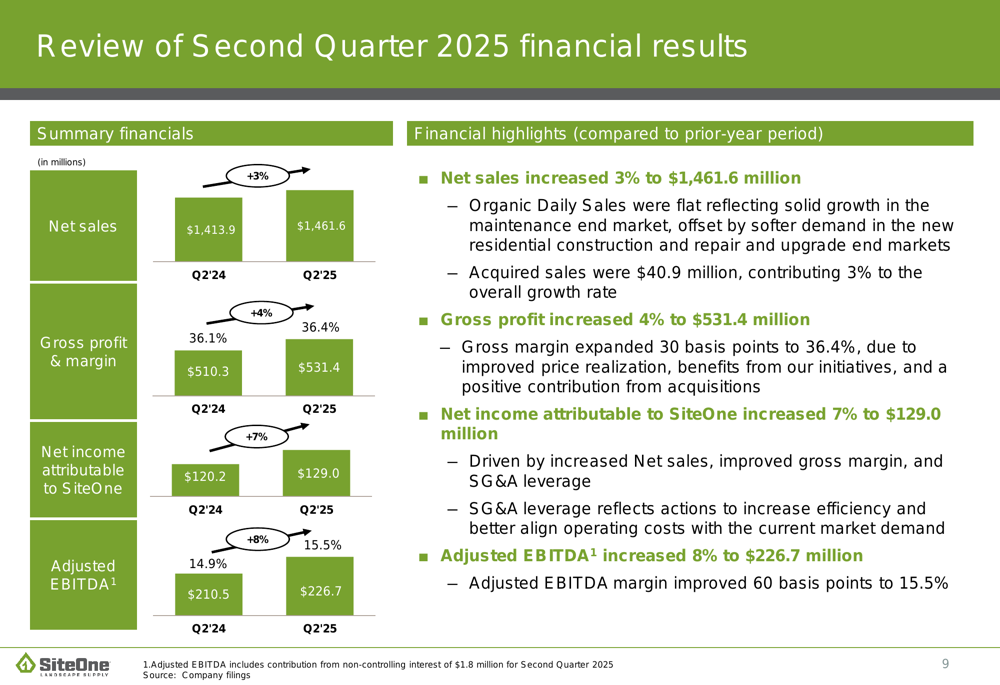

SiteOne delivered solid financial results for the second quarter ended June 29, 2025, with net sales increasing 3% to $1,461.6 million compared to $1,413.9 million in the same period last year. While organic daily sales remained flat, the company achieved notable improvements in profitability metrics.

Gross profit rose 4% to $531.4 million, with gross margin expanding 30 basis points to 36.4%. SG&A as a percentage of net sales decreased 40 basis points to 23.9%, demonstrating improved operational efficiency. Net income attributable to SiteOne increased 7% to $129.0 million, while Adjusted EBITDA grew 8% to $226.7 million with margin improving 60 basis points to 15.5%.

As shown in the following chart of quarterly financial results:

The results represent a significant turnaround from the first quarter of 2025, when the company reported a net loss of $27.3 million and missed earnings expectations with an EPS of -$0.61 compared to forecasts of -$0.44.

Balance Sheet and Cash Flow

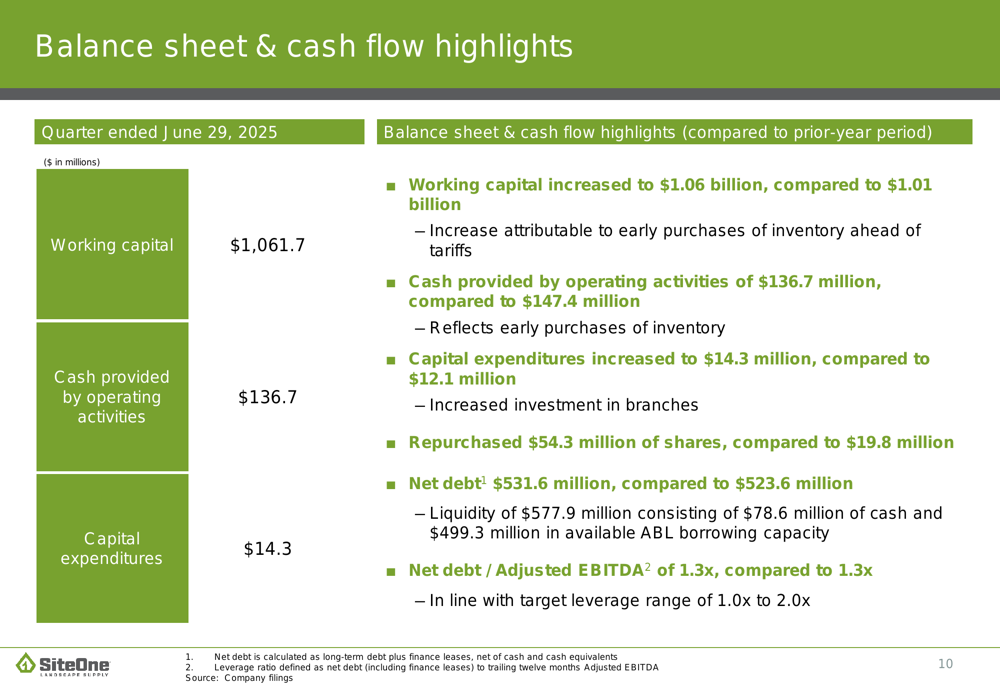

SiteOne maintained a strong financial position with working capital increasing to $1,061.7 billion from $1.01 billion in the prior-year period. Cash provided by operating activities was $136.7 million, down slightly from $147.4 million in Q2 2024. The company’s net debt stood at $531.6 million, resulting in a net debt to Adjusted EBITDA ratio of 1.3x, which remains within the target leverage range of 1.0x to 2.0x.

During the quarter, SiteOne repurchased $54.3 million of shares under its share repurchase authorization, significantly higher than the $19.8 million repurchased in the same period last year. Capital expenditures increased to $14.3 million from $12.1 million in Q2 2024.

The company’s balance sheet details are illustrated below:

Acquisition Strategy

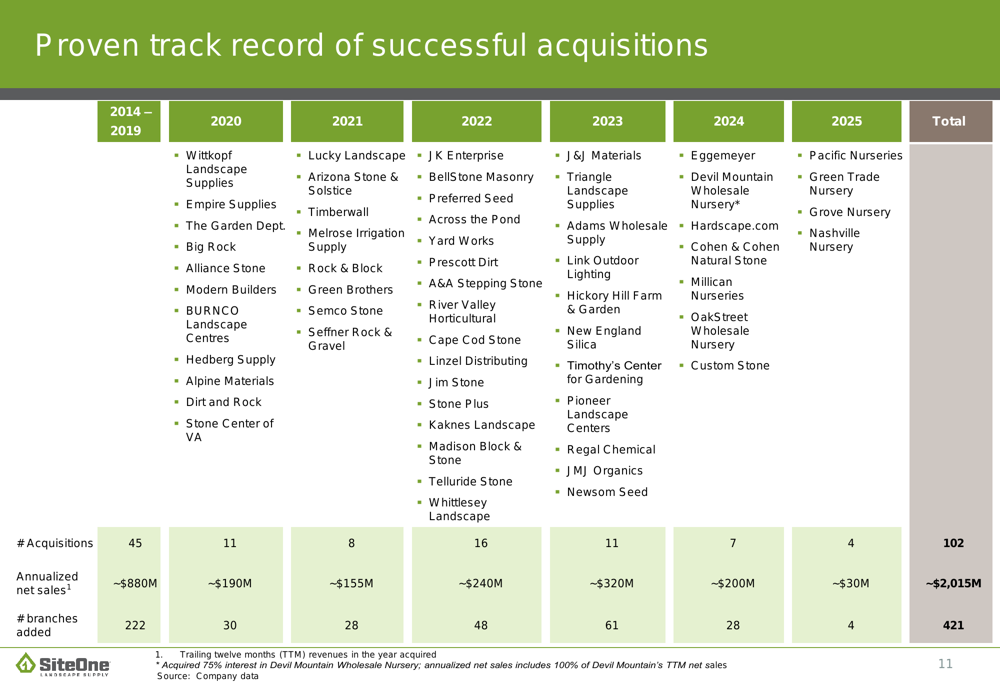

SiteOne continues to execute its growth strategy through strategic acquisitions. In the second quarter, the company completed the acquisition of Green Trade Nursery, a wholesale nursery distributor in the north Atlanta market. Additionally, SiteOne announced two recent acquisitions closed on July 24: Grove Nursery in the northwest Minneapolis market and Nashville Nursery in the northwest Nashville market.

These acquisitions align with the company’s strategy to expand its product offerings across markets and create synergies through purchasing and cross-selling opportunities. Since 2014, SiteOne has completed 102 acquisitions, adding approximately $2,015 million in annualized net sales and 421 branches to its network.

The following chart illustrates SiteOne’s impressive acquisition track record:

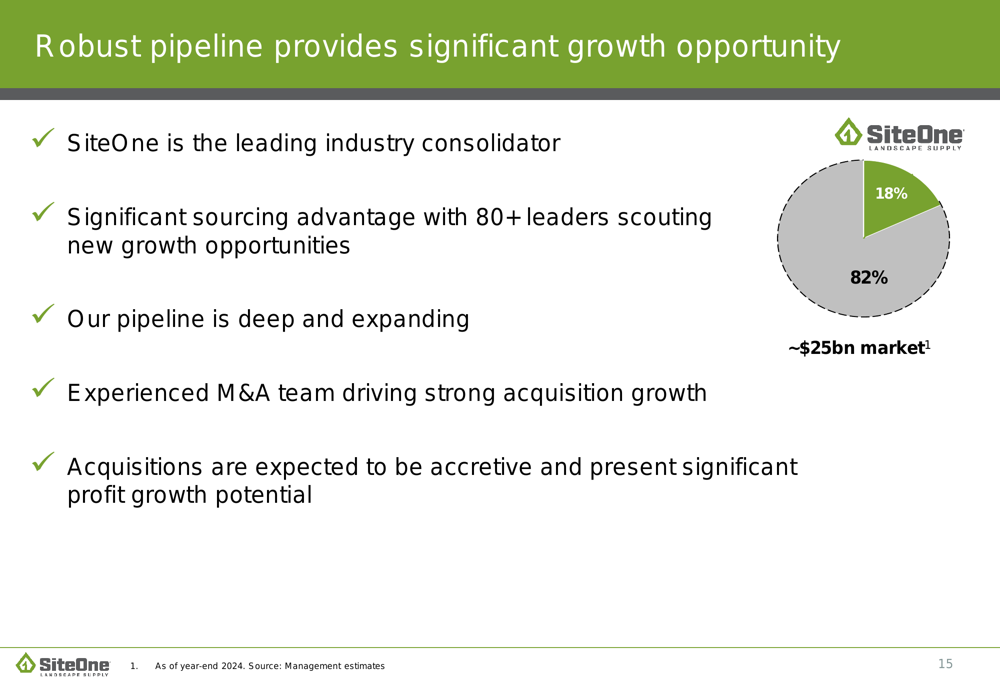

The company emphasized that significant growth opportunities remain, with only 18% of the $25 billion market consolidated and 82% still available for future acquisitions. SiteOne positions itself as the leading industry consolidator with an experienced M&A team and a deep pipeline of potential targets.

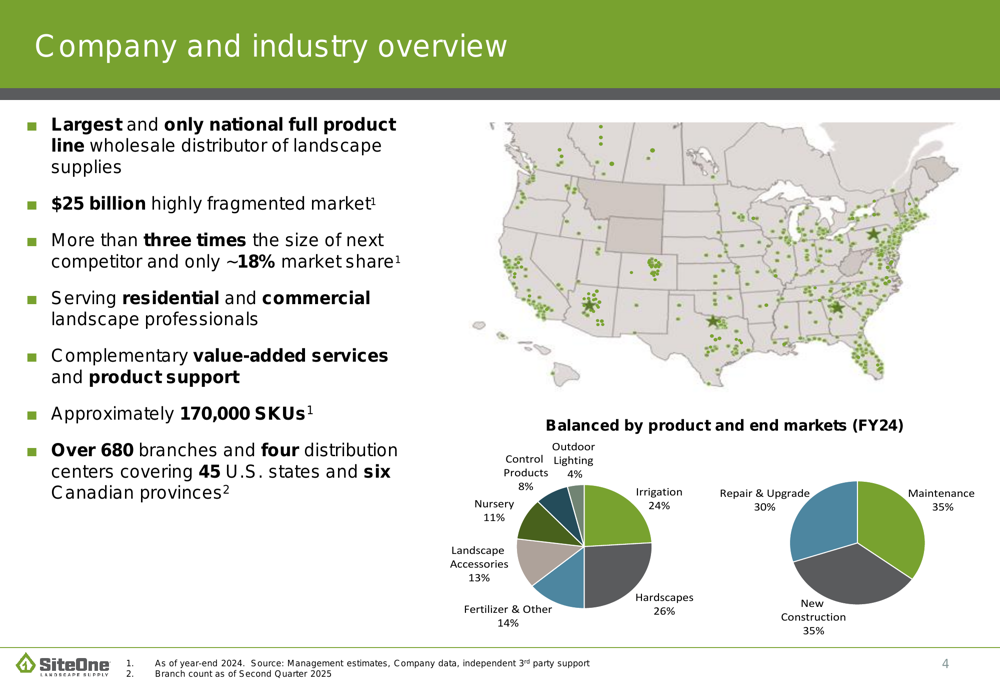

Market Position and Growth Strategy

SiteOne describes itself as the largest and only national full product line wholesale distributor of landscape supplies in a highly fragmented $25 billion market. The company has approximately 18% market share and is more than three times the size of its next competitor. With over 680 branches and four distribution centers covering 45 U.S. states and six Canadian provinces, SiteOne serves residential and commercial landscape professionals with approximately 170,000 SKUs.

The company’s market position and business breakdown are illustrated in the following slide:

SiteOne highlighted significant room for growth, noting that it offers all product lines in only about 25% of its target markets today. The company’s growth strategy focuses on leveraging the strengths of both a large and local company while driving commercial and operational performance through category management, supply chain improvements, salesforce performance, operational excellence, and marketing and digital initiatives.

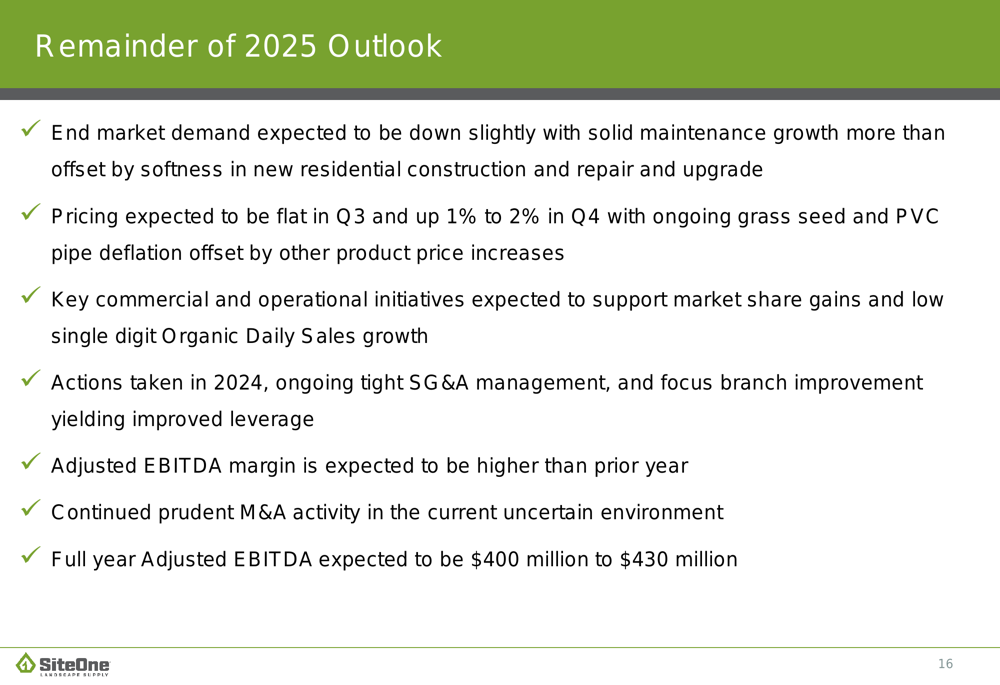

Outlook and Guidance

For the remainder of 2025, SiteOne expects end market demand to be down slightly, with solid maintenance growth more than offset by softness in new residential construction and repair and upgrade segments. Pricing is anticipated to be flat in Q3 and up 1% to 2% in Q4, with ongoing grass seed and PVC pipe deflation offset by other product price increases.

The company maintained its full-year Adjusted EBITDA guidance of $400 million to $430 million, consistent with the outlook provided in the first quarter. SiteOne expects its commercial and operational initiatives to support market share gains and low single-digit organic daily sales growth, while actions taken in 2024 and ongoing tight SG&A management are expected to yield improved leverage and higher Adjusted EBITDA margins compared to the prior year.

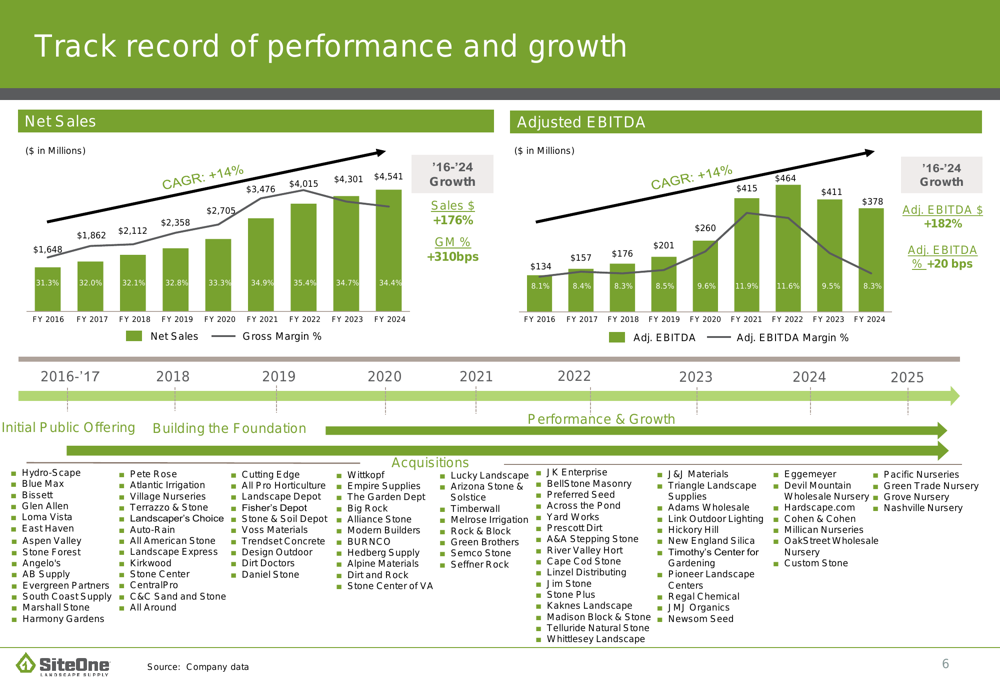

Long-Term Performance

SiteOne has demonstrated consistent growth over the years, with net sales increasing from $1,648 million in 2016 to $4,541 million in 2024, representing a compound annual growth rate (CAGR) of 14%. Similarly, Adjusted EBITDA grew at a 14% CAGR from $134 million in 2016 to $378 million in 2024.

The following chart illustrates the company’s track record of performance and growth:

Investment Highlights

SiteOne summarized its investment case by highlighting several key strengths: an uniquely attractive industry, clear market leadership, a proven management team, value-creating acquisitions, operational and commercial excellence, and a compelling and sustainable growth strategy.

Despite the company’s stock declining 1.85% to close at $128.57 on July 29, 2025, according to the provided fundamentals data, SiteOne’s Q2 results demonstrate resilience in a challenging market environment and continued execution of its long-term growth strategy.

The company’s focus on strategic acquisitions, margin improvement, and operational efficiency positions it well to navigate the current market conditions while continuing to consolidate the fragmented landscape supply industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.