Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

Sitio Royalties Corp (NYSE:STR) released its first quarter 2025 earnings presentation on May 7, highlighting strong operational and financial performance that exceeded analyst expectations. The oil and gas royalty company saw its stock rise 3.17% in aftermarket trading to $17.56, building on a modest 0.35% gain during regular trading hours.

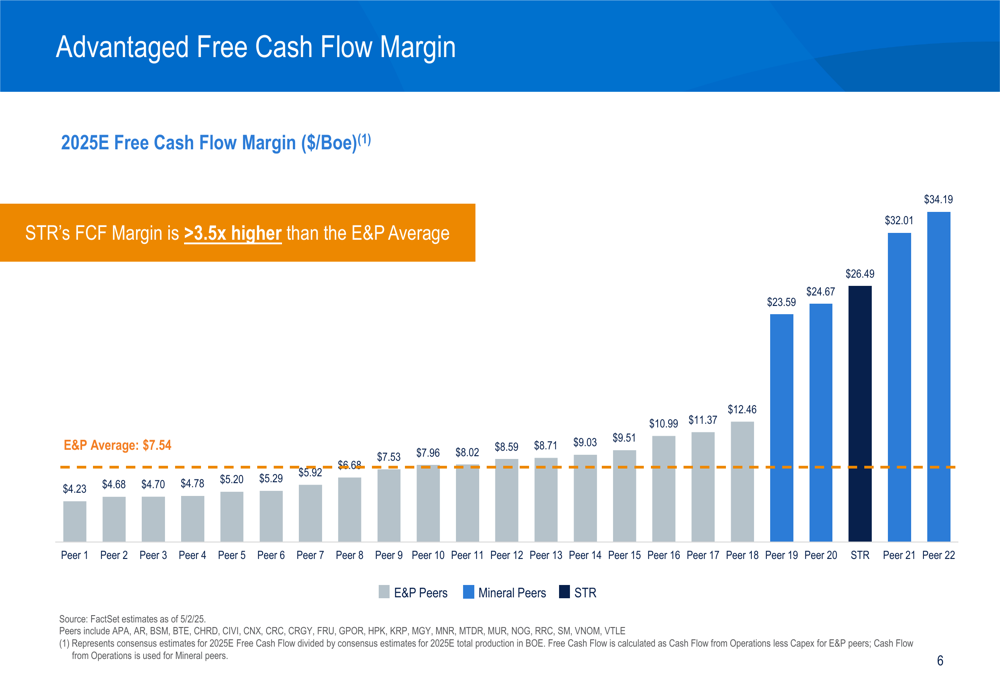

The company’s business model continues to demonstrate resilience in the current commodity price environment, with production levels surpassing the high end of full-year guidance and margins remaining robust at 87%. This performance comes as Sitio maintains its position as a leading consolidator in the highly fragmented minerals and royalties market.

Quarterly Performance Highlights

Sitio reported average daily production of 42.1 MBoe/d for Q1 2025, representing a 19% year-over-year increase and exceeding the high end of the company’s full-year guidance range of 38,250-41,250 Boe/d. Oil production reached 18.9 MBbls/d, a 3% increase compared to the same period last year.

The company generated $142 million in Adjusted EBITDA with an impressive 87% margin, along with $115 million in discretionary cash flow. Cash G&A expenses were well-controlled at $2.27 per Boe, below the midpoint of full-year guidance.

As shown in the following summary of Q1 highlights:

Sitio’s financial performance continues to benefit from its high-margin business model, which generates substantially higher free cash flow per barrel than traditional E&P companies. This advantage is clearly illustrated in the company’s presentation:

Strategic Advantages

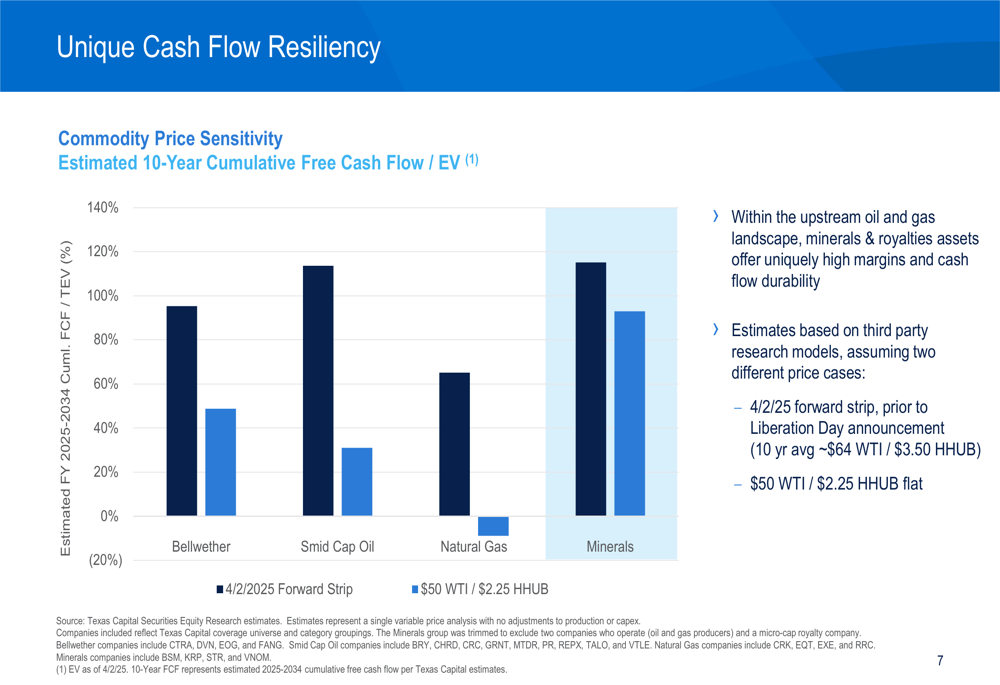

A key strength of Sitio’s business model is its resilience across different commodity price environments. The company’s presentation demonstrated that minerals and royalties assets offer uniquely high margins and cash flow durability compared to other upstream oil and gas companies.

As shown in the following chart comparing estimated 10-year cumulative free cash flow to enterprise value across different types of energy companies:

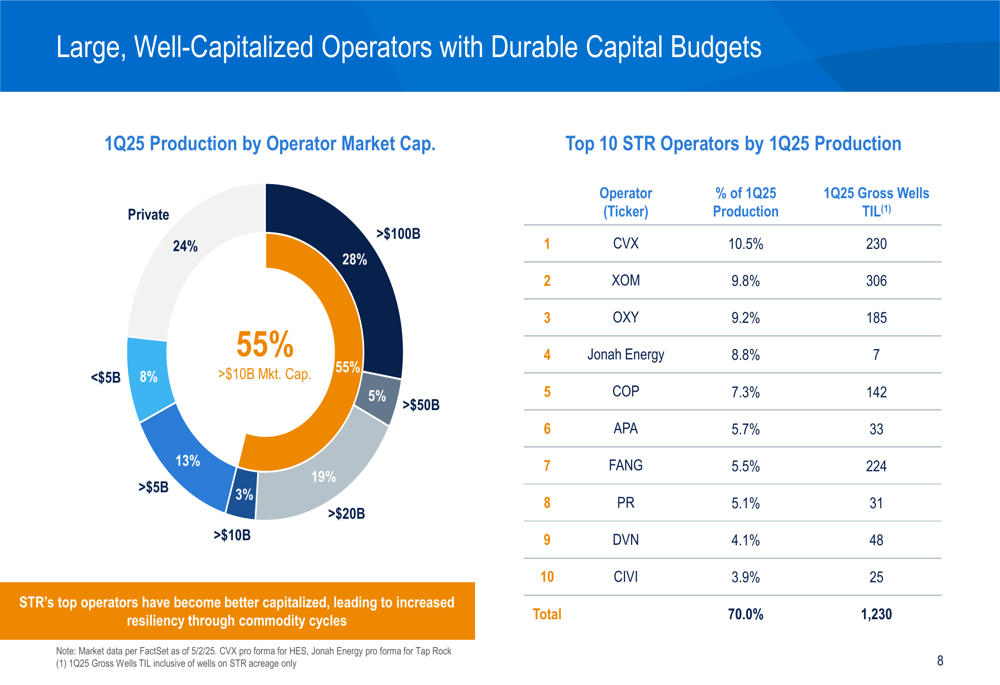

The quality of Sitio’s operator base further enhances its stability, with 55% of Q1 2025 production coming from operators with market capitalizations exceeding $10 billion. Top operators include industry leaders such as Chevron (NYSE:CVX), ExxonMobil (NYSE:XOM), and Occidental Petroleum (NYSE:OXY).

Sitio continues to leverage its proprietary asset management system to optimize value and cash flow. The company reported capturing $15 million in missing payments over the last twelve months through its reconciliation and recovery processes, offsetting approximately 40% of its projected 2025 Cash G&A expenses.

Capital Allocation & Shareholder Returns

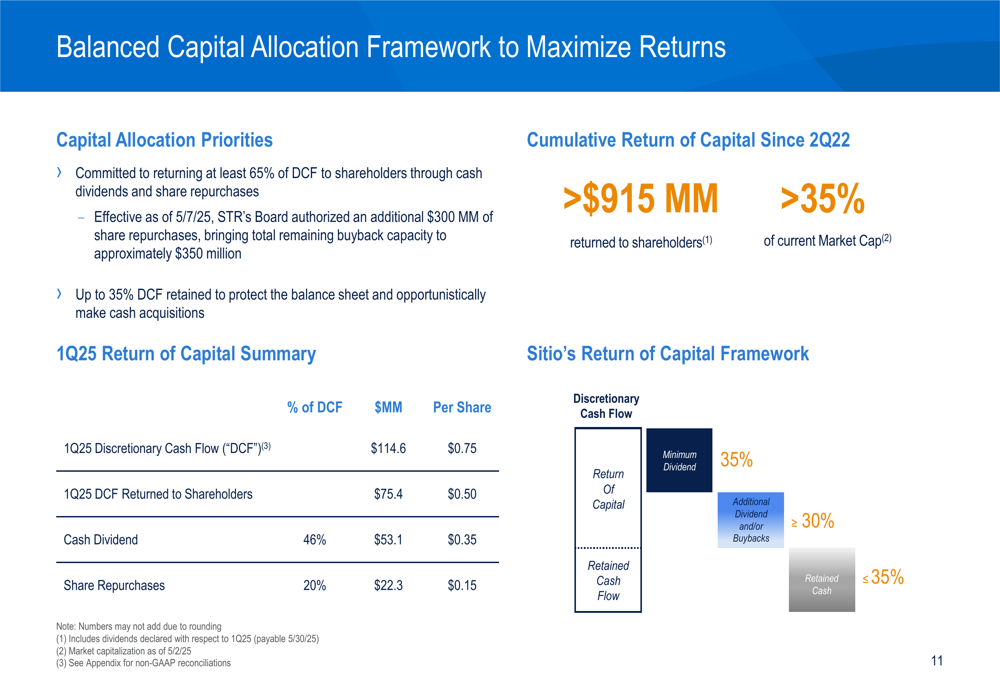

Sitio maintained its commitment to shareholder returns in Q1 2025, distributing $0.50 per share through a combination of a $0.35 cash dividend and stock repurchases equivalent to $0.15 per share. This brings the company’s cumulative return of capital since becoming public in 2022 to over $915 million, representing more than 35% of its current market capitalization.

The company’s balanced capital allocation framework is designed to maximize returns while maintaining financial flexibility:

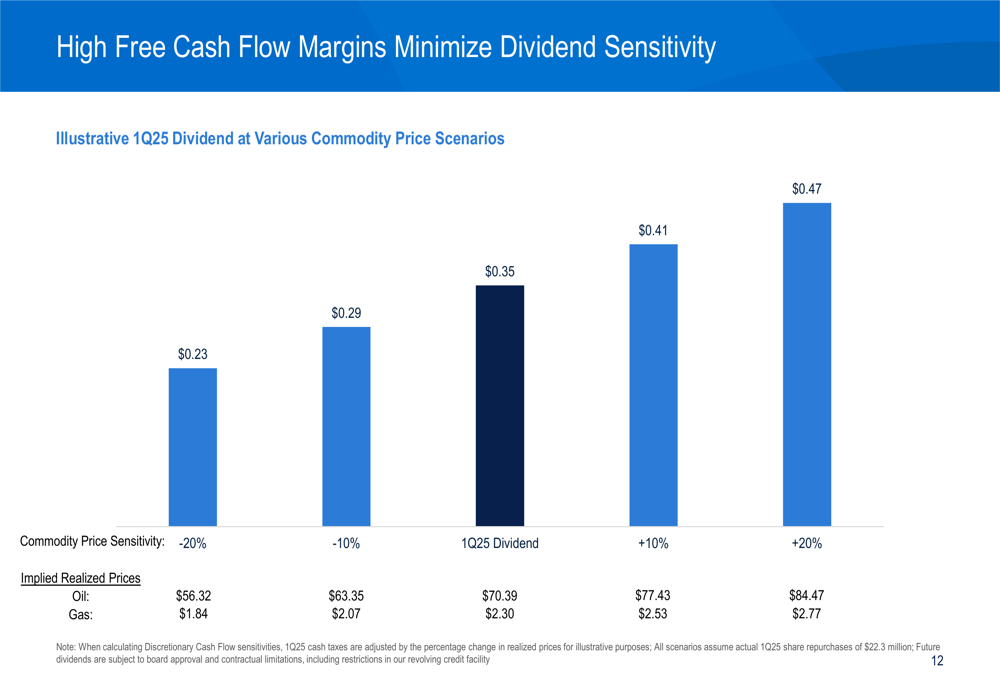

Sitio’s high free cash flow margins provide significant protection for its dividend program even in volatile commodity price environments. The company’s presentation illustrated how its Q1 2025 dividend would be affected under various commodity price scenarios:

Competitive Industry Position

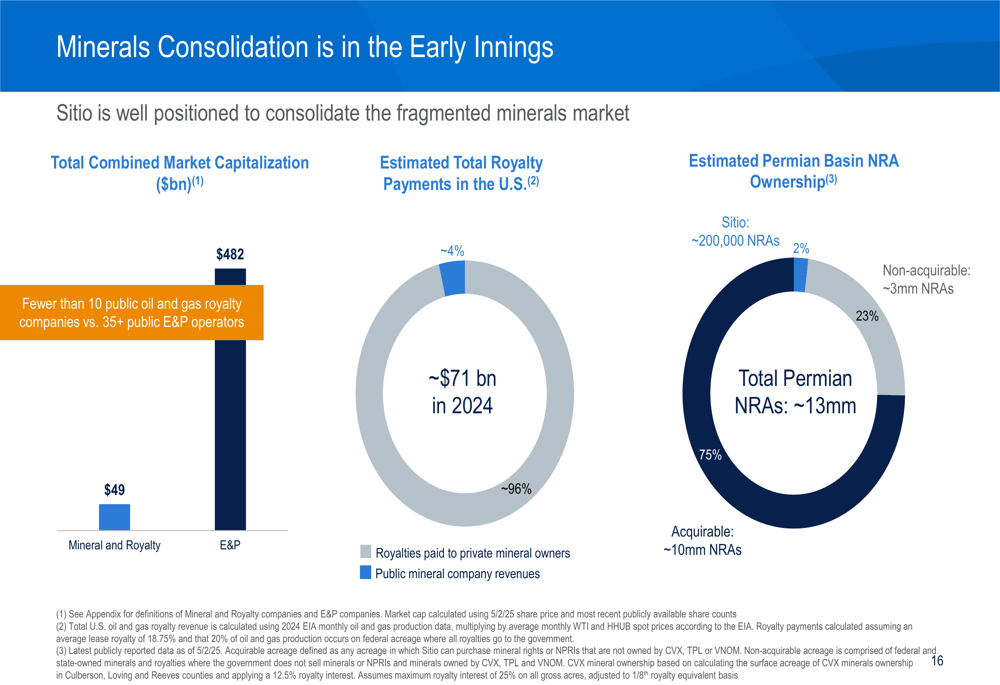

Sitio continues to highlight the significant consolidation opportunity in the minerals and royalties sector. Despite being one of the largest public mineral companies, Sitio owns only about 2% of the total Net Royalty Acres in the Permian Basin, underscoring the fragmented nature of the market and potential for future acquisitions.

The following chart illustrates the early stage of minerals consolidation compared to the broader E&P sector:

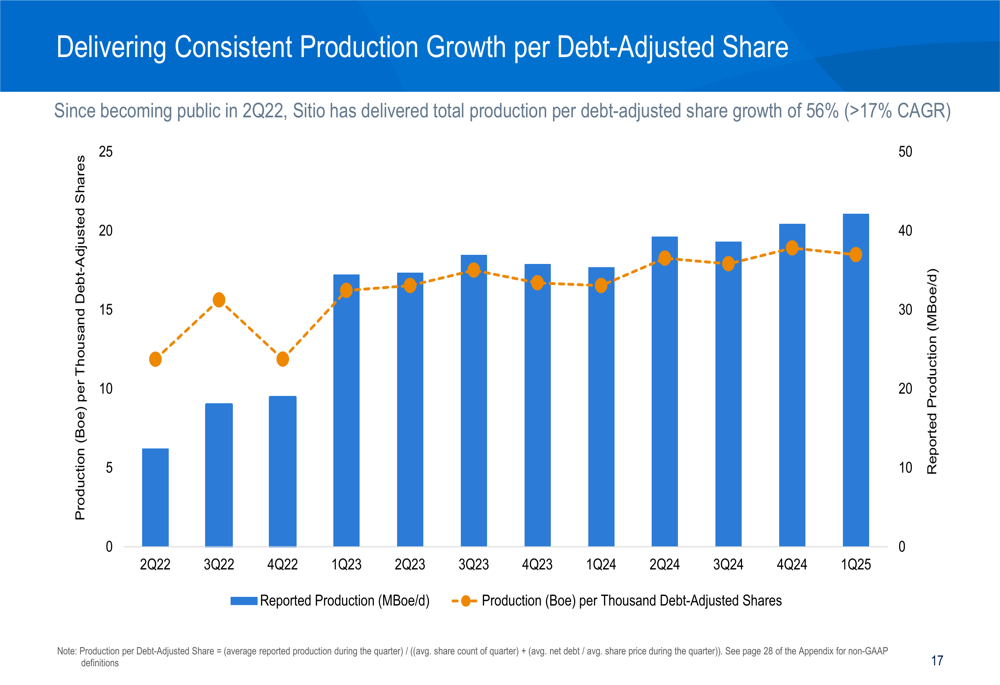

The company closed three acquisitions in Q1 2025 for approximately $21 million, adding around 1,350 Net Royalty Acres to its portfolio. These acquisitions align with Sitio’s returns-driven acquisition strategy, which has helped deliver consistent production growth per debt-adjusted share of 56% (>17% CAGR) since becoming public.

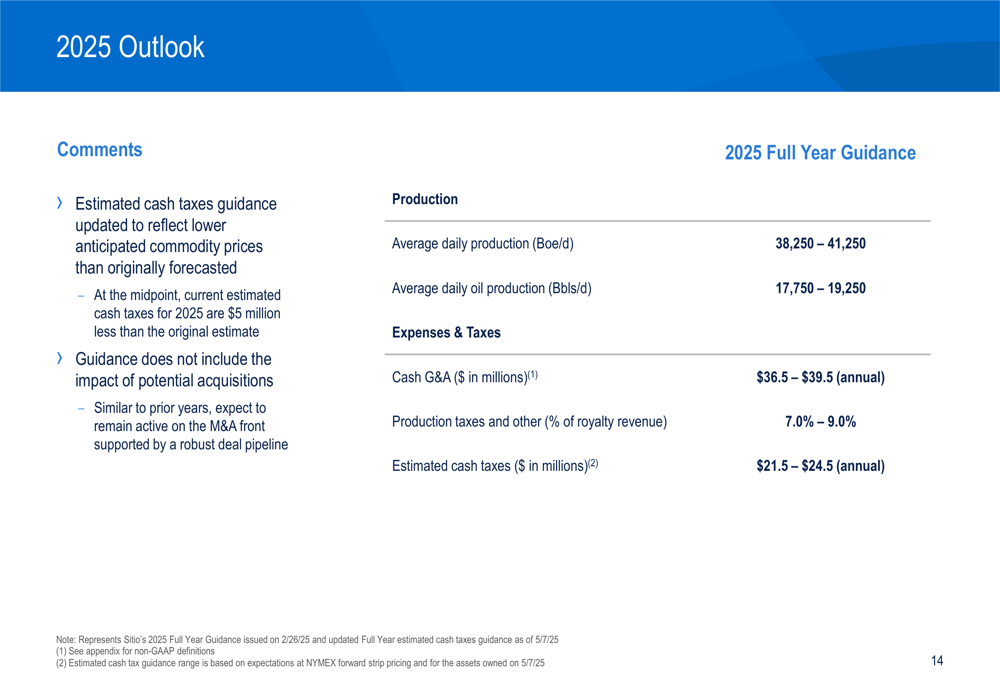

Forward Outlook

For full-year 2025, Sitio maintained its production guidance of 38,250-41,250 Boe/d, including oil production of 17,750-19,250 Bbls/d. The company expects Cash G&A expenses of $36.5-39.5 million and production taxes of 7.0-9.0% of royalty revenue.

Sitio’s financial position remains strong, with a net debt of $1.084 billion against a revolving credit facility borrowing base of $925 million. The company has no near-term debt maturities and maintains $441 million in liquidity, providing flexibility for future acquisitions and shareholder returns.

Looking ahead, Sitio is well-positioned to continue benefiting from operator activity on its acreage, with 48.6 net wells in its line-of-sight pipeline as of March 31, 2025, representing an 8% increase quarter-over-quarter. The company’s inventory of over 50,000 gross normalized remaining wells (429 net) provides visibility into long-term production potential across its diversified asset base.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.