Fed Governor Adriana Kugler to resign

Executive Summary

Snap-on Incorporated (NYSE:SNA) reported declining sales and earnings for the first quarter of 2025, according to the company’s quarterly financial presentation released on April 17. Net sales decreased 3.5% to $1,141.1 million compared to $1,182.3 million in the same period last year, with organic sales down 2.3% and currency translation having a negative 1.2% impact.

Diluted earnings per share fell 8.1% to $4.51 from $4.91 in Q1 2024, while operating earnings before financial services decreased 10.3% to $243.1 million. Despite the overall decline, the company maintained a strong financial position with $1,434.9 million in cash and a negative net debt to capital ratio of 4.4%.

In premarket trading following the release, Snap-on shares were down 5.21% at $314.70, reflecting investor concerns about the company’s performance.

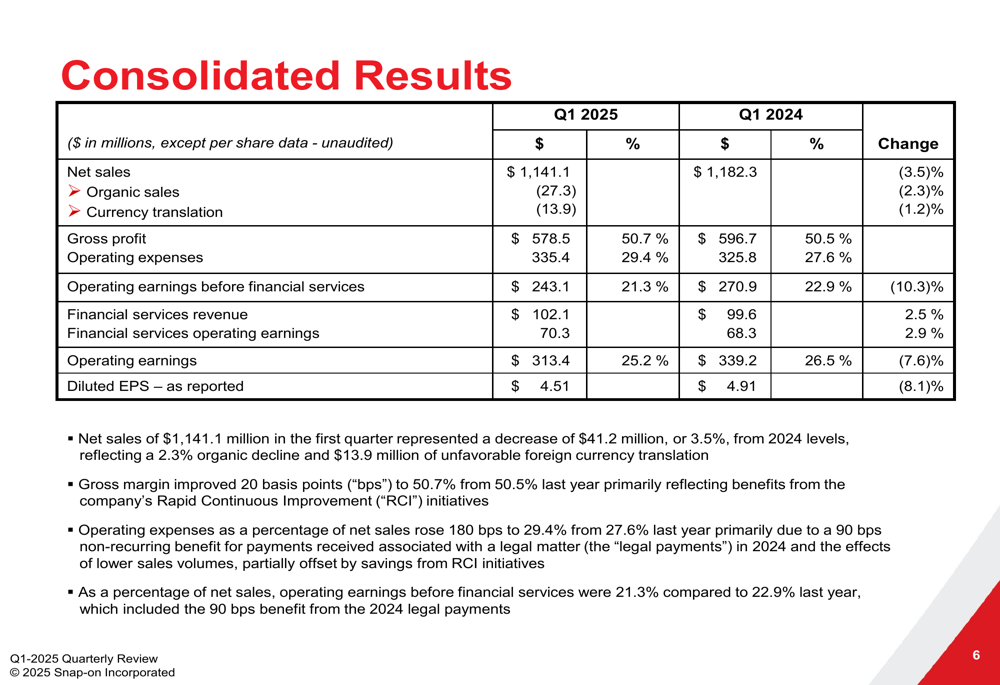

Consolidated Financial Performance

Snap-on’s first quarter results showed pressure across most business segments, though gross margin improved slightly to 50.7% from 50.5% in the prior year. Operating expenses as a percentage of net sales increased to 29.4% from 27.6%, contributing to the decline in operating earnings.

As shown in the following consolidated results chart, the company’s overall operating earnings margin decreased to 21.3% from 22.9% in Q1 2024:

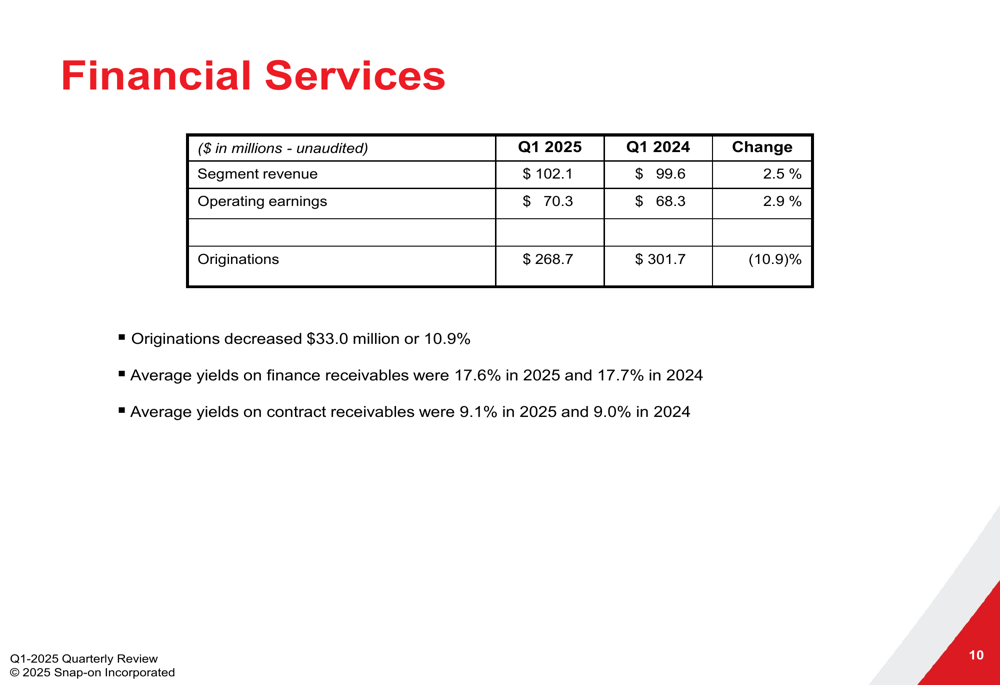

Financial services continued to be a bright spot, with revenue increasing 2.5% to $102.1 million and operating earnings rising 2.9% to $70.3 million. However, this growth was not enough to offset the decline in the tools and industrial segments.

Total (EPA:TTEF) consolidated operating earnings were $313.4 million, representing 25.2% of revenues, down from $339.2 million or 26.5% in the prior year.

Segment Analysis

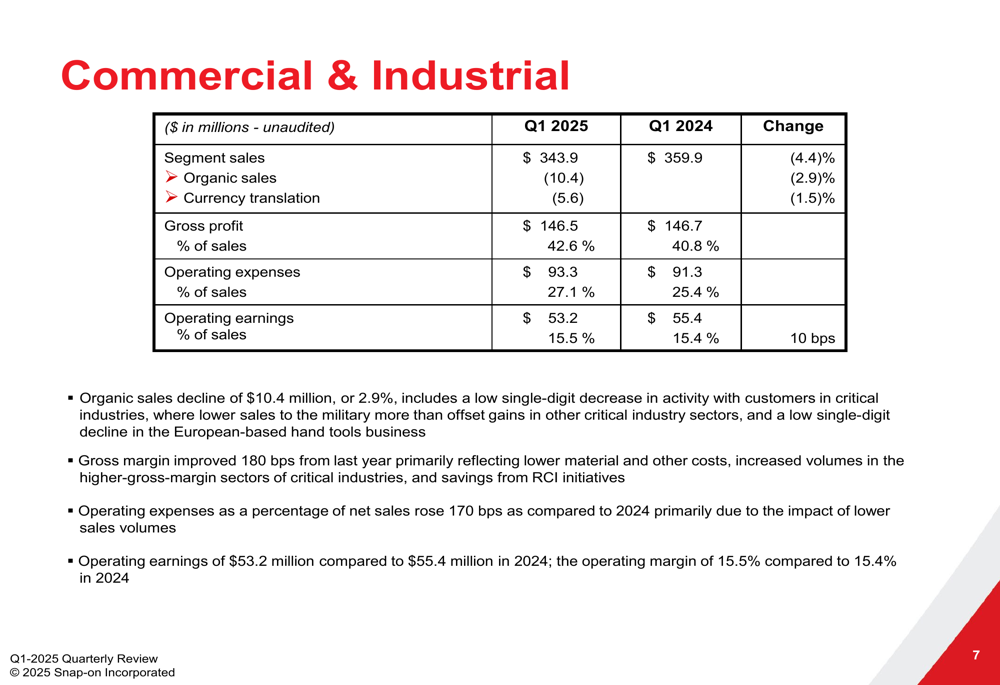

Snap-on’s performance varied significantly across its business segments, with only the Repair Systems & Information group showing growth.

The Commercial & Industrial segment reported sales of $343.9 million, down 4.4% from Q1 2024, with organic sales declining 2.9% and currency translation having a negative 1.5% impact. Despite the sales decrease, the segment’s gross margin improved 180 basis points to 42.6%, while operating earnings fell to $53.2 million from $55.4 million in the prior year.

The segment results are detailed in the following chart:

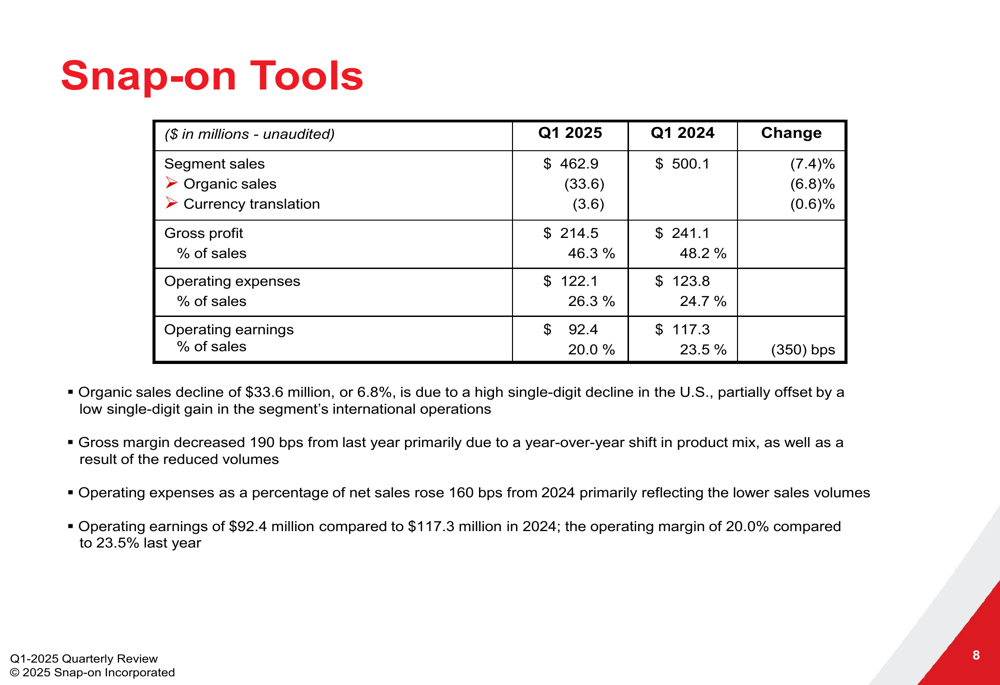

The Snap-on Tools segment, which represents the company’s largest business unit, experienced the steepest decline with sales falling 7.4% to $462.9 million. Organic sales were down 6.8%, with currency translation accounting for an additional 0.6% decrease. Operating earnings in this segment dropped significantly to $92.4 million from $117.3 million in Q1 2024, with operating margin declining to 20.0% from 23.5%.

The following chart illustrates the Tools segment’s performance:

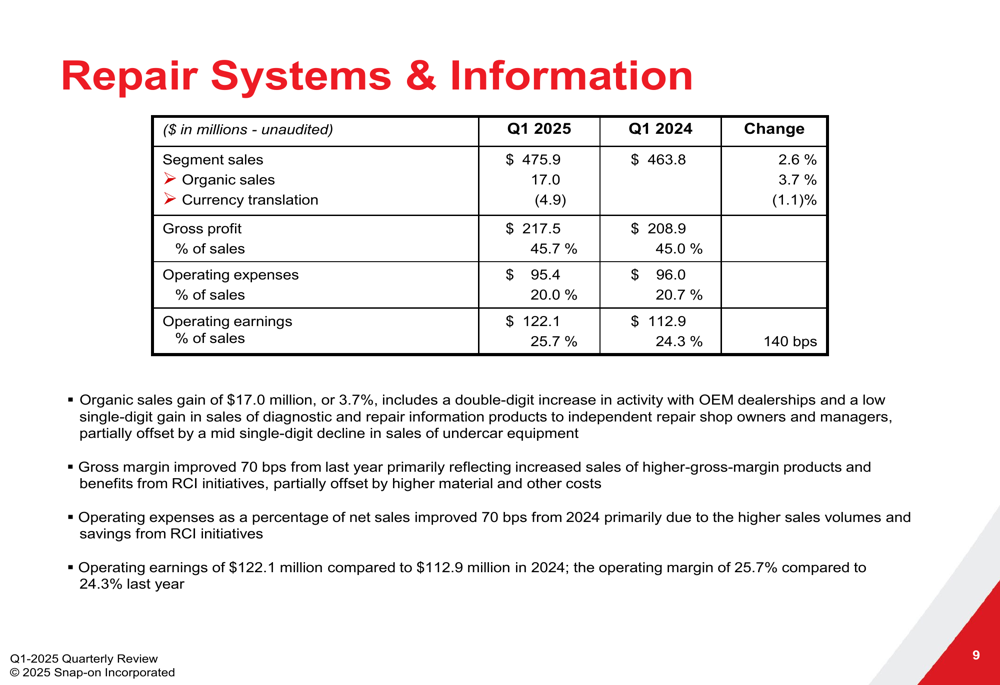

In contrast, the Repair Systems & Information segment was the only business unit to report growth, with sales increasing 2.6% to $475.9 million. Organic sales rose 3.7%, partially offset by a 1.1% negative impact from currency translation. The segment’s operating earnings grew to $122.1 million from $112.9 million, with operating margin improving to 25.7% from 24.3%.

As shown in the following chart, this segment demonstrated resilience despite the challenging environment:

The Financial Services segment continued its positive trajectory with revenue growing 2.5% to $102.1 million and operating earnings increasing 2.9% to $70.3 million. However, originations decreased 10.9% to $268.7 million from $301.7 million in Q1 2024, potentially signaling caution among customers.

Balance Sheet and Cash Flow

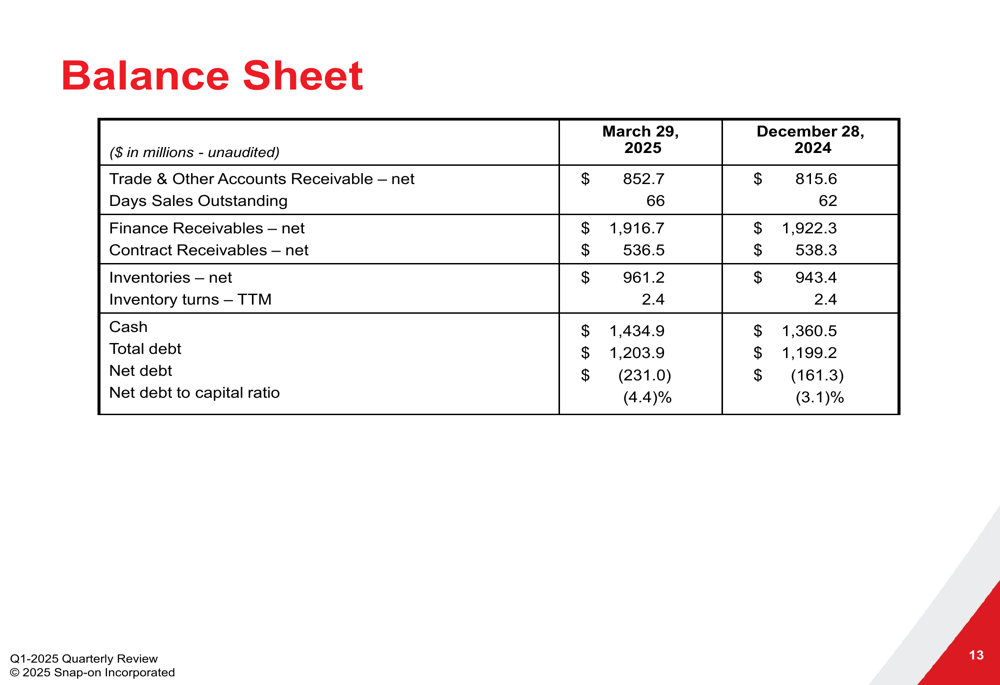

Snap-on maintained a strong financial position with $1,434.9 million in cash as of March 29, 2025, up from $1,360.5 million at the end of 2024. Total debt stood at $1,203.9 million, resulting in a negative net debt position of $231.0 million and a net debt to capital ratio of -4.4%.

The company’s balance sheet highlights are illustrated in the following chart:

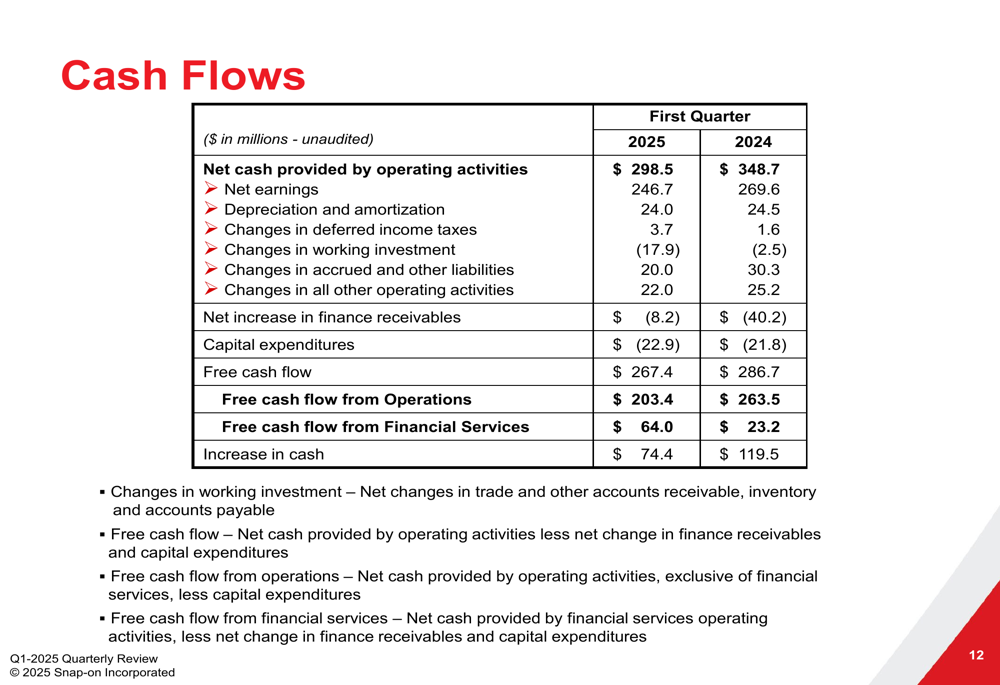

Cash flow generation remained robust despite the earnings decline. Net cash provided by operating activities was $298.5 million, down from $348.7 million in Q1 2024. Free cash flow totaled $267.4 million compared to $286.7 million in the prior year.

The following chart details the company’s cash flow performance:

Inventory management showed slight deterioration, with inventory turns remaining at 2.4, while days sales outstanding increased to 66 days from 62 days at the end of 2024.

Market Context and Outlook

Snap-on’s Q1 2025 results represent a continuation of the sales pressure seen in previous quarters, but with a more pronounced impact on profitability. In Q3 2024, the company reported a 1.7% organic sales decline but managed to increase EPS by 4.2% to $4.70 through margin improvements and cost management.

The contrast between Q3 2024 and Q1 2025 results suggests that market conditions have become more challenging for Snap-on, particularly in the Tools segment where sales declined 6.8% organically compared to a 3.1% decline in Q3 2024.

The growth in the Repair Systems & Information segment provides some optimism, indicating continued demand for diagnostic and information products in the automotive repair industry. However, the significant decline in the Tools segment, which has historically been Snap-on’s core business, raises concerns about the company’s near-term growth prospects.

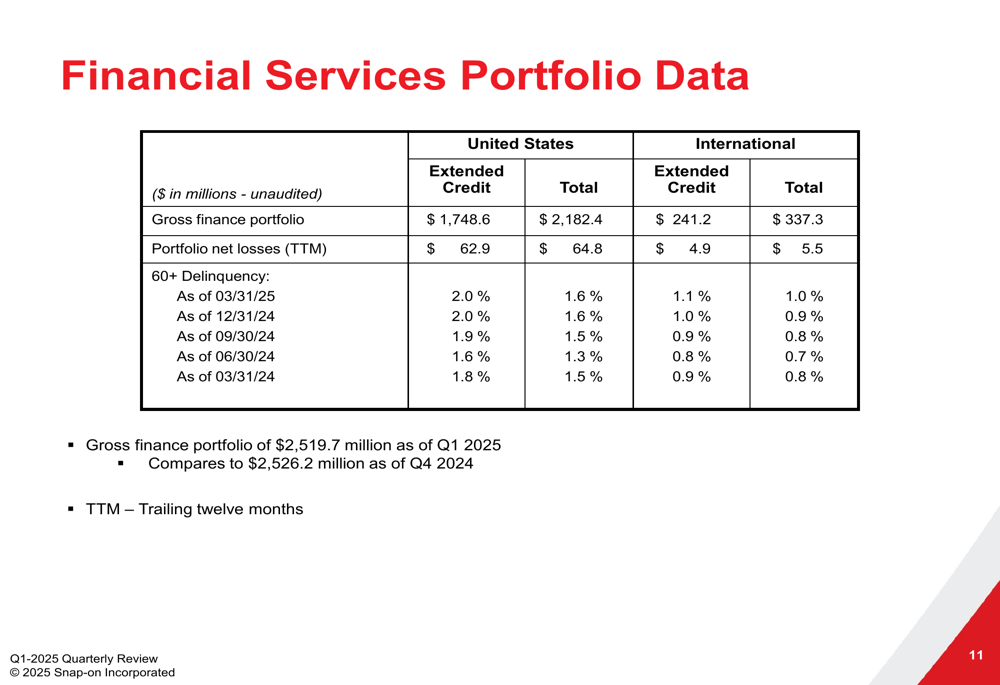

The Financial Services portfolio data shows relatively stable delinquency rates, with 60+ day delinquencies at 2.0% for U.S. extended credit as of March 31, 2025, unchanged from December 31, 2024. This suggests that while customers may be more cautious with new purchases, existing customers are maintaining their payment obligations.

As Snap-on celebrates its 105th anniversary in 2025, the company faces the challenge of navigating a difficult market environment while maintaining its position as a provider of premium tools and equipment. The company’s strong financial position provides flexibility to weather the current headwinds, but investors will be watching closely for signs of improvement in the Tools segment in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.