Wall St futures steady after extended losses on Nvidia, payrolls caution

Introduction & Market Context

Solaris Energy Infrastructure Inc (NYSE:SEI), formerly known as Solaris Oilfield Infrastructure, presented its Q3 2025 earnings supplement on November 4, 2025, outlining ambitious growth plans despite mixed financial results. The company's stock fell 7.71% to $49.81 following the release, reflecting investor concerns over a slight earnings miss despite strong revenue performance.

SEI reported Q3 earnings per share of $0.32, narrowly missing analyst expectations of $0.33, while revenue surged to $167 million, exceeding forecasts of $140.48 million by 18.88%. The company's Power Solutions segment drove over 60% of total revenue, highlighting its successful pivot from traditional oilfield services to broader energy infrastructure.

Quarterly Performance Highlights

SEI reported Q3 2025 Adjusted EBITDA of $68 million, representing a 12% increase from the previous quarter and threefold growth year-over-year. This performance was driven by the company's expanding power generation fleet, which averaged 760 MW during Q3, a 27% increase from the prior quarter.

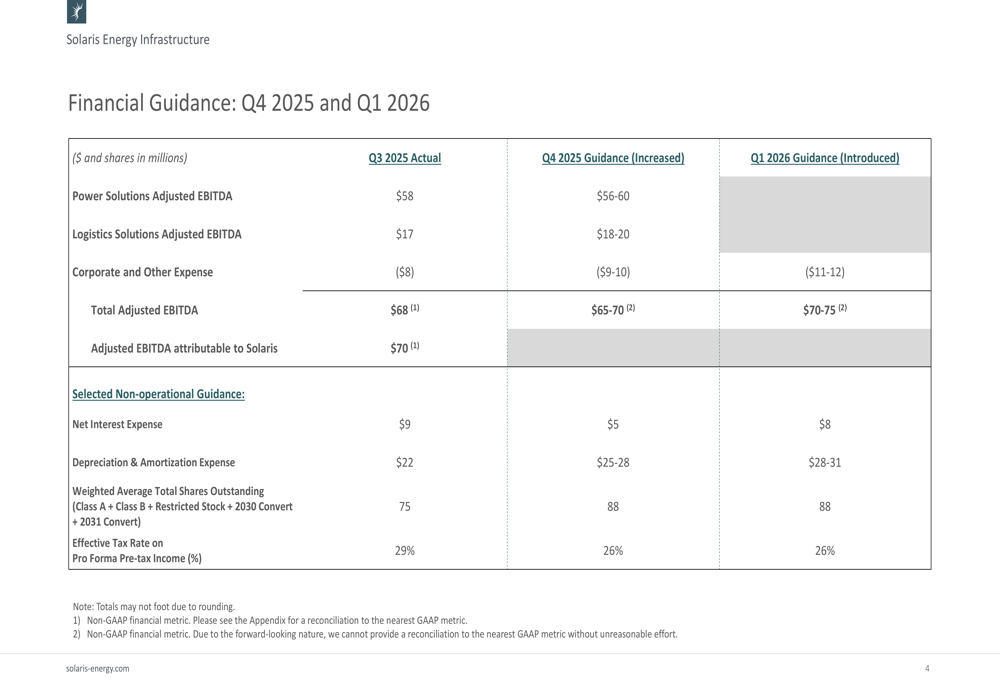

As shown in the following financial guidance table, the company has increased its Q4 2025 guidance and introduced Q1 2026 projections, signaling confidence in continued growth:

The Power Solutions segment contributed $58 million to Q3 Adjusted EBITDA, while Logistics Solutions added $17 million. Corporate expenses of $8 million partially offset these gains. The company expects further growth in Q4 with total Adjusted EBITDA projected at $65-70 million, followed by $70-75 million in Q1 2026.

Growth Strategy and Capital Expenditure

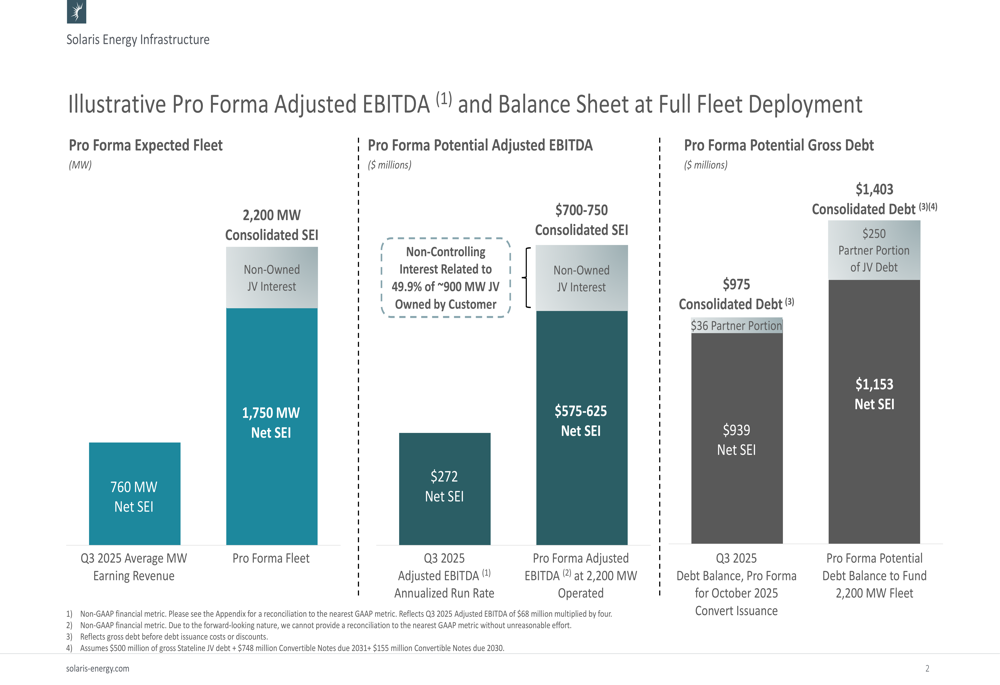

The centerpiece of SEI's presentation was its ambitious growth strategy, targeting expansion from the current 760 MW average capacity to 2,200 MW by early 2028. This expansion is expected to more than double the company's Adjusted EBITDA potential.

The following slide illustrates SEI's pro forma projections at full fleet deployment:

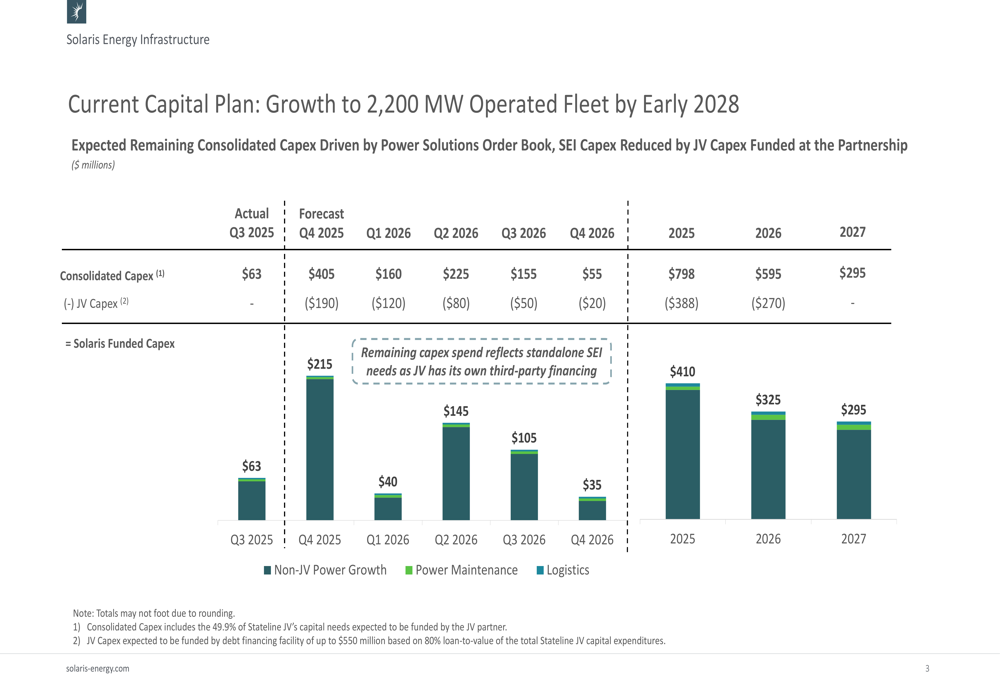

To achieve this growth, SEI outlined a detailed capital expenditure plan through 2027, with significant investments front-loaded in the coming quarters. The plan shows consolidated capex of $798 million in 2025, $595 million in 2026, and $295 million in 2027, with a portion funded through joint venture partnerships.

The quarterly breakdown of capital expenditures reveals the aggressive near-term investment strategy:

During the earnings call, Chairman and Co-CEO Bill Zartler emphasized the scale of opportunity, noting, "The pipeline is enormous... I've never seen anything like it in my life," while Co-CEO Amanda Brock added, "The speed at which this market is moving is unprecedented."

Debt Structure and Financing

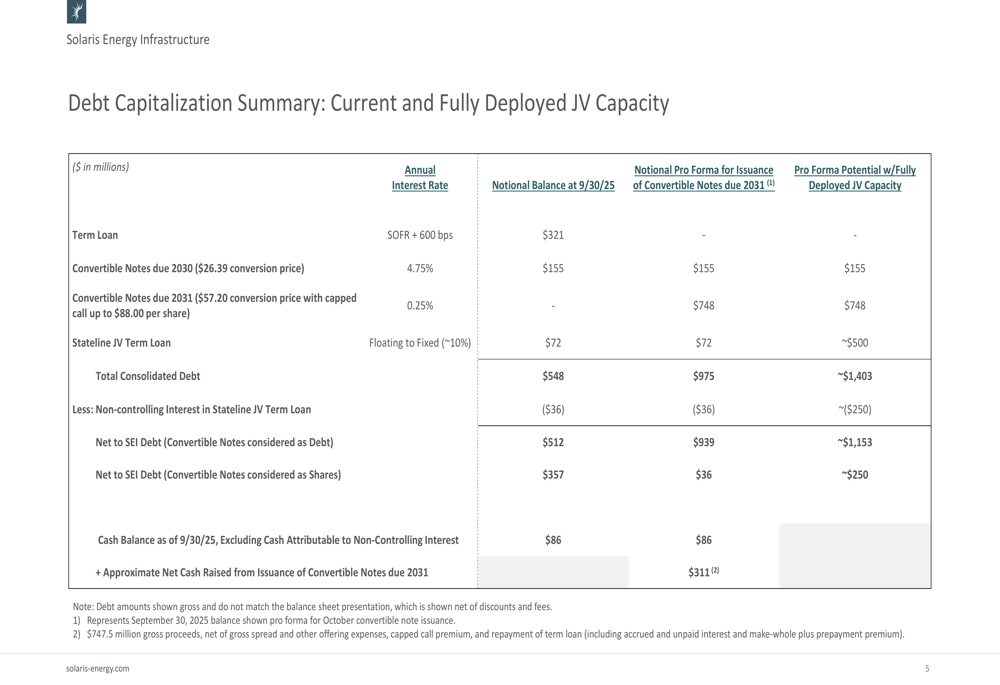

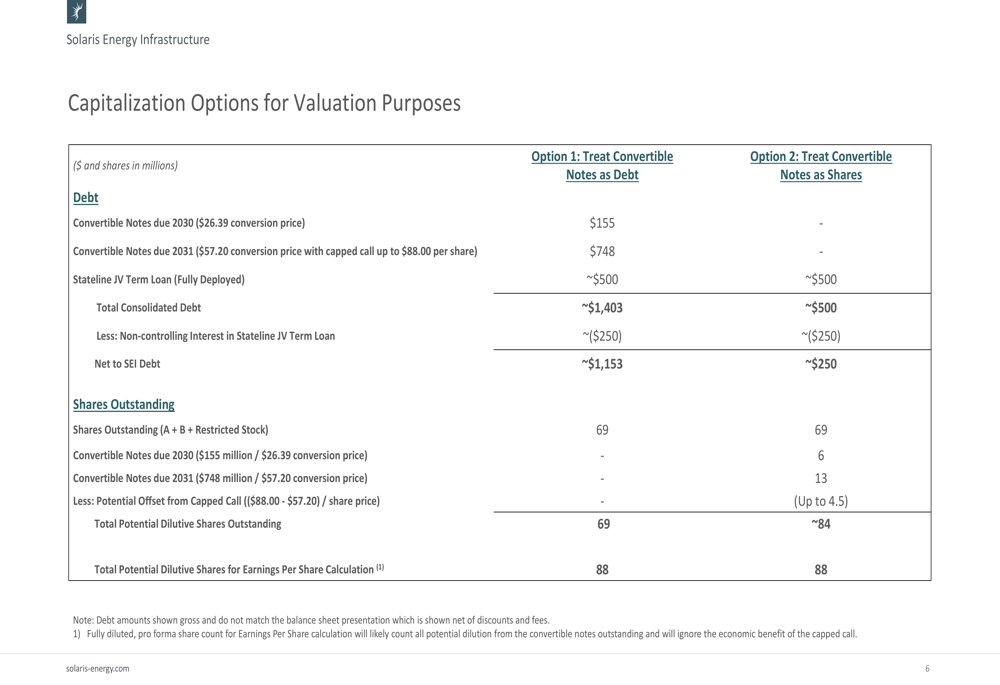

To fund its growth initiatives, SEI has significantly restructured its debt profile, most notably through the recent issuance of $748 million in convertible notes due 2031 with a $57.20 conversion price. This issuance, along with other debt management strategies, is detailed in the company's debt capitalization summary:

The company presents two approaches to evaluating its capitalization structure - treating convertible notes as either debt or equity - which significantly impacts how investors might assess SEI's leverage:

If convertible notes are treated as debt, SEI's pro forma net debt would be approximately $1,153 million at full deployment. However, if considered as equity, this figure drops dramatically to around $250 million, highlighting the hybrid nature of the company's financing strategy.

Forward Guidance and Outlook

Looking beyond the immediate quarters, SEI projects potential consolidated Adjusted EBITDA of $700-750 million once the full 2,200 MW fleet is deployed, with $575-625 million attributable to SEI after accounting for joint venture interests. This represents more than a doubling from the current annualized run rate of $272 million.

Despite this optimistic outlook, investors appear cautious, as reflected in the stock's decline following the earnings release. This may stem from concerns about execution risks in scaling operations, potential supply chain complexities, and the substantial capital requirements to achieve the projected growth.

The market reaction also suggests some skepticism about the company's ability to maintain profitability margins while expanding so rapidly. With a current stock price of $49.81, SEI trades below its 52-week high of $57.165, indicating that investors are taking a measured view of the company's ambitious plans despite its strong revenue performance.

As SEI continues its transformation from an oilfield services provider to a comprehensive energy infrastructure company, its ability to execute on its growth strategy while managing capital expenditures and debt levels will be crucial for future valuation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.