Oil prices rebound sharply on smaller-than-feared OPEC+ output hike

Introduction & Market Context

Solaris Energy Infrastructure Inc. (NYSE:SEI) released its Q2 2025 earnings presentation on July 23, 2025, revealing an ambitious growth strategy focused on expanding its power generation fleet. The company’s stock closed at $28.27, up 4.03% on the day, with an additional 1.84% gain in after-hours trading, signaling positive investor reception to the quarterly results and forward-looking plans.

The presentation highlights Solaris’s ongoing transformation from its traditional oilfield infrastructure roots to a broader energy infrastructure company, with a particular emphasis on data center power solutions. This strategic pivot comes amid surging demand for reliable power generation for data centers and other critical infrastructure.

Quarterly Performance Highlights

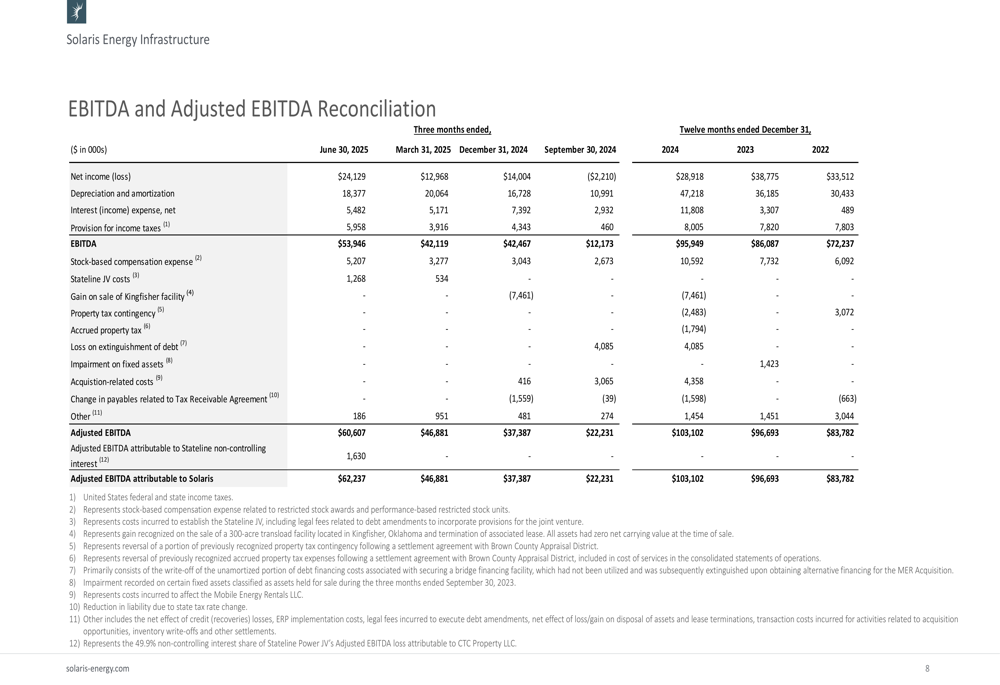

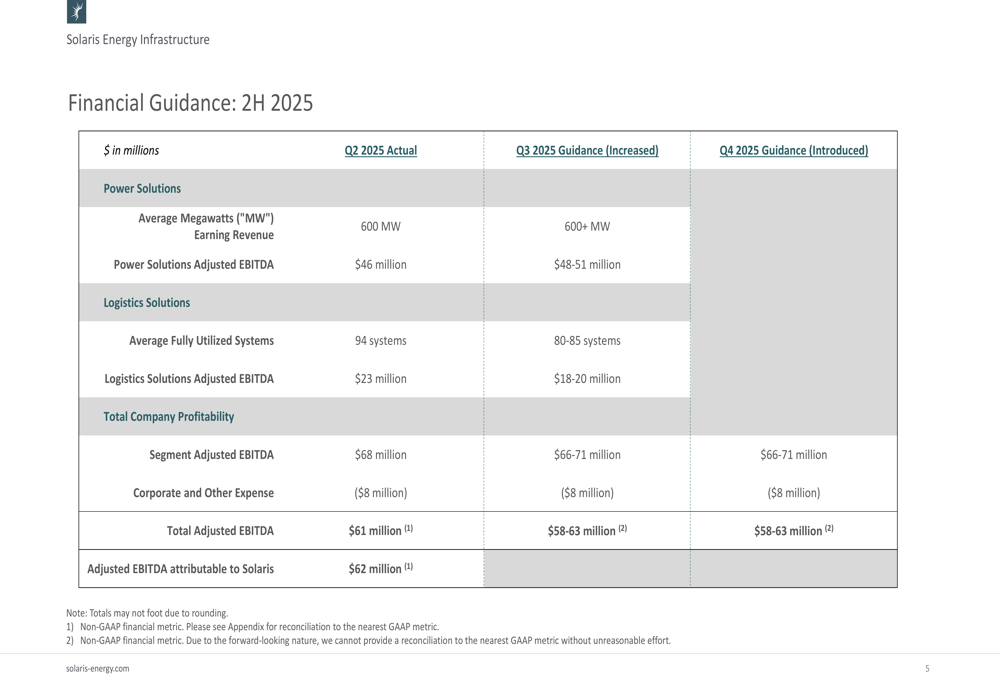

Solaris reported solid financial results for Q2 2025, with a net income of $24.1 million and total Adjusted EBITDA of $61 million. The company’s Power Solutions segment, which currently operates 600 MW of capacity, generated $46 million in Adjusted EBITDA, while the Logistics Solutions segment contributed $23 million from 94 fully utilized systems.

As shown in the detailed EBITDA reconciliation, the company’s performance demonstrates continued profitability and operational efficiency:

These results build upon the momentum from Q1 2025, when the company beat earnings expectations with an EPS of $0.20 against a forecast of $0.14. The Q2 performance reflects the company’s successful execution of its strategic initiatives and operational efficiencies.

Growth Strategy and Market Exposure

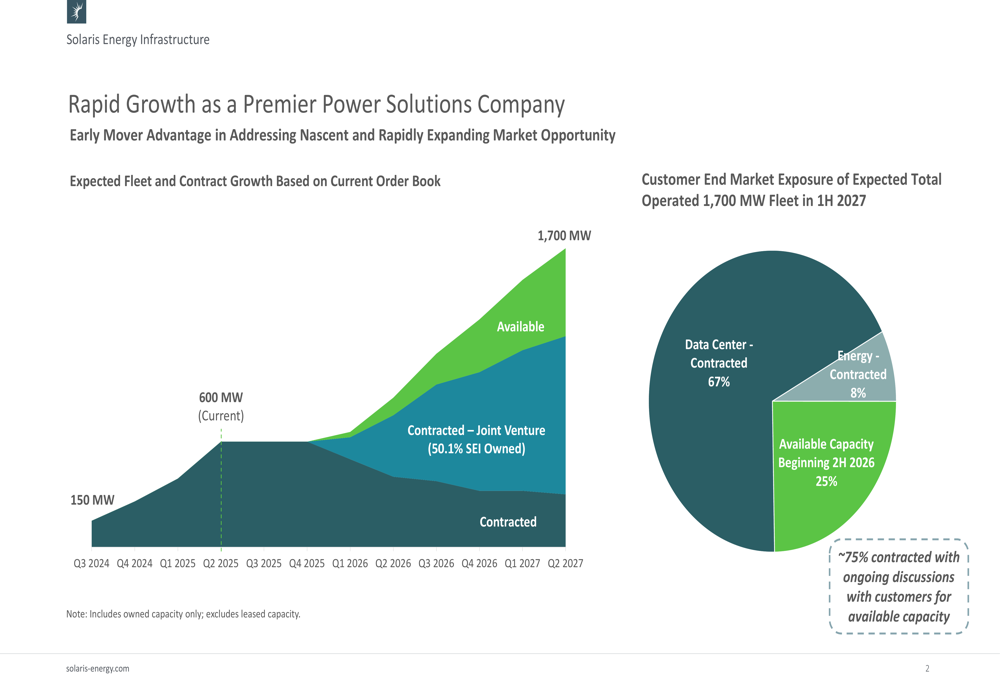

The centerpiece of Solaris’s presentation is its ambitious growth plan to expand from the current 600 MW fleet to 1,700 MW by Q2 2027. This expansion strategy is supported by a strong order book, with approximately 75% of the available capacity already under contract or in advanced discussions with customers.

The following chart illustrates the company’s projected fleet growth and contract status:

Notably, the company’s customer end market exposure reveals a significant focus on data centers, which account for 67% of the expected contracted capacity by 1H 2027. Energy sector customers represent 8% of contracted capacity, with the remaining 25% currently available but expected to be contracted beginning in 2H 2026.

This strategic focus on data centers represents a significant pivot from the company’s traditional oilfield services business, positioning Solaris to capitalize on the growing demand for reliable power solutions in the rapidly expanding data center market.

Detailed Financial Analysis

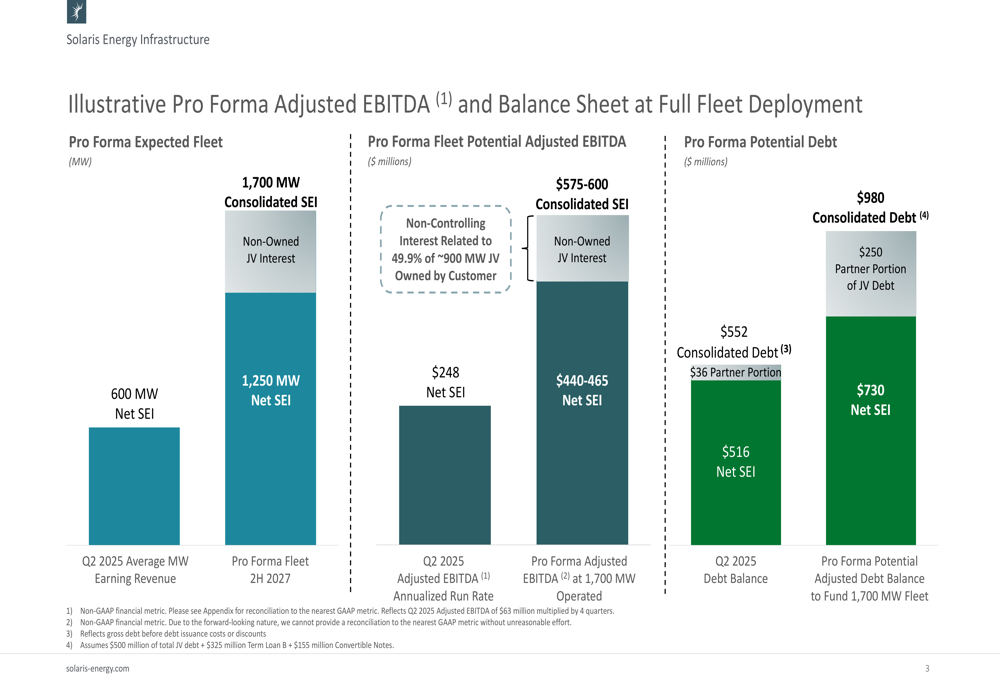

The financial implications of Solaris’s growth strategy are substantial, with projected increases in both adjusted EBITDA and debt levels. The company provided a pro forma analysis of its expected financial position once the full 1,700 MW fleet is deployed.

The following chart shows the projected financial impact of the expanded fleet:

At full deployment, Solaris projects consolidated adjusted EBITDA of $575-600 million, a significant increase from the current $248 million. This growth will be funded in part through additional debt, with consolidated debt projected to increase from the current $552 million to approximately $980 million.

Despite the increased leverage, the company expects to maintain a manageable debt profile, with a portion of the debt ($250 million) attributable to joint venture partners. The net debt attributable to Solaris is expected to be approximately $730 million against net adjusted EBITDA of $440-465 million, suggesting a healthy debt-to-EBITDA ratio.

Capital Expenditure Plan

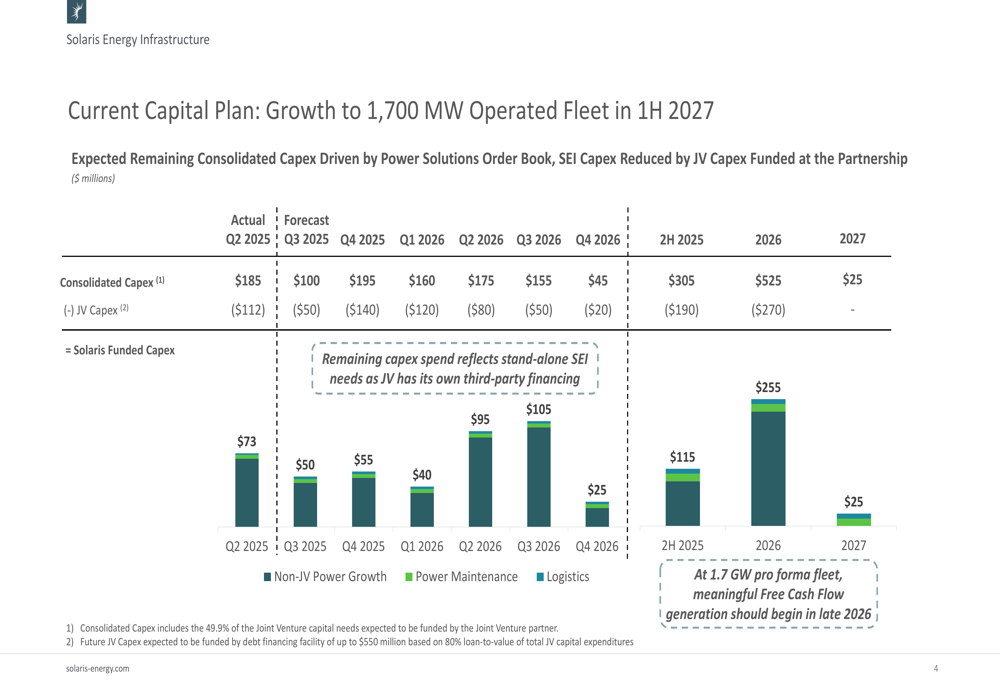

To achieve its growth targets, Solaris has outlined a comprehensive capital expenditure plan through 2027. The plan details both consolidated capital expenditures and the portion funded through joint ventures.

The following chart breaks down the planned capital expenditures by category and timing:

The company plans to invest $73 million in Q2 2025, followed by $115 million in the second half of 2025, $255 million in 2026, and $25 million in 2027. These investments are categorized into non-JV power growth, power maintenance, and logistics.

A key takeaway from the capital plan is that Solaris expects to begin generating meaningful free cash flow in late 2026 once the 1.7 GW fleet is fully operational. This inflection point could mark a significant transition for the company from growth-focused capital deployment to cash generation and potential shareholder returns.

Financial Guidance and Outlook

For the remainder of 2025, Solaris provided detailed financial guidance that suggests stable performance with modest growth. The company expects its Power Solutions segment to maintain at least 600 MW of capacity earning revenue in both Q3 and Q4, with adjusted EBITDA of $48-51 million per quarter.

The following table outlines the company’s financial guidance for the second half of 2025:

The Logistics Solutions segment is expected to see a slight decline in utilized systems from 94 in Q2 to 80-85 in both Q3 and Q4, with corresponding adjusted EBITDA of $18-20 million per quarter. Overall, the company projects total adjusted EBITDA of $58-63 million for both Q3 and Q4, slightly below the $61 million achieved in Q2 2025.

Additional financial guidance includes:

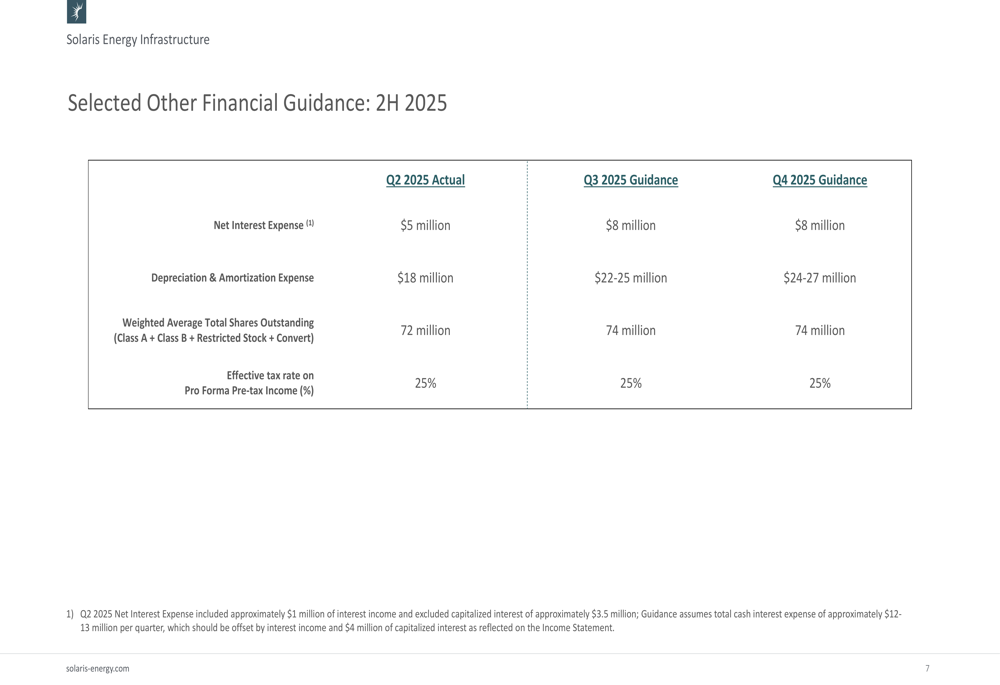

The company expects increased depreciation and amortization expenses in the coming quarters, reflecting the ongoing capital investments in fleet expansion. Net interest expense is projected to increase to $8 million per quarter, up from $5 million in Q2, as the company takes on additional debt to fund its growth initiatives.

Forward-Looking Statements

Solaris’s presentation paints an optimistic picture of substantial growth over the next two years, with a clear focus on data center power solutions. The company’s strategy appears well-aligned with market trends, particularly the increasing demand for reliable power generation for data centers amid the AI boom and cloud computing expansion.

While the growth plan is ambitious, the company’s track record of exceeding expectations—as demonstrated in its Q1 2025 results—provides some confidence in its ability to execute. However, investors should consider potential challenges including regulatory changes, market competition, and the significant capital requirements needed to achieve the projected growth.

As Solaris continues its transformation from an oilfield infrastructure company to a broader energy infrastructure provider, its success will likely depend on its ability to secure and maintain long-term contracts with data center operators and other key customers while managing its increasing debt load effectively.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.