Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Executive Summary

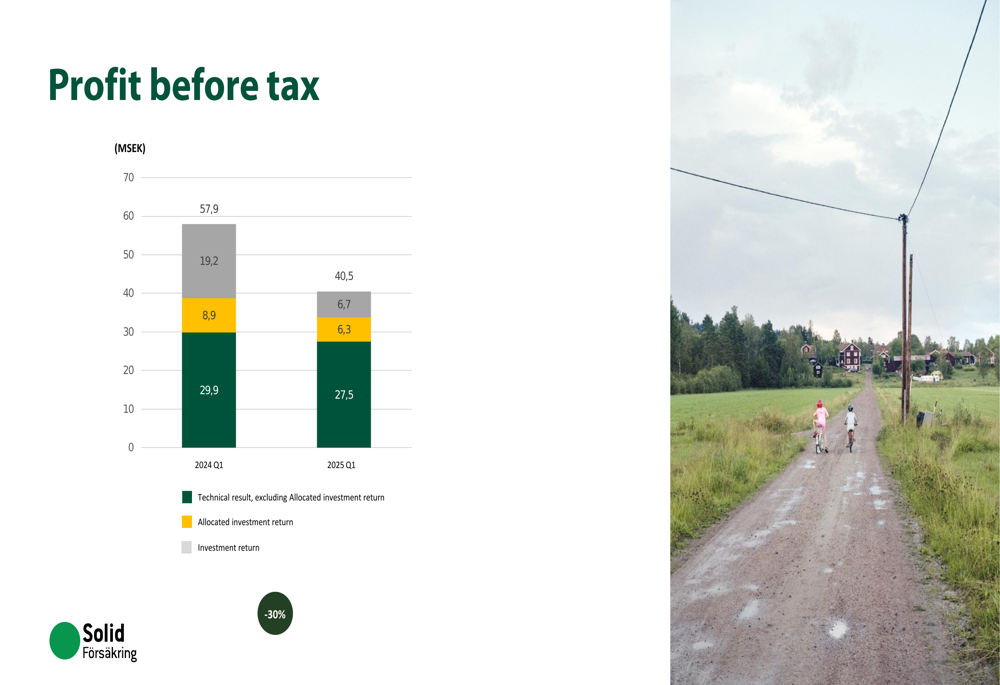

Solid Försäkring (SFAB) reported a significant decline in profitability for the first quarter of 2025, with profit before tax falling 30% year-over-year to 40.5 MSEK (57.9 MSEK). The Swedish insurer’s shares were down 1.62% following the presentation on April 24, 2025, trading at 86.3 SEK.

Despite the profit decline, the company highlighted several strategic initiatives during the quarter, including the acquisition of Garantipartner to strengthen its position in car warranties, and an extended partnership with Niemi Bil to expand into Finland.

As shown in the following quarterly highlights:

Quarterly Performance Highlights

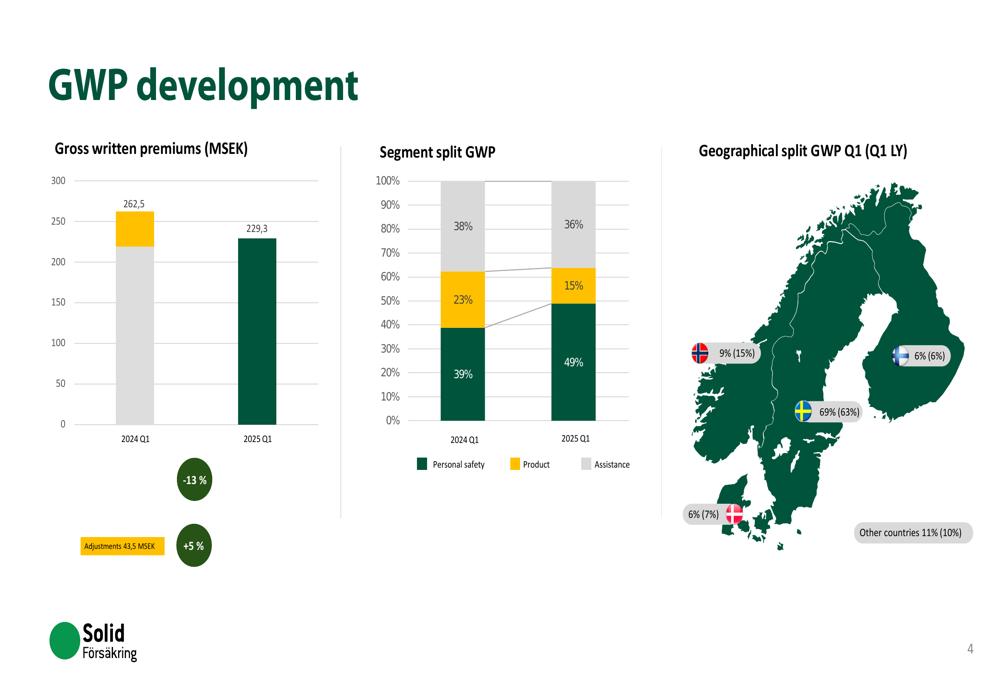

Gross written premiums (GWP) decreased by 13% compared to the previous year, though the company noted this represented a 5% increase when adjusted for certain factors. Net earned premiums (NEP) showed a more modest decline of 1% year-over-year.

The company’s technical result, excluding allocated investment return, decreased by 8% to 27.5 MSEK (29.9 MSEK), while profit from the investment portfolio fell significantly to 13.1 MSEK (28.0 MSEK).

The following chart illustrates the development of gross written premiums across segments and geographical regions:

Segment performance varied considerably, with Personal Safety showing growth while Product experienced significant declines. The geographical distribution of premiums shifted notably toward Sweden, which increased to 69% of GWP (from 63% in Q1 2024), while Norway’s share decreased to 9% (from 15%).

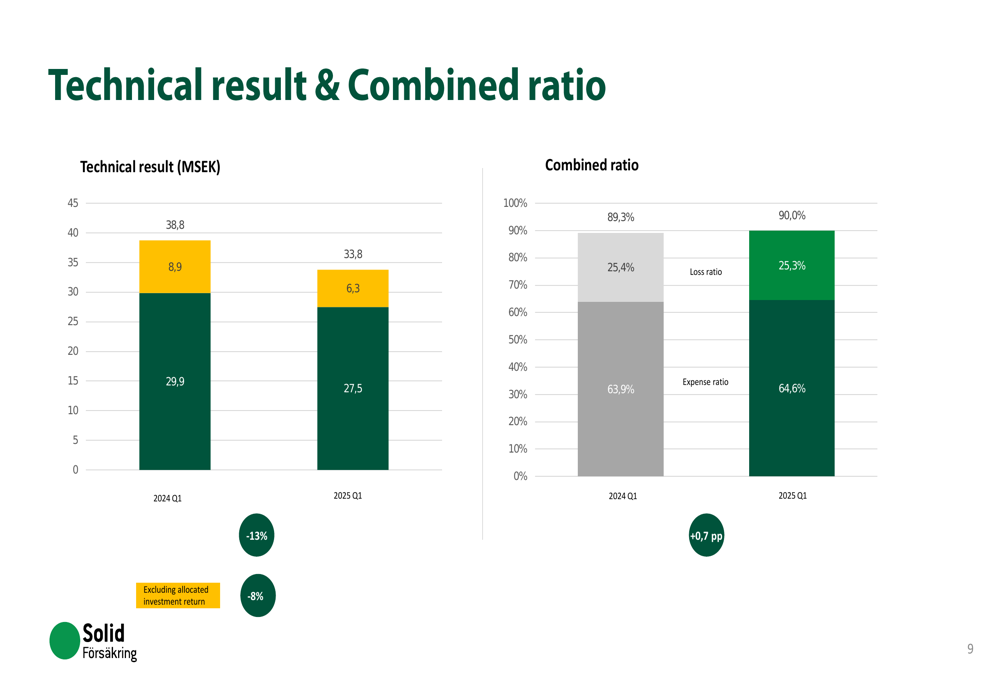

The combined ratio, a key measure of underwriting profitability, worsened slightly to 90.0% from 89.3% in the same period last year, primarily due to a higher expense ratio.

The technical result and combined ratio are illustrated in the following chart:

Segment Performance

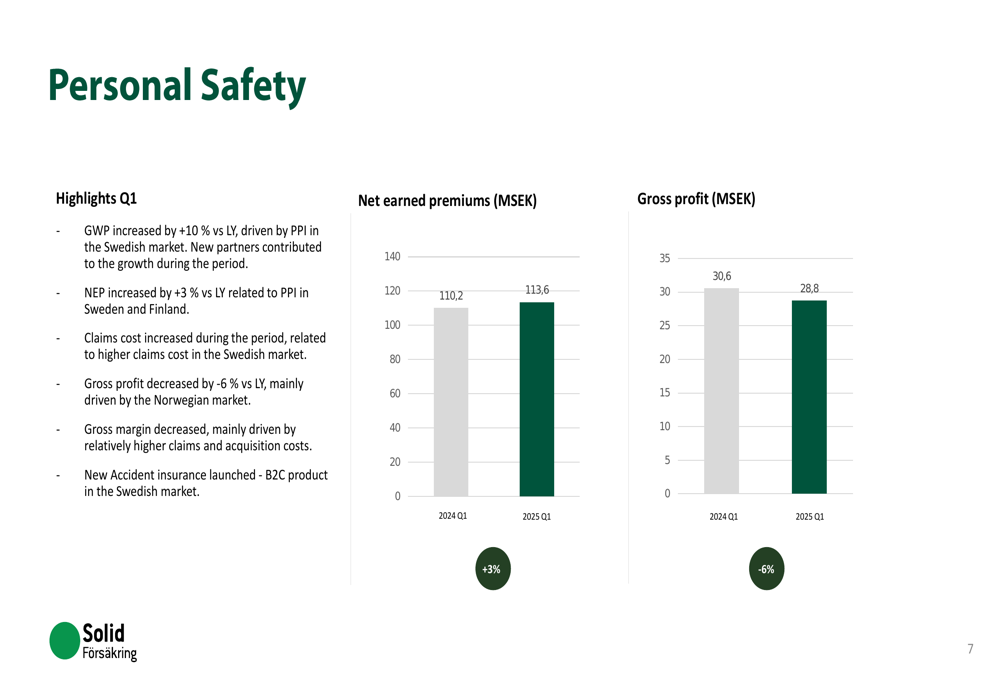

The Personal Safety segment showed positive premium growth but declining profitability. Gross written premiums increased by 10% year-over-year, driven by payment protection insurance (PPI) in the Swedish market and contributions from new partners. Net earned premiums grew by 3%, but gross profit decreased by 6%, primarily due to higher claims costs in the Swedish market and challenges in the Norwegian market.

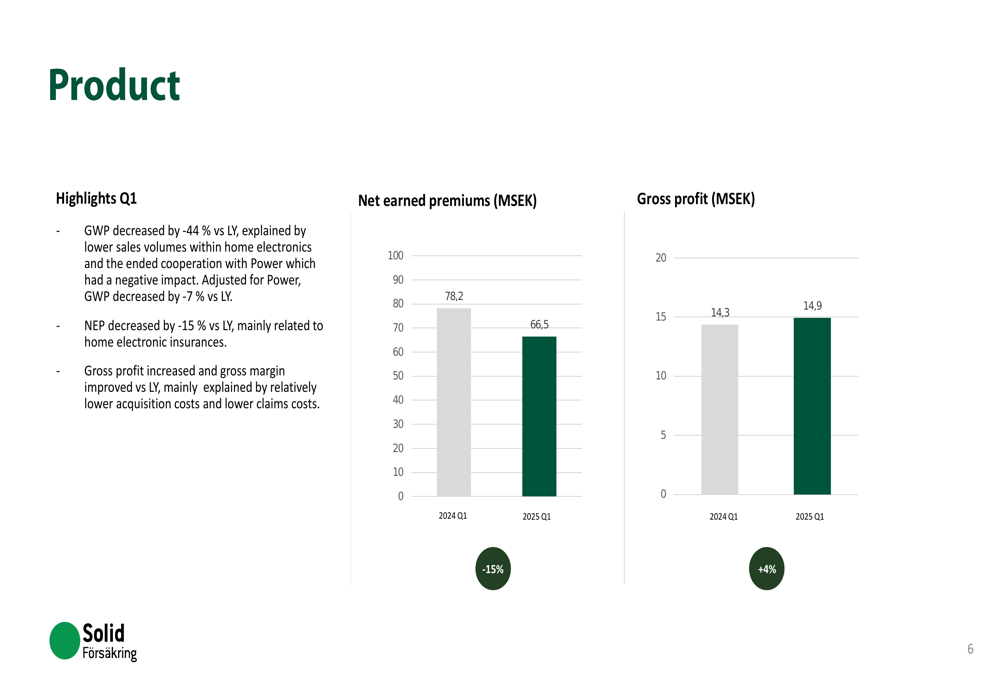

The Product segment experienced the most significant decline, with gross written premiums falling 44% year-over-year. The company attributed this primarily to lower sales volumes in home electronics and the ended cooperation with Power. Even when adjusted for the Power impact, GWP still decreased by 7%. Despite the revenue decline, gross profit increased by 4% due to lower acquisition and claims costs.

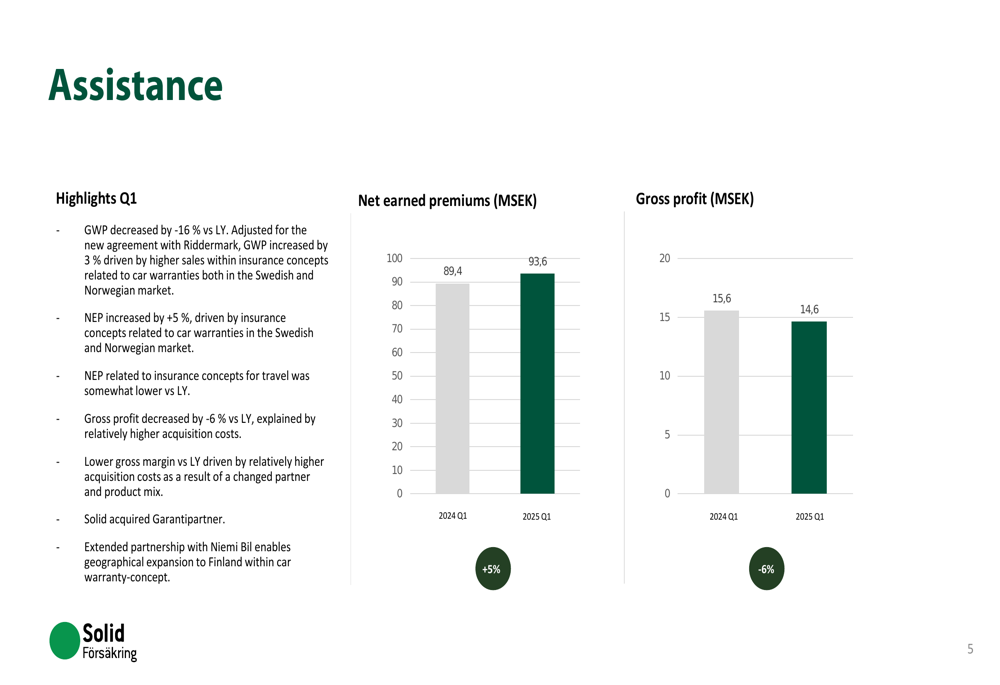

The Assistance segment, which focuses on car warranties and travel insurance, saw gross written premiums decrease by 16% year-over-year. However, when adjusted for the new agreement with Riddermark, GWP increased by 3%. Net earned premiums grew by 5%, driven by car warranty insurance concepts in both Sweden and Norway. Gross profit decreased by 6%, which the company attributed to higher acquisition costs resulting from changes in partner and product mix.

Investment Performance and Profitability

The company’s investment portfolio delivered weaker results compared to the previous year. The total return year-to-date was 1.1%, down from 2.0% in Q1 2024. Investment income remained stable at 19.4 MSEK, but investment charges increased to 2.6 MSEK (from 0.8 MSEK), and the company recorded unrealized losses of 3.7 MSEK compared to gains of 9.5 MSEK in the same period last year.

The following chart shows the breakdown of profit before tax:

Capital Position and Shareholder Returns

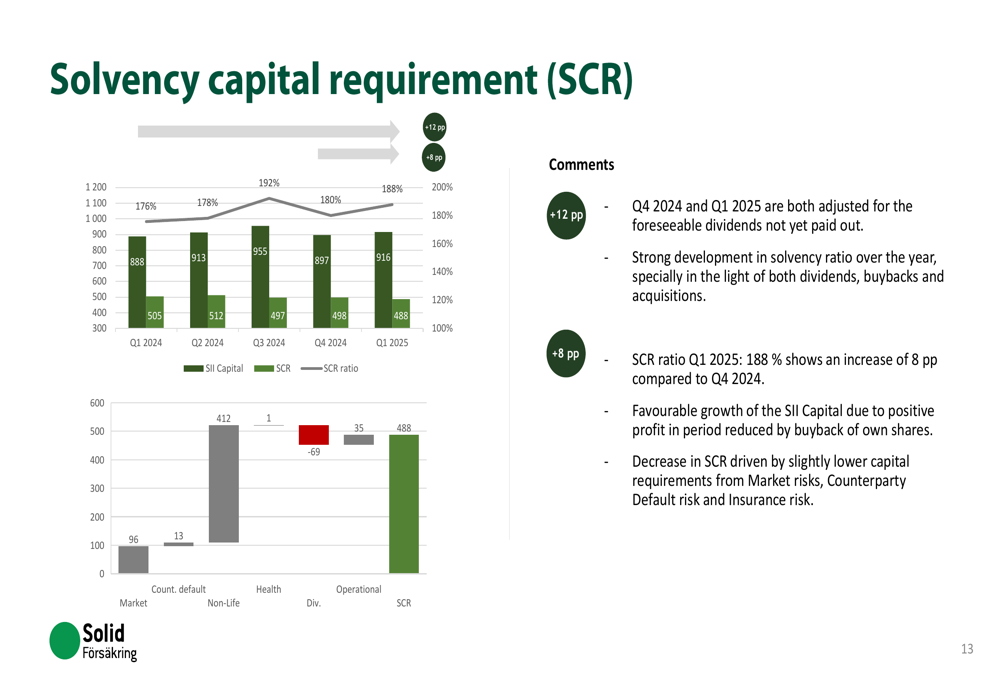

Despite the profit decline, Solid Försäkring maintained a strong capital position, with its Solvency Capital Requirement (SCR) ratio improving to 188%, an increase of 8 percentage points compared to Q4 2024. The company attributed this to positive profit in the period, partially offset by share buybacks.

The solvency position is illustrated in the following chart:

The Board proposed a dividend of 5.00 SEK per share and recommended that the Annual General Meeting authorize the Board to continue the share buyback program until the AGM in 2026. This indicates confidence in the company’s financial stability despite the challenging quarter.

Strategic Initiatives

Solid Försäkring highlighted several strategic moves during the quarter:

1. The acquisition of Garantipartner to strengthen its position in car warranties in the Swedish market

2. Extended partnership with Niemi Bil to enable geographical expansion to Finland within the car warranty segment

3. Extended cooperation with Riddermark Bil AB

4. Launch of a new accident insurance product in the B2C segment in the Swedish market

These initiatives align with the company’s strategy to expand its product offerings and geographical presence, particularly in the car warranty segment, which showed growth within the Assistance business area.

Outlook

While the company did not provide specific forward guidance, management emphasized the "stable development in the insurance business" with "underlying sales growth" despite the headline decline in premiums. The focus on strategic acquisitions and partnerships suggests a continued emphasis on expanding the car warranty business and geographical diversification.

The strong capital position, with an SCR ratio of 188%, provides the company with flexibility to pursue further growth opportunities while maintaining shareholder returns through dividends and share buybacks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.