How are energy investors positioned?

Introduction & Market Context

Solventum Corp (NYSE:SOLV) presented its Q1 FY25 earnings results on May 8, 2025, highlighting improved organic sales growth and raising its full-year organic sales outlook despite anticipated tariff headwinds. The healthcare solutions company, in its second year since spinning off from 3M, reported results that suggest a recovery from its disappointing Q4 2024 performance when it missed earnings expectations.

The stock closed at $65.49 on the day of the presentation and gained 1.31% in after-hours trading to $67.50, indicating a positive market reaction to the quarterly results and improved outlook.

Quarterly Performance Highlights

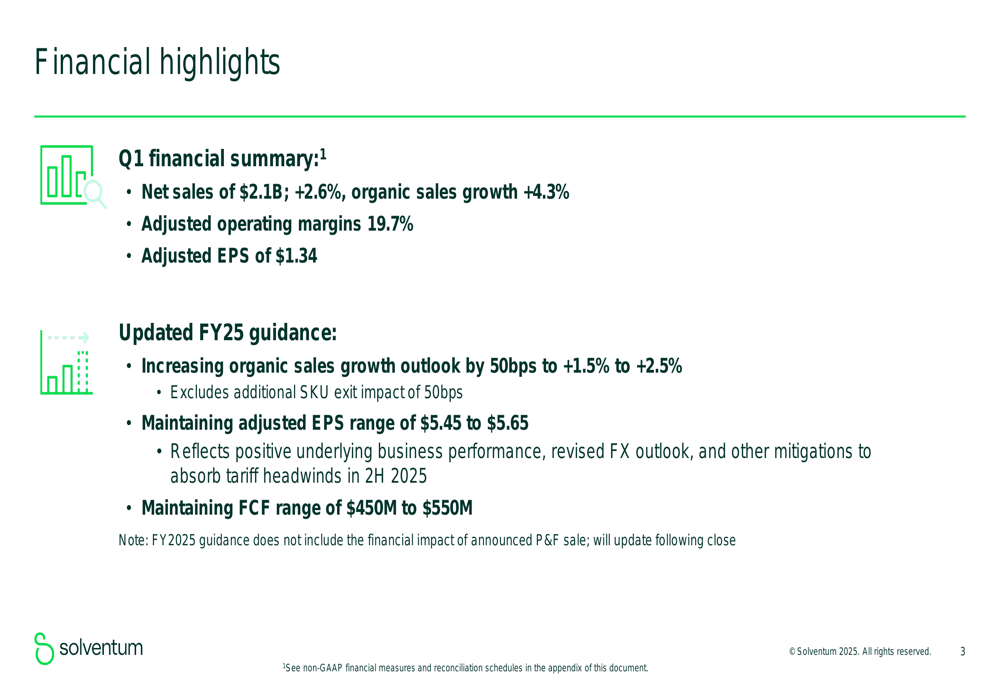

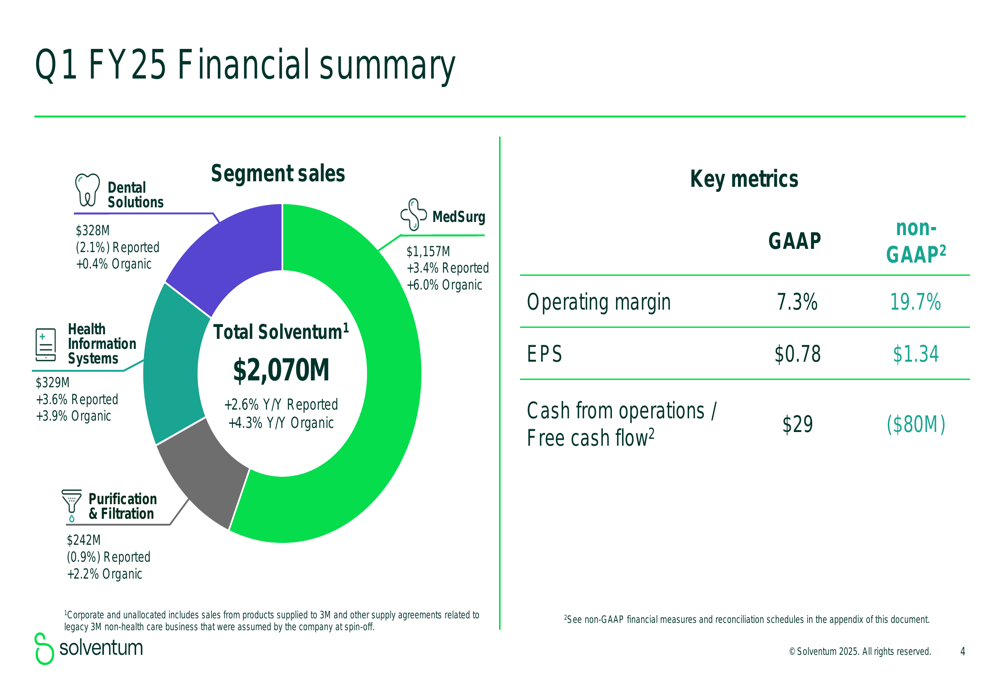

Solventum reported Q1 FY25 net sales of $2.1 billion, representing a 2.6% year-over-year increase on a reported basis and a stronger 4.3% organic growth. The company achieved adjusted operating margins of 19.7% and adjusted earnings per share of $1.34.

As shown in the following financial highlights slide, the company has increased its organic sales growth outlook for FY25 by 50 basis points while maintaining its previous guidance for adjusted EPS and free cash flow:

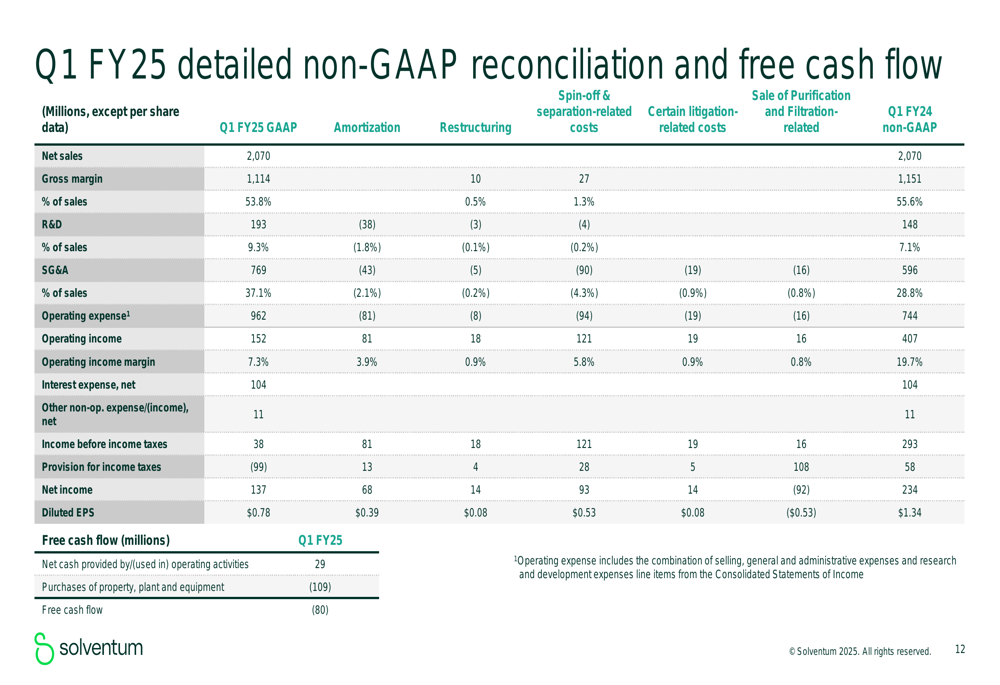

On a GAAP basis, the company reported an operating margin of 7.3% and EPS of $0.78, significantly lower than the adjusted figures due to various one-time costs including restructuring, spin-off and separation-related expenses, and costs related to the planned sale of its Purification & Filtration business.

The detailed segment breakdown reveals that MedSurg, the company’s largest segment, was the primary growth driver:

Segment Performance Analysis

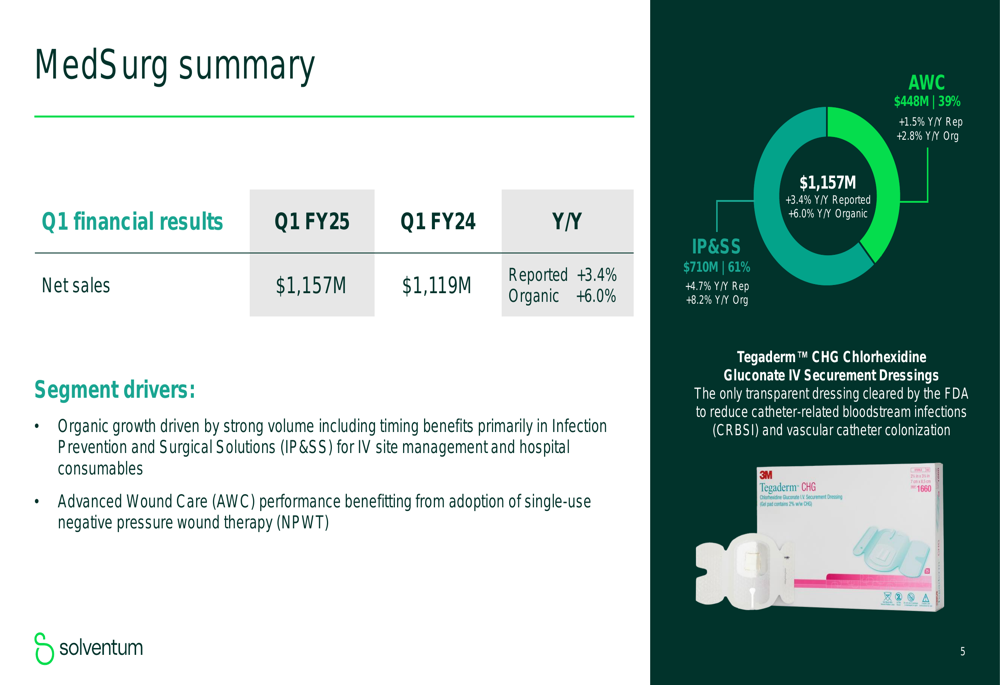

MedSurg, representing approximately 56% of Solventum’s total sales, delivered the strongest performance with 6.0% organic growth. This segment generated $1.157 billion in sales, a 3.4% increase on a reported basis.

The robust MedSurg performance was driven by strong volume, particularly in Infection Prevention and Surgical Solutions, which grew 8.2% organically. Management highlighted timing benefits in IV site management and hospital consumables, along with adoption of single-use negative pressure wound therapy in the Advanced Wound Care division.

Health Information Systems showed steady growth with sales of $329 million, representing 3.9% organic growth. The company attributed this performance to continued adoption of its 360 Encompass™ Revenue Cycle Management solutions.

Dental Solutions faced challenges but managed slight organic growth of 0.4% despite a 2.1% reported sales decline to $328 million. The segment experienced market-driven headwinds in Core Orthodontics, partially offset by performance in Restoratives, which benefited from recent product launches including Filtek™ Easy Match and ClinPro™ Clear.

The Purification & Filtration segment, which Solventum has announced plans to sell, reported $242 million in sales with 2.2% organic growth despite a 0.9% reported decline. The company noted continued strength in Bioprocessing Filtration and Industrial Filtration, partially offset by declines in Membrane OEM.

Forward Guidance & Strategic Outlook

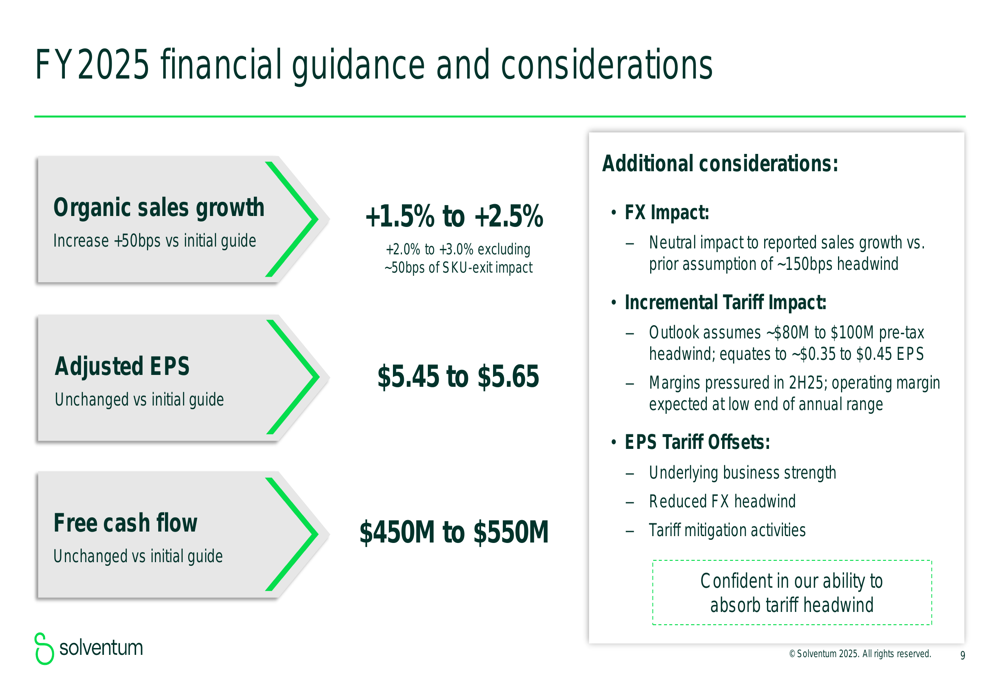

In a sign of confidence, Solventum raised its FY25 organic sales growth outlook to 1.5%-2.5%, up 50 basis points from its initial guidance. This improved outlook excludes an additional 50 basis point impact from planned SKU exits.

Despite facing significant tariff headwinds estimated at $80-$100 million (approximately $0.35-$0.45 per share) in the second half of 2025, the company maintained its full-year adjusted EPS guidance of $5.45-$5.65 and free cash flow projection of $450-$550 million.

The following slide details the company’s updated guidance and outlines how it plans to offset the tariff impact:

Management indicated that the improved outlook reflects positive underlying business performance, a revised foreign exchange outlook, and various tariff mitigation activities. The company noted that its guidance does not yet include the financial impact of the announced Purification & Filtration business sale, which will be updated following the close of that transaction.

Financial Position & Challenges

While Solventum demonstrated confidence in its full-year outlook, the company did report negative free cash flow of $80 million for Q1 FY25. This was calculated from $29 million in net cash provided by operating activities less $109 million in capital expenditures.

The detailed reconciliation between GAAP and non-GAAP figures reveals significant adjustments, particularly related to restructuring, spin-off costs, and the planned divestiture:

Looking ahead, Solventum faces several challenges, including the significant tariff headwinds expected in the second half of 2025, which management expects will pressure margins. The company anticipates operating margins to be at the low end of its annual range due to these pressures.

Additionally, the Dental Solutions segment continues to face market-driven headwinds, particularly in Core Orthodontics, though new product launches are helping to offset some of this pressure.

Despite these challenges, Solventum’s raised organic sales growth outlook and maintained EPS guidance suggest management confidence in the company’s ability to navigate the complex healthcare market environment while continuing its post-spin transformation journey.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.