Fed Governor Cook sues Trump over firing attempt

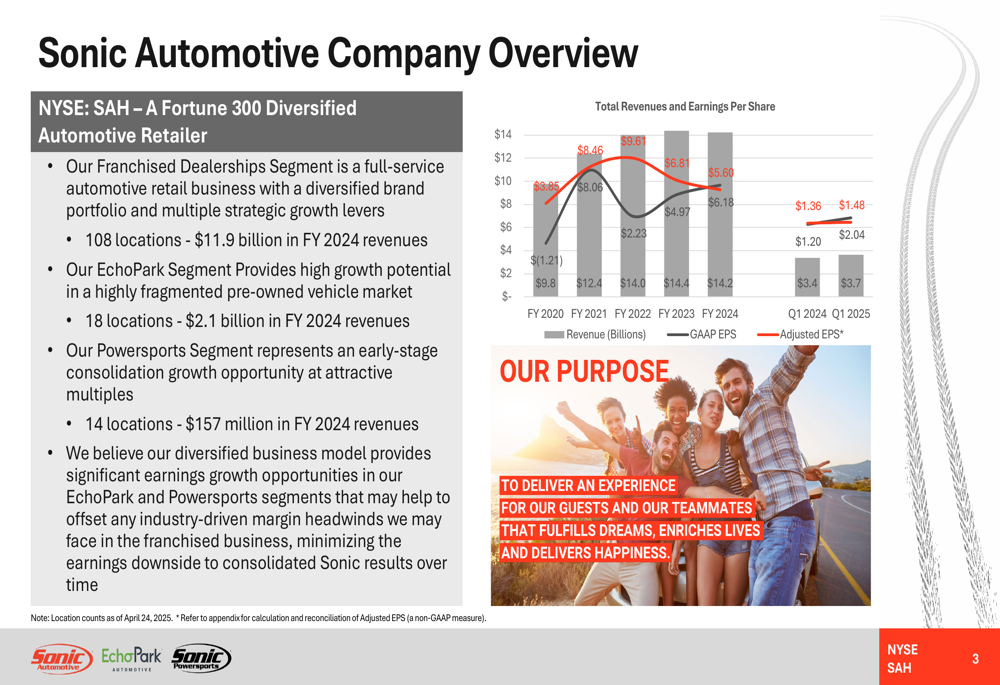

Sonic Automotive Inc (NYSE:SAH), a Fortune 300 diversified automotive retailer, presented its first quarter 2025 results on April 24, highlighting significant earnings growth and record performance in its EchoPark segment amid an evolving automotive retail landscape.

Quarterly Performance Highlights

Sonic Automotive reported strong financial results for Q1 2025, with total revenues reaching $3.7 billion, up from $3.4 billion in Q1 2024, representing a 9% year-over-year increase. The company’s GAAP earnings per share surged to $1.48, more than quadrupling from $0.34 in the same period last year, while adjusted EPS climbed to $9.61 from $6.81, marking a 41% increase.

As shown in the company overview chart, Sonic has maintained a steady revenue trajectory while significantly improving its earnings performance:

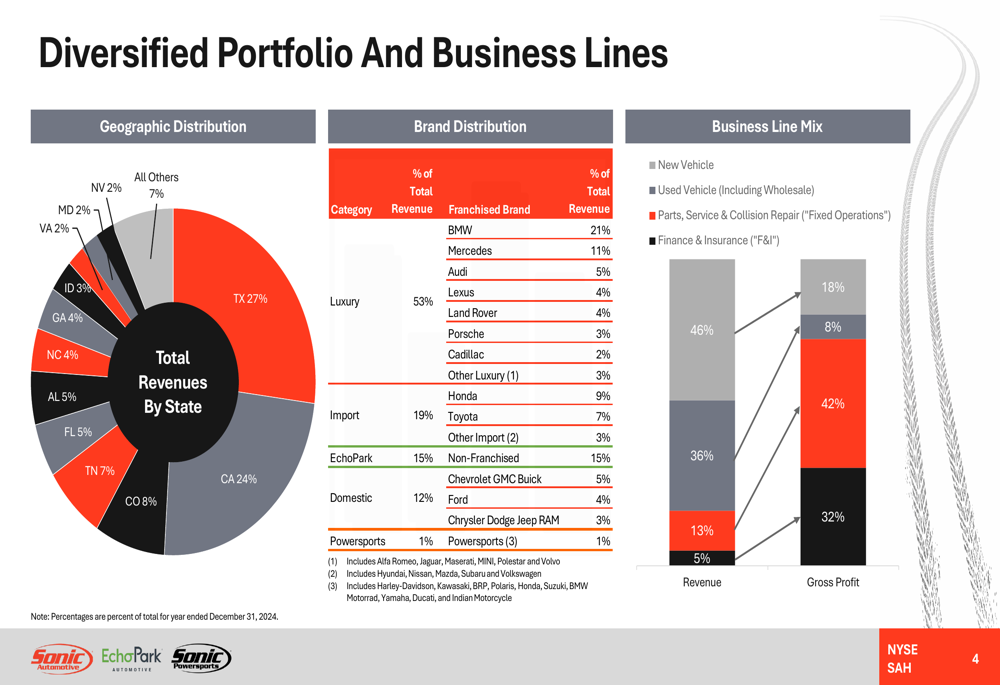

The company’s diversified business model spans three segments: Franchised Dealerships ($11.9 billion in FY 2024 revenues), EchoPark ($2.1 billion), and Powersports ($157 million). This diversification extends to geographic markets and brand portfolio, providing resilience against regional and brand-specific challenges.

The following chart illustrates Sonic’s geographic and brand distribution, showing strong presence in Texas (27%) and California (24%), with luxury brands comprising 53% of total revenue:

Segment Performance Analysis

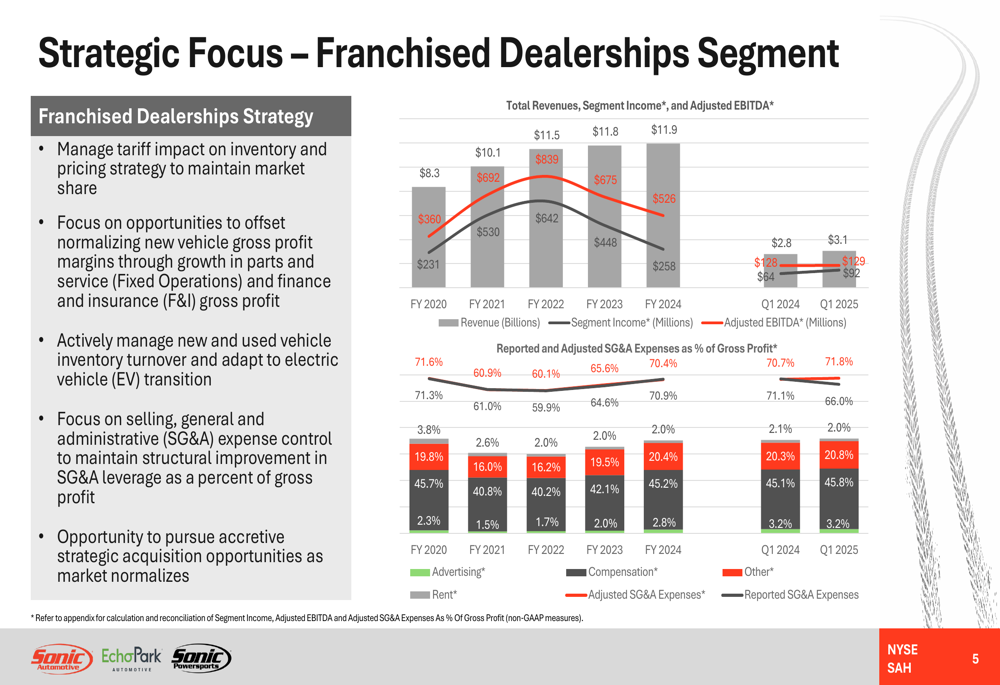

Franchised Dealerships

The Franchised Dealerships segment, which forms the core of Sonic’s business, posted Q1 2025 revenues of $3.1 billion, up from $2.8 billion in Q1 2024. Segment income increased to $92 million from $64 million in the prior-year period, while adjusted EBITDA remained stable at $128 million.

The company’s strategic focus for this segment includes managing tariff impacts, offsetting normalizing new vehicle gross profit margins through growth in fixed operations and F&I, and controlling SG&A expenses. The following chart details the segment’s financial performance:

Sonic reported that new vehicle gross profit per unit (GPU) was $3,089 in Q1 2024, with expectations for FY 2025 to maintain GPU in the $2,500-$3,000 range, depending on tariff impacts and brand mix shifts. The company also highlighted its success in growing fixed operations, with gross profit increasing to $237 million in Q1 2025 from $221 million in Q1 2024, maintaining a strong gross margin of 50.7%.

The company has made significant investments in its service capacity, increasing technician headcount by 335 in FY 2024, which is projected to generate approximately $100 million in annualized fixed operations gross profit once fully productive.

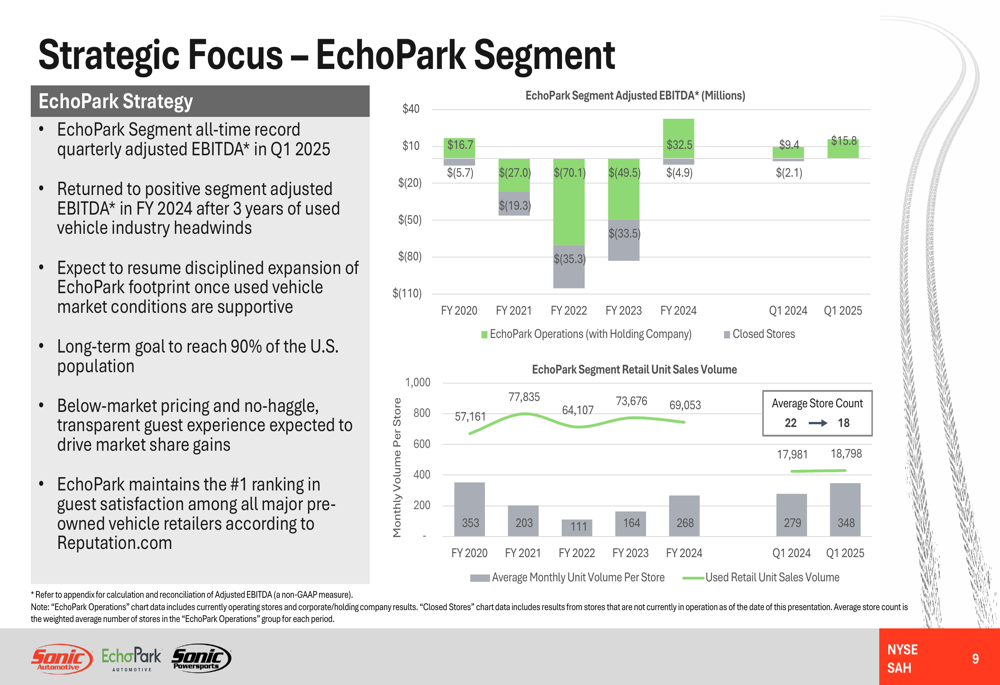

EchoPark Segment

A standout performer in Q1 2025 was the EchoPark segment, which achieved an all-time record quarterly adjusted EBITDA of $15.8 million, up from $9.4 million in Q1 2024. This represents a significant turnaround from previous years of losses, with retail unit sales volume increasing to 18,798 units in Q1 2025 from 17,981 in Q1 2024.

The following chart shows EchoPark’s improving performance trajectory:

Management attributes EchoPark’s success to faster inventory turns, stability in the spread between wholesale and retail prices, and a focus on sourcing more inventory from non-auction sources. The segment’s GPU (used GPU + F&I GPU) reached $348 per unit in Q1 2025, up from $279 in Q1 2024.

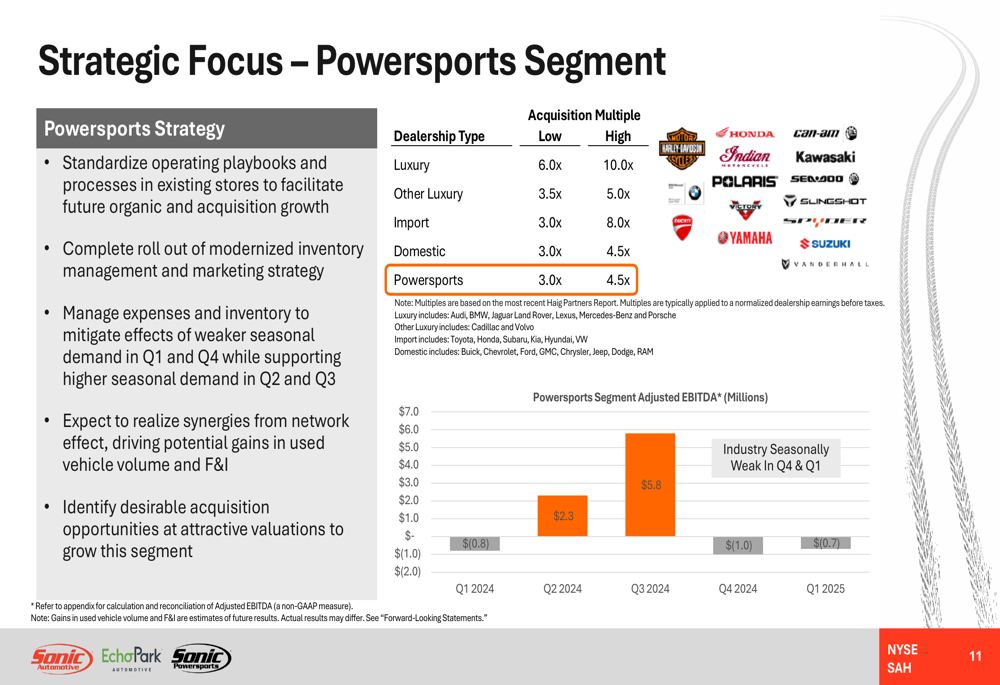

Powersports Segment

The Powersports segment, Sonic’s newest business line, reported an adjusted EBITDA of -$0.7 million in Q1 2025, a slight improvement from -$0.8 million in Q1 2024. The company notes that this segment experiences significant seasonality, with Q1 and Q4 typically showing negative results while Q2 and Q3 perform strongly.

As illustrated in the following slide, Sonic views Powersports as an attractive acquisition opportunity with multiples significantly lower than luxury automotive dealerships:

Strategic Initiatives

Sonic Automotive is pursuing several strategic initiatives across its business segments. For the Franchised Dealerships segment, the company is focusing on adapting to the electric vehicle transition while maintaining strong performance in hybrid vehicles, which are showing better consumer demand and higher GPU than BEVs.

In the EchoPark segment, Sonic plans to resume disciplined expansion once used vehicle market conditions are supportive, with a long-term goal to reach 90% of the U.S. population. The company maintains that EchoPark’s below-market pricing and no-haggle, transparent guest experience will drive market share gains.

For the Powersports segment, Sonic is standardizing operating playbooks and processes in existing stores to facilitate future organic and acquisition growth, while identifying desirable acquisition opportunities at attractive valuations.

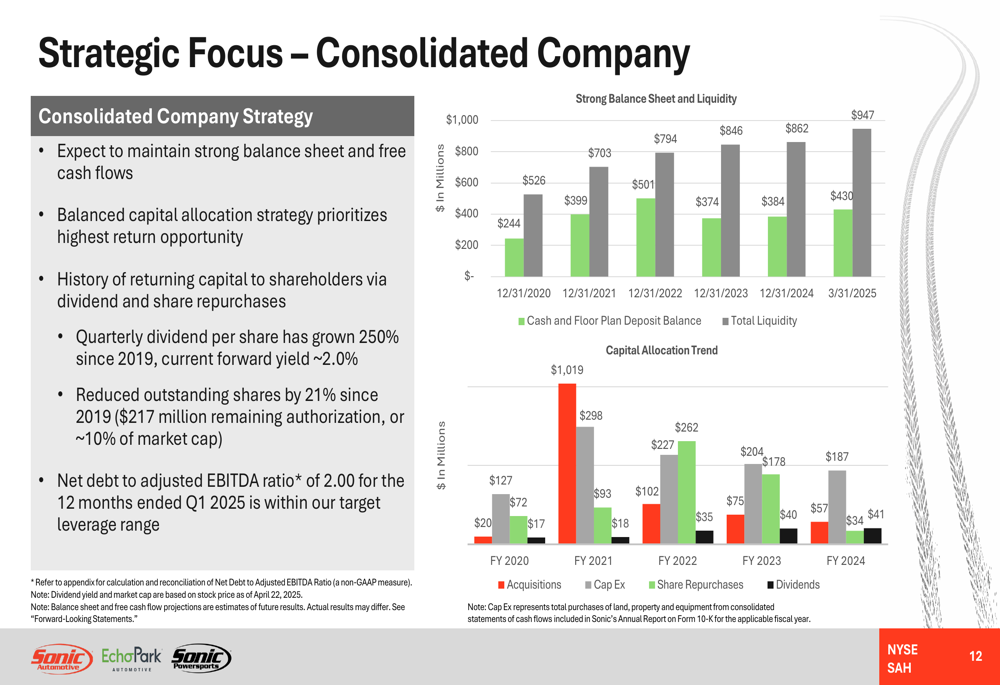

The company’s consolidated strategy emphasizes maintaining a strong balance sheet and free cash flows, with a balanced capital allocation approach. As shown in the following chart, Sonic has maintained strong liquidity while returning capital to shareholders through dividends and share repurchases:

Forward-Looking Statements

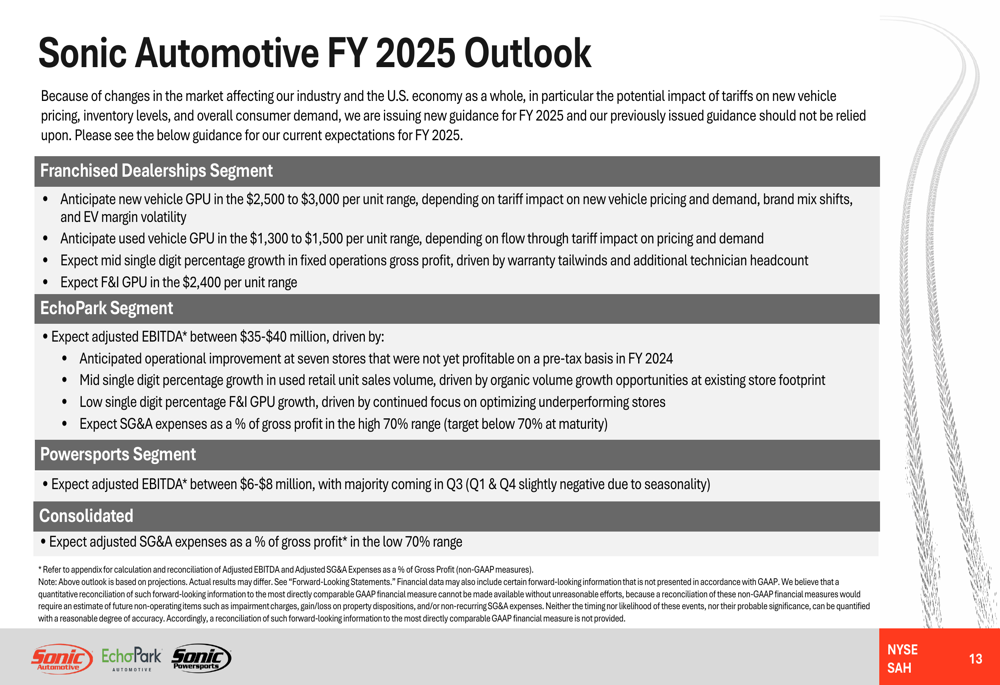

Looking ahead to FY 2025, Sonic Automotive provided specific guidance for each segment. For Franchised Dealerships, the company anticipates new vehicle GPU in the $2,500-$3,000 range and used vehicle GPU in the $1,300-$1,500 range, with mid-single-digit percentage growth in fixed operations gross profit.

For the EchoPark segment, Sonic expects adjusted EBITDA between $35-$40 million, driven by operational improvements at underperforming stores and mid-single-digit percentage growth in used retail unit sales volume.

The Powersports segment is projected to generate adjusted EBITDA between $6-$8 million for FY 2025, with the majority coming in Q3 due to seasonality.

On a consolidated basis, Sonic expects adjusted SG&A expenses as a percentage of gross profit to be in the low 70% range, reflecting the company’s continued focus on operational efficiency.

The company’s Q1 2025 results represent a significant improvement from the challenges noted in its Q3 2024 earnings call, where adjusted EPS had declined by 38% year-over-year and operational disruptions from a CDK outage negatively impacted earnings. The strong Q1 2025 performance suggests that Sonic has successfully navigated these challenges while positioning itself for continued growth across its diversified business model.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.