Nucor earnings beat by $0.08, revenue fell short of estimates

Introduction & Market Context

Sonos Inc . (NASDAQ:SONO) presented its second quarter fiscal year 2025 financial results on May 7, 2025, showing modest revenue growth and significant improvements in operational efficiency. The premium audio equipment manufacturer reported revenue of $260 million, representing a 3% year-over-year increase, while beating earnings expectations with an EPS of -$0.18 compared to forecasts of -$0.36. Following the earnings announcement, Sonos shares rose 1.67% in aftermarket trading, closing at $9.12.

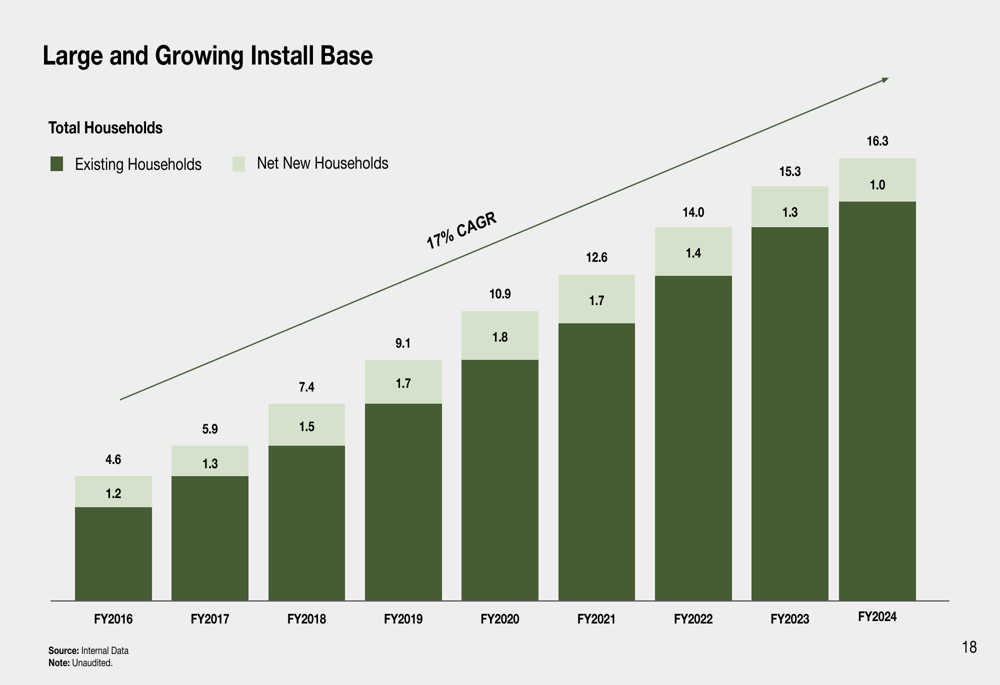

The company continues to position itself as a premium brand in the audio market, competing against tech giants like Google (NASDAQ:GOOGL) and Amazon (NASDAQ:AMZN) while maintaining leadership in specific high-end segments. With a current household install base of 16.3 million and a product portfolio spanning multiple categories, Sonos is executing a strategy focused on operational efficiency while continuing to innovate across its product lines.

Quarterly Performance Highlights

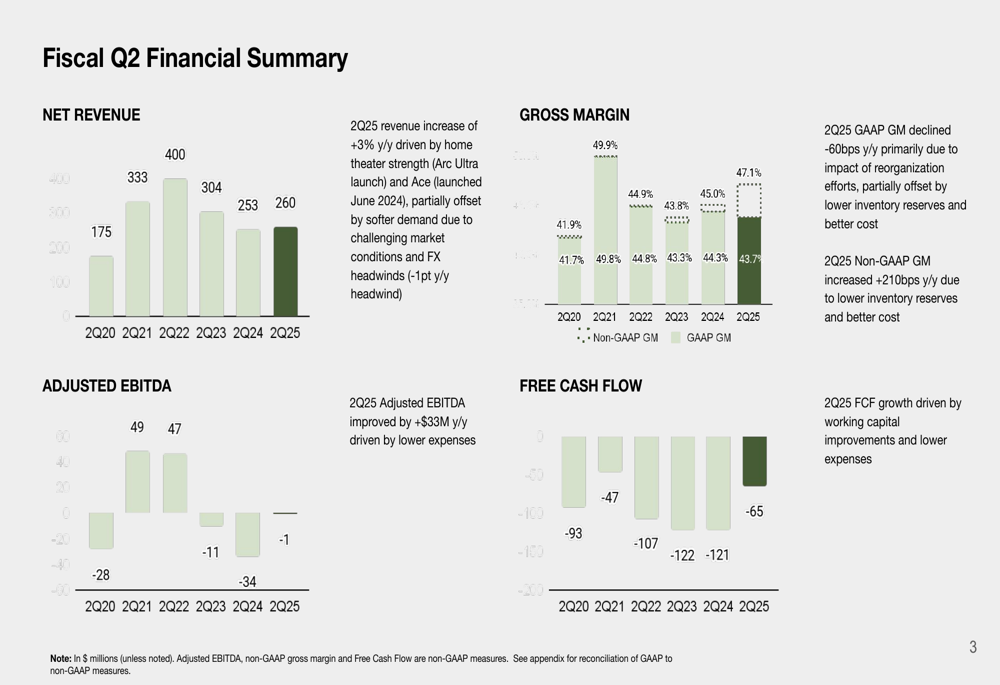

Sonos reported Q2 FY2025 revenue of $260 million, a 3% increase year-over-year, slightly exceeding analyst expectations of $253.52 million. The company’s GAAP gross margin stood at 43.7%, while non-GAAP gross margin reached 47.1%.

As shown in the following financial summary chart, the company has made significant progress in improving its adjusted EBITDA, which reached -$1 million in Q2 FY2025, a substantial improvement from previous quarters:

Free cash flow also showed marked improvement at -$65.2 million compared to -$121.4 million in the same quarter last year. This 46% year-over-year improvement reflects the company’s enhanced working capital management and reduced capital expenditures.

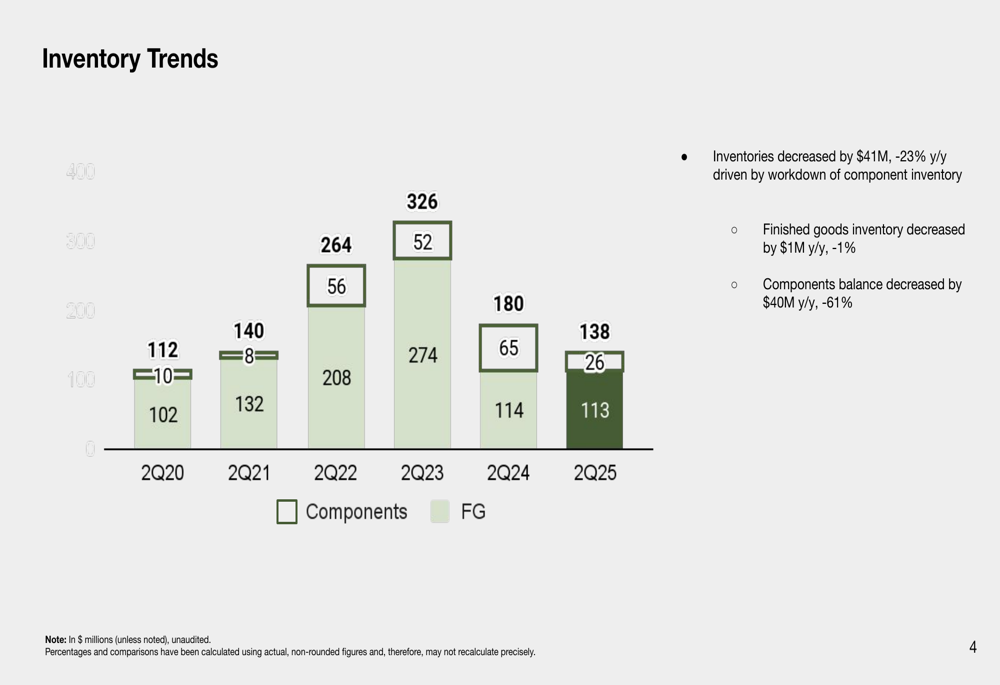

The company has made substantial progress in inventory management, with total inventory decreasing by $41 million or 23% year-over-year. This reduction was primarily driven by a 61% decrease in components inventory, while finished goods inventory remained relatively stable with just a 1% decrease.

Detailed Financial Analysis

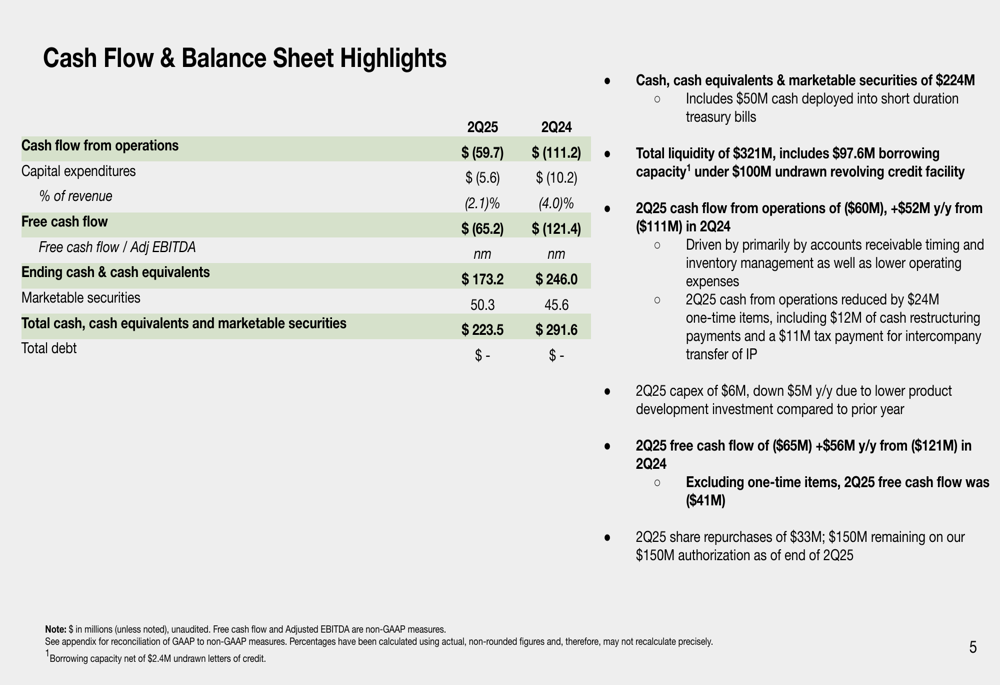

Sonos has implemented significant cost-cutting measures, resulting in a 14% year-over-year reduction in non-GAAP operating expenses, which totaled $135 million for the quarter. The company’s cash flow from operations improved to -$59.7 million, compared to -$111.2 million in Q2 FY2024.

The following slide details the company’s cash flow and balance sheet highlights, showing a total liquidity position of $321 million, including $224 million in cash, cash equivalents, and marketable securities:

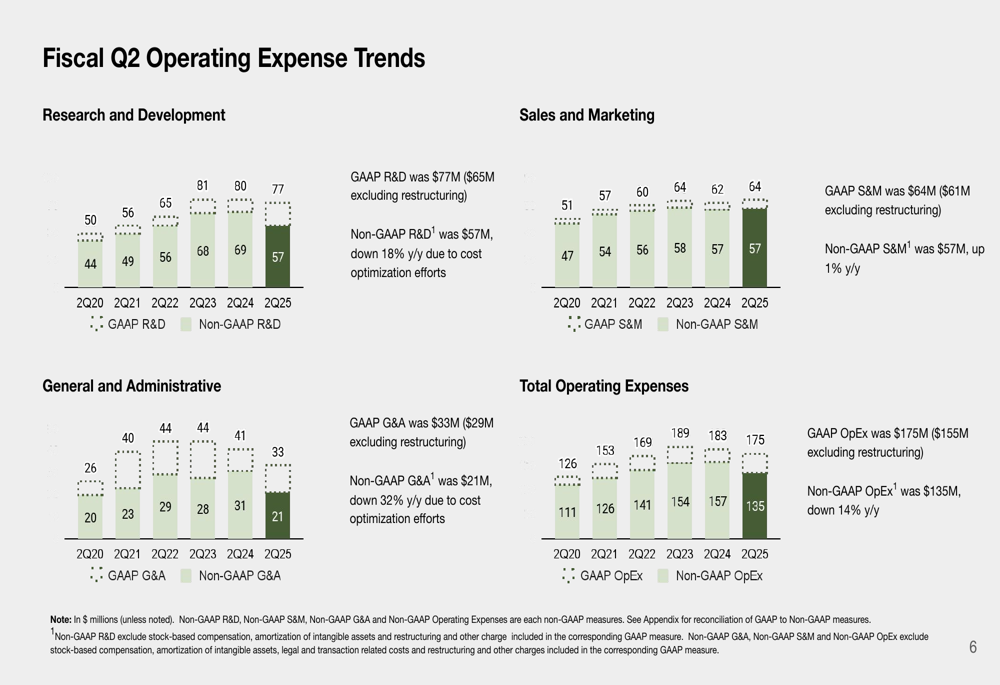

The company’s operating expense trends reveal targeted reductions across all major categories. Research and Development (R&D) expenses decreased by 18% year-over-year on a non-GAAP basis, while General and Administrative (G&A) expenses saw the most significant reduction at 32% year-over-year. Sales and Marketing (S&M) expenses remained relatively flat with a 1% increase.

Sonos continues to maintain a strong balance sheet with no debt, though its cash position has decreased from $291.6 million in Q2 FY2024 to $223.5 million in Q2 FY2025. The company repurchased $33 million worth of shares during the quarter, with $150 million remaining on its authorization at the end of Q2.

Competitive Industry Position

Sonos maintains its position as a premium brand in the audio market, differentiating itself from both legacy home audio companies and commodity brands like Google and Amazon. The company holds the #1 brand rank in the $200+ Home Theater category in both the United States and EMEA (UK and Germany), and the #2 position in the $150+ Streaming Audio category in these markets.

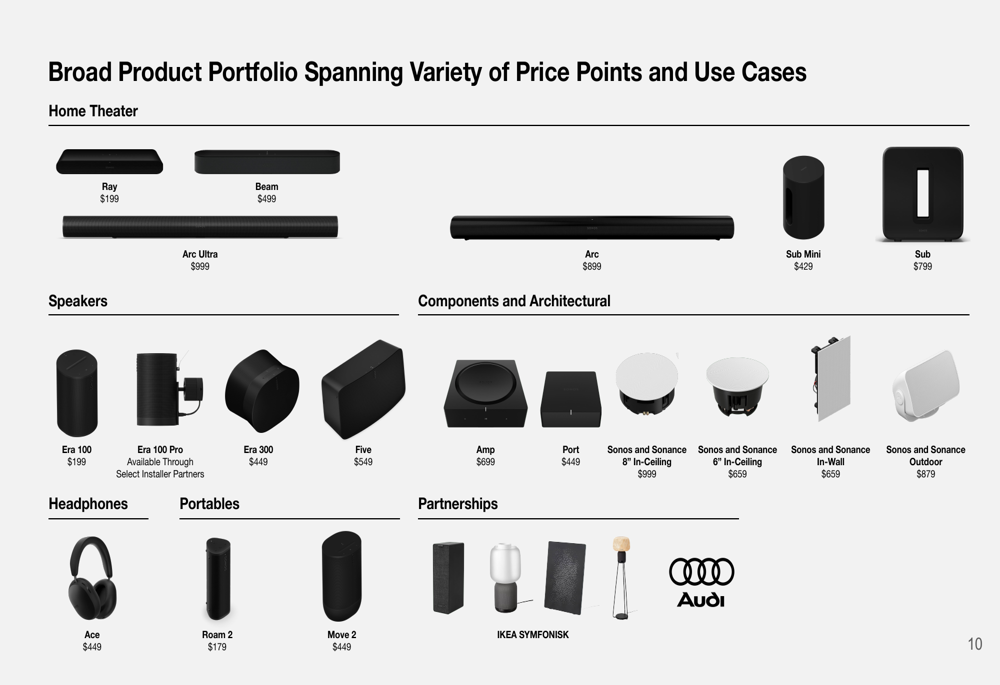

The company’s product portfolio spans multiple categories and price points, from the $199 Ray soundbar to the $999 Arc Ultra, and includes speakers, headphones, portables, and architectural components:

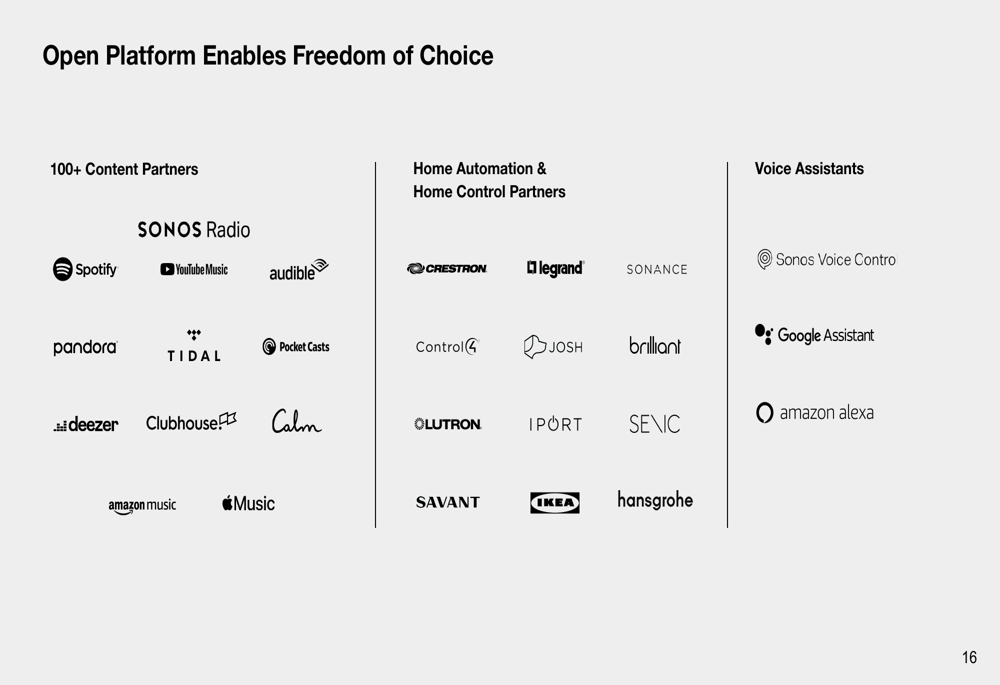

With over 4,300 US patents and applications, Sonos has built a substantial intellectual property portfolio that supports its innovation strategy. The company’s open platform approach includes integrations with over 100 content partners, various home automation systems, and multiple voice assistants.

Strategic Initiatives

Sonos continues to focus on expanding its household install base, which has grown at a 17% CAGR since 2016 to reach 16.3 million households in FY2024. The company’s strategy leverages the "Sonos Flywheel" concept, where new customer acquisition drives the ecosystem, leading to additional purchases from existing customers.

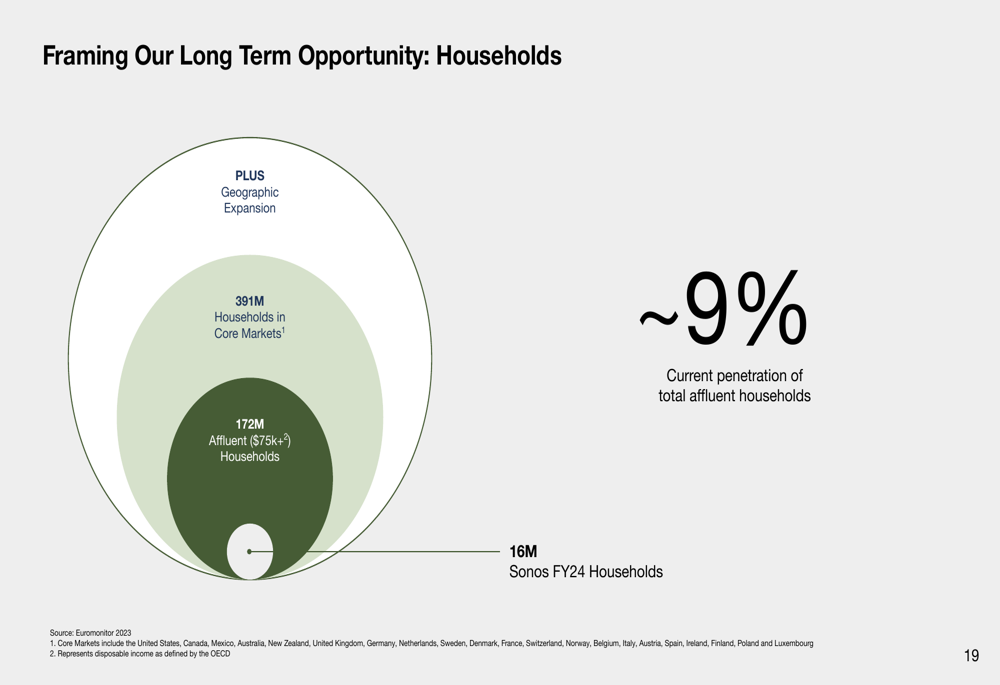

The company sees significant growth potential, with current penetration at only 9% of the 172 million affluent households ($75k+ income) in its core markets. The total addressable market for premium global audio and over-the-ear headphones is estimated at $27 billion, compared to Sonos’s FY2024 revenue of $1.52 billion.

Sonos has been evolving its channel distribution strategy over time, with direct-to-consumer (DTC) sales accounting for 27% of revenue in FY2024, down from a peak of 32% in FY2021. Meanwhile, installer solutions have grown to represent 13% of revenue, up from 8% in FY2018.

Forward-Looking Statements

During the earnings call, Sonos provided guidance for Q3 FY2025, projecting revenue between $310 million and $340 million, representing a sequential growth of 19-31%. The company expects modest year-over-year revenue growth in Q4 FY2025.

Interim CEO Tom Conrad emphasized the company’s focus on efficiency and innovation, stating, "We’re executing with more focus and efficiency," while highlighting ongoing efforts to improve the company’s market position. The company is currently conducting a comprehensive CEO search while continuing to implement its restructuring plan, which included $23.7 million in restructuring charges during Q2.

Sonos faces several challenges, including supply chain disruptions, competitive pressures in the portable speaker market, potential tariff impacts, and macroeconomic factors affecting consumer spending. However, the company’s strong market position in premium segments, growing install base, and operational efficiency improvements position it to navigate these challenges while pursuing long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.