S&P 500 cuts losses as Nvidia climbs ahead of results

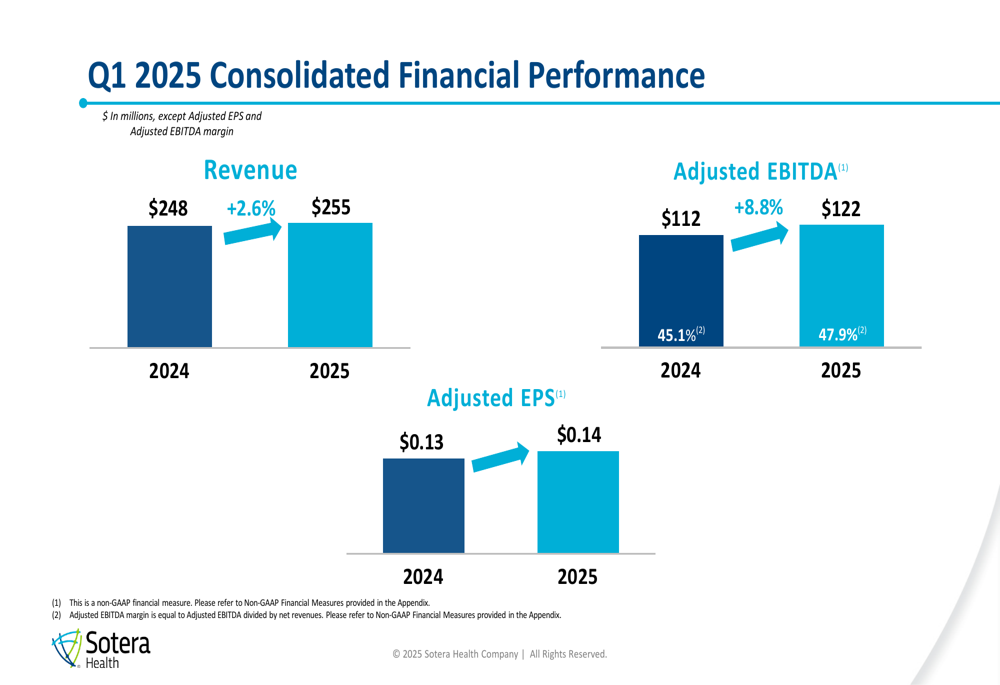

Sotera Health Company (NASDAQ:SHC) released its first-quarter 2025 earnings presentation on May 1, 2025, showing a return to growth after a challenging fourth quarter. The company reported revenue of $255 million, up 2.6% year-over-year, with adjusted EBITDA rising 8.8% to $122 million. The stock responded positively, trading up 4.35% in pre-market activity.

Quarterly Performance Highlights

Sotera Health’s Q1 2025 results demonstrate a significant turnaround from Q4 2024, which had seen a 6.5% revenue decline. The company achieved 4.4% constant currency revenue growth and expanded its adjusted EBITDA margin by 276 basis points to 47.9%. Adjusted earnings per share increased by $0.01 to $0.14.

As shown in the following consolidated financial performance chart, both revenue and adjusted EBITDA showed meaningful improvement compared to the same period last year:

Michael B. Petras, Jr., Chairman and CEO, highlighted that these results continue the company’s remarkable track record of consistent revenue growth every year since 2005, including through both the 2008 recession and COVID-19 pandemic.

Segment Analysis

Performance varied significantly across Sotera Health’s three business segments, with Nordion showing exceptional growth while Nelson Labs experienced revenue challenges despite margin improvements.

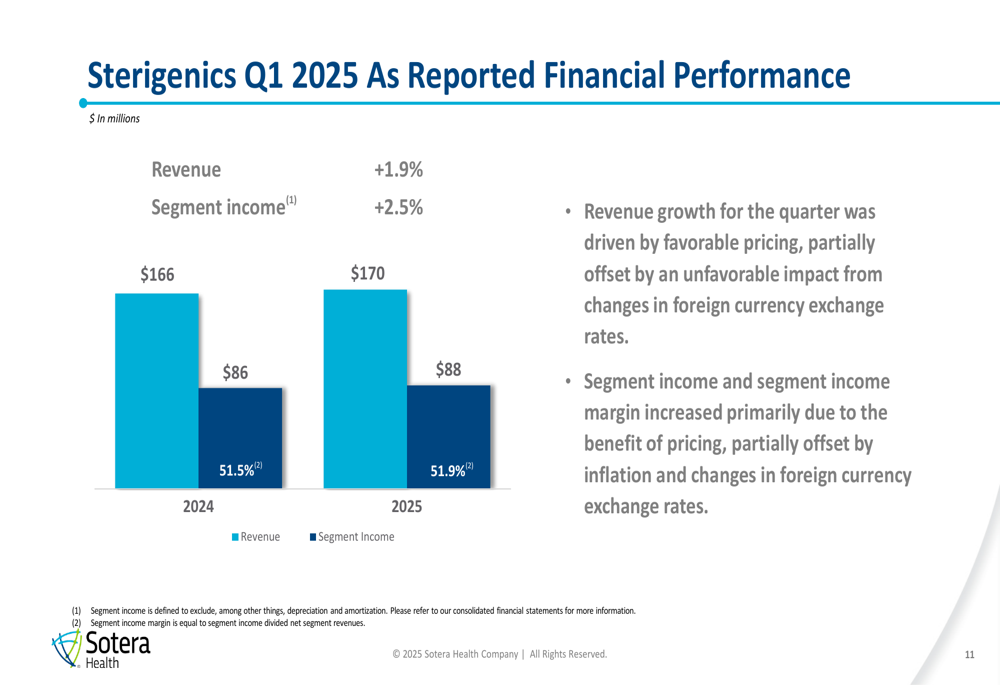

Sterigenics, the company’s largest segment providing sterilization solutions, delivered modest growth with revenue increasing 1.9% to $170 million. Segment income rose 2.5% to $88 million, with margin expansion to 51.9%. Management noted that favorable pricing drove growth, partially offset by foreign currency headwinds.

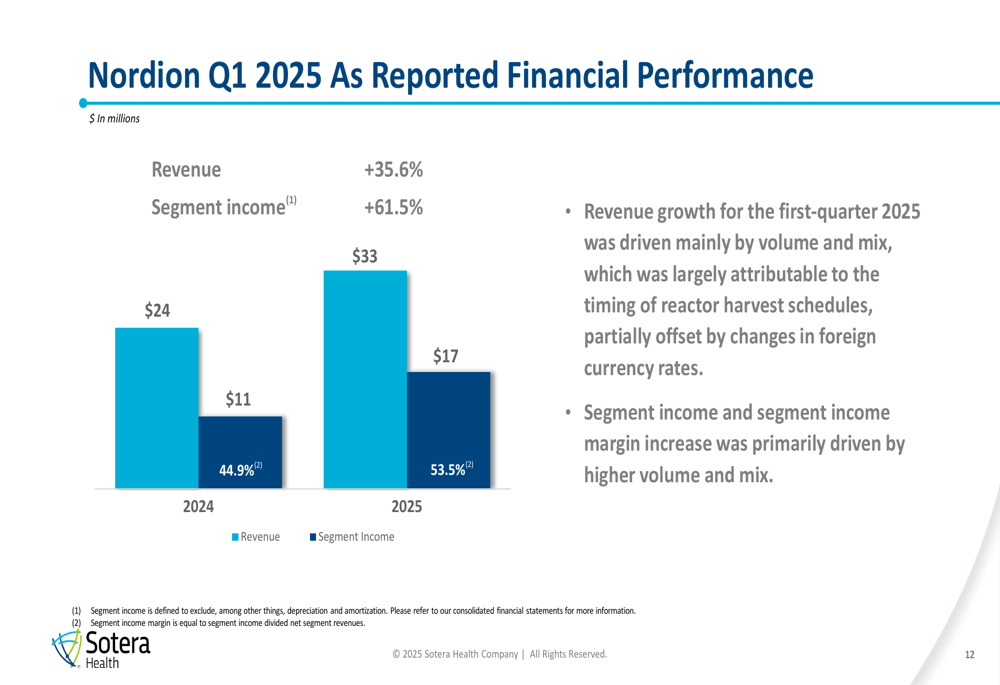

Nordion, which supplies Cobalt-60 for medical device sterilization, was the standout performer with revenue surging 35.6% to $33 million and segment income jumping 61.5% to $17 million. This dramatic improvement was primarily attributed to timing of reactor harvest schedules, with some Q2 shipments moving into Q1.

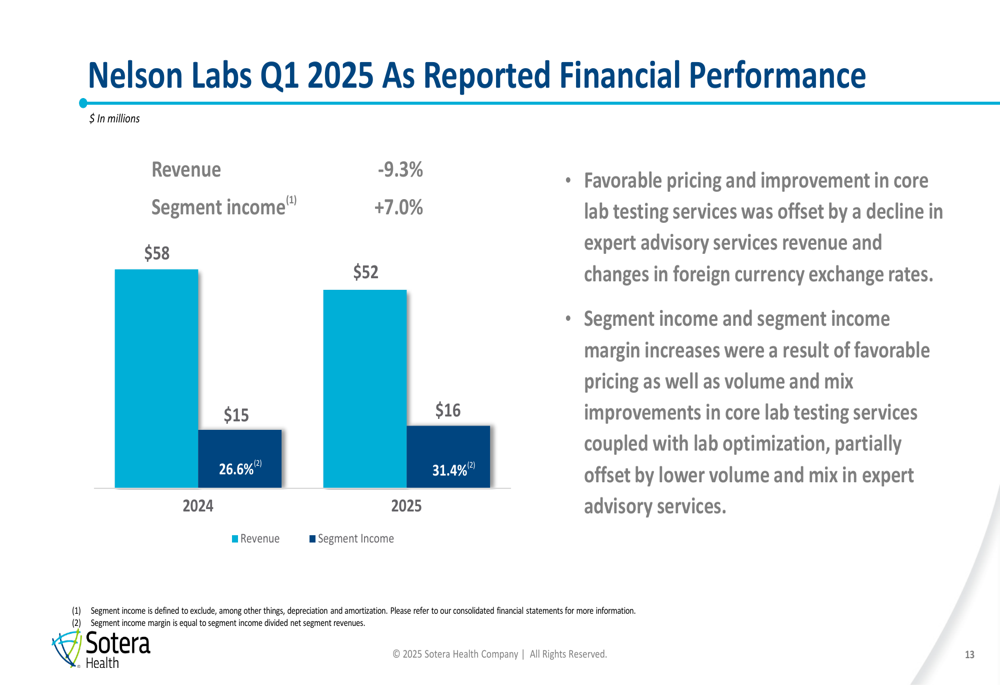

Nelson Labs, providing microbiological and analytical testing services, saw revenue decline 9.3% to $52 million. However, segment income increased 7.0% to $16 million, with margins expanding significantly from 26.6% to 31.4%. Management attributed this to favorable pricing and lab optimization efforts, offset by lower volume in expert advisory services.

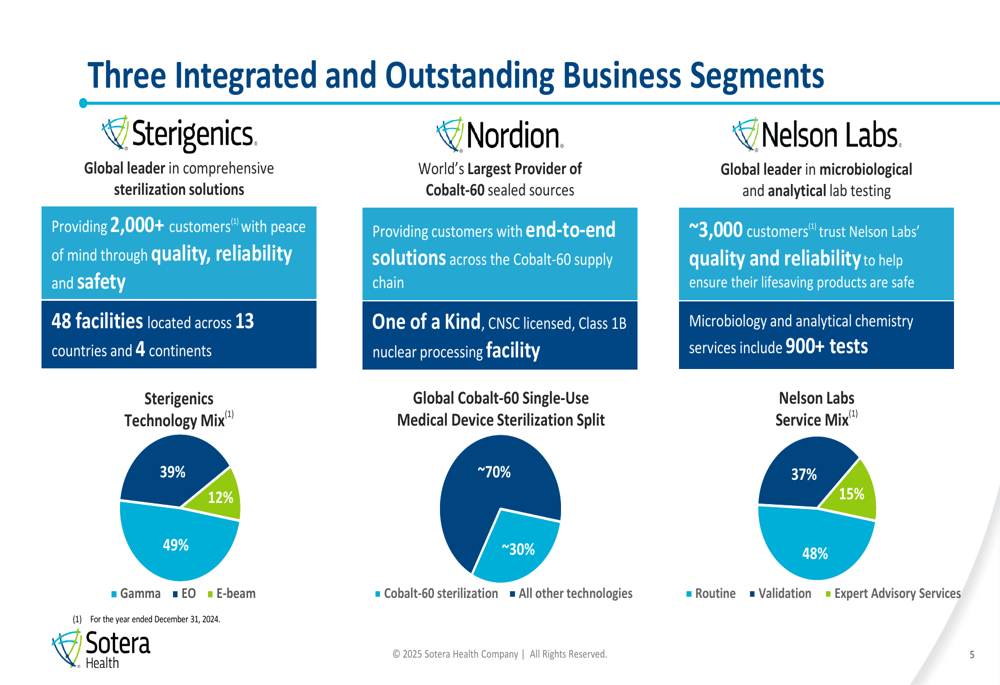

The company’s three integrated business segments serve approximately 5,000 customers across more than 50 countries, with customer relationships averaging over 10 years among its top 25 clients.

Financial Position & Capital Allocation

Sotera Health continues to strengthen its financial position, with its net leverage ratio improving to 3.6x as of March 31, 2025, down from 3.7x at year-end 2024 and 3.8x at the end of 2023. The company maintains a strong liquidity position of $715 million with no outstanding borrowings on its revolving credit facility, which was recently upsized by $176 million and extended to April 2030.

Capital expenditures decreased to $20 million in Q1 2025 from $35 million in Q1 2024. The company continues to invest in Sterigenics capacity expansions, Nordion Cobalt-60 development projects, and Nelson Labs pharmaceutical testing expansion.

On the legal front, Sotera Health signed a $31 million binding term sheet on April 3, 2025, to settle 97 ethylene oxide (EO) cases in Illinois, with finalization expected this summer.

Forward-Looking Statements

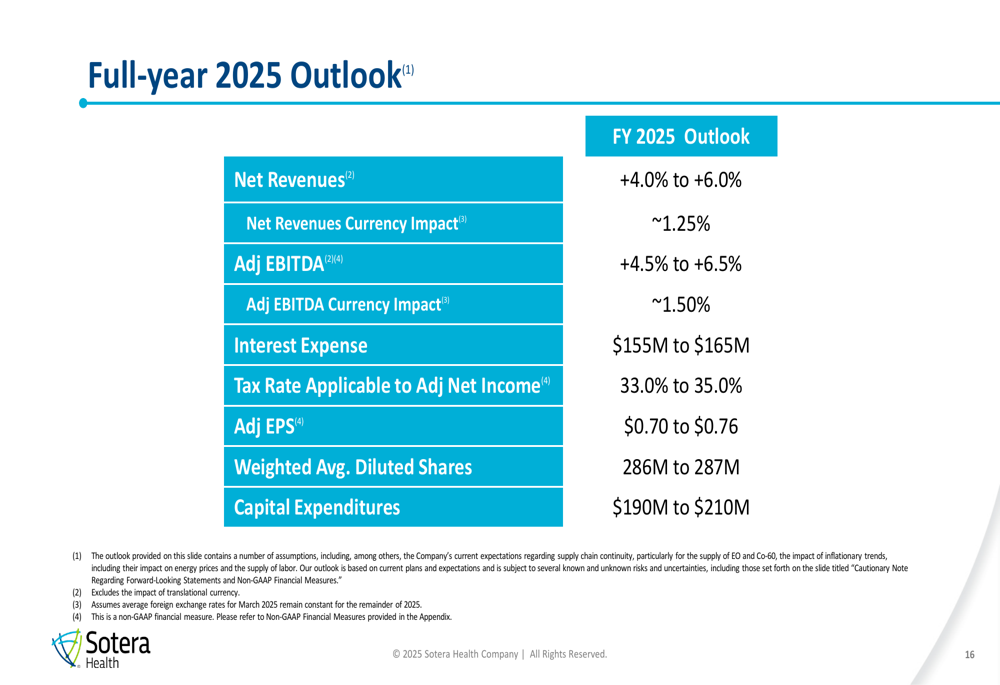

For full-year 2025, Sotera Health projects revenue growth of 4.0% to 6.0% and adjusted EBITDA growth of 4.5% to 6.5%, both on a constant currency basis. The company expects foreign exchange headwinds of approximately 1.25% for revenue and 1.50% for adjusted EBITDA.

As shown in the following outlook chart, adjusted EPS is expected to range from $0.70 to $0.76, with capital expenditures projected between $190 million and $210 million:

Management provided additional color on the 2025 outlook, noting that Sterigenics volumes are expected to improve throughout the year, with constant currency revenue growth in the mid-single digits. Nordion’s revenue timing is expected to follow a similar pattern to 2024, while Nelson Labs is projected to see a low to mid-single digit decline in Q2 before improving in the second half.

The company remains focused on four key priorities: excellence in serving customers with end-to-end solutions, winning in growth markets, driving operational excellence to enhance free cash flow, and disciplined capital deployment.

This earnings presentation marks a positive shift for Sotera Health after its Q4 2024 results, which had missed revenue forecasts and led to a significant stock decline. With margins expanding and a clear path to continued deleveraging, the company appears to be regaining momentum in early 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.