Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Source Energy Services Ltd (TSXV:SHLE) shared its Q2 2025 corporate presentation on July 31, 2025, highlighting record sand sales volumes and strong financial performance. Despite these positive results, the company’s stock fell 8.61% on the day, closing at $13.69, suggesting investors may have expected even stronger performance or reacted to forward guidance not detailed in the presentation.

Quarterly Performance Highlights

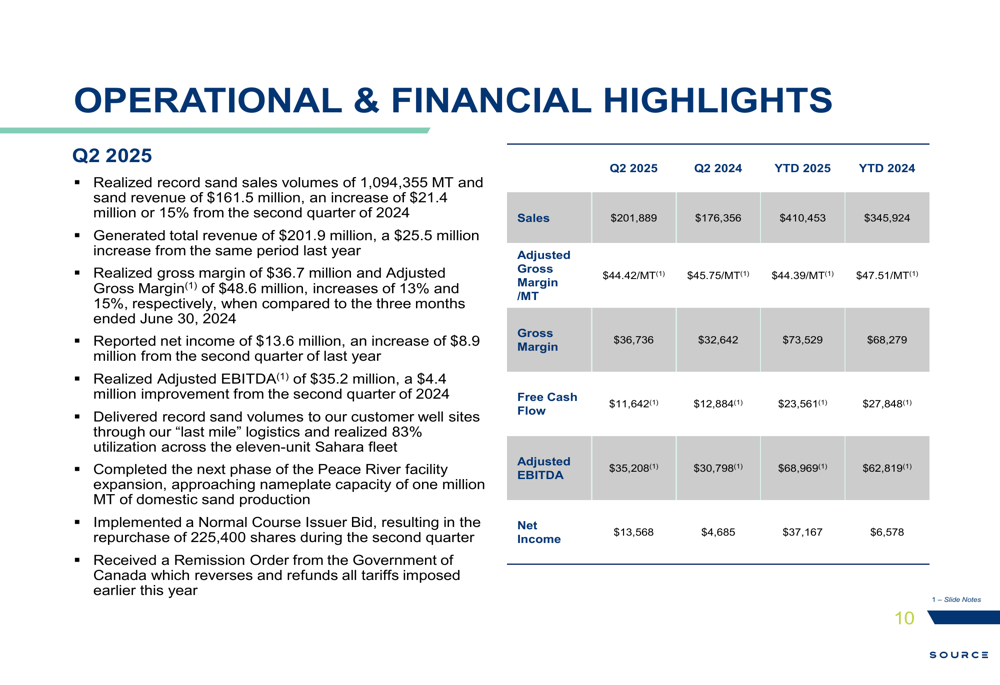

Source Energy reported record sand sales volumes of 1,094,355 metric tons (MT) for Q2 2025, generating sand revenue of $161.5 million. Total (EPA:TTEF) revenue reached $201.9 million, representing a 14.5% increase from $176.4 million in Q2 2024. The company achieved a gross margin of $36.7 million and adjusted gross margin of $48.6 million.

Net income for the quarter was $13.6 million, nearly tripling from $4.7 million in the same period last year, while adjusted EBITDA rose to $35.2 million from $30.8 million in Q2 2024.

As shown in the following financial performance summary:

While the company reported strong year-over-year growth in most metrics, adjusted gross margin per MT slightly decreased to $44.42 in Q2 2025 from $45.75 in Q2 2024. Free cash flow also saw a minor decline to $11.6 million from $12.9 million in the comparable quarter.

These results follow a strong Q1 2025, where the company reported earnings per share of $1.74, significantly exceeding analyst expectations of $0.94, and revenue of $208.6 million against a forecast of $174.75 million.

Strategic Initiatives and Growth Opportunities

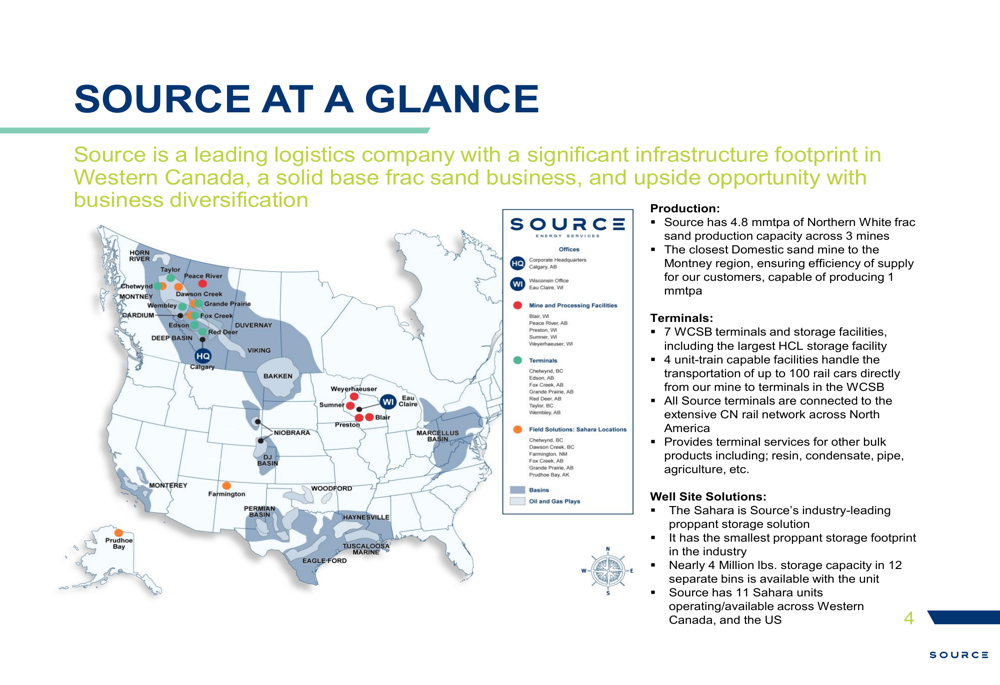

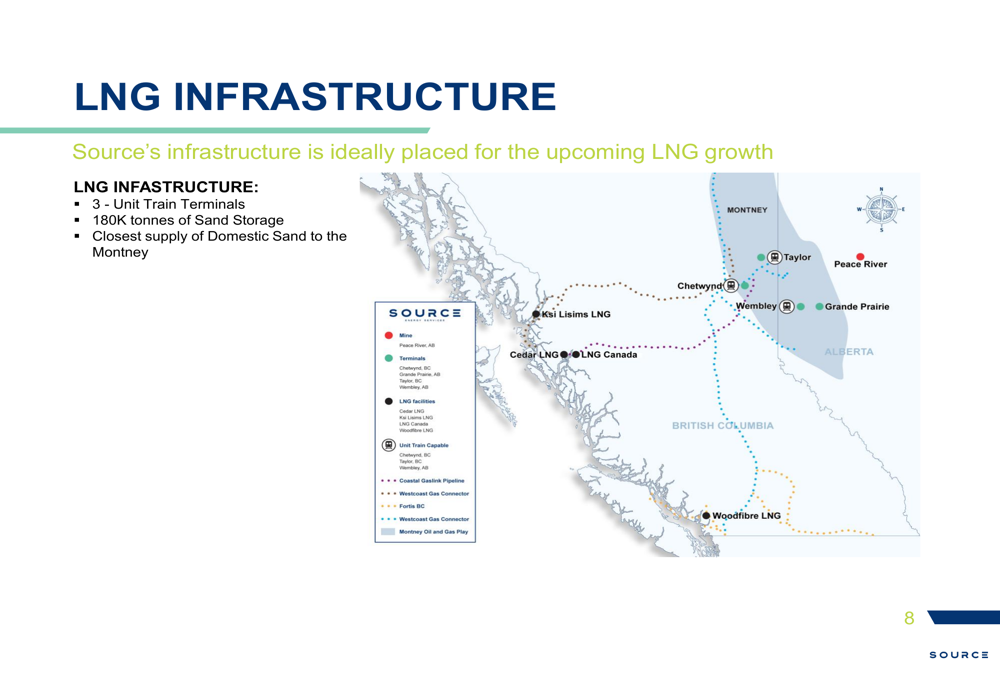

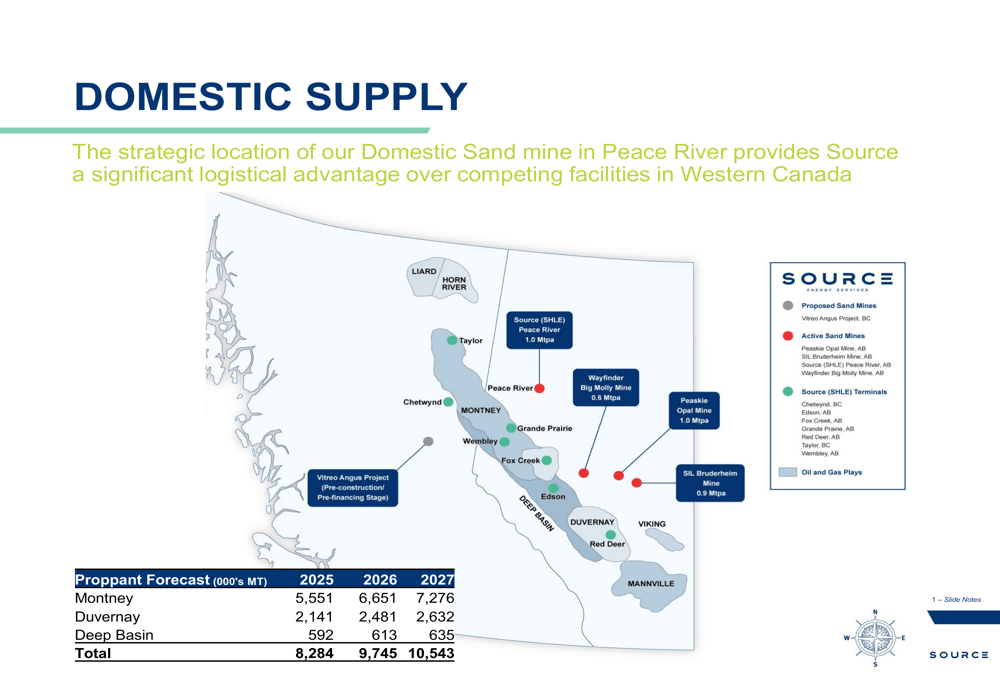

Source Energy is positioning itself to capitalize on growing demand for natural gas and condensate in Western Canada, particularly driven by LNG development. The company’s presentation emphasized its strategic infrastructure footprint across the Western Canadian Sedimentary Basin (WCSB).

The company’s extensive operational network includes:

Source Energy highlighted its unique position as the only supplier offering both Northern White and domestic sand, with its Peace River facility being the closest domestic sand mine to the Montney region, a key area for natural gas production.

The company’s strategic positioning for LNG growth is illustrated in this infrastructure map:

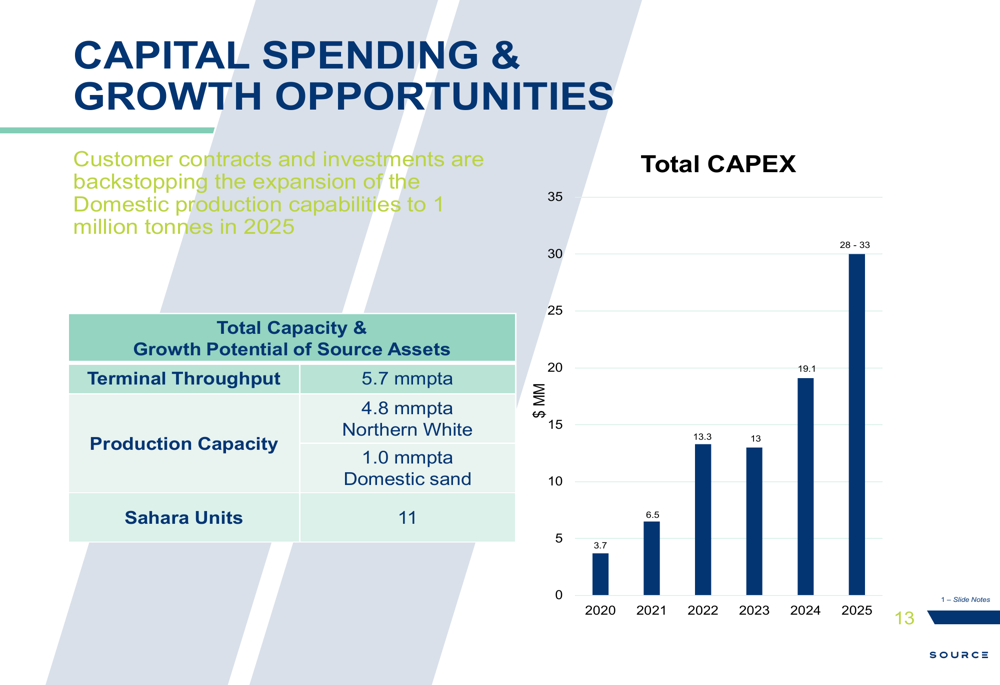

Source Energy is expanding its domestic production capabilities to 1 million tonnes in 2025, backed by customer contracts and investments. The company’s capital expenditure is projected to increase from $19.1 million in 2024 to between $28-33 million in 2025, reflecting its growth strategy.

The capital spending trend and growth opportunities are detailed in the following chart:

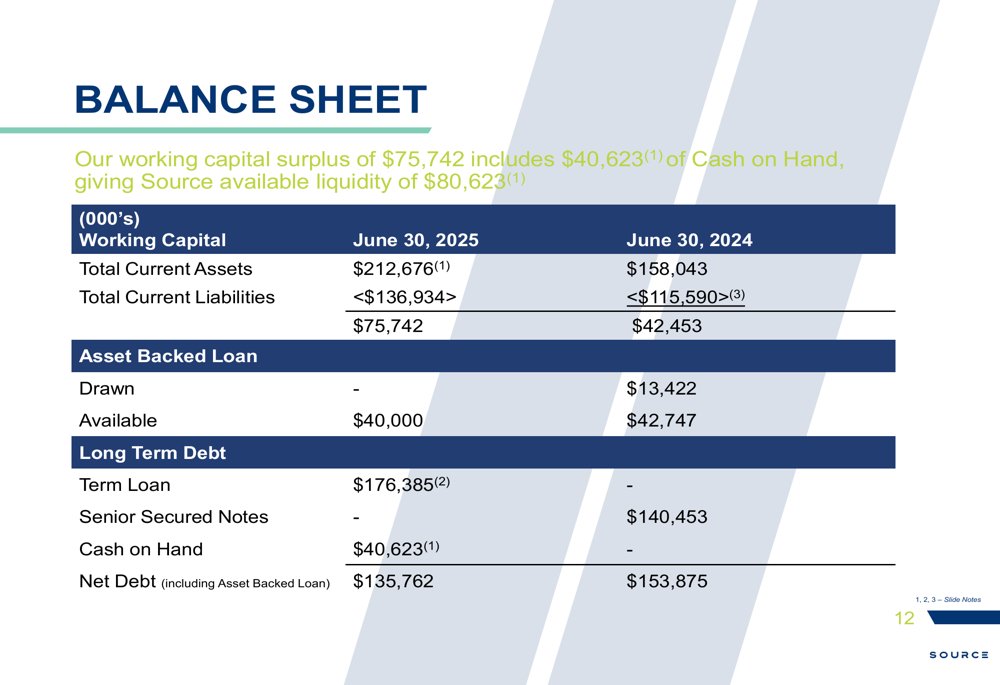

Balance Sheet and Financial Position

Source Energy reported significant improvements in its financial position, with a working capital surplus of $75,742 as of June 30, 2025, compared to $42,453 a year earlier. The company secured a new credit package consisting of a $135 million USD Term Loan (with an additional $25 million available until December 2025) and a $40 million CDN Asset-Backed Loan (ABL) Facility.

Net debt decreased to $135,762 from $153,875 in the prior year, while available liquidity stood at $80,623, providing flexibility for future growth initiatives.

The company’s balance sheet summary shows these improvements:

Forward-Looking Statements

Source Energy expects continued growth in demand for its products and services, driven by increased natural gas production in Western Canada, particularly in the Montney region. The company projects that natural gas demand will continue growing from 2025 to 2030, supported by LNG export growth.

The presentation included a proppant forecast showing expected demand growth across key regions:

In its Q1 2025 earnings call, management had projected 5-10% volume growth for the full year 2025, with adjusted gross margins expected to remain between $45-46 per metric ton. The company anticipates a busy Q2 and Q3, with market stability expected from the completion of LNG Canada.

Source Energy’s investment highlights emphasize its positioning for long-term, sustainable growth in a more stable industry environment with increasing demand for natural gas. The company continues to focus on expanding its logistics services and building flexibility into its business model to adapt to changing market conditions.

Despite the positive outlook presented in the corporate presentation, the 8.61% stock price decline on July 31 suggests investors may have concerns about future performance or broader market factors affecting the energy services sector. The stock closed at $13.69, down from its previous close of $14.98, but still well above its 52-week low of $6.79.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.