Navitas stock soars as company advances 800V tech for NVIDIA AI platforms

Introduction & Market Context

Southern First Bancshares Inc (NASDAQ:SFST) shares jumped 3.99% in premarket trading to $33.61 following the release of its first quarter 2025 investor presentation on April 22, 2025. The bank, which operates 12 branches across eight southeastern metro markets, reported significant year-over-year improvements in earnings and margins while maintaining strong asset quality.

The $4.3 billion asset bank continues to benefit from its strategic positioning in high-growth southeastern markets, where population growth substantially outpaces the national average. This regional focus, combined with improving interest rate dynamics, has contributed to the bank’s strong performance in early 2025.

Quarterly Performance Highlights

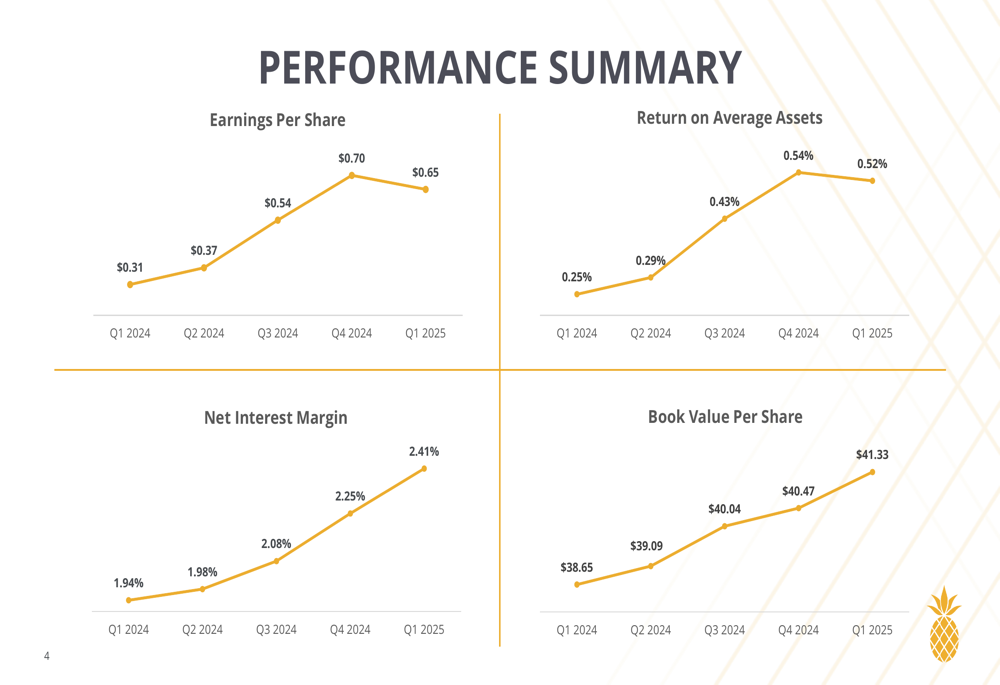

Southern First reported net income of $5.3 million and diluted earnings per share of $0.65 for Q1 2025, representing a 109% increase compared to the same period in 2024. While this marks a slight decrease from $0.70 in Q4 2024, the overall trend shows substantial improvement throughout the past year.

As shown in the following performance summary chart, the bank has demonstrated consistent improvement in key metrics over the past five quarters:

Net interest margin – a critical profitability measure for banks – expanded to 2.41% in Q1 2025, compared to 2.25% in Q4 2024 and 1.94% in Q1 2024. This 47 basis point year-over-year improvement reflects the bank’s success in managing its balance sheet amid changing interest rate conditions.

Return on average assets reached 0.52% in Q1 2025, more than double the 0.25% reported in Q1 2024, while book value per share increased to $41.33, continuing its steady upward trajectory.

Balance Sheet and Asset Quality

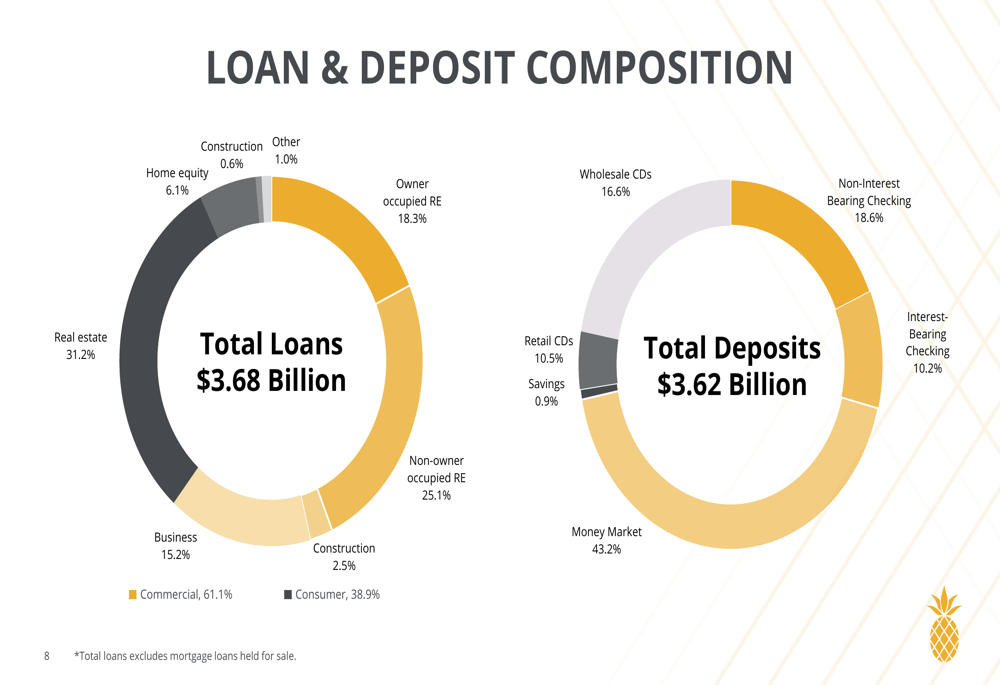

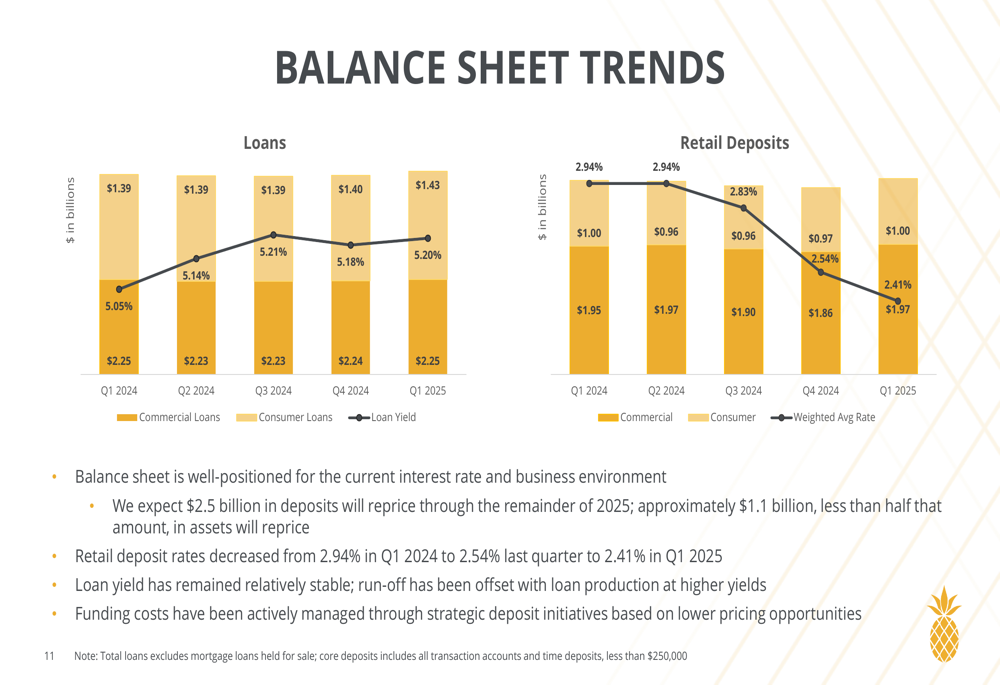

Southern First reported total loans of $3.7 billion, representing 6% annualized growth over Q4 2024. Core deposits grew at an impressive 23% annualized rate to $2.8 billion. The bank’s loan portfolio remains well-diversified, with 61.1% in commercial loans and 38.9% in consumer loans.

The deposit composition reveals a healthy funding mix, with 18.6% in non-interest bearing checking accounts and 43.2% in money market accounts. The bank noted that retail deposit rates have decreased from 2.94% in Q1 2024 to 2.41% in Q1 2025, contributing to margin expansion.

The following charts illustrate the bank’s loan and deposit composition:

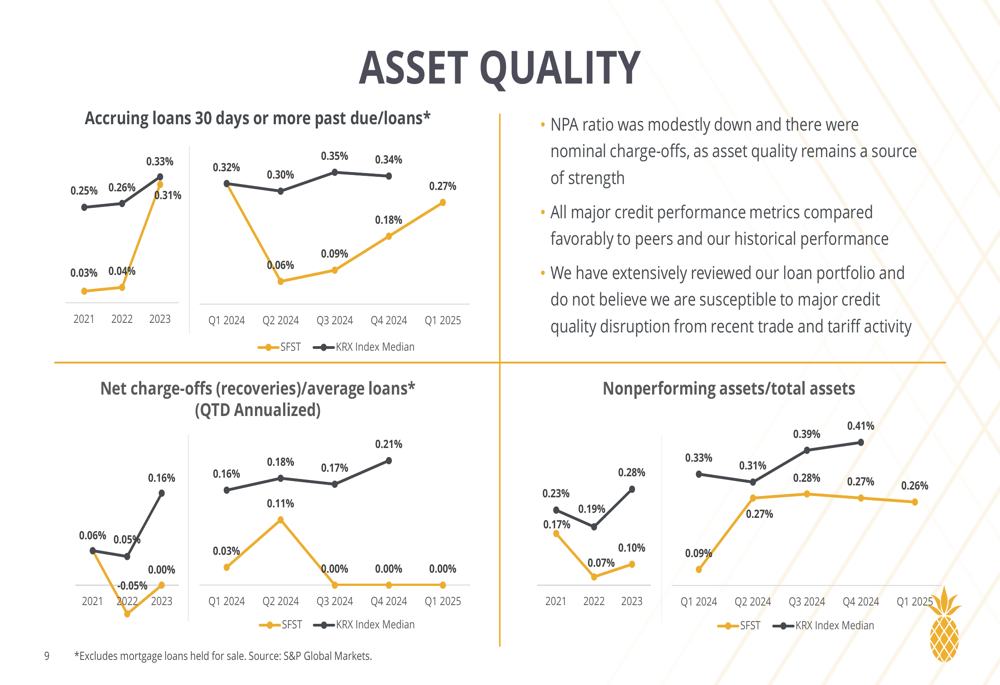

Asset quality remains strong, with nonperforming assets to total assets at 0.26% and past due loans to total loans at 0.27%. These metrics compare favorably to industry benchmarks, as shown in the following asset quality comparison:

The bank’s office loan portfolio, an area of concern for many financial institutions, represents 5.3% of total loans with $214 million in total exposure. The portfolio is diversified across medical offices, multi-tenant, and single-tenant properties, with minimal delinquencies.

Strategic Position and Growth Markets

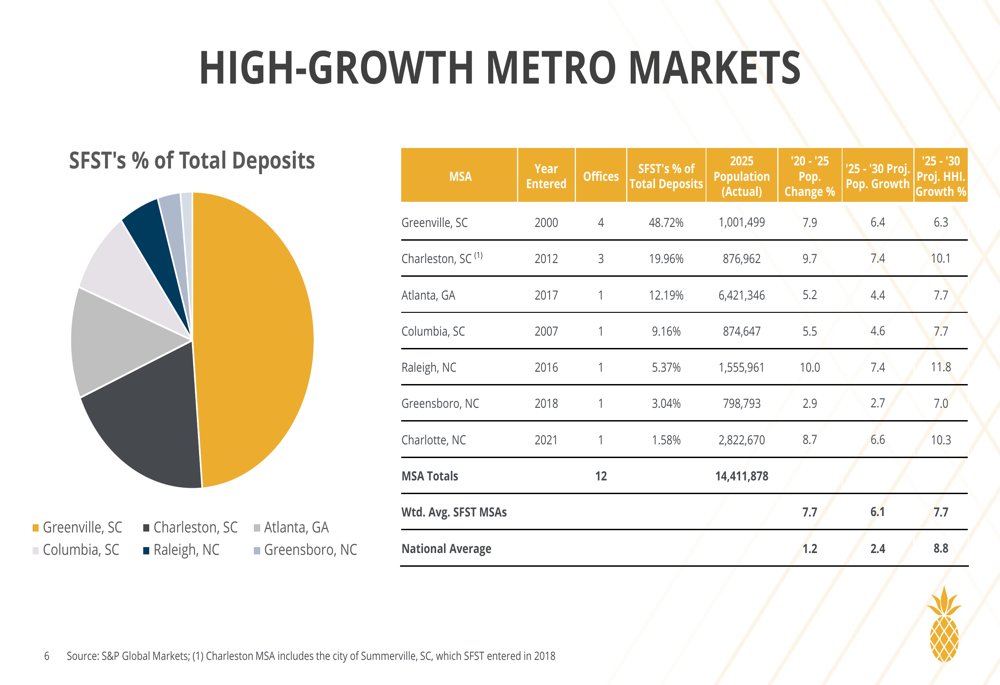

Southern First’s strategic focus on high-growth southeastern markets continues to be a key differentiator. The bank operates in metropolitan areas experiencing population growth rates significantly above the national average, providing a favorable environment for continued organic expansion.

As illustrated in the following market analysis, Southern First’s footprint includes markets with projected population growth rates of 6.4% to 6.6% for 2025-2030, compared to the national average of 2.4%:

The bank’s balance sheet trends demonstrate the benefits of this strategic positioning, with improving loan yields and decreasing deposit costs:

Southern First’s efficient operating model, with just 12 banking offices and approximately 300 associates, contributes to competitive noninterest expense ratios. The bank’s noninterest expense to average assets ratio stood at 1.87% in Q1 2025.

Forward-Looking Statements

Looking ahead, Southern First outlined several strategic priorities, including strengthening its balance sheet, growing core deposits, and optimizing its loan portfolio. Management indicated they expect $2.5 billion in deposits to reprice, potentially providing further margin improvement opportunities.

The bank’s capital position continues to strengthen, with a total risk-based capital ratio of 12.69%, tier 1 risk-based capital ratio of 11.15%, and tangible common equity ratio of 7.88%.

Southern First remains focused on its relationship-driven banking model while embracing technology and maintaining its commitment to organic growth in its southeastern markets. With its strong Q1 2025 performance and favorable regional dynamics, the bank appears well-positioned for continued growth throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.