Gold prices fall as geopolitical tensions ease; U.S. CPI looms

Introduction & Market Context

Sparebanken Sør (Sparebanken Sor) reported its first quarter 2025 results on April 30, showing resilience in core operations despite merger-related expenses weighing on overall profitability. The Norwegian regional bank’s shares traded at 195.28 NOK following the presentation, up 0.31% for the day, and remain near the upper end of their 52-week range of 141.1-215 NOK.

The bank’s performance reflects the challenging interest rate environment in Norway, with pressure on deposit margins in the personal market, while benefiting from strong contributions from associated companies and improved commission income.

Quarterly Performance Highlights

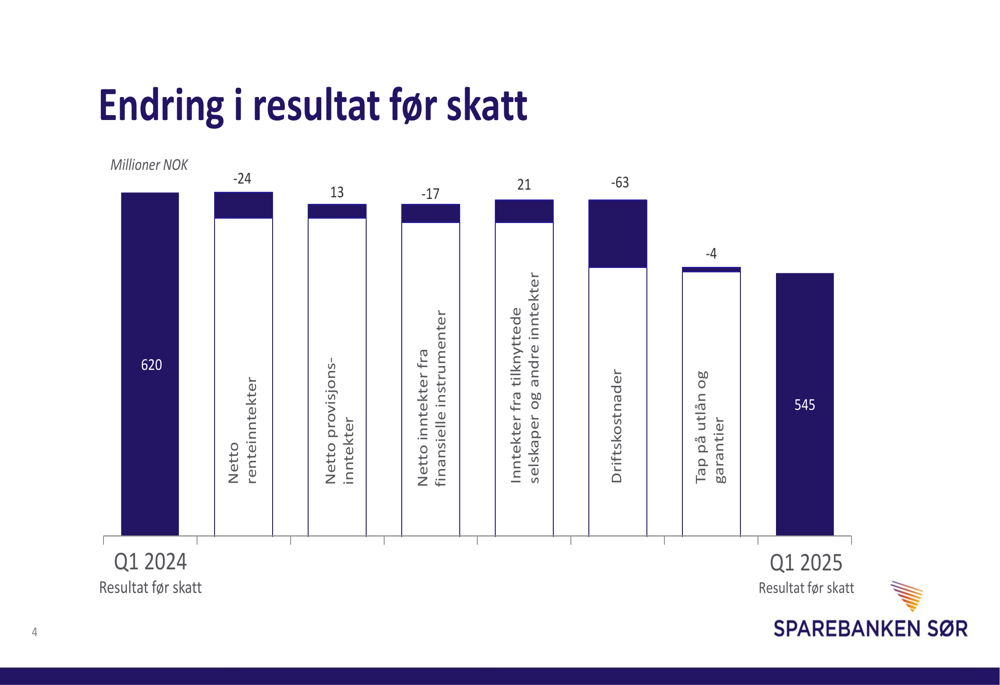

Sparebanken Sør reported profit before tax of 545 million NOK for Q1 2025, down from 620 million NOK in the same period last year. Profit after tax came in at 529 million NOK, compared to 573 million NOK in Q1 2024. The bank noted that merger costs of 30 million NOK significantly impacted the quarterly results.

As shown in the following financial summary table, the bank maintained solid income despite some headwinds:

Net interest income decreased slightly to 800 million NOK from 824 million NOK in Q1 2024, while net commission income showed positive development, increasing to 98 million NOK from 85 million NOK. A notable bright spot was the contribution from associated companies, which rose to 27 million NOK from just 5 million NOK in the prior-year quarter.

The following waterfall chart illustrates the key factors affecting the change in profit before tax from Q1 2024 to Q1 2025:

Detailed Financial Analysis

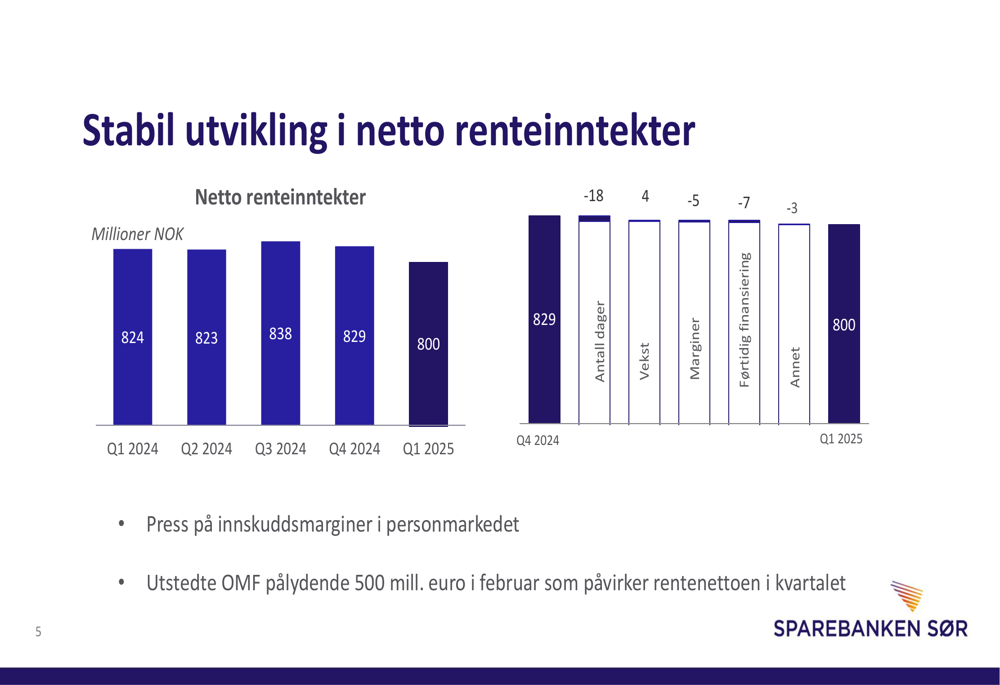

Net interest income has remained relatively stable over the past five quarters, though showing a slight decline in Q1 2025. The bank cited pressure on deposit margins in the personal market and the impact of a 500 million euro covered bond issuance in February as factors affecting interest income during the quarter.

The following chart shows the development of net interest income over the past five quarters:

Operating costs increased to 393 million NOK from 330 million NOK in Q1 2024. This 19% increase was primarily driven by merger costs (30 million NOK), increased headcount, higher depreciation, and general wage and price inflation. Excluding merger costs, the bank maintained a competitive cost percentage of 38.3%.

The bank reported continued low loan losses of 10 million NOK, slightly up from 6 million NOK in Q1 2024, reflecting the overall good quality of the loan portfolio.

Growth and Portfolio Composition

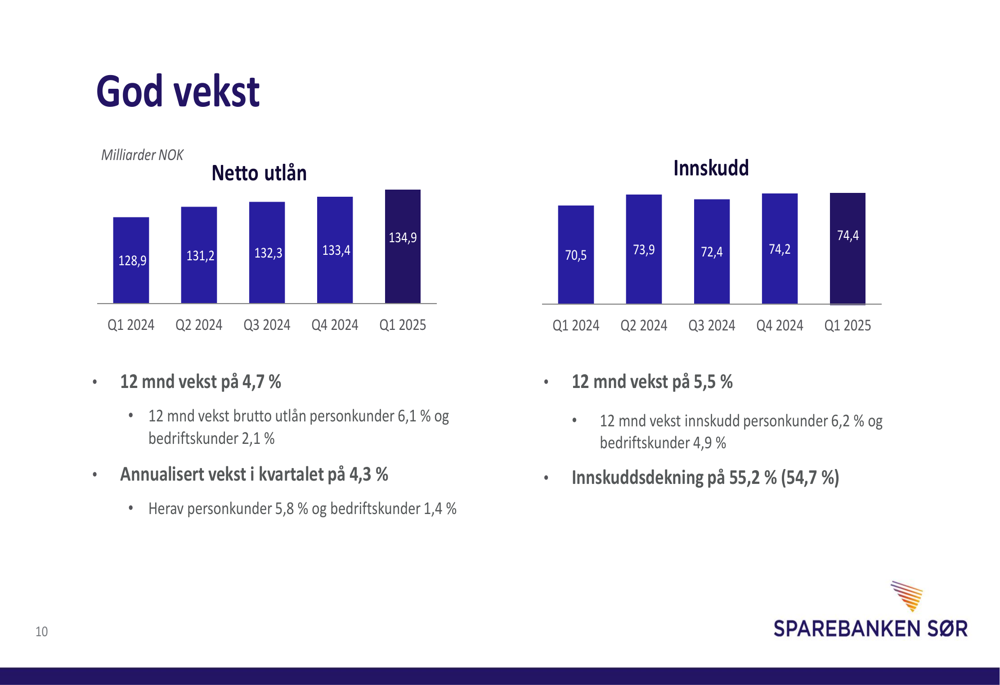

Sparebanken Sør achieved solid growth in both loans and deposits. Net loans increased to 134.9 billion NOK, representing 12-month growth of 4.7%. Growth was stronger in the personal customer segment at 6.1%, compared to 2.1% for business customers.

Deposits grew by 5.5% over the past 12 months to 74.4 billion NOK, with the deposit coverage ratio improving to 55.2% from 54.7% a year earlier. The bank’s growth trajectory is illustrated in the following chart:

The bank maintains a well-diversified lending portfolio with a conservative risk profile. Personal customers account for 65% of the loan portfolio, with business customers making up the remaining 35%. Geographically, 62% of loans are in the Agder region, with the remainder spread across Vestfold and Telemark (15%), Oslo (9%), Rogaland (4%), and other regions (10%).

Associated Companies and Strategic Initiatives

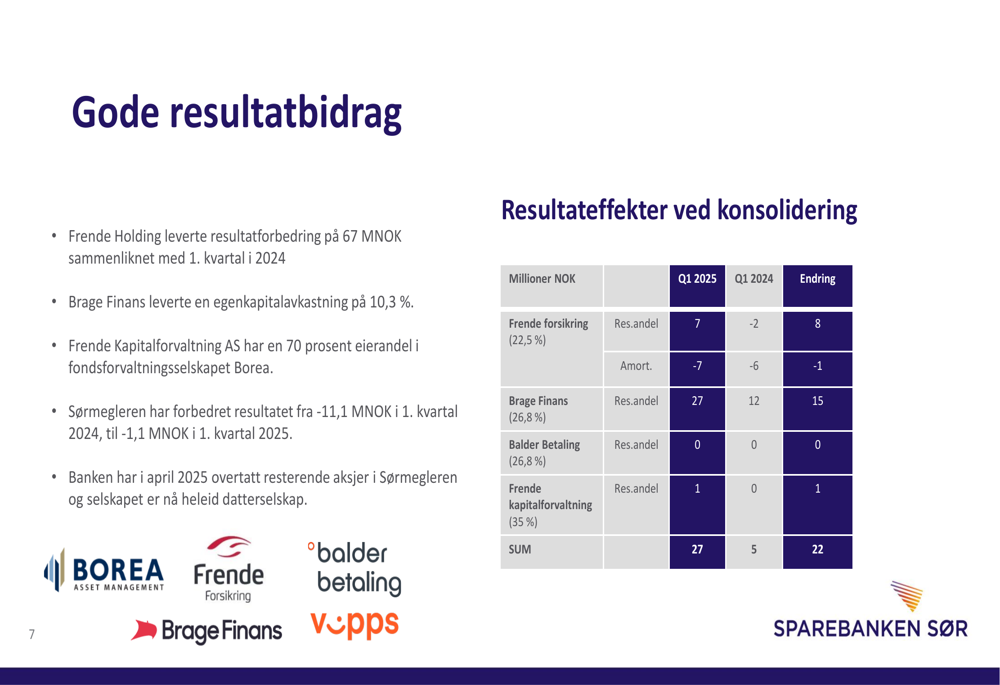

A significant highlight in the quarter was the strong performance of Sparebanken Sør’s associated companies. Frende Holding delivered a 67 million NOK improvement in results compared to Q1 2024, while Brage Finans achieved a return on equity of 10.3%.

The bank’s real estate broker, Sørmegleren, substantially improved its results from a loss of 11.1 million NOK in Q1 2024 to a much smaller loss of 1.1 million NOK in Q1 2025. In April 2025, the bank acquired the remaining shares in Sørmegleren, making it a wholly-owned subsidiary.

The following table details the contributions from associated companies:

Capital Position and Forward Outlook

Sparebanken Sør significantly strengthened its capital position, with the core equity tier 1 capital ratio increasing from 16.1% to 18.5% between March and April 2025. This places the bank well above the regulatory requirement of 14.9% and the internal target including capital margin of 15.9%.

The bank expects to benefit from the implementation of CRR3 (Basel IV) regulations, which should result in capital release and improved return on equity. The solid capital position provides flexibility for future growth and shareholder returns.

Despite the impact of merger costs in Q1, Sparebanken Sør’s underlying performance remains solid, with strong contributions from associated companies, improved commission income, and continued low loan losses offsetting pressure on interest margins. The bank’s diversified lending portfolio and strong capital position position it well for sustainable growth in the Norwegian banking market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.