Gold prices edge higher on raised Fed rate cut hopes

Introduction & Market Context

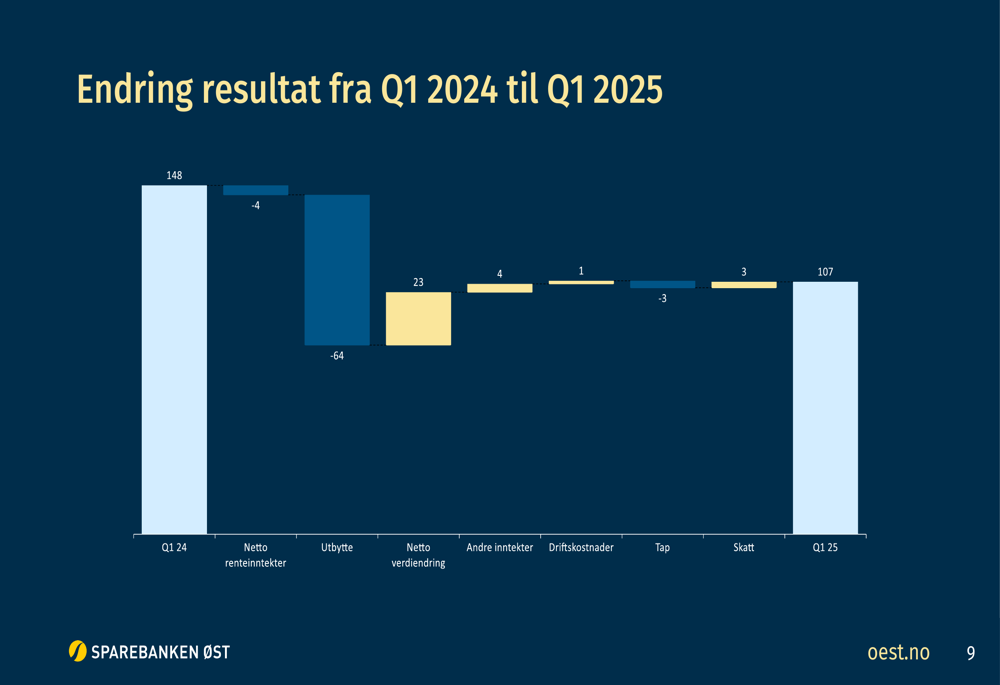

Sparebanken Øst (OB:SPOG) presented its first quarter 2025 financial results on May 14, revealing a 28% year-over-year decline in profit after tax to 107 million Norwegian kroner (NOK), down from 148 million NOK in Q1 2024. The bank’s shares closed at 72.41 NOK on May 13, down 1.2% ahead of the results announcement.

Despite the profit decline, the regional Norwegian bank emphasized its solid capital position and stable core operations, with management highlighting "satisfactory return on equity" as a key achievement for the quarter.

Quarterly Performance Highlights

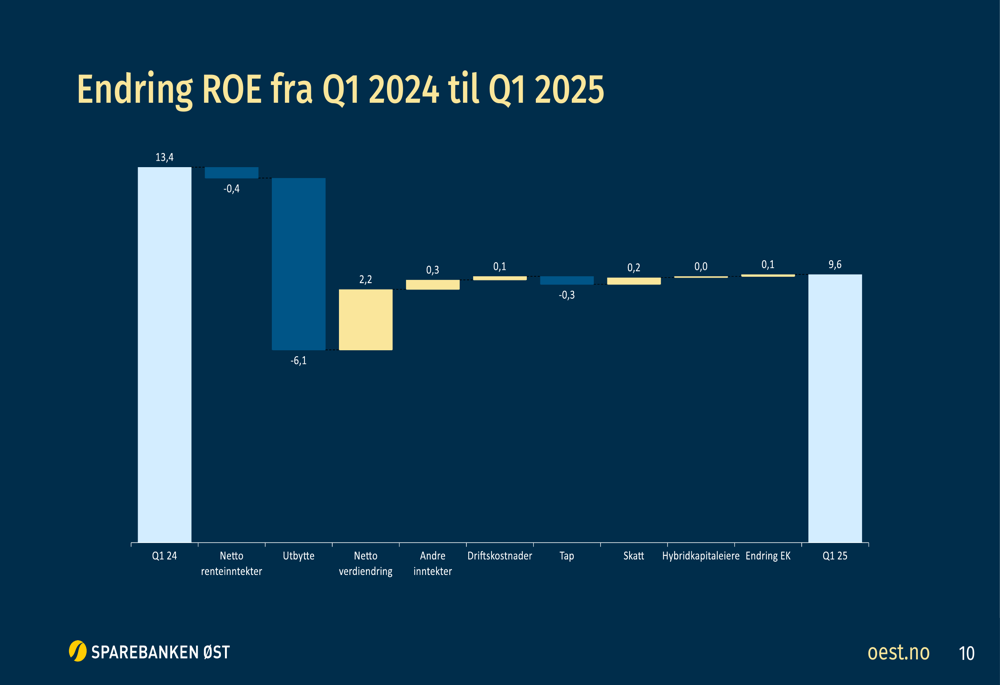

Sparebanken Øst reported return on equity (ROE) of 9.6% for Q1 2025, down significantly from 13.4% in the same period last year. The bank’s net interest income reached 220 million NOK (1.90% of average assets under management), slightly below the 224 million NOK (1.95%) recorded in Q1 2024.

As shown in the following breakdown of profit changes, the primary driver behind the 41 million NOK profit decline was a 64 million NOK decrease in dividend income, partially offset by a 23 million NOK increase in net value changes:

The bank’s operating costs increased marginally to 96 million NOK in Q1 2025 from 95 million NOK in Q1 2024, representing 39.8% of income compared to 34.3% in the prior-year period. This cost-to-income deterioration reflects both the slight cost increase and the lower overall income.

The decline in return on equity can be attributed to several factors, as illustrated in the following waterfall chart:

Total (EPA:TTEF) loans to customers decreased to 36.8 billion NOK in Q1 2025, down 0.6% from the previous quarter and 4.4% lower than Q1 2024. Retail loans remained flat at 33.4 billion NOK quarter-over-quarter, while corporate loans declined by 5.6% to 3.4 billion NOK.

Customer deposits, meanwhile, grew to 17.0 billion NOK, up 0.9% from the previous quarter and 6.3% higher than Q1 2024. This improved the bank’s deposit coverage ratio to 46.3%, strengthening its funding profile.

Capital Position and Regulatory Outlook

Sparebanken Øst maintained a strong capital position, with its capital adequacy ratio increasing to 22.80% and an unweighted core capital ratio of 8.55%. This places the bank well above the minimum requirement for core equity capital of 15.6%.

As shown in the following capital adequacy chart, the bank’s solid capital position provides flexibility for growth opportunities and dividend capacity:

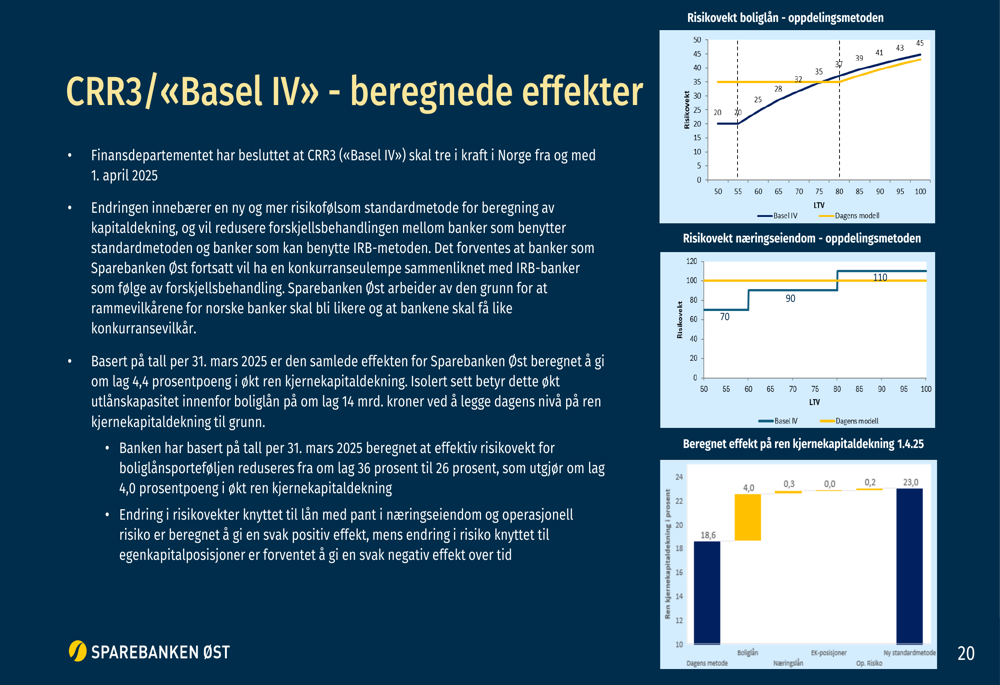

Looking ahead to regulatory changes, Sparebanken Øst expects the implementation of CRR3/Basel IV to have a positive impact on its capital position. The bank estimates these changes will increase its Tier 1 capital adequacy ratio by approximately 4.4 percentage points, with the effective risk weight for the mortgage portfolio expected to decrease from approximately 36% to 26%.

Strategic Initiatives

In a significant development, Sparebanken Øst announced it has received an offer from DNB Bank ASA to sell its shares in Eksportfinans ASA. The bank owns 12,787 shares, representing a 4.85% stake in Eksportfinans, with the offer price set at 18,940 NOK per share.

If completed, the transaction would generate a positive effect of approximately 80 million NOK for Sparebanken Øst. However, the bank noted that selling these shares is not expected to materially impact its capital coverage.

The bank continues to benefit from its strategic location in a growing region. According to Statistics Norway, Sparebanken Øst’s geographical area is expected to grow by 15%, adding approximately 350,000 new inhabitants, providing a solid foundation for future growth.

Forward-Looking Statements

Looking ahead, Sparebanken Øst expects loan growth to align with overall credit growth in Norway. Management acknowledged that high competition for mortgage customers will continue to put pressure on lending margins, while deposit margins are expected to remain high but decrease with lower money market rates and increased competition.

The bank anticipates maintaining solid cost control, though it warned that price growth, rising wages, and increased IT costs are likely to impact overall cost developments. Loan losses are expected to remain low, consistent with recent trends despite the slight uptick in non-performing loans.

Management emphasized that the group remains "very solid," providing room for growth opportunities and dividend capacity, and is well-positioned to navigate macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.