Bullish indicating open at $55-$60, IPO prices at $37

Sparebanken Øst (OB:SPOG) reported a significant jump in profitability for the second quarter of 2025, driven largely by a one-time gain from the sale of its stake in Eksportfinans ASA, according to the bank’s financial presentation released on July 14.

Quarterly Performance Highlights

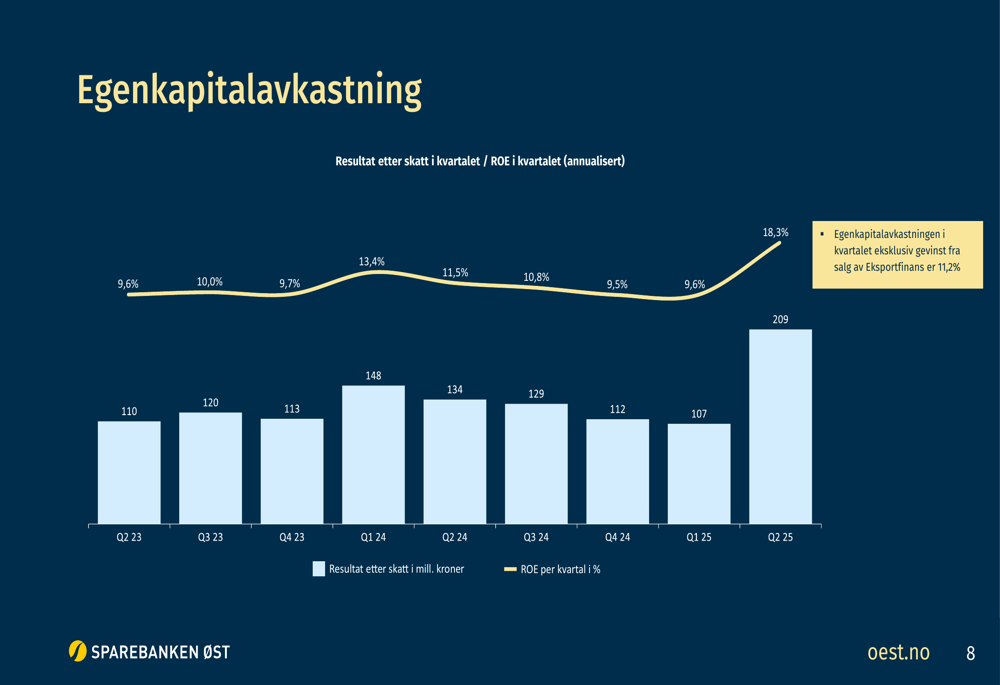

The Norwegian regional bank posted a return on equity (ROE) of 18.3% in Q2 2025, nearly doubling from 9.6% in the previous quarter. Profit after tax surged to 209 million Norwegian kroner, compared to 107 million kroner in Q1 2025.

The exceptional performance was primarily attributed to the sale of the bank’s 4.85% stake (12,787 shares) in Eksportfinans ASA to DNB Bank ASA at 18,940 kroner per share, generating a profit of 80.1 million kroner. Excluding this one-time gain, the bank’s underlying ROE for the quarter would have been 11.2%.

As shown in the following chart of quarterly return on equity:

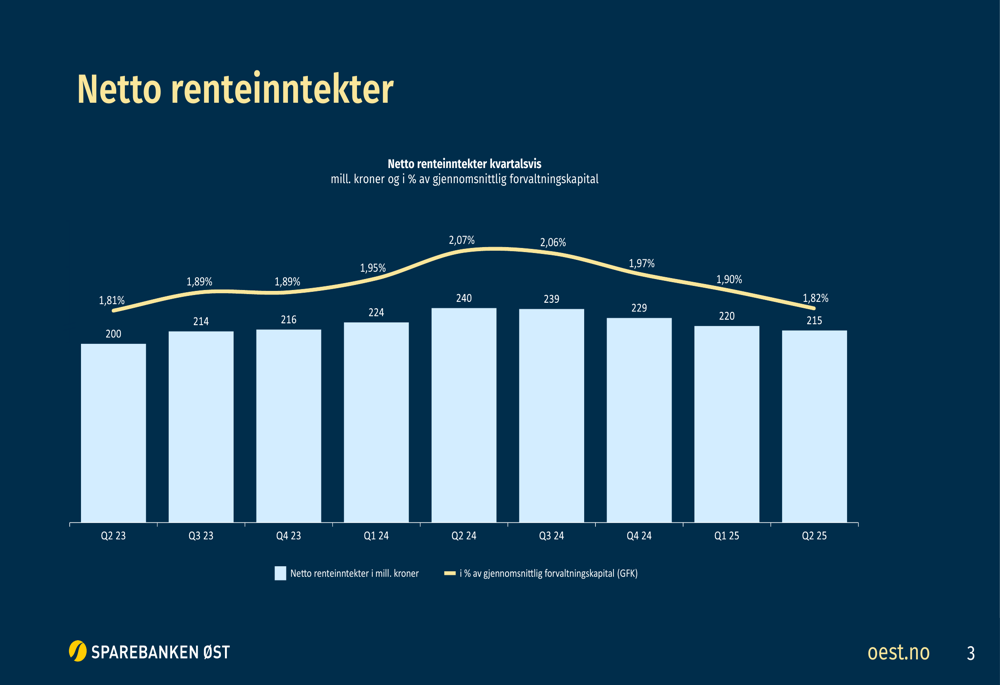

Despite the strong bottom-line results, Sparebanken Øst faced challenges with its core banking operations. Net interest income continued its downward trend, reaching 215 million kroner (1.90% of average assets) in Q2 2025, down from 220 million kroner (1.97%) in Q1 2025 and significantly below the peak of 240 million kroner (2.07%) recorded in Q3 2024.

The following chart illustrates the declining trend in net interest income:

Detailed Financial Analysis

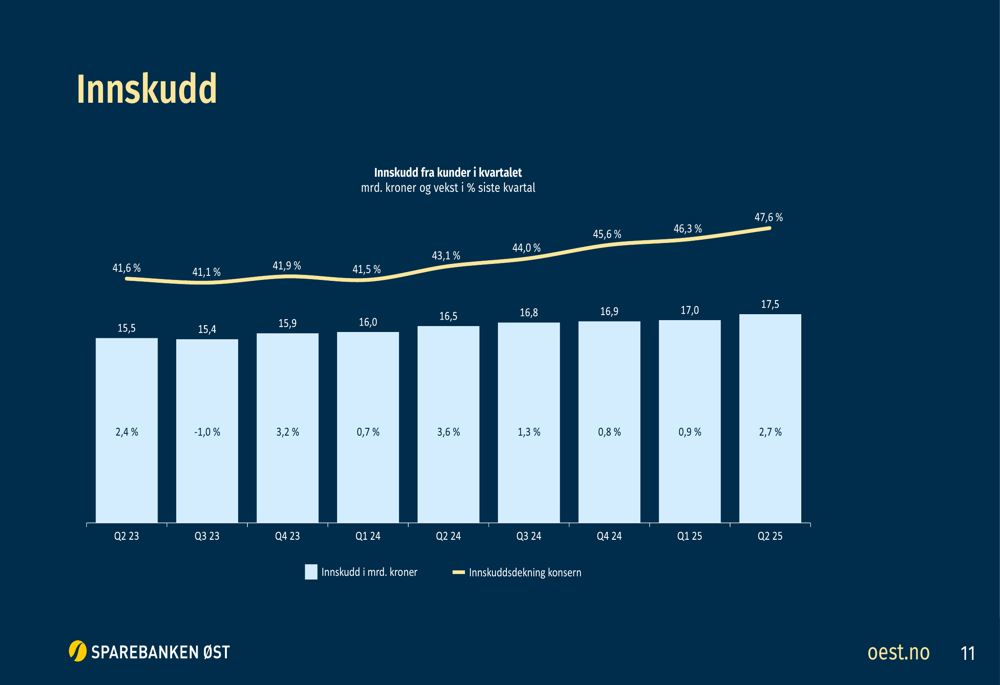

The bank’s deposit volume showed continued growth, reaching 17.5 billion kroner in Q2 2025, a 2.9% increase from the previous quarter. The deposit-to-loan ratio improved to 47.6%, continuing a steady upward trend from 41.6% in Q2 2023.

This deposit growth is illustrated in the following chart:

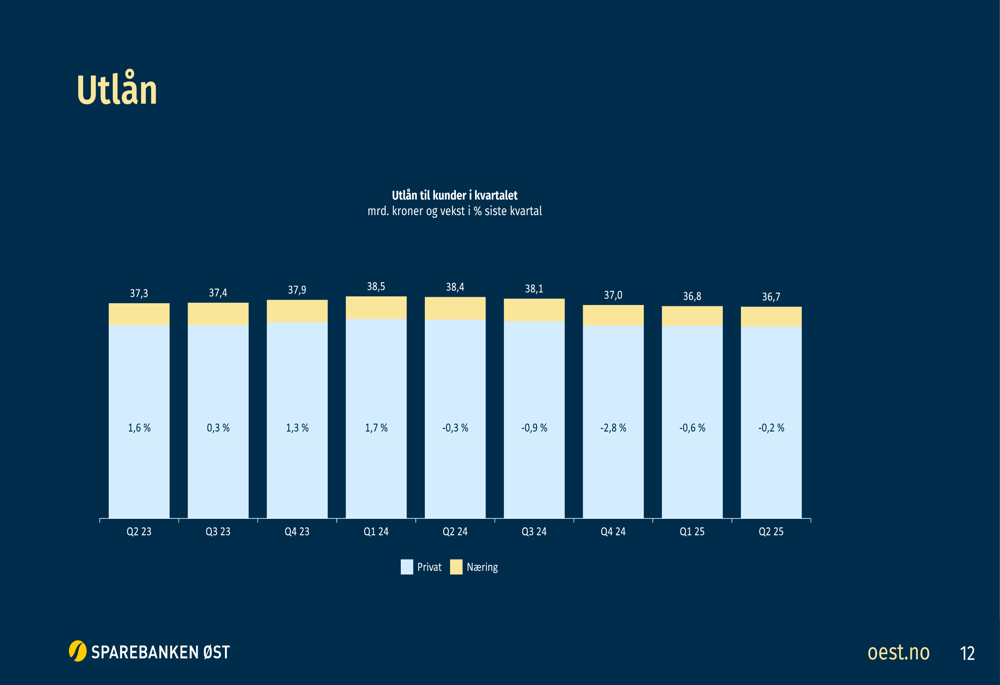

Meanwhile, lending volumes remained relatively stable with a slight decrease of 0.2% quarter-over-quarter to 36.7 billion kroner. The bank has experienced a gradual decline in lending over the past year, with volumes down from 38.4 billion kroner in Q2 2024.

The lending trend is shown in this chart:

Cost efficiency improved markedly in Q2 2025, with operating costs representing 25.6% of income, down from 38.8% in Q1 2025. Total (EPA:TTEF) operating costs for the quarter were 84 million kroner, with personnel costs decreasing to 41 million kroner from 52 million in the previous quarter.

Asset quality remained strong with impairments at just 1.5 million kroner (0.02% of net loans) in Q2 2025, down from 5.7 million kroner (0.06%) in Q1 2025, indicating minimal credit risk concerns.

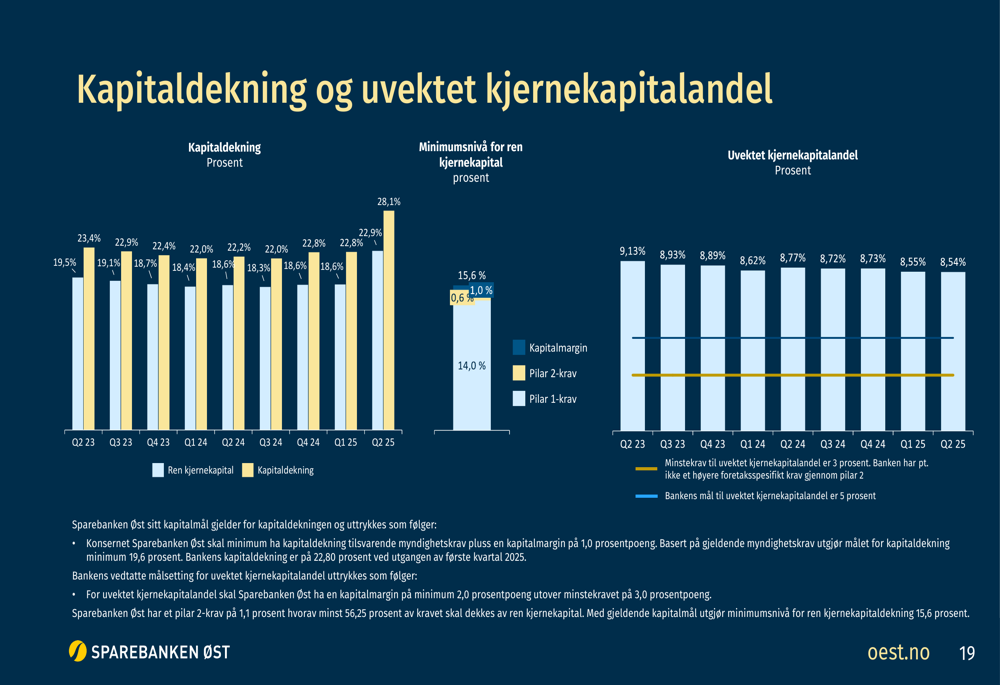

The implementation of the new standard method for capital adequacy (CRR3/"Basel IV") on April 1, 2025, positively impacted the bank’s capital position. The capital adequacy ratio improved to 22.8% in Q2 2025, well above the minimum requirement of 15.6%.

The following chart shows the bank’s strong capital position:

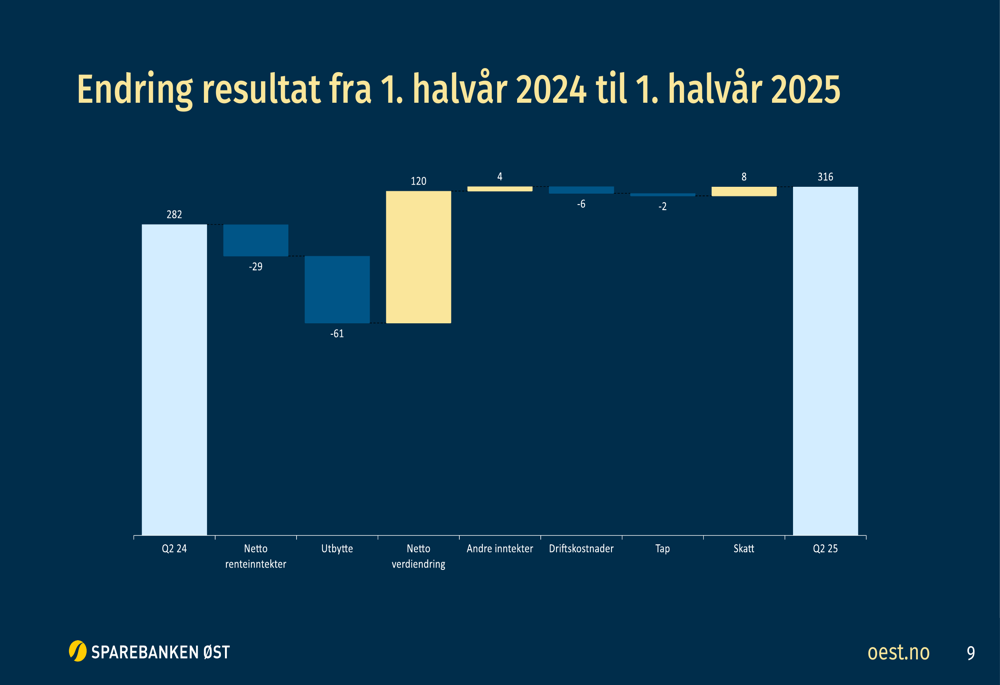

The bank’s profit change from H1 2024 to H1 2025 can be broken down into several components, with net value changes contributing positively while net interest income and dividends had negative impacts:

Forward-Looking Statements

Looking ahead, Sparebanken Øst expects loan growth to follow national credit growth trends. The bank acknowledged the highly competitive environment in the mortgage market and anticipated further pressure on deposit margins.

Management also highlighted that while the bank maintains good cost control, future expenses will be influenced by price and salary increases as well as rising IT costs.

Sparebanken Øst closed at 77 Norwegian kroner on July 11, 2025, down 0.77% for the day. The stock has traded between 54.51 and 83.99 kroner over the past 52 weeks.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.