CCH Holdings prices IPO at $4 per share on NASDAQ

Introduction & Market Context

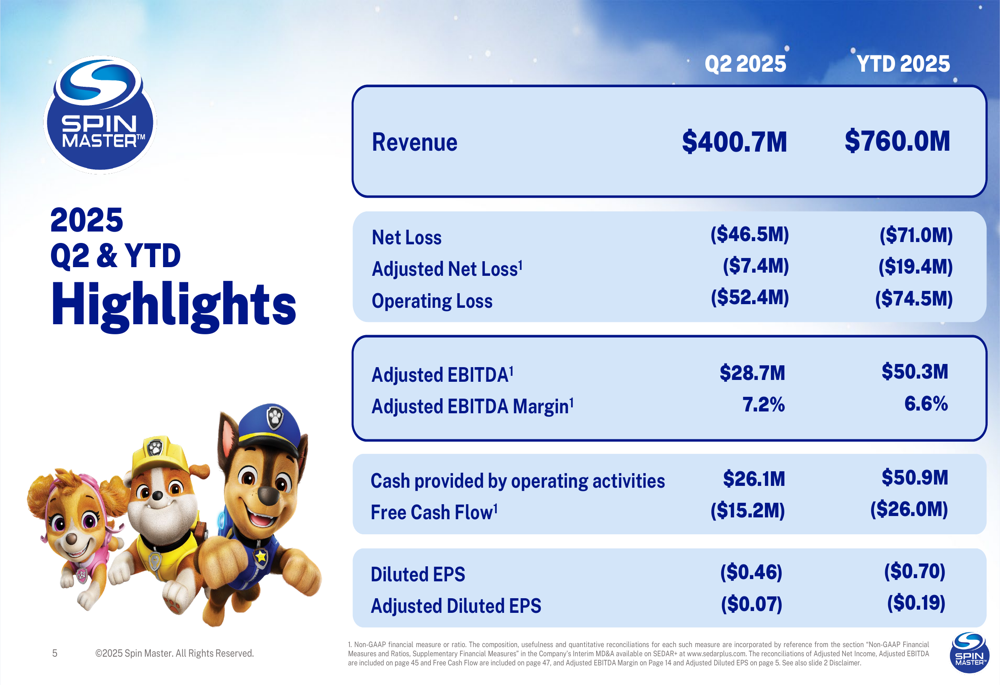

Spin Master Corp (TSX:TOY) released its Q2 2025 supplemental information presentation on July 31, 2025, revealing a mixed quarter with overall revenue declining while its Digital Games segment showed strong growth. The company reported total revenue of $400.7 million, representing a 2.7% decrease compared to Q2 2024, though year-to-date revenue increased by 4.4% to $760 million.

The children’s entertainment company, known for brands like PAW Patrol, Bakugan, and Melissa & Doug, continues to navigate challenges including tariff uncertainties that previously led to the withdrawal of its 2025 financial guidance during Q1 earnings. The stock closed at $24.93 on July 30, 2025, down 0.8% ahead of the earnings release, and is currently trading closer to its 52-week low of $20.97 than its high of $35.44.

Quarterly Performance Highlights

Spin Master reported a net loss of $46.5 million for Q2 2025, with an adjusted net loss of $7.4 million. Adjusted EBITDA came in at $28.7 million with a 7.2% margin, significantly down from $53.6 million and a 13.0% margin in the same period last year.

As shown in the following financial highlights chart, the company’s operating metrics show pressure on profitability despite some revenue growth on a year-to-date basis:

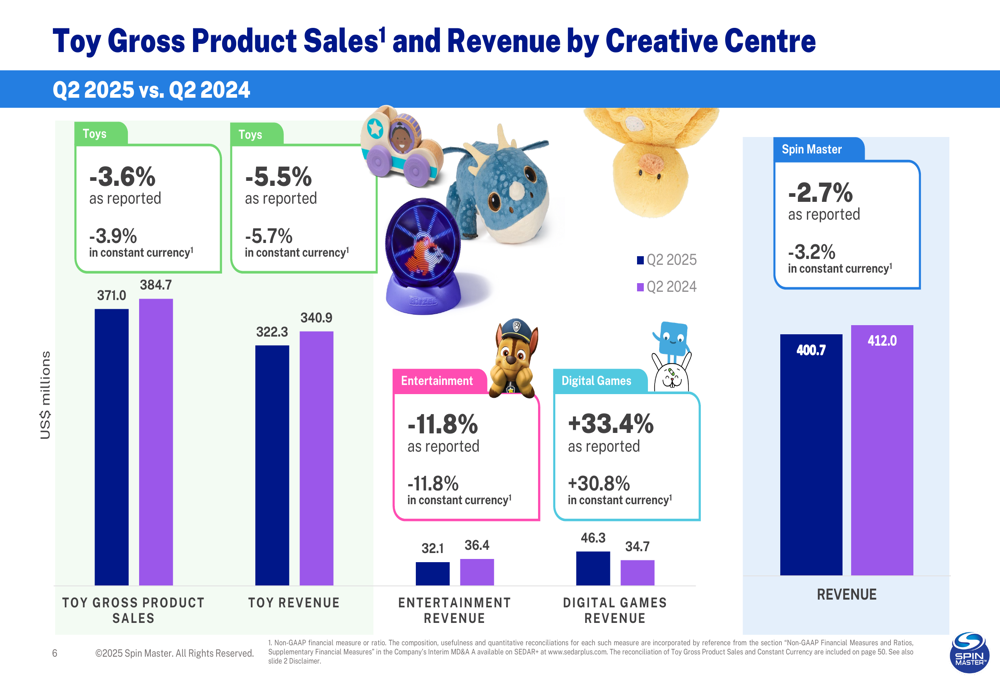

The company’s three creative centers showed divergent performance. Toy Gross Product Sales decreased by 3.6% to $371.0 million, Entertainment Revenue fell by 11.8% to $32.1 million, while Digital Games Revenue increased by 33.4% to $46.3 million compared to Q2 2024.

The following chart illustrates this mixed performance across Spin Master’s creative centers:

Detailed Financial Analysis

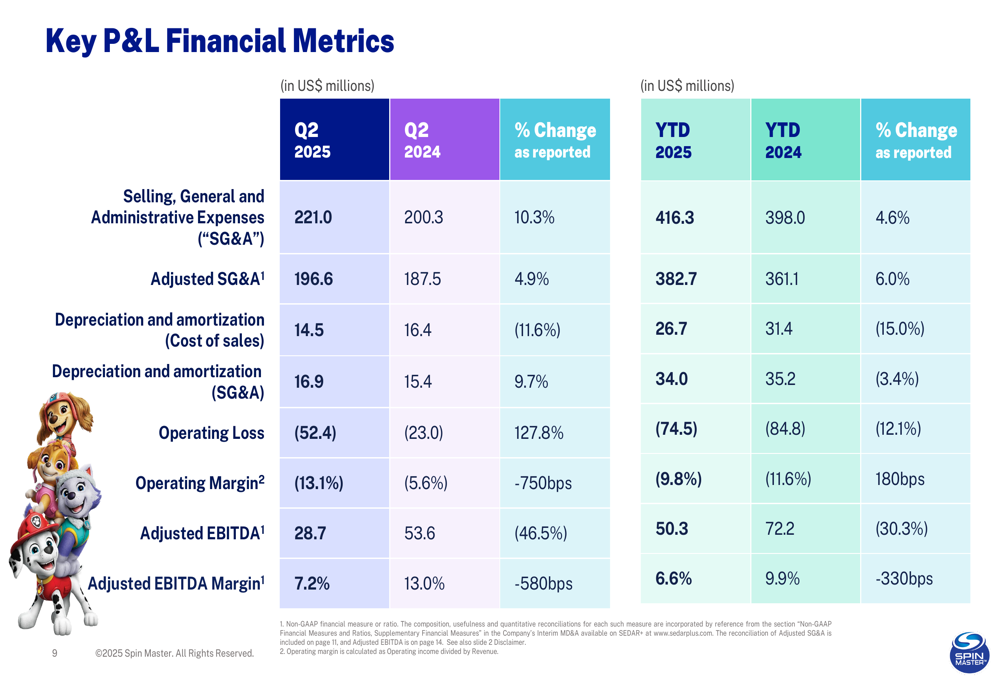

Despite the revenue decline, Spin Master’s gross margin improved to 52.4% in Q2 2025 compared to 48.4% in Q2 2024. However, adjusted gross margin (which excludes certain acquisition-related adjustments) declined to 52.4% from 54.3% in the prior year period.

The company’s operating expenses increased, with Selling, General and Administrative expenses rising to $221.0 million in Q2 2025 from $200.3 million in Q2 2024. This contributed to an operating loss of $52.4 million, compared to a loss of $23.0 million in the same period last year.

The following detailed P&L metrics provide further insight into the company’s financial performance:

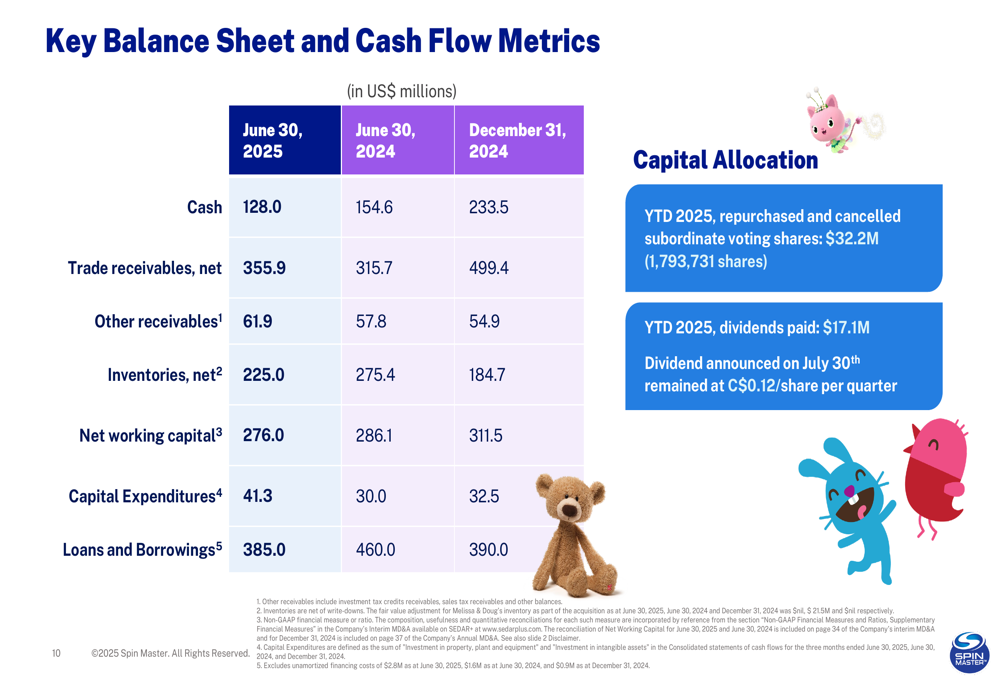

From a balance sheet perspective, Spin Master’s cash position decreased to $128.0 million as of June 30, 2025, down from $233.5 million at the end of 2024. The company maintained a net working capital of $276.0 million and reduced its loans and borrowings to $385.0 million from $390.0 million at year-end 2024.

The company’s capital allocation strategy included repurchasing and cancelling 1,793,731 subordinate voting shares worth $32.2 million and paying $17.1 million in dividends year-to-date. The quarterly dividend remained unchanged at C$0.12 per share.

Segment Analysis

Toys Segment

The Toys segment, which represents Spin Master’s largest business, reported an operating loss of $39.7 million in Q2 2025, with an operating margin of -12.3%. Adjusted EBITDA for the segment was -$0.7 million with a margin of -0.2%.

Performance varied significantly across toy categories. Preschool, Infant & Toddler and Plush increased by 12.1%, and Wheels & Action (WA:ACT) grew by 17.3% in Q2 2025. However, these gains were offset by declines in Outdoor (-39.5%) and Activities, Games & Puzzles and Dolls & Interactive (-31.7%).

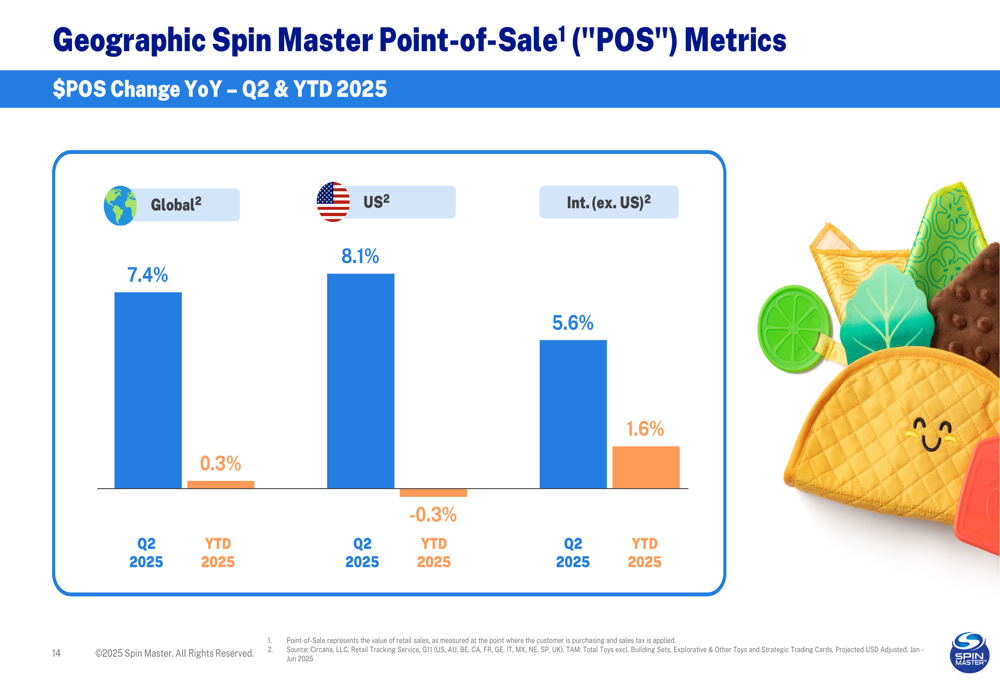

Despite the mixed category performance, Spin Master’s global point-of-sale (POS) metrics showed positive momentum, with global POS increasing by 7.4% in Q2 2025, though year-to-date growth was more modest at 0.3%.

Entertainment Segment

The Entertainment segment, which includes properties like PAW Patrol, reported revenue of $32.1 million in Q2 2025, down 11.8% compared to Q2 2024. Despite the revenue decline, the segment remained profitable with operating income of $15.7 million and an operating margin of 48.9%. Adjusted operating income was $17.7 million with a margin of 55.1%.

Digital Games Segment

The Digital Games segment emerged as the bright spot in Spin Master’s portfolio, with revenue increasing by 33.4% to $46.3 million in Q2 2025. Despite this strong revenue growth, the segment reported an operating loss of $15.5 million, though adjusted operating income was positive at $7.7 million with a margin of 16.6%.

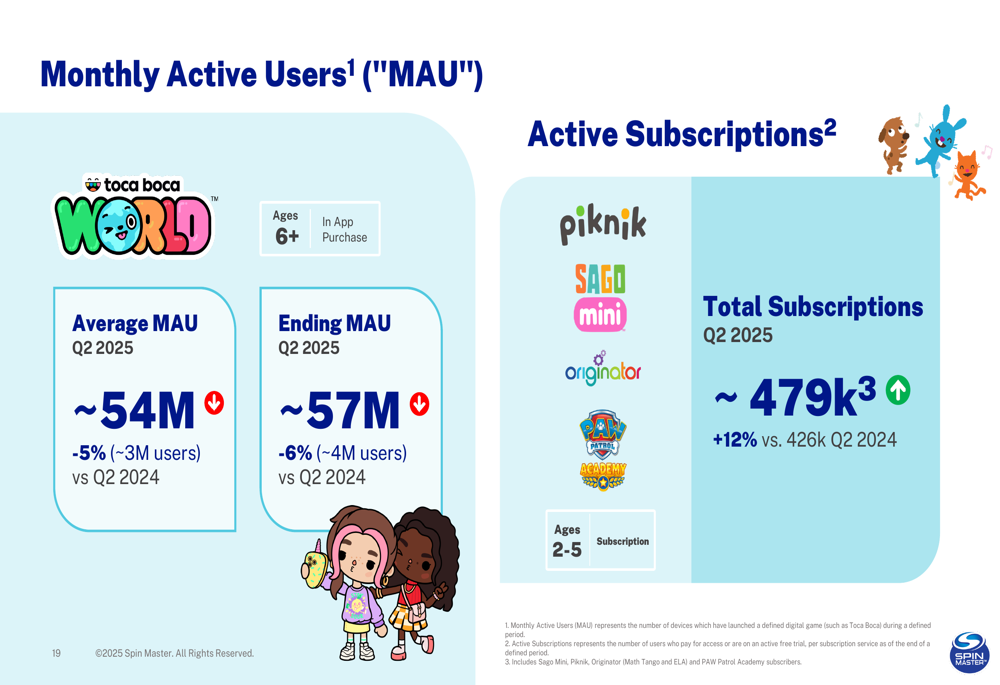

Monthly Active Users (MAU) for Toca Boca World, the company’s main digital game, averaged approximately 54 million in Q2 2025, representing a 5% decrease compared to Q2 2024. However, total subscriptions across digital properties grew by 12% to approximately 479,000, indicating improved monetization.

Strategic Initiatives

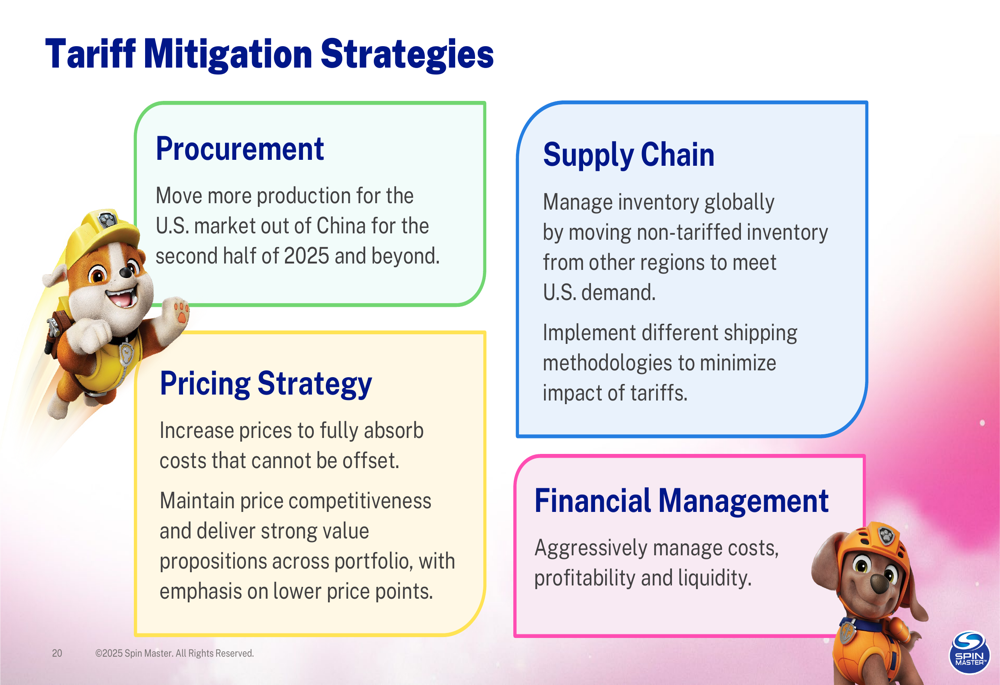

A significant focus of Spin Master’s presentation was on tariff mitigation strategies, highlighting the company’s response to global trade challenges. These strategies include diversifying procurement away from China, implementing strategic pricing, optimizing supply chain management, and enhancing financial management practices.

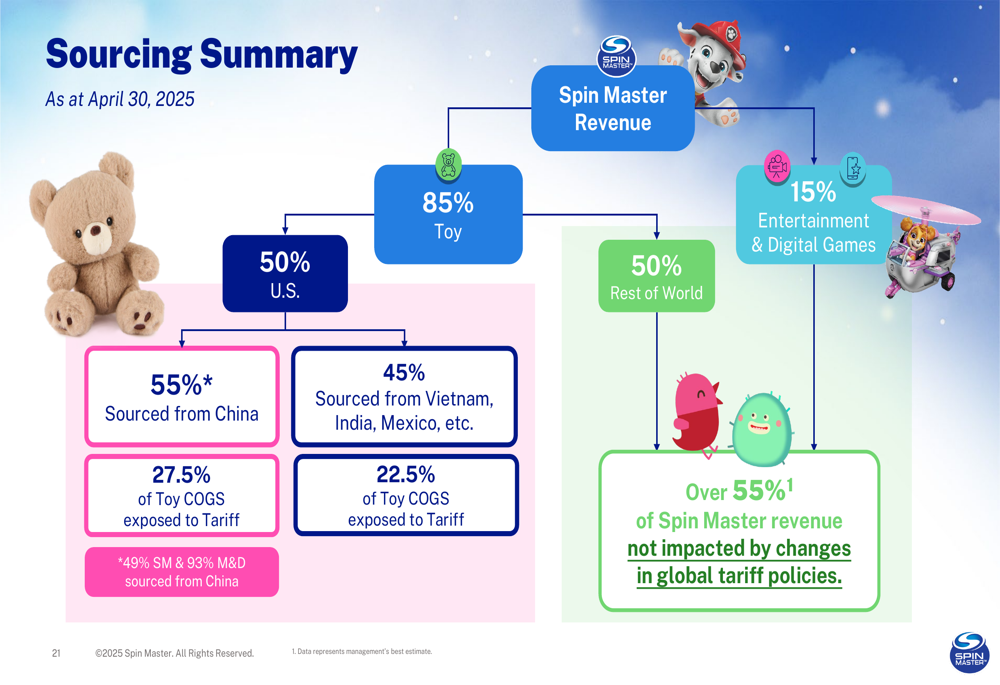

The company provided a detailed sourcing summary, noting that 55% of Spin Master’s revenue is not impacted by changes in global tariff policies. For the toy segment, which represents 85% of revenue, the company is working to reduce its exposure to tariffs by diversifying production locations.

Forward-Looking Statements

While Spin Master did not reinstate its previously withdrawn 2025 financial guidance, the presentation emphasized the company’s focus on mitigating tariff impacts and optimizing its global supply chain. The company is continuing its strategy of diversifying production outside of China, which aligns with statements made during Q1 earnings about targeting 70% of US market toys to be produced outside China by the end of 2025.

The company’s digital games segment represents a growing opportunity, with increasing subscription revenues offsetting some of the challenges in the traditional toy business. Meanwhile, the entertainment segment, despite revenue declines, continues to deliver strong margins and supports the broader toy ecosystem.

Spin Master’s mixed Q2 2025 results reflect both challenges and opportunities as the company navigates a complex global trade environment while continuing to innovate across its three creative centers. The strong performance in Digital Games demonstrates the value of the company’s diversified portfolio approach, even as it works to address headwinds in its core toy business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.