Street Calls of the Week

Introduction & Market Context

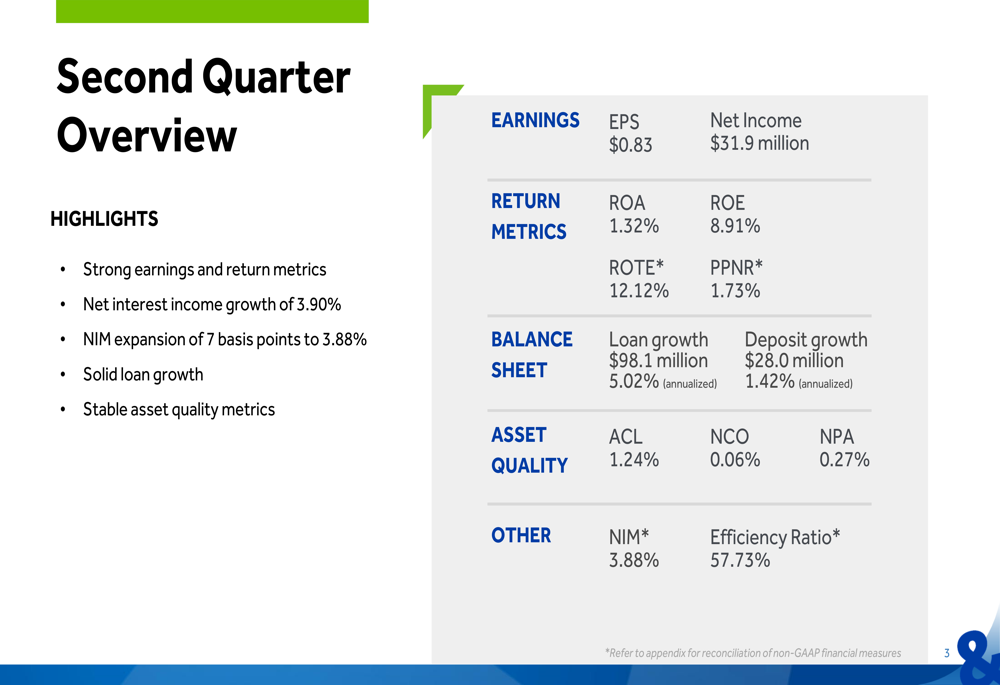

S&T Bancorp (NASDAQ:STBA) released its second quarter 2025 earnings presentation on July 24, highlighting solid performance driven by loan growth and net interest margin expansion. The Pennsylvania-based regional bank reported earnings per share (EPS) of $0.83 and net income of $31.9 million, representing a slight decline from the $0.87 EPS reported in the first quarter.

Despite this modest sequential EPS decline, the bank’s shares have remained relatively stable, trading near $38.62, reflecting investor confidence in the company’s fundamentals and growth trajectory. The bank continues to demonstrate resilience in a challenging economic environment, with improving asset quality and a strong capital position.

Quarterly Performance Highlights

S&T Bancorp delivered solid financial results for the second quarter of 2025, with several key metrics showing improvement. The bank reported return on assets (ROA) of 1.32%, return on equity (ROE) of 8.91%, and return on tangible equity (ROTE) of 12.12%.

As shown in the following comprehensive overview of the quarter’s performance, the bank achieved notable growth in both loans and deposits while maintaining strong asset quality:

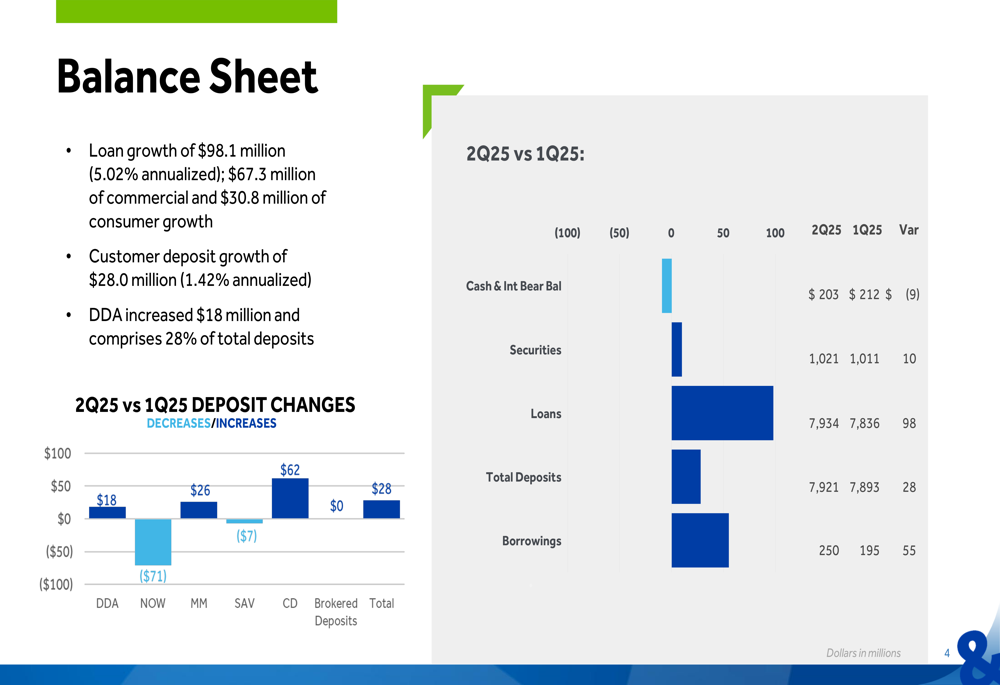

Loan growth was particularly strong at $98.1 million (5.02% annualized), comprised of $67.3 million in commercial loans and $30.8 million in consumer loans. Customer deposits also increased by $28.0 million (1.42% annualized), with demand deposits (DDA) rising by $18 million to comprise 28% of total deposits.

The following balance sheet analysis illustrates these trends in detail:

Detailed Financial Analysis

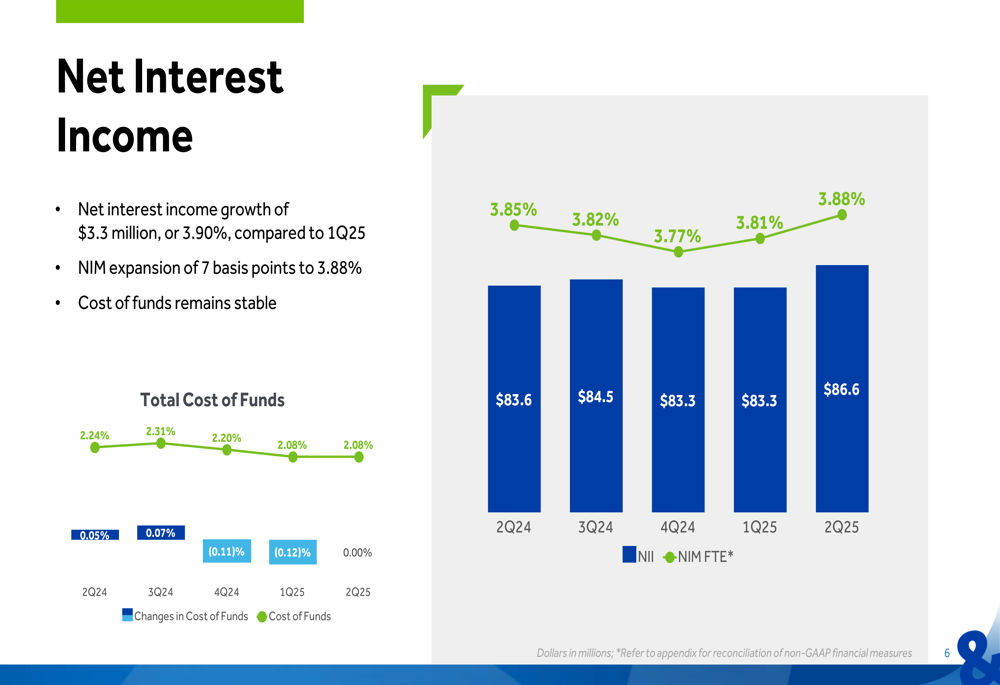

Net interest income, a critical revenue driver for banks, grew by $3.3 million or 3.90% compared to the first quarter of 2025, reaching $86.6 million. The net interest margin (NIM) expanded by 7 basis points to 3.88%, continuing a positive trend from previous quarters. Importantly, the cost of funds remained stable at 2.08%, helping to support margin expansion.

The following chart illustrates the bank’s net interest income growth and stable cost of funds:

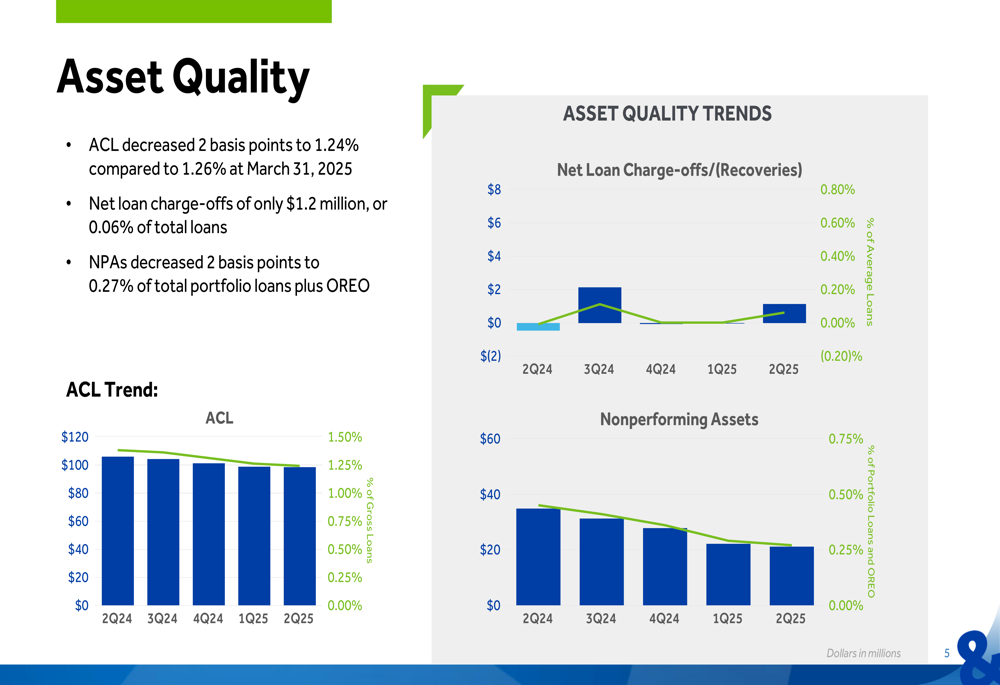

Asset quality continued to improve, with nonperforming assets (NPAs) decreasing by 2 basis points to 0.27% of total portfolio loans plus other real estate owned (OREO). The allowance for credit losses (ACL) stood at 1.24%, slightly down from 1.26% in the previous quarter, while net loan charge-offs remained minimal at $1.2 million, or 0.06% of total loans.

The following charts demonstrate the bank’s improving asset quality trends:

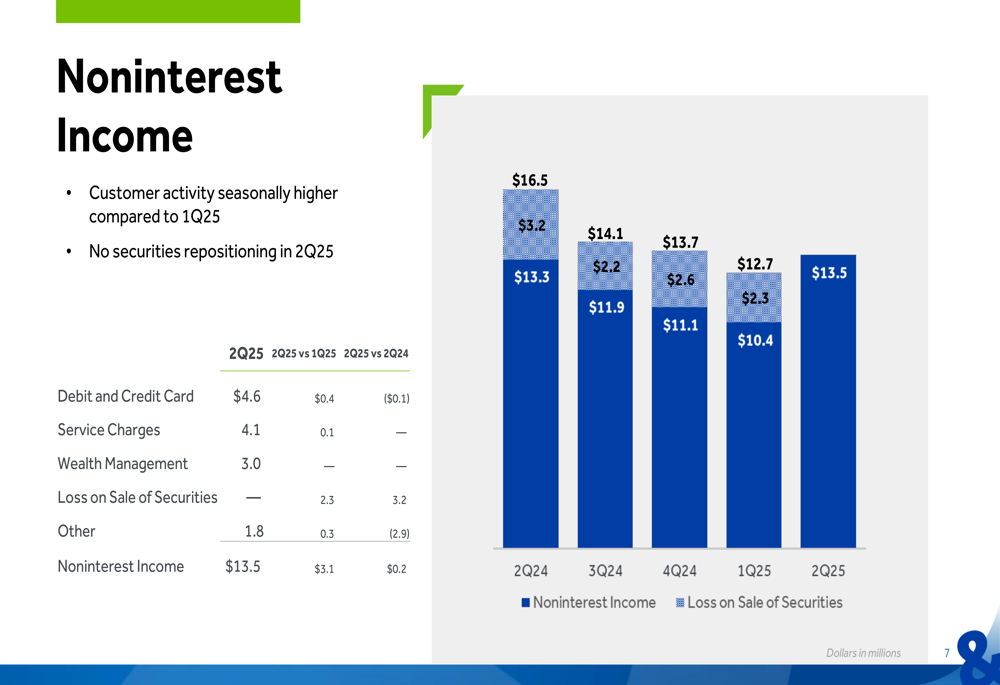

Noninterest income increased significantly to $13.5 million in Q2 2025, up from $10.4 million in Q1 2025. This improvement was driven by seasonally higher customer activity and the absence of securities repositioning losses that had impacted previous quarters.

As shown in the following breakdown of noninterest income sources:

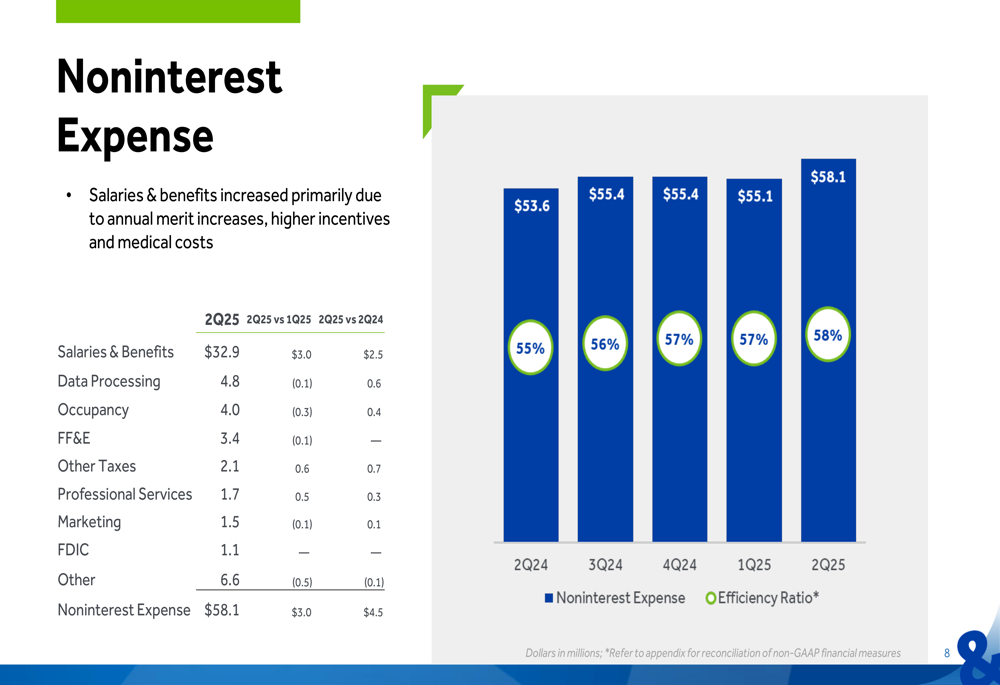

However, noninterest expenses also increased, rising to $58.1 million from $55.1 million in the previous quarter. This 5.4% increase was primarily attributed to higher salaries and benefits due to annual merit increases, higher incentives, and increased medical costs. The efficiency ratio consequently rose to 58%, continuing an upward trend from 55% in Q2 2024.

The following chart details the bank’s noninterest expense components and efficiency ratio:

Strategic Initiatives

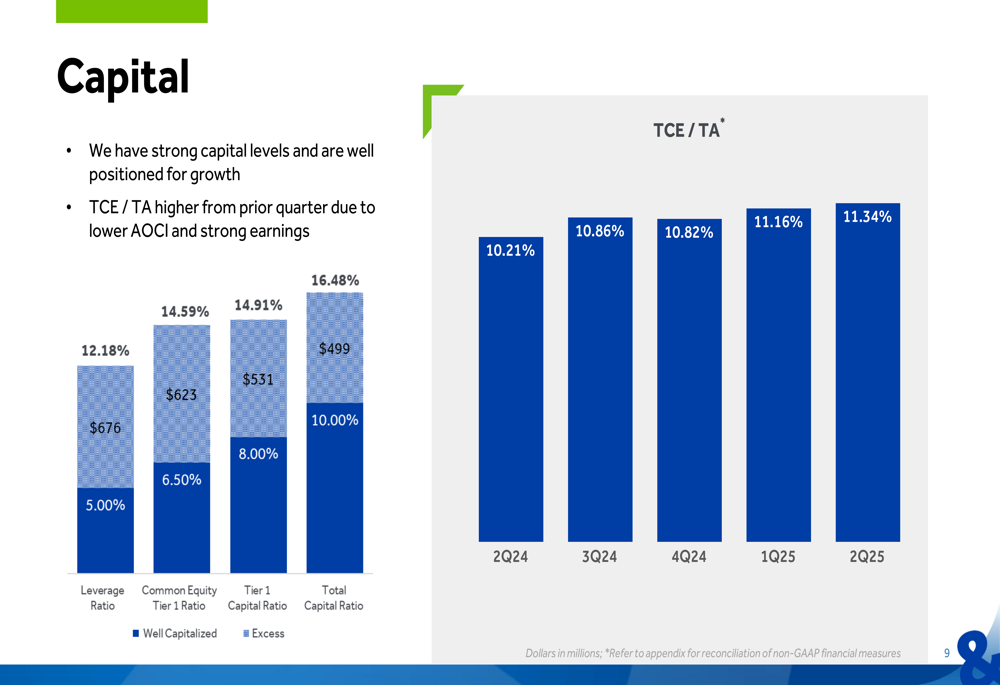

S&T Bancorp maintains a strong capital position, well above regulatory requirements, providing a solid foundation for continued growth. The tangible common equity to tangible assets (TCE/TA) ratio improved to 11.34% from 11.16% in the previous quarter, benefiting from lower accumulated other comprehensive income (AOCI) and strong earnings.

The following capital position overview demonstrates the bank’s strong capital levels:

This robust capital position aligns with the bank’s previously stated expectation to cross $10 billion in assets in the second half of 2025, as mentioned in their Q1 earnings call. The current asset level of $9.81 billion indicates steady progress toward this milestone.

Forward-Looking Statements

Based on current trends and the information presented in the Q2 2025 slides, S&T Bancorp appears well-positioned for continued growth. The bank’s strong loan growth, expanding net interest margin, and improving asset quality provide a solid foundation for future performance.

While rising noninterest expenses and the resulting increase in the efficiency ratio bear watching, the bank’s overall financial health remains strong. The stable cost of funds amid a changing interest rate environment is particularly noteworthy and suggests effective balance sheet management.

The bank’s previous guidance from Q1 indicated expectations for low to mid-single-digit loan growth in the first half of 2025 and high mid-single-digit growth in the second half. The Q2 results, with 5.02% annualized loan growth, align with these projections and suggest the bank is on track to meet its full-year growth targets.

As S&T Bancorp approaches the $10 billion asset threshold, investors should monitor potential regulatory changes and associated compliance costs that typically accompany this milestone for financial institutions. However, the bank’s strong capital position provides flexibility to navigate these challenges while continuing to pursue both organic and potential inorganic growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.