TSX up after index logs fresh record high close

Introduction & Market Context

Stagwell Inc. (NASDAQ:STGW) shares surged 10.56% following its second quarter 2025 earnings presentation on July 31, as investors responded positively to the company’s digital transformation strategy and steady financial performance. The marketing services company reported revenue of $707 million, slightly exceeding analyst expectations of $699.86 million, while adjusted earnings per share met forecasts at $0.17.

The company’s presentation emphasized its strategic pivot toward artificial intelligence and technology integration, positioning itself as a digital-first marketing services provider in an increasingly competitive landscape.

Quarterly Performance Highlights

Stagwell reported total net revenue of $598 million for Q2 2025, representing an 8% year-over-year increase. Adjusted EBITDA reached $93 million with a margin of 15.5%, maintaining the same margin level as Q2 2024. The company highlighted significant improvement in cash flow operations, which improved by $122 million compared to the first half of 2024.

As shown in the following quarterly highlights:

While total growth was solid at 8%, organic revenue growth was modest at just 0.6% for the quarter, with acquisitions contributing 6.7% to the overall growth. This indicates that Stagwell’s expansion strategy is currently more dependent on acquisitions than organic business development.

The company’s performance varied significantly by geography, with the United States showing a slight organic decline of 0.2%, the United Kingdom (TADAWUL:4280) declining by 7.7%, while "Other" locations demonstrated strong 10.1% organic growth. When excluding advocacy business, which can be cyclical, total organic growth improved to 2.0%.

Digital Transformation Strategy

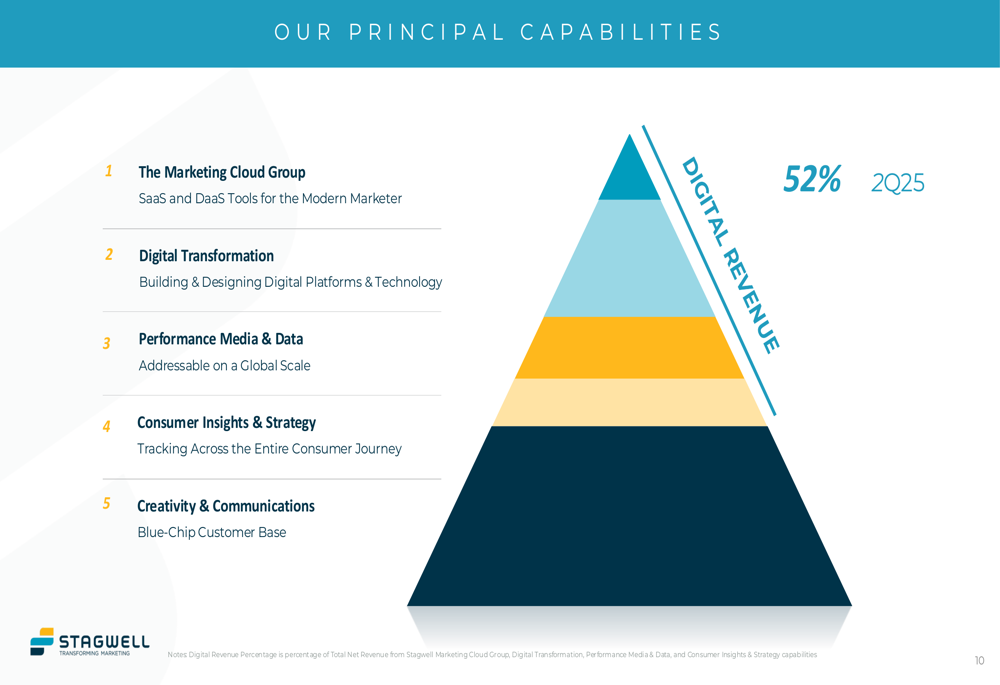

Stagwell’s presentation emphasized its positioning as a digital-first marketing services provider, with digital revenue now accounting for 52% of total revenue in Q2 2025. The company outlined its principal capabilities across five key areas, with particular focus on its digital offerings.

The following slide illustrates Stagwell’s business structure and digital revenue percentage:

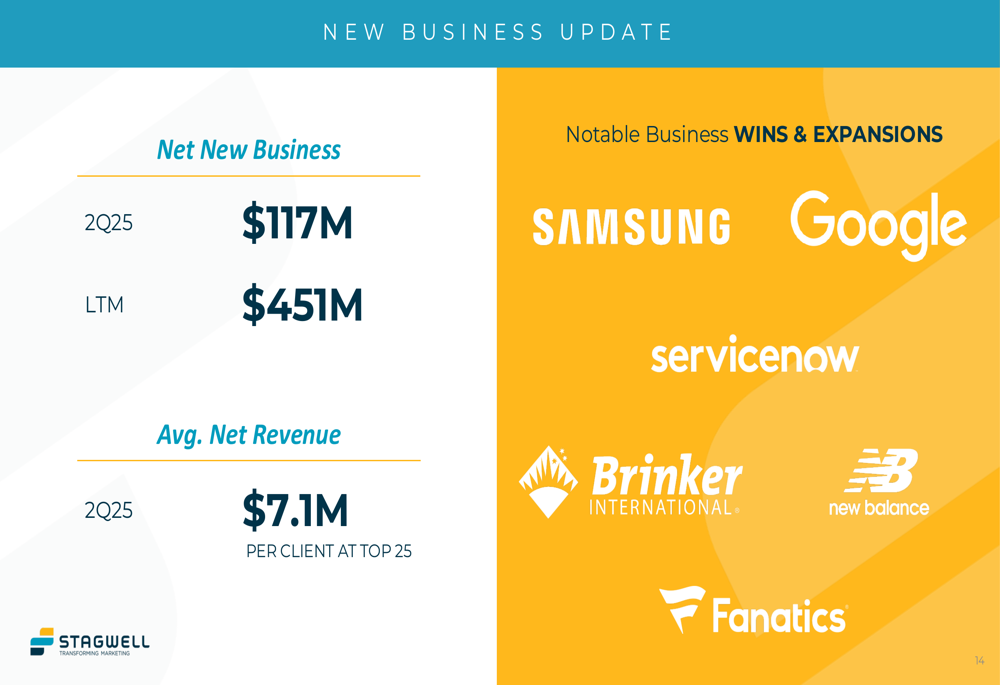

The company’s new business momentum remains strong, with $117 million in net new business secured during Q2 2025, bringing the last twelve months total to $451 million. Notable client wins include major technology and consumer brands such as Samsung (KS:005930), Google (NASDAQ:GOOGL), ServiceNow (NYSE:NOW), and New Balance.

As illustrated in the new business update:

CEO Mark Penn emphasized during the earnings call that "While digital transformation of other companies is lagging, ours is booming," highlighting the company’s focus on AI-native marketing solutions as a competitive differentiator.

Marketing Cloud Group Focus

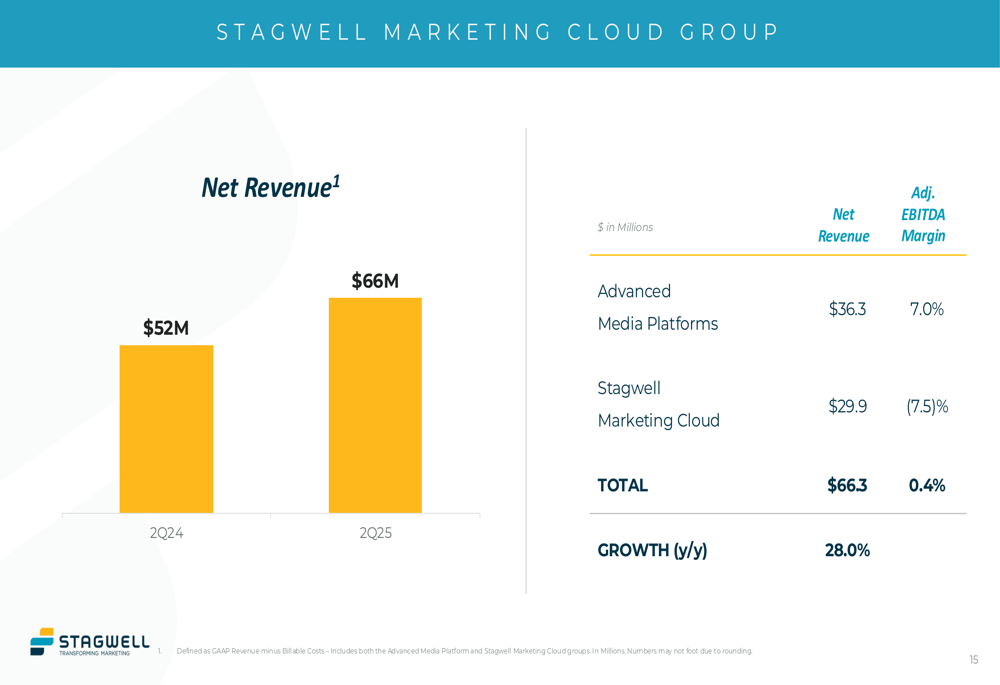

A central theme of Stagwell’s presentation was its strategic emphasis on the Marketing Cloud Group, which showed strong revenue growth of 28% year-over-year, reaching $66.3 million in Q2 2025. However, this segment faces profitability challenges with an adjusted EBITDA margin of just 0.4%.

The following chart details the Marketing Cloud Group’s performance:

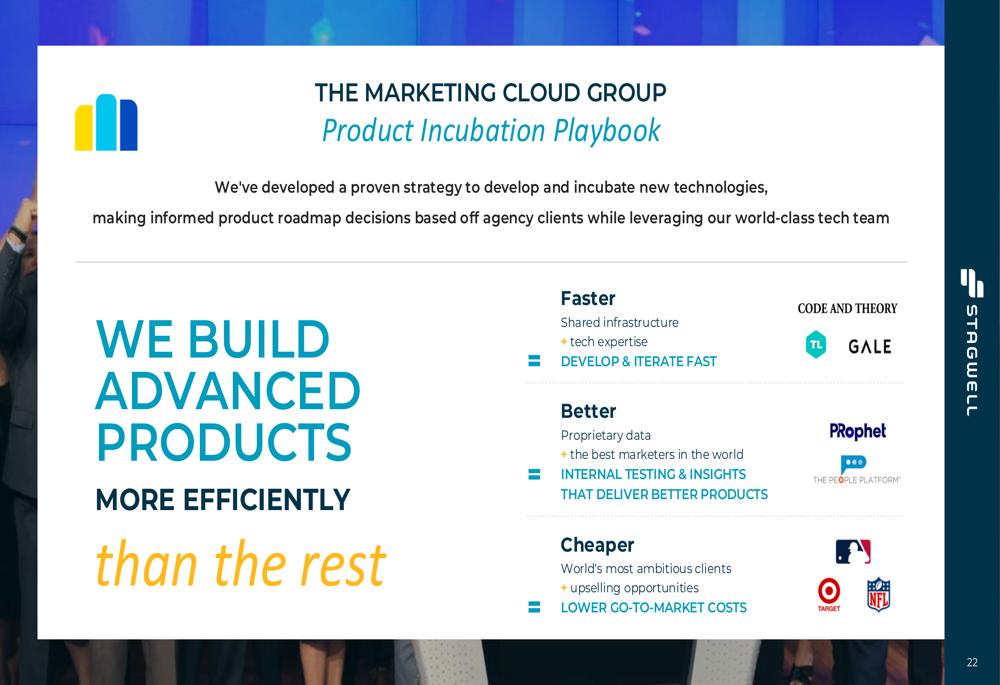

Stagwell outlined its strategy for scaling this division through a combination of digital services and technology products. The company is applying lessons learned from its digital transformation business to create a more efficient product development cycle.

As shown in the company’s strategic approach:

The presentation showcased several technology products being developed within the Marketing Cloud Group, including Harris QuestBrand for real-time consumer insights, PRophet Earn for AI-assisted public relations, and Around for augmented reality experiences in sports and entertainment venues.

The company’s product incubation strategy emphasizes faster development, better products through internal testing, and lower go-to-market costs:

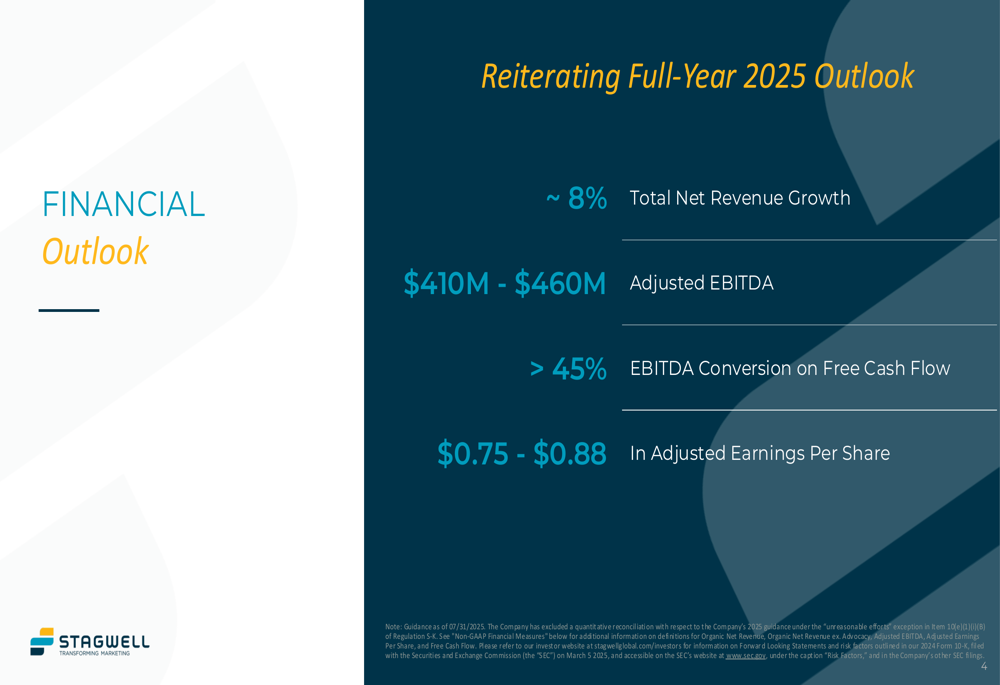

Financial Outlook & Guidance

Stagwell reaffirmed its full-year 2025 guidance, projecting approximately 8% total net revenue growth and adjusted EBITDA between $410 million and $460 million. The company expects adjusted earnings per share to range from $0.75 to $0.88, with EBITDA conversion on free cash flow exceeding 45%.

The following slide details the company’s full-year outlook:

The company’s financial position includes available liquidity of $539 million as of June 30, 2025, with a net leverage ratio of 3.18x. Management noted that deferred acquisition costs decreased by $10 million from the FY24 year-end balance, demonstrating discipline in managing acquisition-related expenses.

CFO Ryan Green emphasized during the earnings call that "Cash has been a primary focus for us," highlighting the importance of financial stability amid the company’s expansion efforts. The improvement in cash flow from operations by $122 million versus the first half of 2024 supports this focus.

Despite the positive market reaction, Stagwell faces challenges including a relatively high leverage ratio and modest organic growth. The company’s strategic bet on the Marketing Cloud Group also presents execution risks as it works to improve profitability in this segment while driving overall growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.