Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

Stainless Tankers ASA (STST) presented its second quarter 2025 results on August 6, revealing a cautiously optimistic outlook despite ongoing market challenges. The chemical tanker operator reported improved day rates quarter-over-quarter while maintaining its substantial dividend policy in a market characterized by slow recovery and geopolitical uncertainties.

The company’s stock closed at NOK 48 on August 5, up 0.63% ahead of the results announcement, trading well below its 52-week high of NOK 68.2 but above its 52-week low of NOK 44.9.

Quarterly Performance Highlights

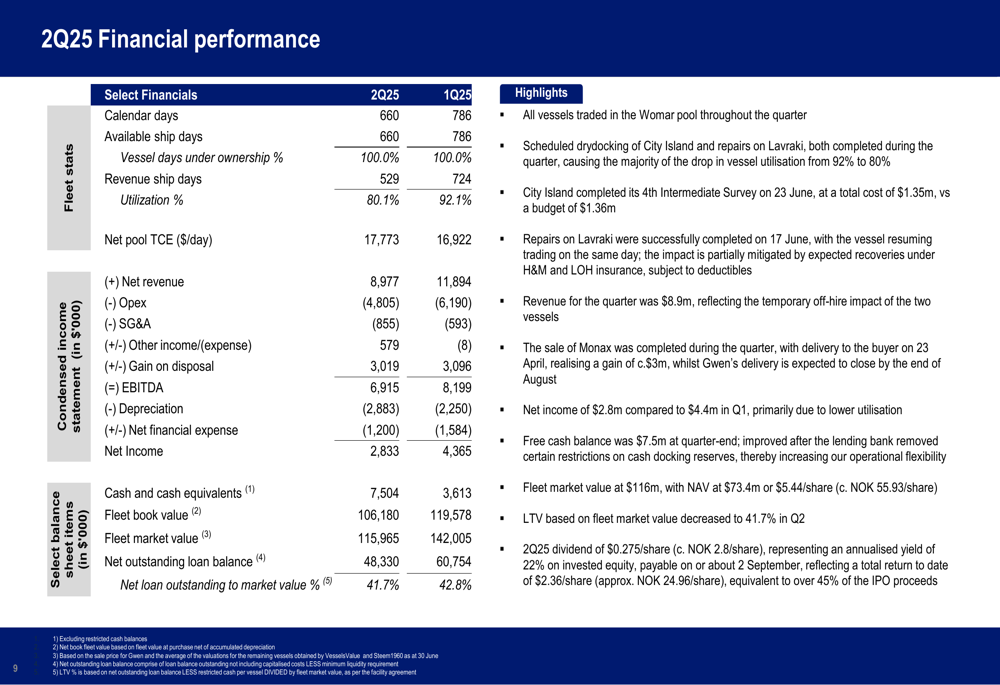

Stainless Tankers reported Q2 2025 EBITDA of $6.9 million and net income of $2.8 million on net revenue of $8.9 million. The company’s pool time charter equivalent (TCE) rates improved to $17,773 per day in Q2, up from $16,922 in the previous quarter, though still below budget expectations.

The company announced a Q2 2025 dividend of $0.275 per share (approximately NOK 2.8 per share), representing an annualized yield of 22%. Since its IPO, Stainless Tankers has returned $2.36 per share to investors, equivalent to over 45% of IPO proceeds.

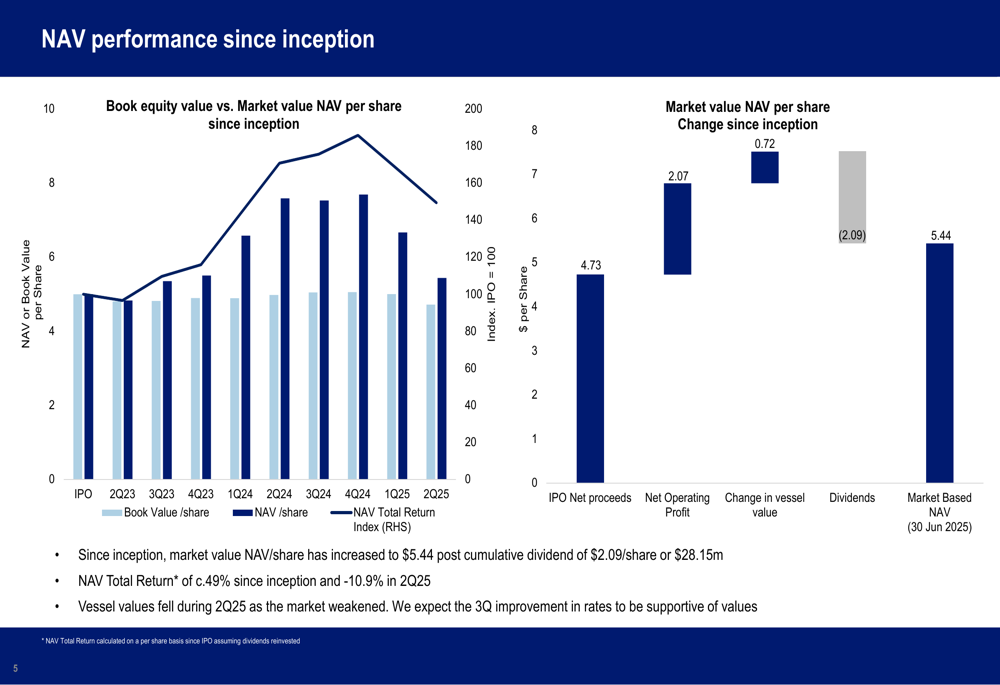

As shown in the following chart of NAV performance since inception, the company’s market value NAV per share has increased to $5.44 after cumulative dividends of $2.09 per share:

The company’s Net Asset Value (NAV) total return since inception stands at approximately 49%, despite a 10.9% decrease in Q2 2025 as vessel values declined amid weakening market conditions. The presentation highlighted that vessel values fell during the quarter as the overall market softened.

Financial Analysis

Stainless Tankers’ financial position remained solid in Q2 2025, with cash and cash equivalents increasing to $7.5 million from $3.6 million in Q1. The company’s fleet market value stood at $116 million, against a net outstanding loan balance of $48.3 million, resulting in a loan-to-value ratio of 41.7%, slightly improved from 42.8% in the previous quarter.

The detailed financial performance revealed some operational challenges, with vessel utilization dropping to 80.1% in Q2 from 92.1% in Q1, primarily due to scheduled drydocking of the vessel City Island and repairs on Lavraki. This contributed to the decline in net revenue from $11.9 million in Q1 to $9 million in Q2.

The following table presents the company’s comprehensive financial performance for the quarter:

Despite the reduced utilization, the company’s improved TCE rates helped offset some of the negative impact on revenue. The completion of vessel sales also contributed positively to the company’s cash position, with the sale of Monax completed during the quarter and Gwen’s delivery expected to close by the end of August.

Fleet Management and Strategy

Stainless Tankers continues to execute its fleet management strategy, balancing vessel sales with market opportunities. The Board has indicated its intention to make a partial return of capital to shareholders through a special dividend following the sale of Gwen, further demonstrating its commitment to shareholder returns.

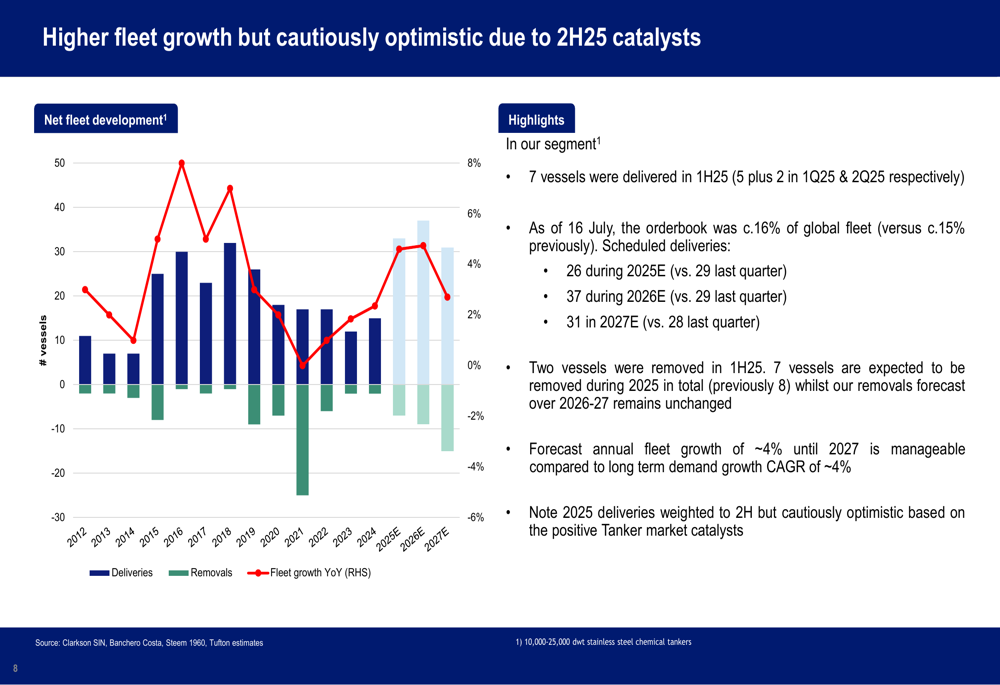

The company operates in a market with manageable fleet growth, as illustrated in the following chart:

The presentation highlighted that seven vessels were delivered in the first half of 2025, with an orderbook representing approximately 16% of the global fleet as of mid-July. Scheduled deliveries include 26 vessels during the remainder of 2025, 37 during 2026, and 31 in 2027. The company expects annual fleet growth of around 4% until 2027, which it considers manageable compared to long-term demand growth CAGR of 4%.

Market Outlook and Guidance

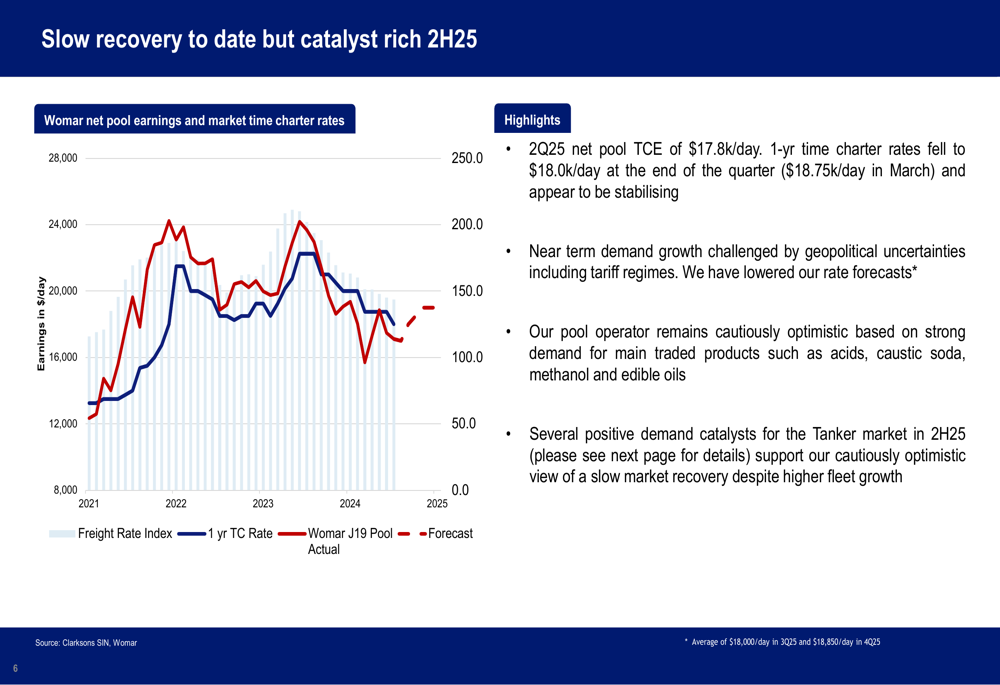

Stainless Tankers maintains a cautiously optimistic outlook for the remainder of 2025, despite acknowledging near-term demand growth challenges due to geopolitical uncertainties. The company expects full-year 2025 rates to average approximately $17,900 per day.

The market dynamics are illustrated in the following chart showing the slow recovery trajectory:

The company noted that July 2025 rates were slightly lower at $17,300 per day, but have recovered to around $17,800 per day in August. Several positive demand catalysts for the tanker market are expected in the second half of 2025, supporting the company’s cautiously optimistic view.

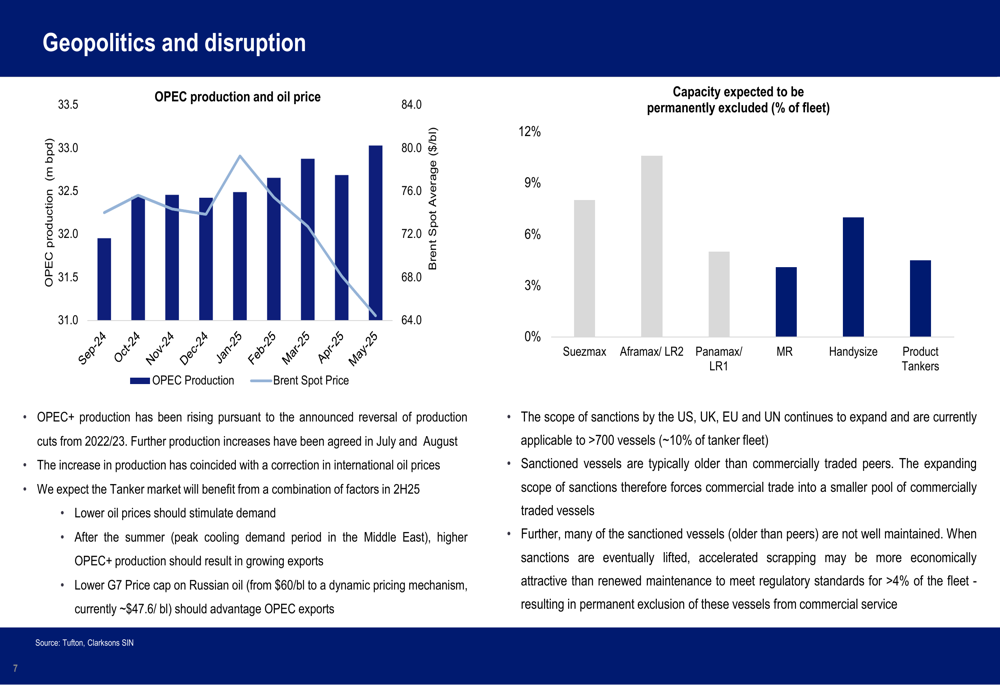

Geopolitical factors continue to influence the market, with OPEC+ production rising following the announced reversal of production cuts, and an expanding scope of sanctions by major global powers:

The company highlighted that sanctioned vessels are typically older than commercially traded peers and often not well maintained, which could potentially benefit operators of newer, well-maintained vessels like Stainless Tankers.

Despite the challenges, Stainless Tankers’ combination of steady dividend payments, manageable debt levels, and strategic vessel sales positions the company to navigate the current market environment while continuing to deliver value to shareholders through its industry-leading dividend yield.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.