Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Standard Motor Products Inc . (NYSE:SMP) released its first quarter 2025 financial results on April 30, showing substantial growth in both revenue and profitability. The automotive parts manufacturer’s stock responded positively, rising 11.25% to $27.10 following the announcement, as investors reacted to results that significantly exceeded analyst expectations.

The company reported diluted earnings per share of $0.81, representing a 68.75% beat compared to the forecasted $0.48 and an 80% increase from the $0.45 reported in the same period last year. This strong performance comes amid ongoing industry challenges, including supply chain pressures and economic uncertainties.

Quarterly Performance Highlights

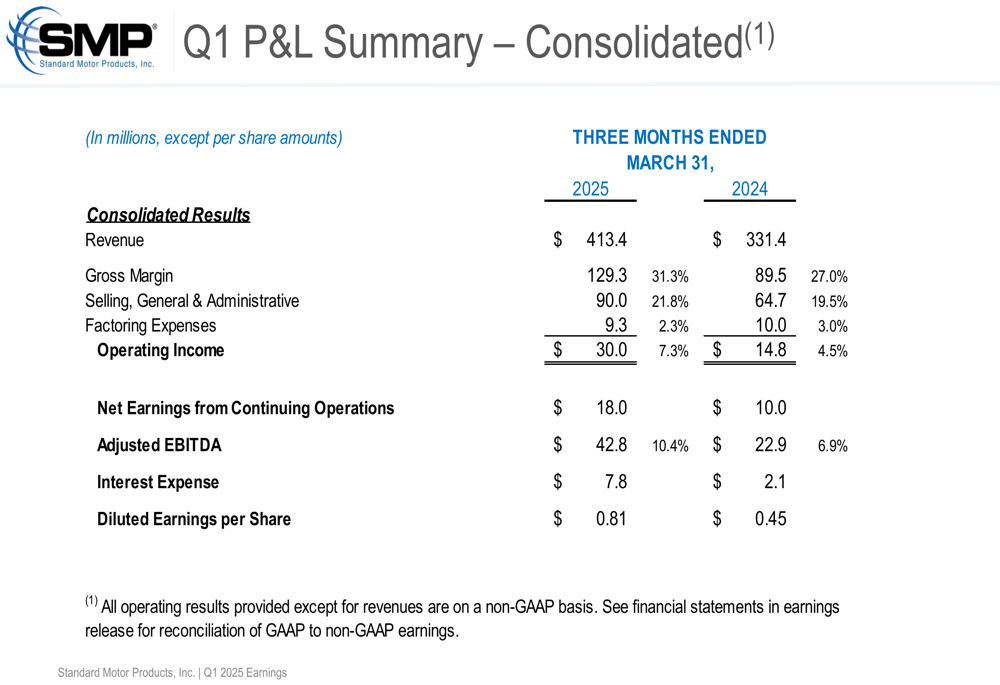

SMP’s consolidated revenue reached $413.4 million in Q1 2025, a 24.7% increase from $331.4 million in Q1 2024. This growth was accompanied by substantial margin expansion, with gross margin improving to 31.3% from 27.0% in the prior year period.

As shown in the following consolidated P&L summary, operating income grew to $30.0 million (7.3% of sales) from $14.8 million (4.5%) in Q1 2024, while net earnings from continuing operations increased to $18.0 million from $10.0 million:

The company’s adjusted EBITDA reached $42.8 million, representing 10.4% of sales compared to $22.9 million (6.9%) in the first quarter of 2024. However, interest expense increased significantly to $7.8 million from $2.1 million, reflecting the higher debt levels associated with recent acquisitions.

Segment Analysis

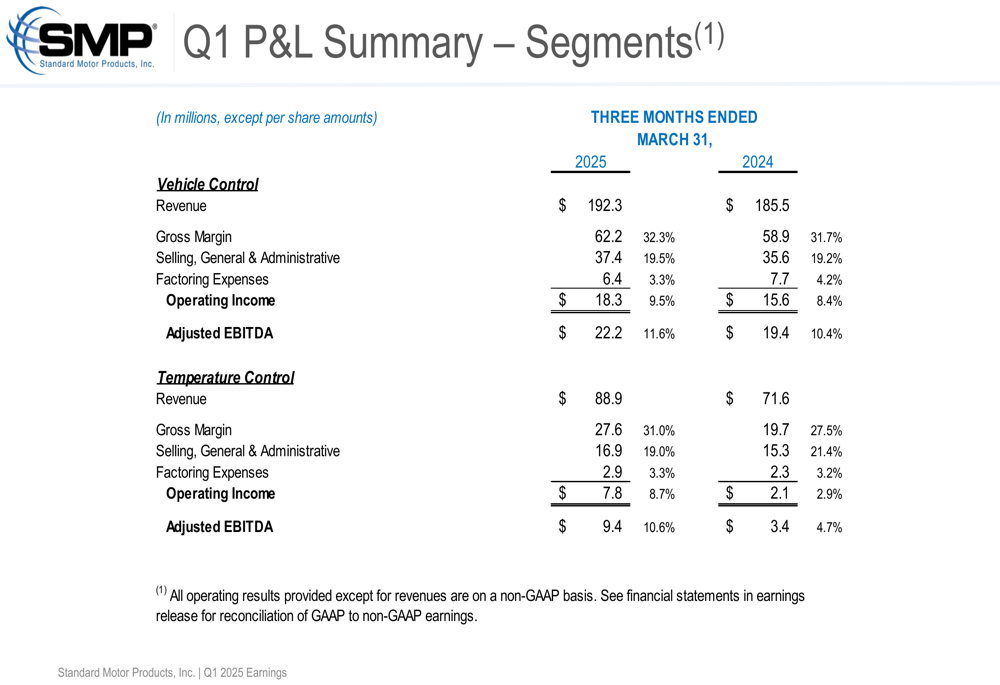

SMP’s performance varied across its business segments, with particularly strong results in Temperature Control and the newly acquired Nissens Automotive division. The Vehicle Control segment, which remains the company’s largest business unit, showed modest growth with revenue increasing 3.7% to $192.3 million and operating income rising to $18.3 million (9.5% margin) from $15.6 million (8.4% margin) in Q1 2024.

The following segment breakdown illustrates the performance of the Vehicle Control and Temperature Control divisions:

The Temperature Control segment demonstrated robust growth with revenue increasing 24.1% to $88.9 million and operating income more than tripling to $7.8 million (8.7% margin) from $2.1 million (2.9% margin). This significant improvement reflects both seasonal factors and operational efficiencies.

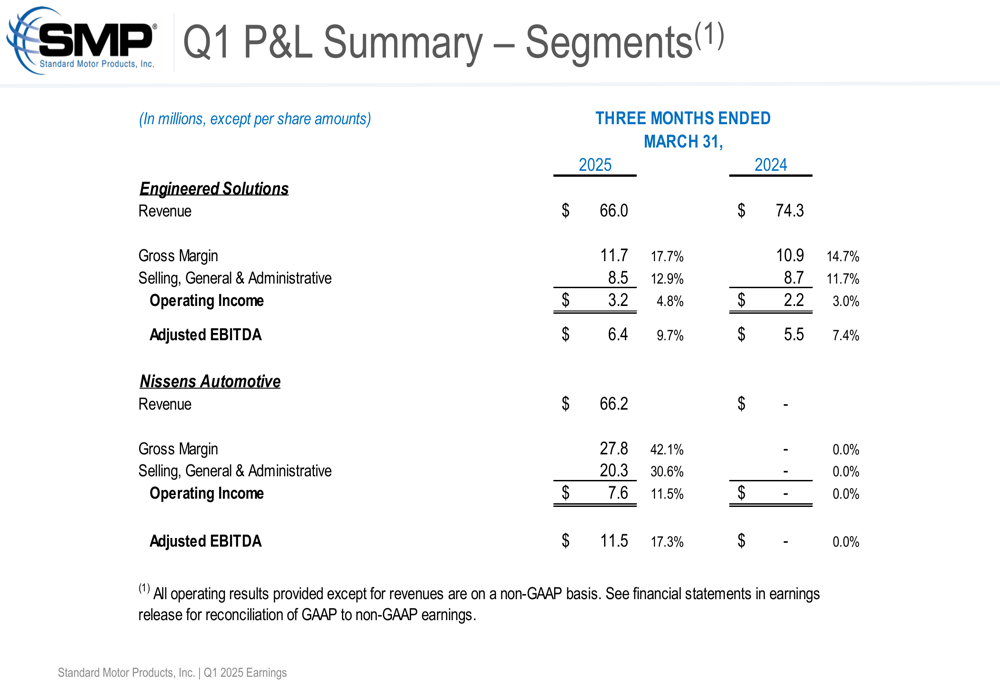

The Engineered Solutions segment was the only division to report a revenue decline, with sales falling 11.2% to $66.0 million. Despite this, the segment improved its profitability with operating income rising to $3.2 million (4.8% margin) from $2.2 million (3.0% margin) in the prior year period.

The performance of Engineered Solutions and the newly acquired Nissens Automotive segment is detailed below:

Nissens Automotive, acquired in late 2024, contributed $66.2 million in revenue with an impressive operating income of $7.6 million (11.5% margin) and adjusted EBITDA of $11.5 million (17.3% margin). This acquisition appears to be immediately accretive to SMP’s overall profitability.

Balance Sheet and Cash Flow

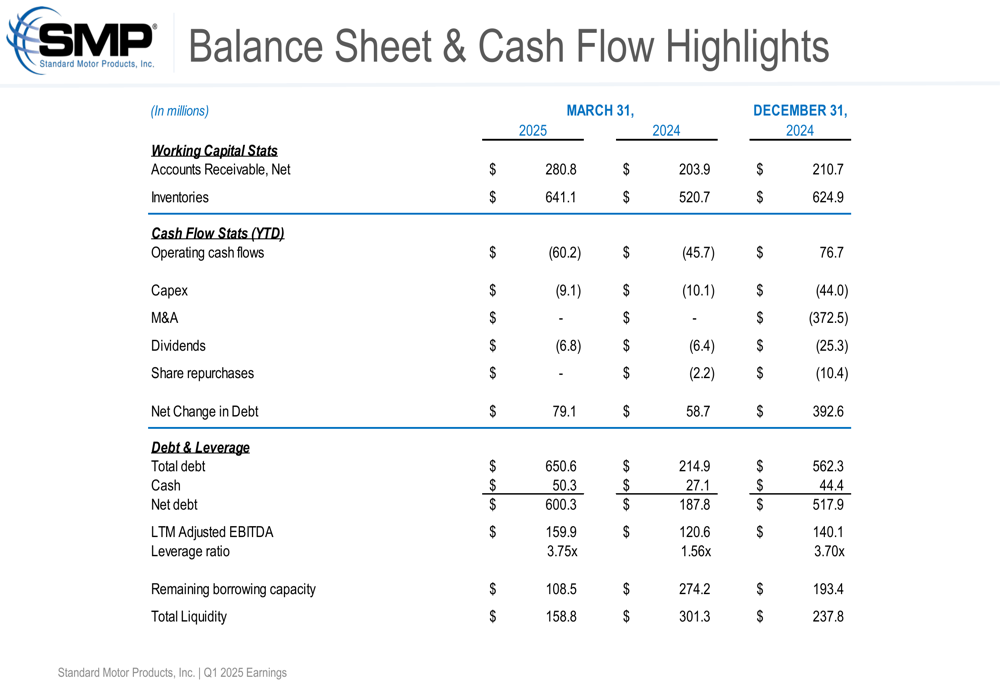

While SMP’s operational performance was strong, the company’s balance sheet reflects the significant impact of recent acquisitions. Total (EPA:TTEF) debt increased to $650.6 million as of March 31, 2025, compared to $214.9 million a year earlier. Net debt rose to $600.3 million from $187.8 million, resulting in a leverage ratio of 3.75x compared to 1.56x in the prior year.

The following balance sheet and cash flow highlights illustrate these changes:

Operating cash flow was negative $60.2 million for the quarter, compared to negative $45.7 million in Q1 2024, reflecting typical seasonal inventory build ahead of the summer selling season. Inventory levels increased to $641.1 million from $520.7 million a year earlier, partly due to the addition of Nissens Automotive.

Capital expenditures for the quarter were $9.1 million, slightly below the $10.1 million spent in Q1 2024. The company maintained its commitment to shareholder returns with dividend payments of $6.8 million during the quarter.

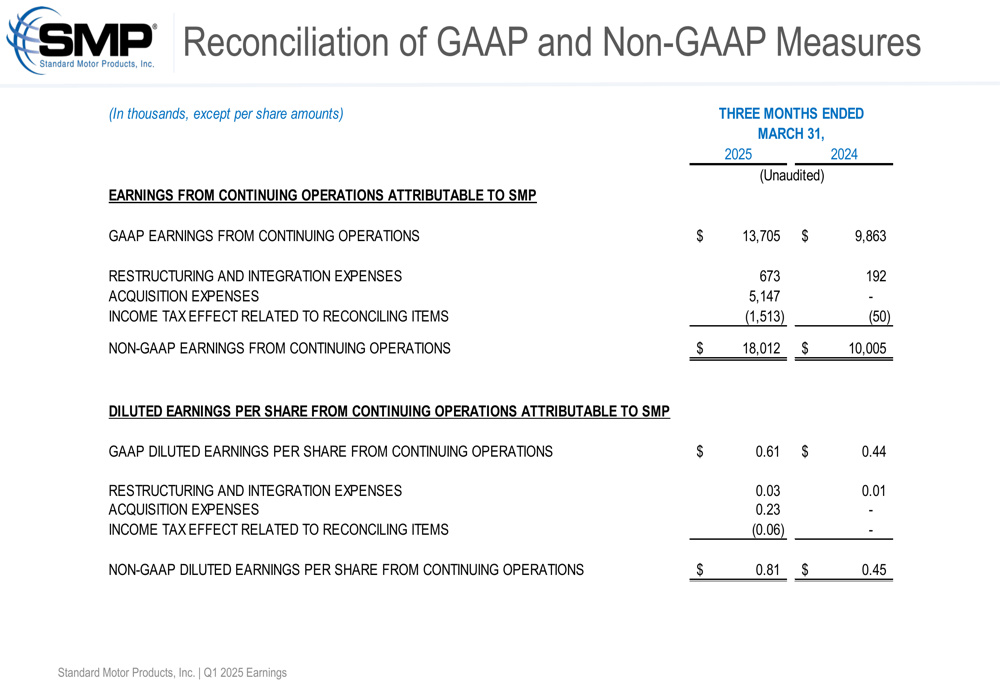

GAAP to Non-GAAP Reconciliation

SMP’s reported results include several non-recurring items, primarily related to acquisition and integration expenses. The reconciliation between GAAP and non-GAAP measures provides clarity on the company’s underlying performance:

The reconciliation shows that GAAP earnings from continuing operations were $13.7 million ($0.61 per diluted share), with acquisition expenses of $5.1 million representing the largest adjustment. After accounting for these special items, non-GAAP earnings from continuing operations were $18.0 million ($0.81 per diluted share).

Forward-Looking Statements

Based on the earnings call transcript, SMP expects net sales to grow in the mid-teens percentage range for the full year 2025, with an adjusted EBITDA margin of 10-11%. The company is focusing on realizing synergies from the Nissens acquisition and plans to pass through any tariff costs on a dollar-for-dollar basis.

CEO Eric Sills expressed confidence in the company’s competitive position, stating, "We believe that we have many structural underpinnings that will provide us with a relative advantage." He also highlighted the resilience of the automotive aftermarket, noting that it "has been able to mute the impact of economic downturns and, in fact, tends to outperform."

While the company’s operational performance is strong, investors should monitor the elevated leverage ratio, which could limit financial flexibility if market conditions deteriorate. However, the consistent profitability improvement across segments suggests that SMP is successfully executing its growth strategy despite broader economic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.