Tonix Pharmaceuticals stock halted ahead of FDA approval news

StandardAero Inc (NYSE:SARO) reported strong second-quarter results on August 13, 2025, showcasing double-digit growth across all business segments and prompting management to raise full-year guidance. The company’s aftermarket strength in commercial aerospace, business aviation, and military sectors continues to drive performance, despite ongoing supply chain challenges.

Quarterly Performance Highlights

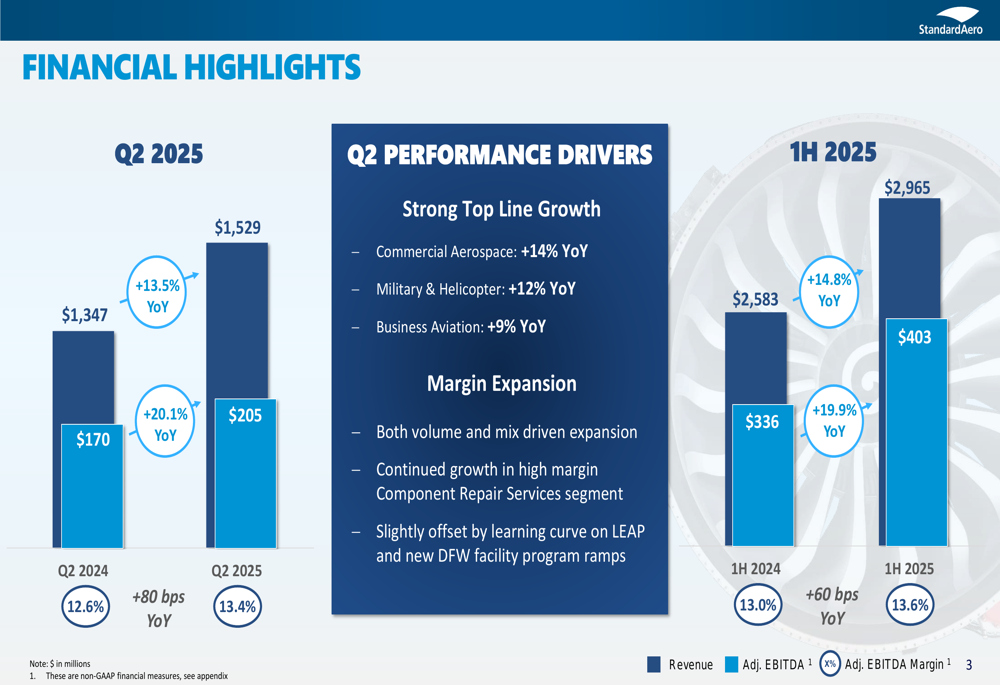

StandardAero delivered impressive financial results for Q2 2025, with revenue reaching $1,529 million, a 13.5% increase year-over-year. Adjusted EBITDA grew even faster at 20.1%, reaching $205 million, while adjusted EBITDA margin expanded by 80 basis points to 13.4%. Net income surged to $68 million, a substantial $62 million increase from the same period last year.

As shown in the following chart of quarterly financial performance:

The company’s growth was broad-based across all major market segments, with Commercial Aerospace leading at 14% year-over-year growth, followed by Military & Helicopter at 12%, and Business Aviation at 9%. This performance builds on the momentum seen in Q1 2025, when the company reported 16% year-over-year revenue growth.

"Our Q2 performance demonstrates continuing aftermarket strength driven by strong commercial aero demand, growth in business jet platforms, and AE1107 utilization recovery," the company noted in its presentation, while acknowledging that "persistent supply chain challenges" remain a factor in the market environment.

Segment Analysis

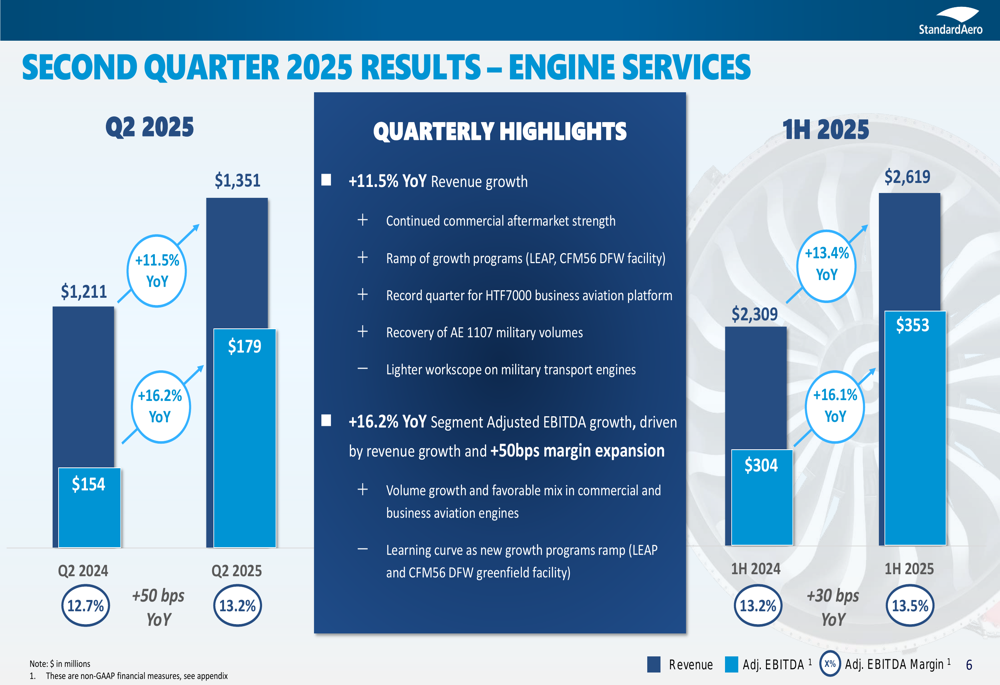

StandardAero’s Engine Services segment, which represents the bulk of the company’s business, reported revenue of $1,351 million, an 11.5% increase year-over-year. The segment’s adjusted EBITDA grew by 16.2%, with margin expansion of 50 basis points to 13.2%.

Key drivers for the Engine Services segment included continued commercial aftermarket strength, the ramp-up of growth programs including LEAP and the new CFM56 Dallas-Fort Worth facility, a record quarter for the HTF7000 business aviation platform, and recovery of AE1107 military volumes.

The segment’s performance is illustrated in the following chart:

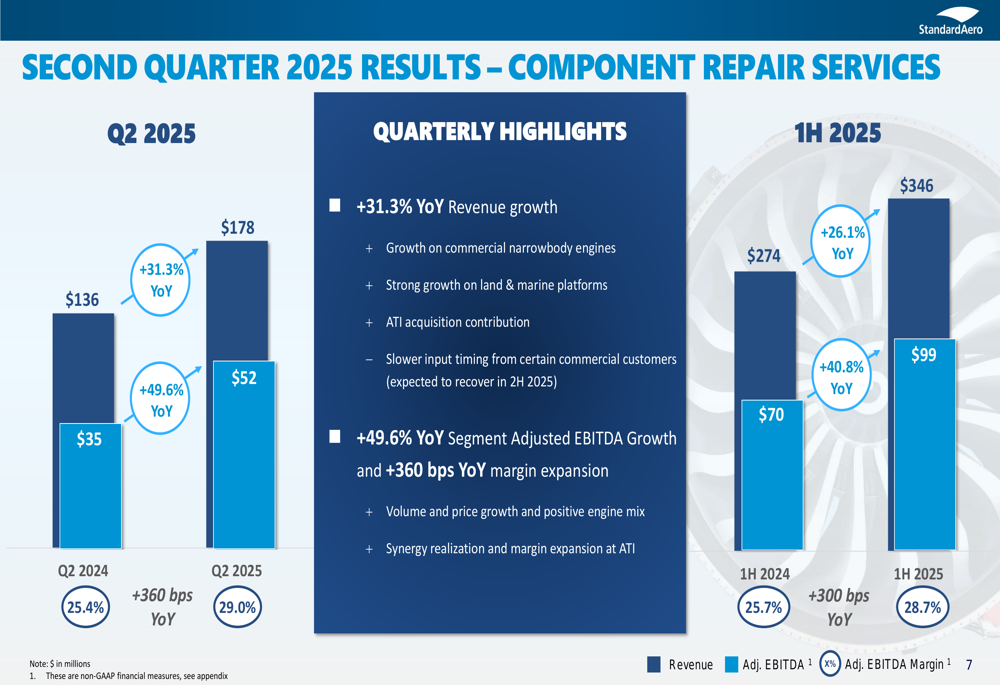

The Component Repair Services segment delivered even stronger results, with revenue increasing 31.3% year-over-year to $178 million. This segment achieved impressive profitability with an adjusted EBITDA margin of 29.0%, representing a substantial 360 basis point improvement from the prior year.

The following chart highlights the Component Repair Services segment’s exceptional performance:

Growth in this segment was attributed to increased activity on commercial narrowbody engines, strong performance in land and marine platforms, and contributions from the ATI acquisition. The company also noted volume and price growth, positive engine mix, and synergy realization at ATI as factors driving margin expansion.

Balance Sheet Improvements

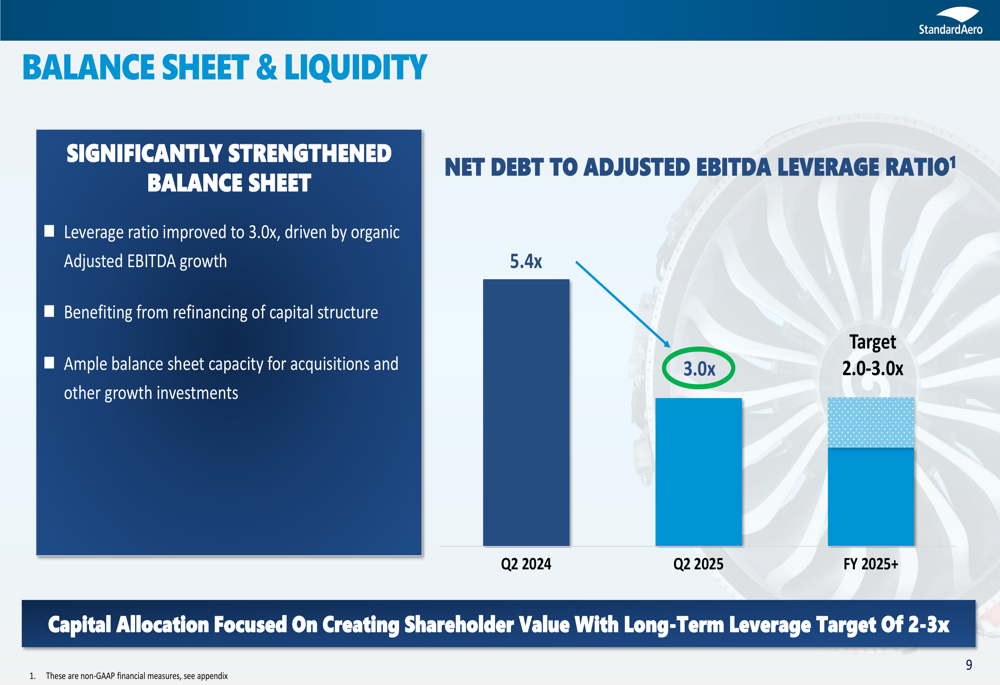

StandardAero has significantly strengthened its balance sheet, with its net debt to adjusted EBITDA leverage ratio improving to 3.0x from 5.4x in Q2 2024. This improvement was driven by organic adjusted EBITDA growth and benefits from refinancing of the company’s capital structure.

The following chart illustrates this substantial improvement in financial leverage:

The company emphasized that its capital allocation strategy remains focused on creating shareholder value, with a long-term leverage target of 2-3x. Management noted that the improved balance sheet provides "ample capacity for acquisitions and other growth investments."

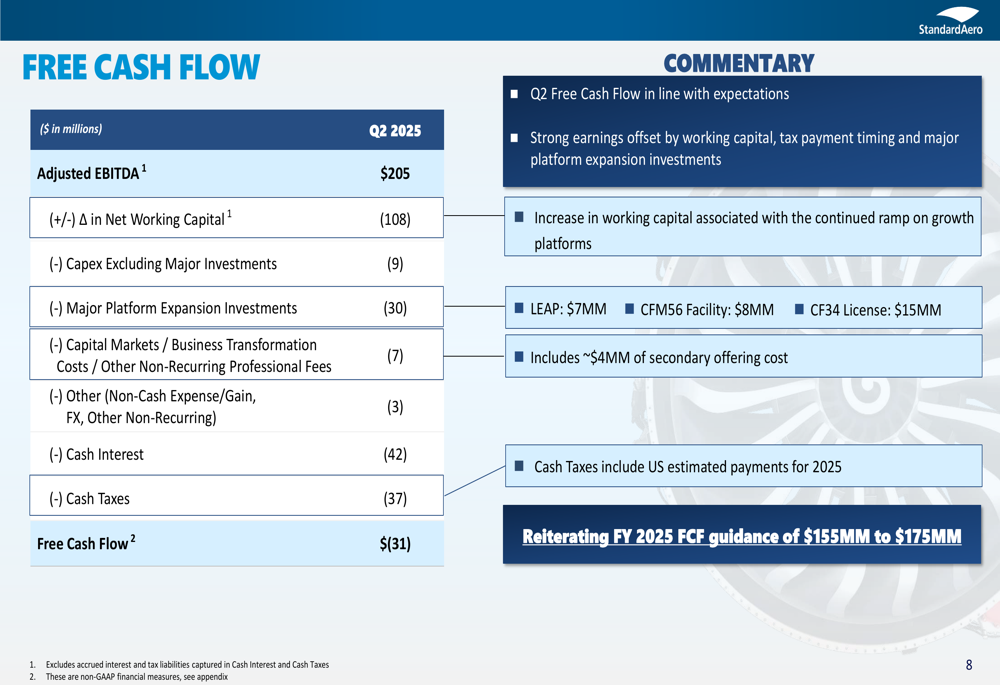

Despite reporting negative free cash flow of $31 million for the quarter, the company indicated this was in line with expectations, reflecting higher earnings offset by working capital needs, tax payment timing, and major platform expansion investments.

The free cash flow breakdown is detailed in the following chart:

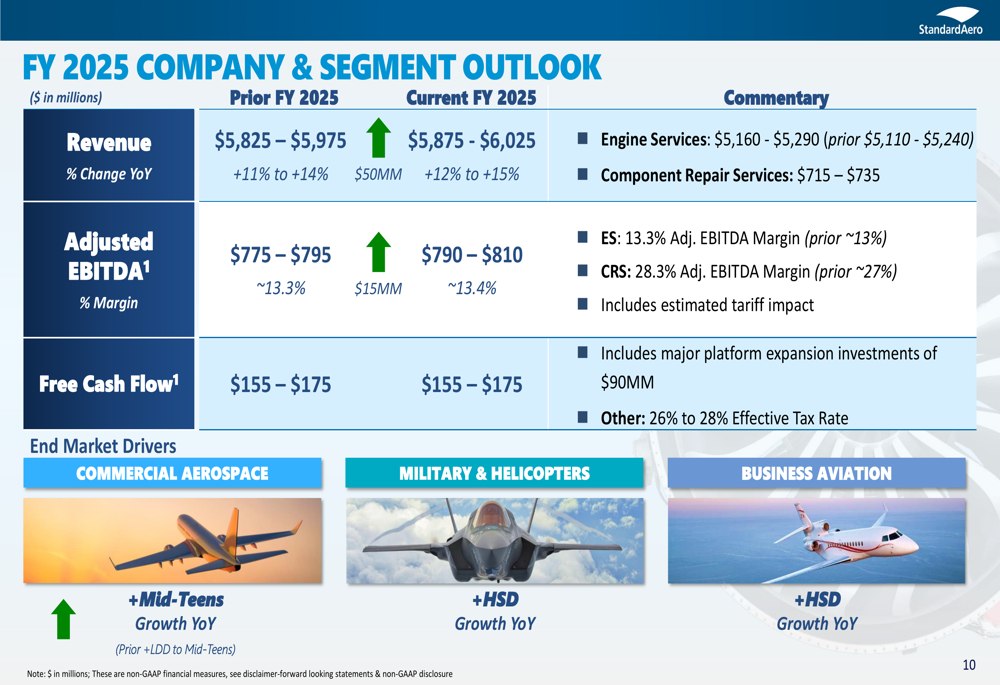

Updated 2025 Outlook

Based on strong first-half performance, StandardAero raised its full-year 2025 guidance. The company now projects revenue of $5,875-$6,025 million, representing 12-15% year-over-year growth, up from the previous guidance of $5,825-$5,975 million.

Adjusted EBITDA guidance was also increased to $790-$810 million (approximately 13.4% margin), compared to the prior guidance of $775-$795 million. The company maintained its free cash flow guidance of $155-$175 million.

The updated outlook is presented in the following chart:

By segment, Engine Services revenue is now expected to reach $5,160-$5,290 million with an adjusted EBITDA margin of 13.3%, while Component Repair Services is projected to generate $715-$735 million in revenue with an impressive 28.3% margin.

The company anticipates mid-teens growth in Commercial Aerospace, with high single-digit growth in both Military & Helicopters and Business Aviation segments.

Strategic Initiatives

StandardAero highlighted several strategic priorities that are driving current performance and positioning the company for future growth. The LEAP program continues to gain momentum, with revenue growing threefold quarter-over-quarter and more than $1.5 billion in LEAP wins to date.

The company is also capitalizing on recent investments, noting the first CFM56 Dallas-Fort Worth PRSV (Partial Restoration Service Visit) completed in the quarter, continued CFM56 wins, and the Augusta expansion.

As shown in the business highlights slide:

The expansion of Component Repair Services remains a strategic focus, with the segment delivering a record margin quarter. The company is developing new repairs and pursuing insourcing opportunities in this high-margin business.

StandardAero also emphasized its pursuit of accretive M&A opportunities, with ATI synergy realization progressing well and a strong M&A pipeline supported by the company’s improved balance sheet.

Following the earnings presentation, StandardAero’s stock price rose 0.31% to $28.76 in aftermarket trading, building on the positive momentum established after the company’s strong Q1 results earlier this year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.