TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

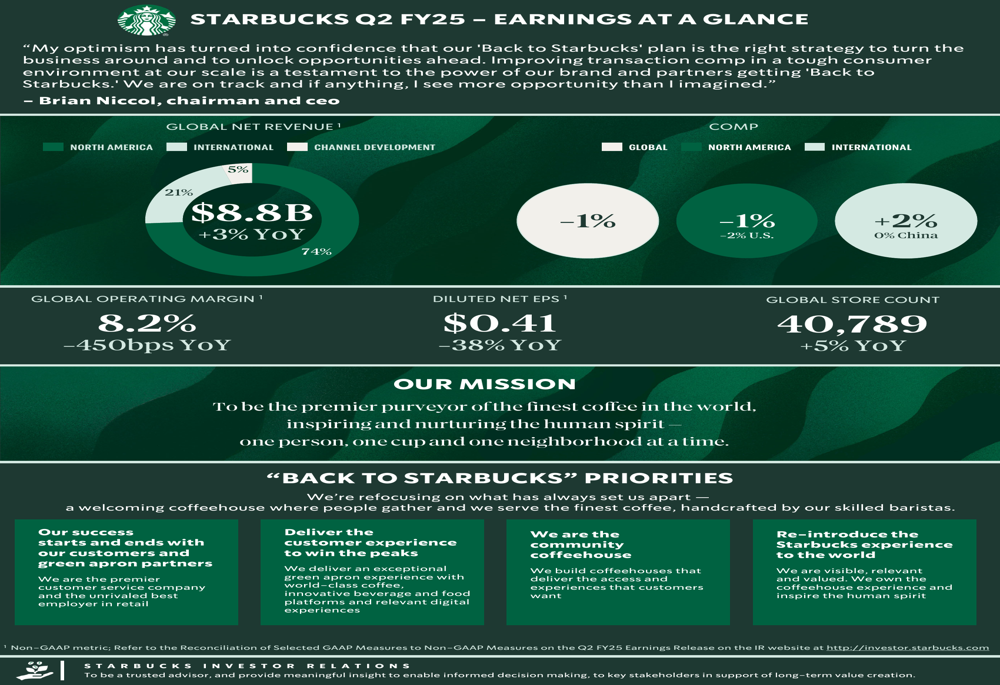

Starbucks Corporation (NASDAQ:SBUX) released its second-quarter fiscal year 2025 earnings presentation on April 29, highlighting modest revenue growth amid significant profitability challenges. The coffee giant’s shares traded at $83.90 at market close, with after-hours trading showing a 1.24% decline to $83.80, reflecting investor reaction to the mixed results.

The presentation marks a pivotal moment for Starbucks as new chairman and CEO Brian Niccol outlines his strategic vision through the "Back to Starbucks" plan, aimed at revitalizing the brand amid competitive pressures and changing consumer preferences.

Quarterly Performance Highlights

Starbucks reported global net revenue of $8.8 billion for Q2 FY25, representing a 3% year-over-year increase. However, this modest top-line growth was overshadowed by concerning metrics in other key performance indicators.

Global comparable store sales declined 1%, with North American comps also down 1% (including a 2% drop in the U.S. market). International comparable sales provided a bright spot with 2% growth, though China reported flat comparable sales at 0%.

The company’s profitability metrics showed significant pressure, with global operating margin contracting 450 basis points year-over-year to 8.2%. This margin compression translated to diluted earnings per share of $0.41, representing a substantial 38% decline from the same period last year.

Detailed Financial Analysis

Starbucks’ revenue composition remains heavily weighted toward North America, which accounts for 74% of total revenue. International markets contribute 21%, while Channel Development (which includes consumer packaged goods and foodservice operations) represents the remaining 5%.

The stark contrast between modest revenue growth (+3%) and significant EPS decline (-38%) indicates substantial cost pressures and operational challenges. The 450 basis point contraction in operating margin suggests multiple factors may be at play, potentially including increased labor costs, inflationary pressures on raw materials, and reduced operational leverage due to lower comparable store traffic.

Despite these challenges, Starbucks continues to expand its global footprint, with store count reaching 40,789 locations worldwide, a 5% increase year-over-year. This ongoing expansion strategy appears to be contributing to revenue growth even as same-store sales face headwinds.

Strategic Initiatives

In response to these challenges, CEO Brian Niccol is spearheading the "Back to Starbucks" plan, which aims to refocus the company on its core strengths and customer experience. The plan outlines four key priorities:

1. Prioritizing customers and "green apron partners" (Starbucks employees)

2. Delivering superior customer experiences during peak business hours

3. Reinforcing Starbucks’ position as a community coffeehouse

4. Reintroducing the Starbucks experience to consumers worldwide

This strategic shift appears to align with information from previous quarters, where the company indicated it was moving away from discount-driven transactions toward broader marketing initiatives. The emphasis on the customer experience and community aspects suggests Starbucks is working to differentiate itself in an increasingly competitive specialty coffee market.

Forward-Looking Statements

CEO Brian Niccol expressed optimism regarding the "Back to Starbucks" plan, though specific financial guidance for upcoming quarters was not detailed in the presentation summary. The company continues to emphasize its mission "to be the premier purveyor of the finest coffee in the world, inspiring and nurturing the human spirit – one person, one cup and one neighborhood at a time."

The significant margin compression and EPS decline in Q2 FY25 present clear challenges for Starbucks’ leadership team. Investors will likely be watching closely to see if the "Back to Starbucks" initiatives can reverse negative comparable sales trends in the U.S. market and restore margin expansion in coming quarters.

With the stock trading near $84, well below its 52-week high of $117.46, market sentiment appears cautious as stakeholders evaluate whether Niccol’s strategic vision can successfully address the operational and financial challenges evident in this quarterly presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.