Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Stellar Bancorp Inc (NYSE:STEL) released its second quarter 2025 earnings presentation on July 25, 2025, highlighting its position as Houston’s largest regionally focused bank. The presentation emphasized the bank’s strong capital position, improving asset quality, and strategic focus on the Houston market. STEL shares closed at $31.53, down 0.44% for the day, following the release.

The Q2 results come after a mixed first quarter where Stellar beat earnings expectations but missed revenue forecasts. The bank continues to navigate a competitive deposit environment while maintaining its focus on relationship-based banking in the Houston region.

Quarterly Performance Highlights

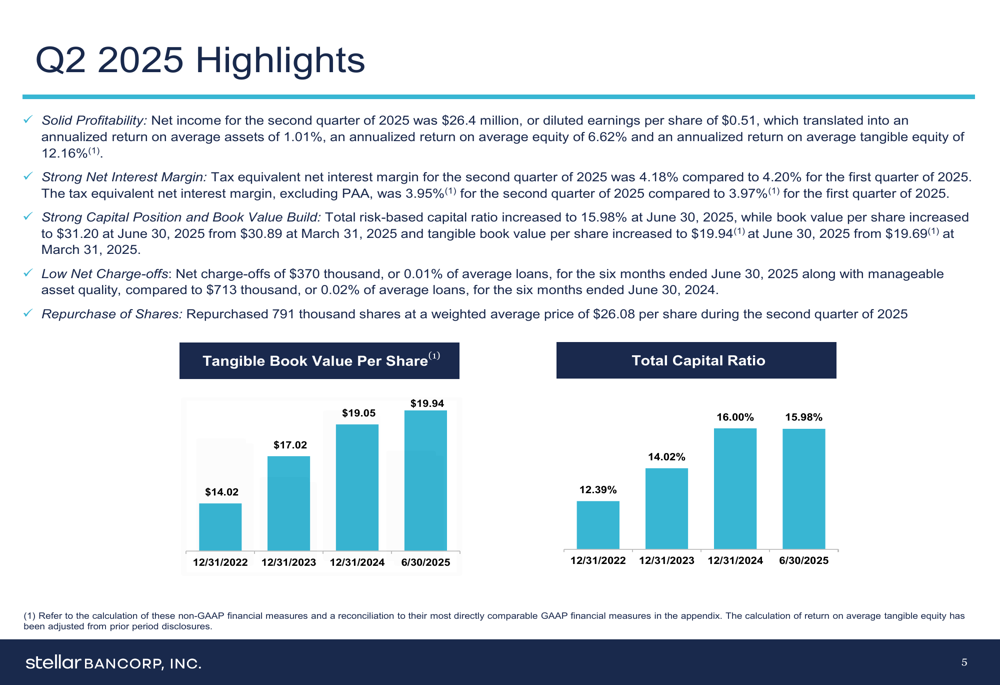

Stellar Bancorp reported solid profitability for Q2 2025, with key metrics showing stability and modest improvement from the previous quarter. The bank’s net interest margin (tax equivalent) stood at 4.18%, with the core margin excluding purchase accounting adjustments at 3.95%.

Book value per share increased to $31.20 as of June 30, 2025, up from $30.89 at the end of the previous quarter. Similarly, tangible book value per share rose to $19.94 from $19.69, continuing a positive trend that has seen this metric grow from $14.02 at the end of 2022.

As shown in the following chart of tangible book value growth and capital ratio improvement:

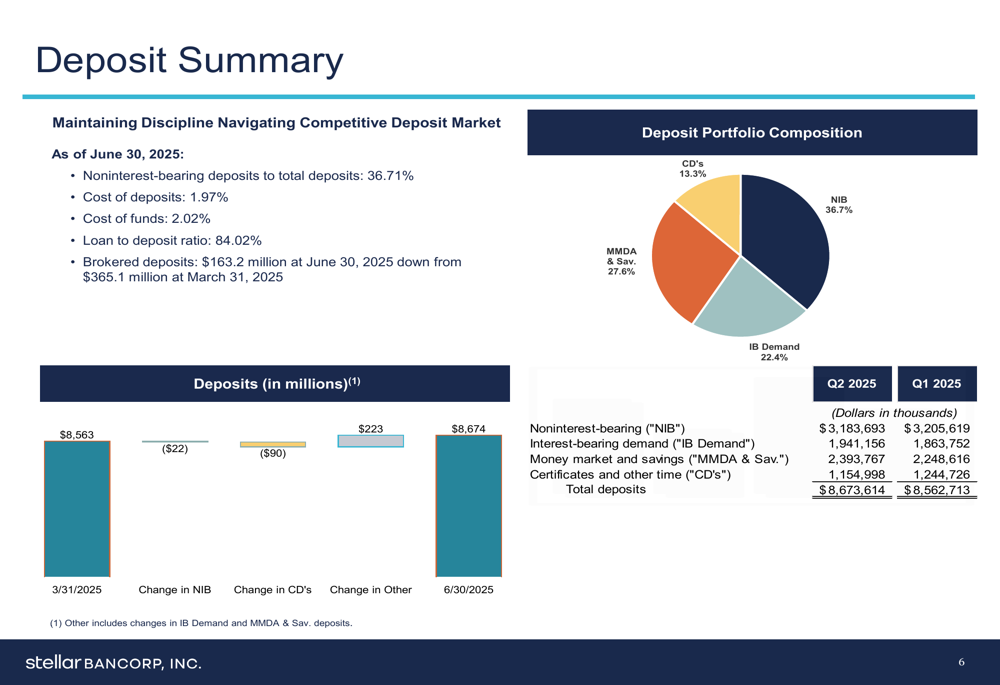

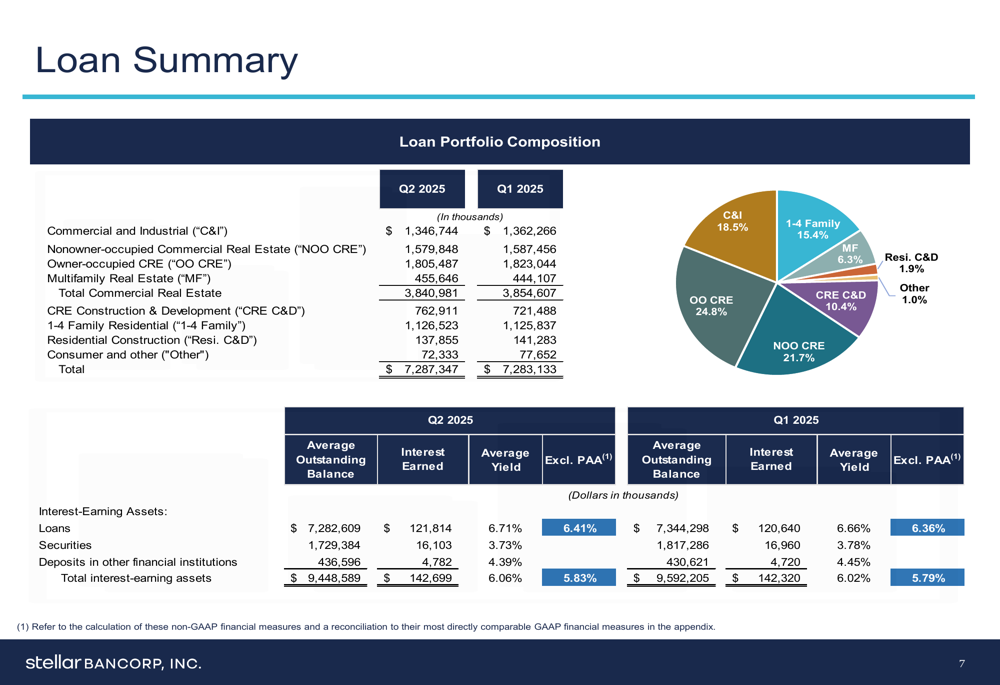

Total (EPA:TTEF) assets reached $10.49 billion, with total loans of $7.29 billion and total deposits of $8.67 billion. The loan-to-deposit ratio stood at 84.02%, reflecting a balanced approach to lending relative to the deposit base.

Deposit and Loan Portfolio Analysis

Stellar maintained a strong deposit franchise with noninterest-bearing deposits comprising 36.71% of total deposits as of June 30, 2025. This represents a slight decrease from the previous quarter but remains a competitive advantage in the current rate environment. The cost of deposits was 1.97%, while the overall cost of funds was 2.02%.

The deposit composition is illustrated in the following breakdown:

On the lending side, the loan portfolio remained relatively stable at $7.29 billion, showing minimal change from the $7.28 billion reported in Q1 2025. Commercial real estate (including multifamily) represents the largest segment of the portfolio, followed by commercial and industrial loans.

The detailed loan portfolio composition is shown here:

The bank’s loan portfolio features a balanced rate structure with 51.31% fixed-rate loans, 26.28% variable-rate loans, and 22.41% floating-rate loans. This diversification helps manage interest rate risk while providing some benefit from the current rate environment.

Asset Quality and Capital Position

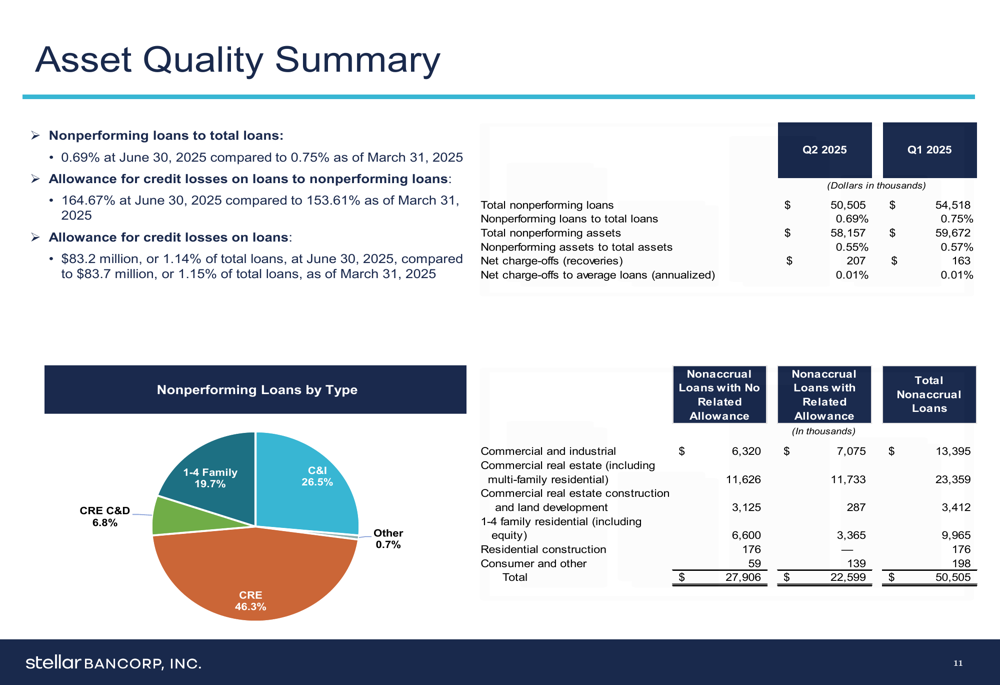

Asset quality metrics showed improvement in Q2 2025, with nonperforming loans decreasing to $50.5 million from $54.5 million in the previous quarter. The distribution of nonperforming loans shows commercial real estate representing the largest portion at 46.3%, followed by commercial and industrial loans at 26.5%.

The following chart illustrates the nonperforming loan composition:

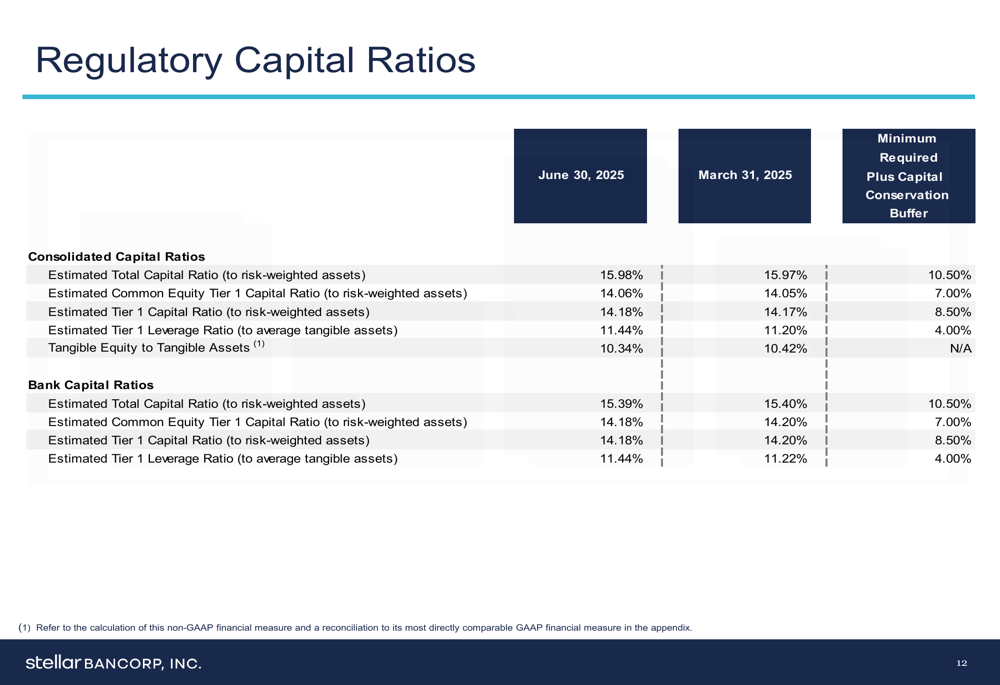

Stellar’s capital position continued to strengthen, with the total capital ratio increasing to 15.98% as of June 30, 2025, well above regulatory requirements. This represents a significant improvement from 12.39% at the end of 2022, demonstrating the bank’s focus on building capital strength.

The regulatory capital ratios are detailed below:

Houston Market Strength

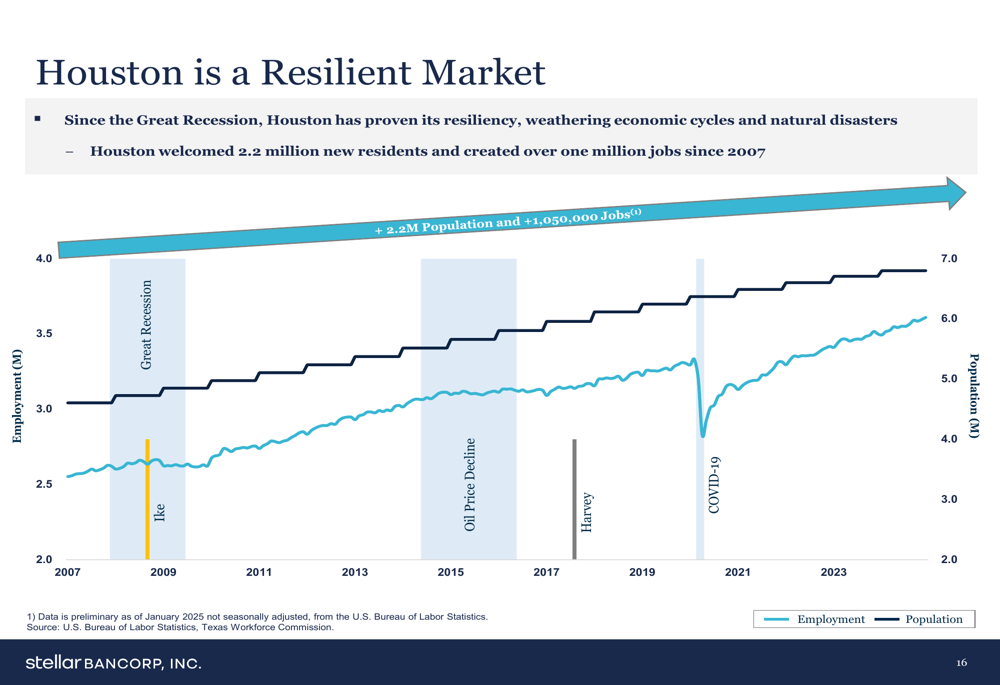

A significant portion of the presentation highlighted Stellar’s strategic focus on the Houston market, which the bank describes as diverse and economically resilient. Houston ranked first in GDP growth among the 20 most populous U.S. metro areas and has the third lowest cost of living among major metropolitan areas.

The bank emphasized Houston’s population growth and economic diversification as key factors supporting its market strategy. While energy remains important to the local economy, Houston has diversified significantly across healthcare, manufacturing, transportation, and professional services.

As shown in the following chart of Houston’s employment and population growth:

The bank also highlighted Houston’s housing affordability advantage, with median home prices to household income ratios significantly lower than other major markets like Los Angeles, New York, and San Francisco. This affordability factor, combined with Houston’s position as the leader in U.S. annual new home construction, supports the bank’s optimism about continued growth in its core market.

Forward-Looking Statements

Looking ahead, Stellar Bancorp emphasized several key factors for future success, including credit performance and risk management. The bank highlighted its strong earnings power, excellent core funding profile, and significant financial flexibility as foundations for continued growth.

These forward-looking statements align with comments from the Q1 earnings call, where management expressed optimism about loan growth in the latter half of 2025, targeting low to mid-single-digit increases. The Q2 presentation reinforces this outlook, emphasizing the bank’s positioning for continued strong internal capital generation.

The bank’s focus on the Houston market appears well-founded given the region’s economic resilience and growth prospects. However, as noted in the Q1 earnings discussion, economic uncertainties including potential impacts from tariff policies remain challenges to navigate in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.