Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

Stepan Company (NYSE:SCL) presented its second quarter 2025 earnings results on July 30, 2025, showcasing a 27% year-over-year increase in adjusted net income despite challenges in free cash flow. The specialty chemicals manufacturer, which had reported strong first quarter results earlier this year, continued to demonstrate earnings growth in Q2, though at a more moderate pace compared to Q1’s 32% adjusted net income growth.

The company’s stock, which had surged 9.3% following its Q1 results, has since faced pressure, closing at $55.24 on July 29, 2025, down 1.66% ahead of the earnings presentation. Stepan’s shares have traded between $44.23 and $87.45 over the past 52 weeks, indicating significant volatility.

Quarterly Performance Highlights

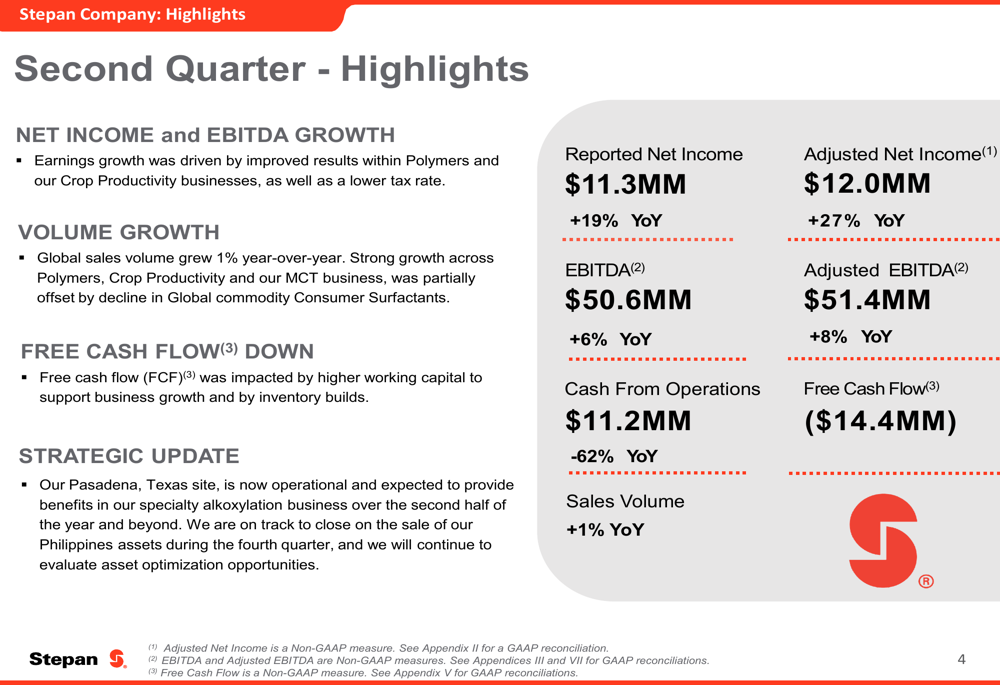

Stepan reported Q2 2025 net income of $11.3 million, a 19% increase from the same period last year, while adjusted net income rose 27% to $12.0 million. The company’s EBITDA grew 6% to $50.6 million, with adjusted EBITDA increasing 8% to $51.4 million. These improvements were primarily driven by stronger performance in the Polymers segment and the company’s Crop Productivity businesses, as well as a lower effective tax rate.

As shown in the following quarterly highlights slide, global sales volume grew modestly at 1% year-over-year, while free cash flow turned negative at ($14.4 million), impacted by higher working capital requirements to support business growth and inventory builds:

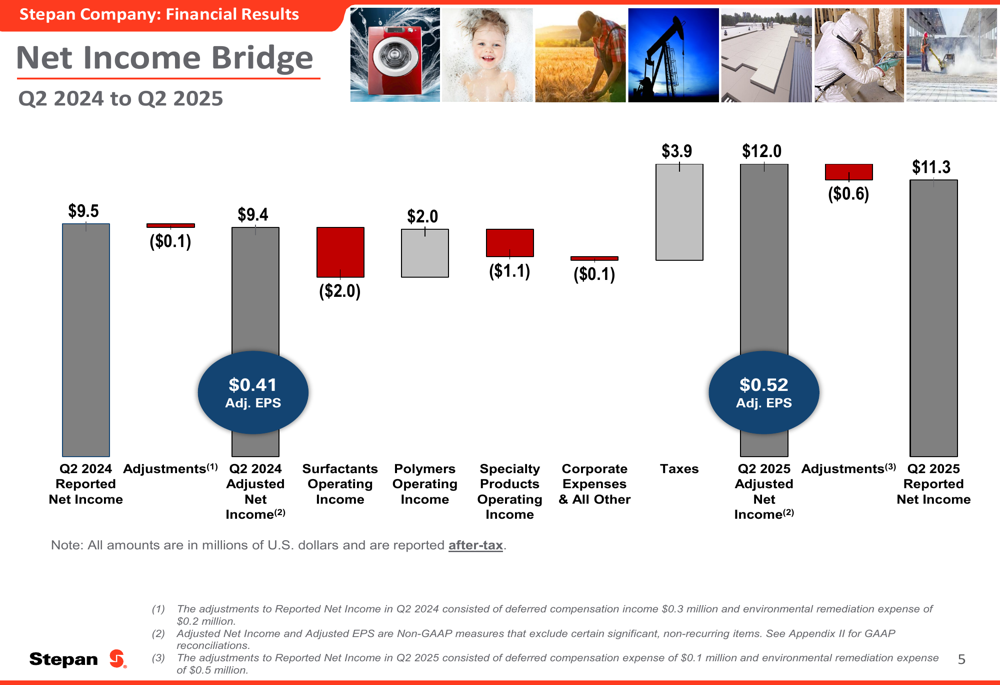

The company’s earnings growth trajectory can be better understood through the Net Income Bridge, which illustrates the key factors contributing to the year-over-year improvement:

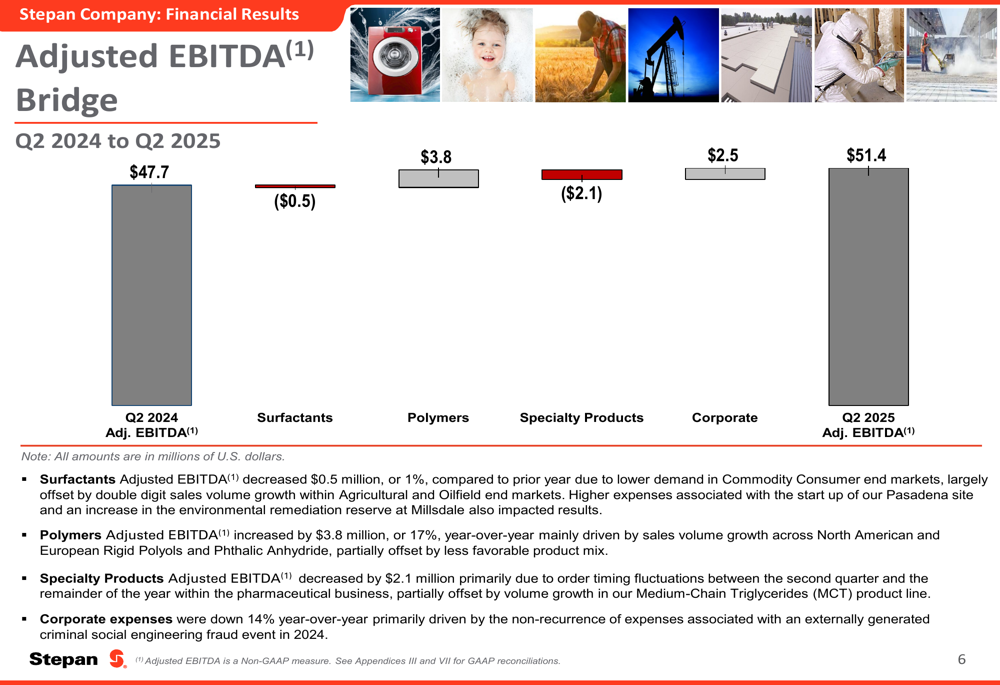

The adjusted EBITDA bridge further demonstrates how segment performance affected overall results, with Polymers contributing $3.8 million in additional EBITDA while Surfactants remained relatively flat and Specialty Products declined:

Segment Analysis

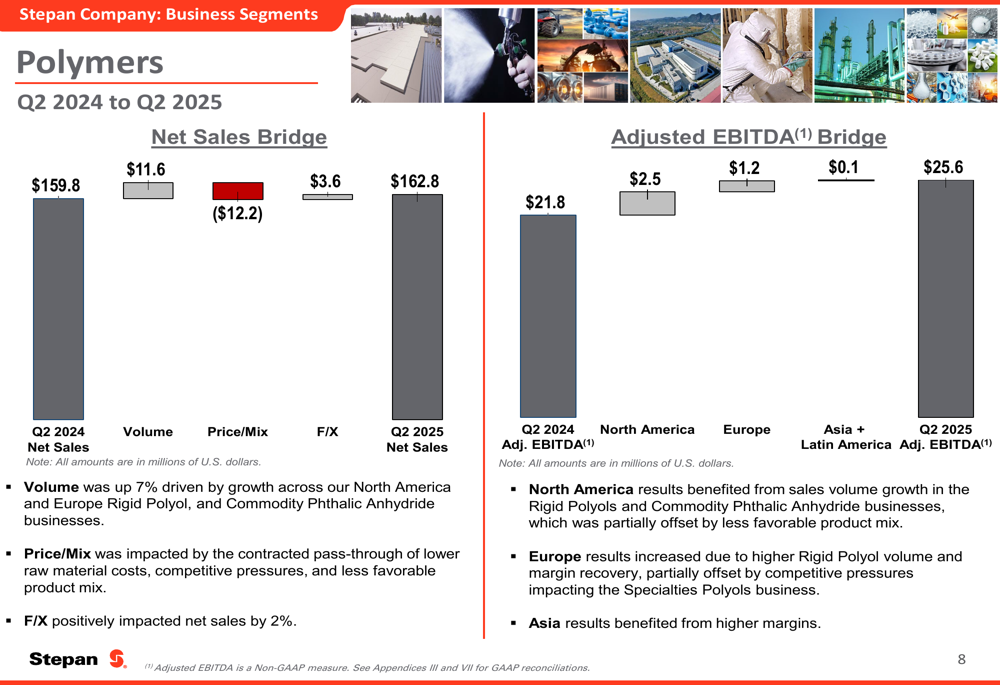

Stepan’s business segments showed divergent performance in Q2 2025. The Polymers segment emerged as the standout performer, with adjusted EBITDA increasing by $3.8 million or 17.4% year-over-year to $25.6 million. This growth was primarily driven by sales volume increases across North American and European Rigid Polyols and Phthalic Anhydride products.

The Polymers segment’s performance is illustrated in the following bridge chart, showing volume growth of $11.6 million partially offset by price/mix declines of $12.2 million:

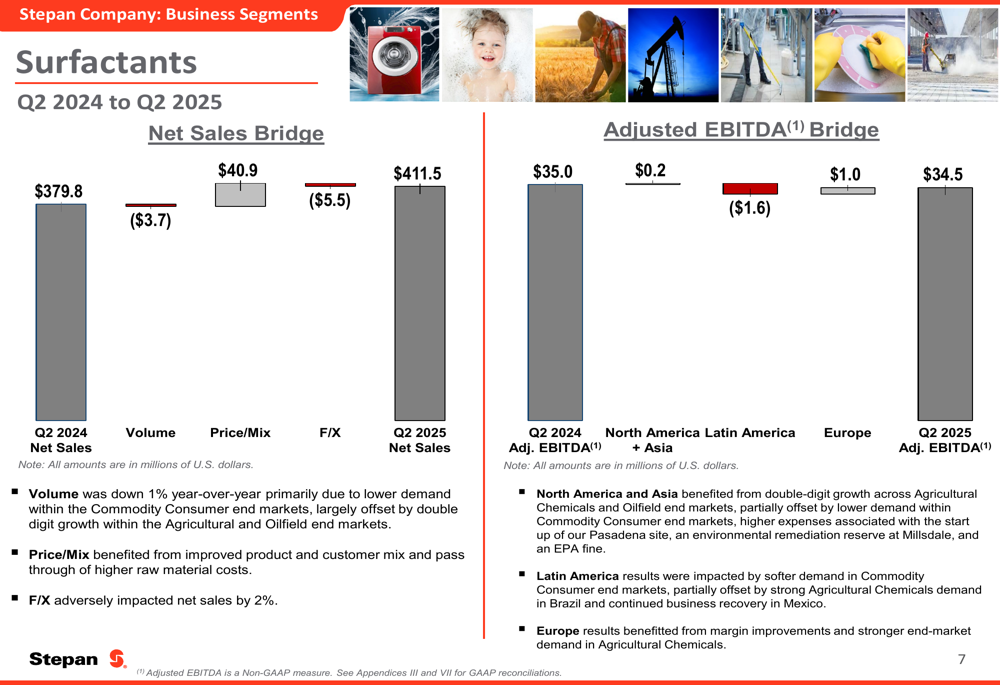

In contrast, the Surfactants segment, which represents the largest portion of Stepan’s business, experienced a slight decline in adjusted EBITDA, decreasing by $0.5 million to $34.5 million. This decrease was attributed to lower demand in Commodity Consumer end markets, though partially offset by double-digit sales volume growth in Agricultural and Oilfield end markets.

The Surfactants segment’s performance is detailed in the following bridge chart:

The Specialty Products segment saw the largest relative decline, with adjusted EBITDA decreasing by $2.1 million, primarily due to order timing fluctuations within the pharmaceutical business.

Balance Sheet and Cash Flow

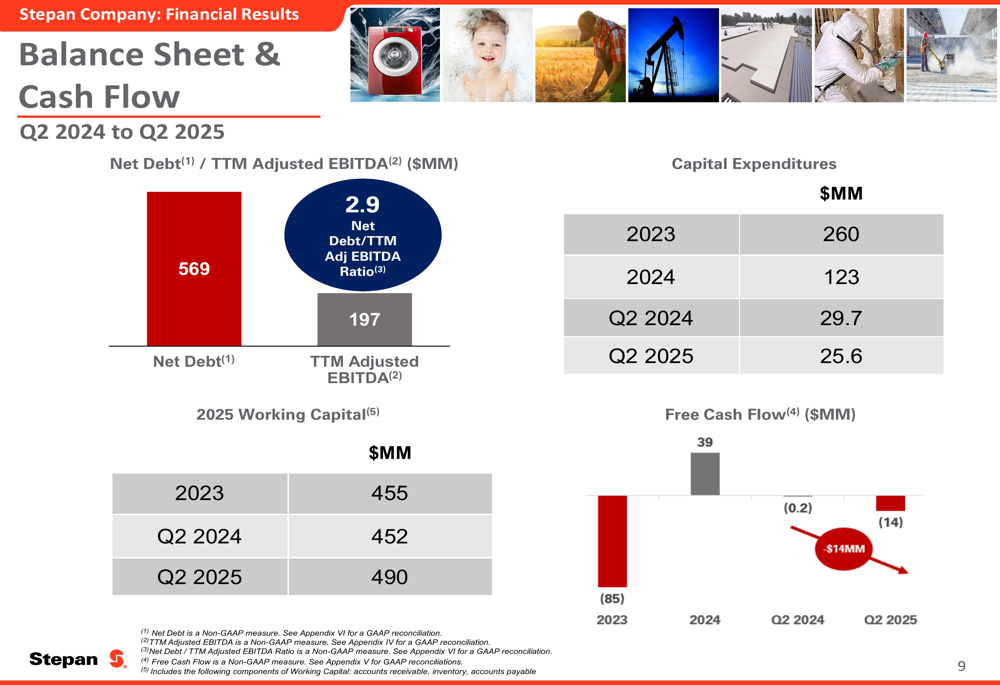

Stepan’s balance sheet metrics and cash flow showed some concerning trends in Q2 2025. The company’s Net Debt to TTM Adjusted EBITDA ratio stood at 2.9x, while working capital increased to $490 million from $452 million in Q2 2024. Free cash flow turned negative at ($14.4 million) compared to positive $14 million in the same period last year.

The following slide illustrates these key financial metrics:

Capital expenditures for Q2 2025 were $25.6 million, down from $29.7 million in Q2 2024. For the full year 2025, Stepan forecasts capital expenditures of $120-125 million, in line with 2024’s $123 million but significantly lower than the $260 million spent in 2023.

Strategic Initiatives

Stepan highlighted its strategic priorities focused on high-margin growth markets, customer-centric innovation, key strategic investments, and operational excellence. The company’s strategic roadmap is illustrated in the following slide:

A significant milestone in Stepan’s strategic initiatives is the operational status of its new alkoxylation capacity in Pasadena, Texas. This facility, Stepan’s third alkoxylation site, is expected to provide benefits in the specialty alkoxylation business over the second half of 2025 and beyond. The site supports growth in ethoxylates and propoxates, which are core surfactant technologies used across Stepan’s key agricultural, oilfield, construction, and household end markets.

The Pasadena investment is showcased in the following slide:

Forward-Looking Statements

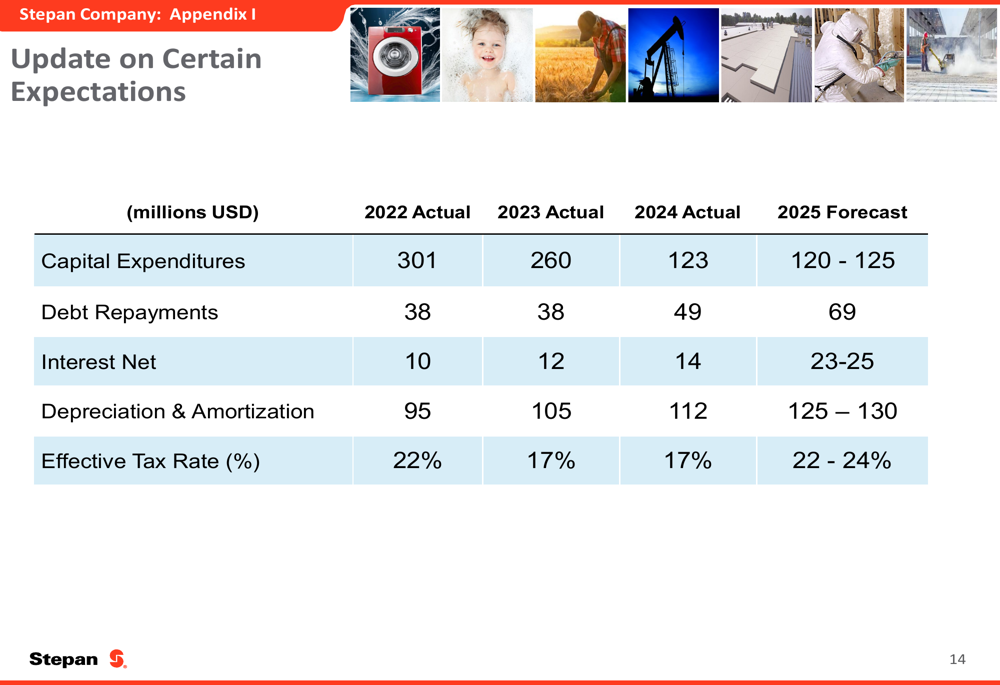

Looking ahead, Stepan provided updates on certain financial expectations for 2025. The company forecasts capital expenditures of $120-125 million, debt repayments of $69 million, and an effective tax rate of 22-24%, up from 17% in 2023 and 2024. Depreciation and amortization are expected to increase to $125-130 million from $112 million in 2024.

These forward-looking expectations are detailed in the following table:

During the Q1 2025 earnings call, CEO Luis Rojo had expressed cautious optimism about delivering full-year growth despite market uncertainties, including potential tariff impacts. The Q2 results suggest that while earnings growth remains solid, challenges in cash flow generation and working capital management require attention.

The company’s ability to successfully leverage its new Pasadena facility while addressing free cash flow concerns will likely be key factors in its performance for the remainder of 2025. Investors will be watching closely to see if Stepan can maintain its earnings momentum while improving its cash flow metrics in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.