Bitcoin price today: dips to $92k as Fed cut doubts spark risk-off mood

Introduction & Market Context

Sterling Infrastructure, Inc. (NASDAQ:STRL) reported strong first-quarter 2025 results on May 6, showcasing significant profitability improvements despite modest revenue changes. The infrastructure services provider continued its multi-year transformation toward higher-margin business segments, with operating income increasing 33.3% year-over-year to $56.1 million.

The company’s stock, which closed at $165.64 on May 5, jumped 4.82% in after-hours trading following the earnings release, reaching $174.70. This positive reaction reflects investor confidence in Sterling’s strategic direction and improved profitability metrics.

Quarterly Performance Highlights

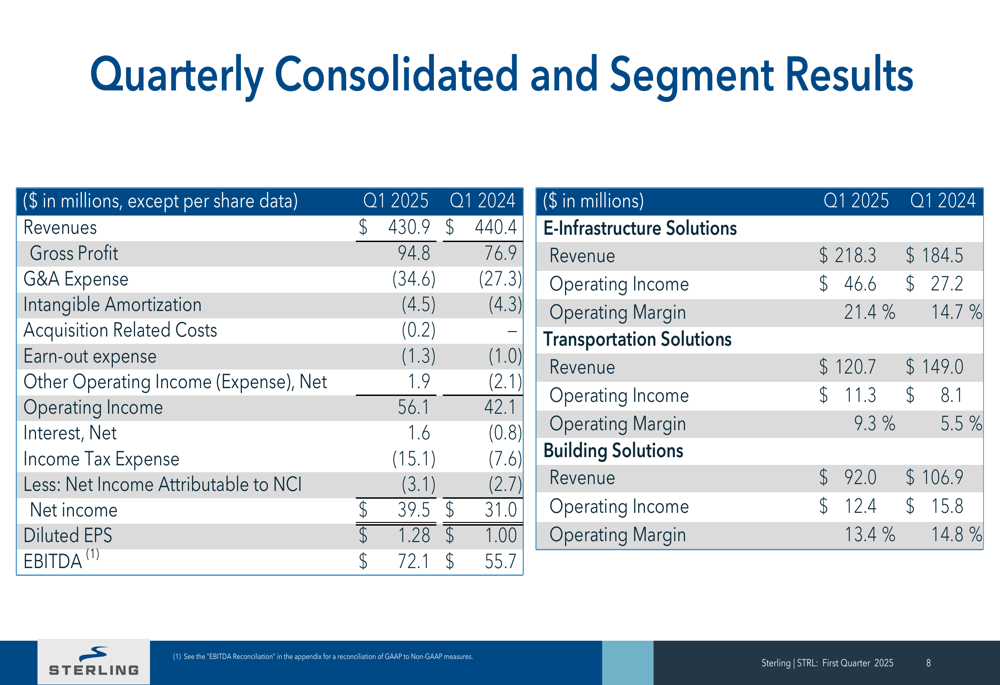

Sterling reported Q1 2025 revenues of $430.9 million, representing a 7.2% increase from the comparable prior-year period when adjusted for the deconsolidation of RHB. While total revenue declined slightly from $440.4 million in Q1 2024 on an unadjusted basis, the company delivered substantial improvements in profitability metrics.

Gross profit increased 32.4% year-over-year to $94.8 million, while operating income rose 33.3% to $56.1 million. Net income attributable to Sterling common stockholders reached $39.5 million, translating to diluted earnings per share of $1.28, compared to $1.00 in the prior-year period.

As shown in the following quarterly results comparison:

The company’s adjusted metrics also showed strong performance, with adjusted net income of $50.2 million and adjusted diluted EPS of $1.63. Adjusted EBITDA reached $80.3 million, while cash flow from operations was robust at $84.9 million.

Segment Performance

Sterling’s strategic shift toward higher-margin business continues to bear fruit, with the E-Infrastructure Solutions segment now representing 51% of total revenue, up from 46% in Q1 2024. This segment, which focuses on data centers and other technology infrastructure, delivered the strongest performance with revenue increasing 18.3% to $218.3 million and operating income surging 61.4% to $50.6 million.

The segment’s operating margin expanded significantly to 23.2%, up from 17.0% in the prior-year period, demonstrating Sterling’s ability to capitalize on strong demand in the data center and technology infrastructure markets.

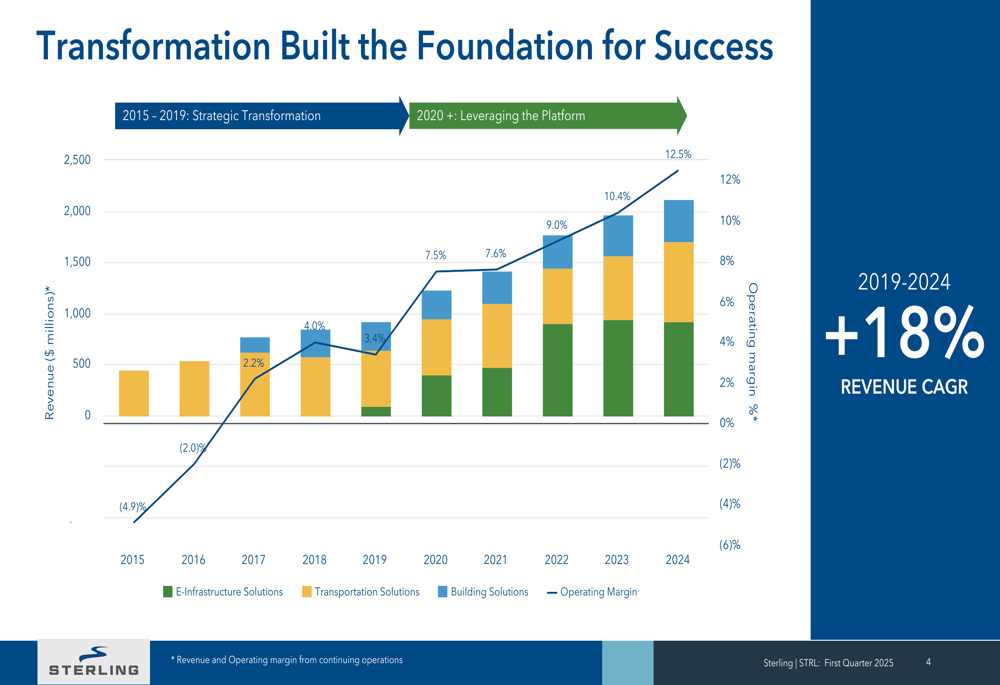

The following chart illustrates the company’s long-term revenue growth and margin expansion, highlighting the successful strategic transformation that began in 2019:

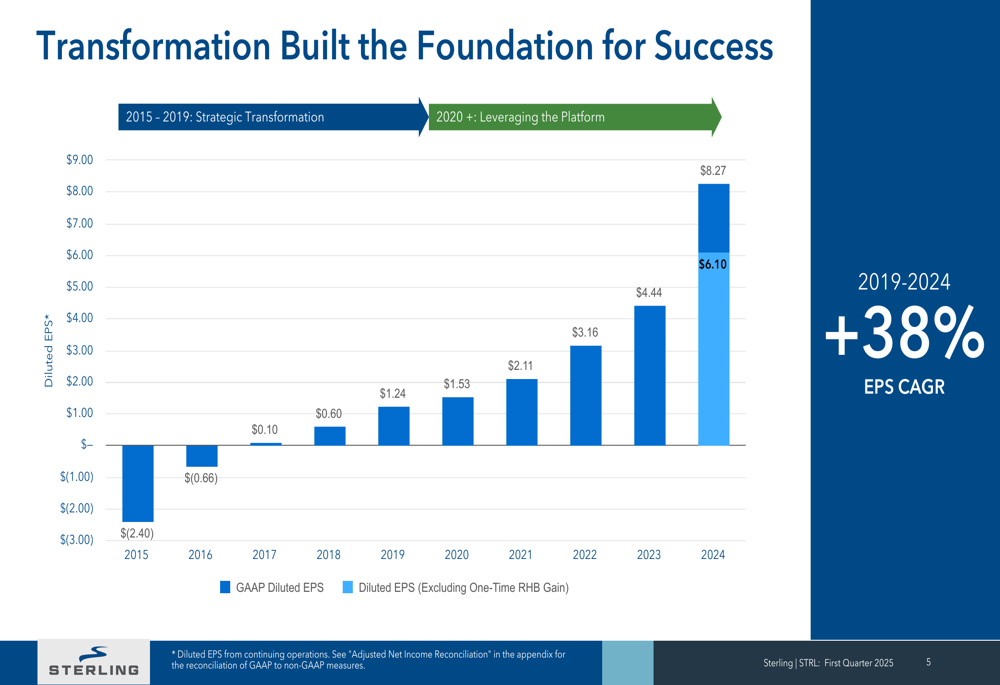

This transformation has driven substantial improvement in earnings per share over the same period:

The Transportation Solutions segment also showed strong margin improvement, with operating margin increasing to 11.3% from 7.7% in Q1 2024. The Building Solutions segment, while experiencing a revenue decline, maintained a healthy 15.5% operating margin.

Financial Position & Backlog

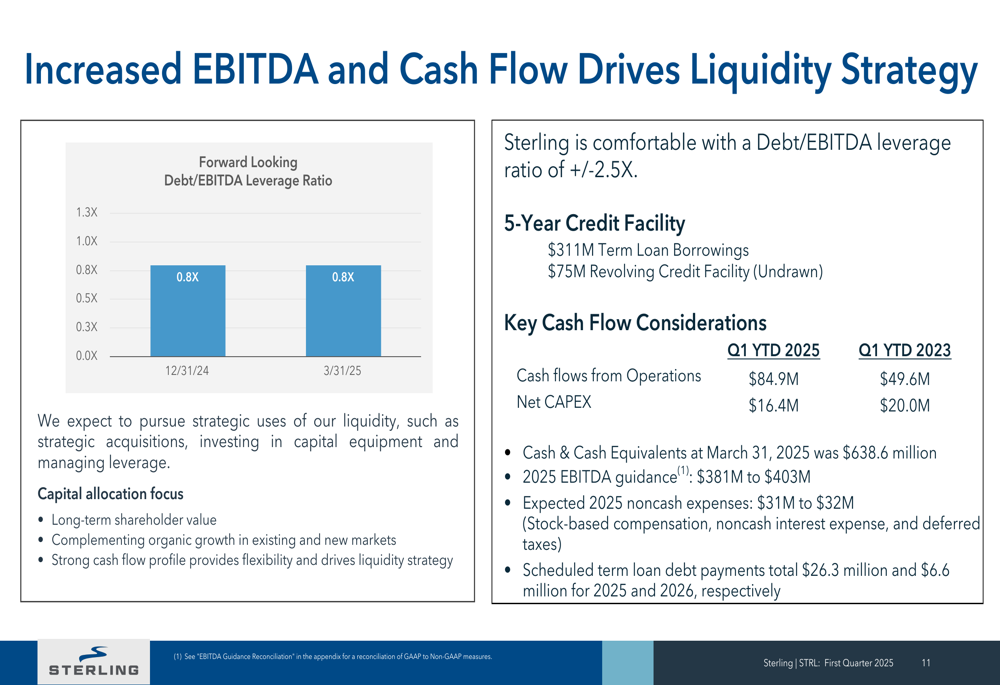

Sterling continues to strengthen its financial position, ending the quarter with $638.6 million in cash and cash equivalents. The company maintains a conservative leverage profile with a Debt/EBITDA ratio of 0.8x as of March 31, 2025.

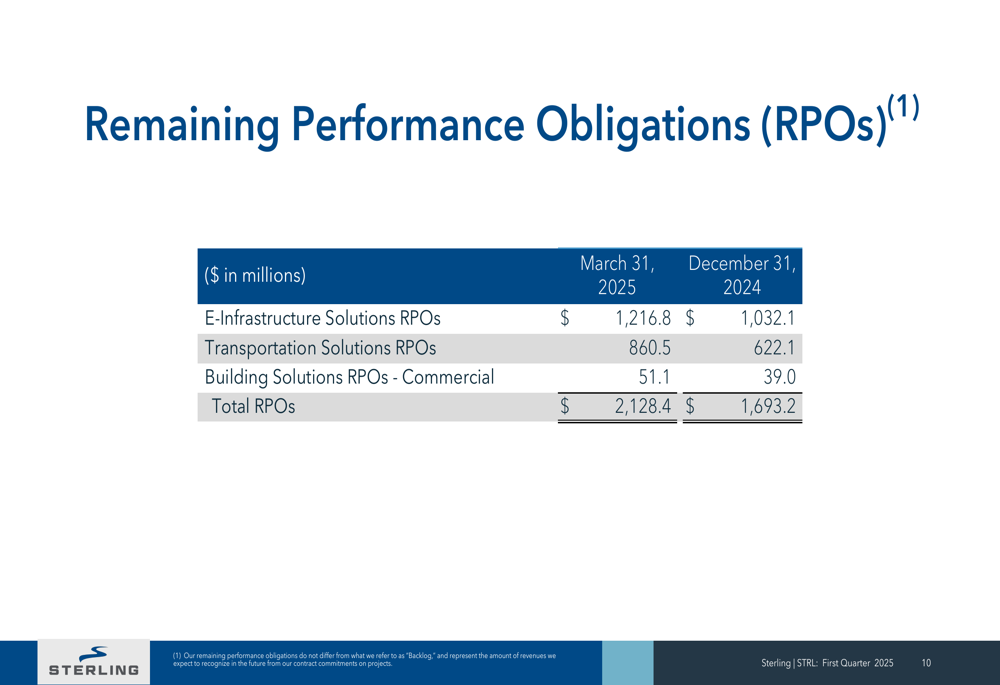

The company’s backlog grew significantly to $2.13 billion as of March 31, 2025, compared to $1.69 billion at the end of 2024, representing a 25.7% increase in just one quarter. This growth was driven primarily by the E-Infrastructure and Transportation segments, as illustrated in the following breakdown:

The strong backlog provides solid visibility for the remainder of 2025 and supports management’s full-year guidance. Sterling’s liquidity strategy emphasizes increased EBITDA and cash flow generation while maintaining a comfortable debt level:

2025 Outlook & Guidance

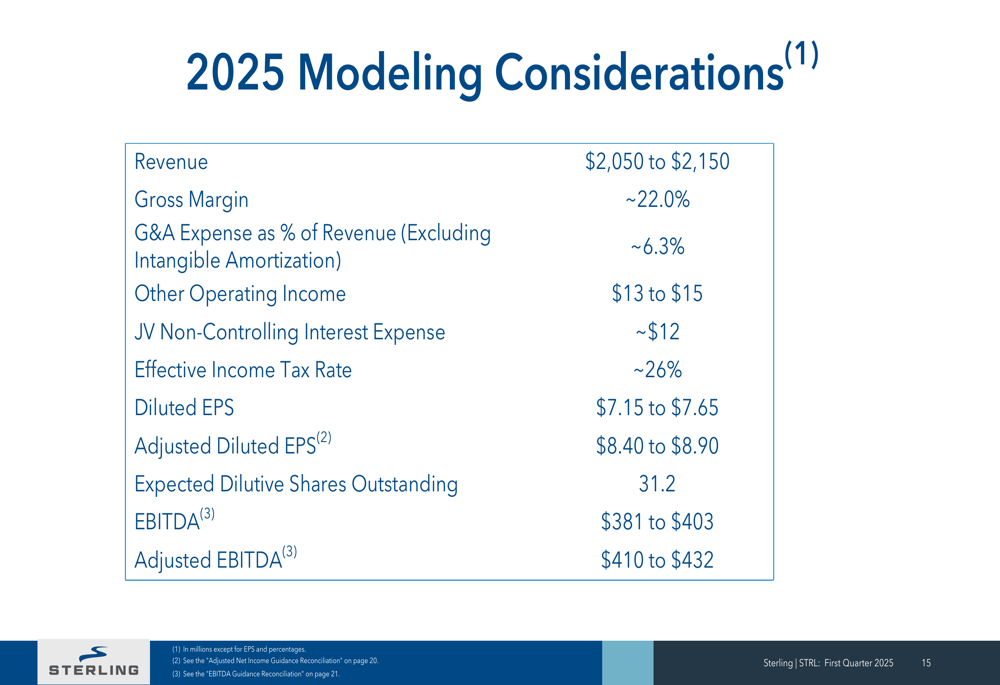

Based on its strong Q1 performance and growing backlog, Sterling has provided full-year 2025 guidance that projects continued growth. The company expects:

- Revenue between $2,050 million and $2,150 million

- Diluted EPS of $7.15 to $7.65

- Adjusted Diluted EPS of $8.40 to $8.90

- EBITDA of $381 million to $403 million

- Adjusted EBITDA of $410 million to $432 million

The detailed modeling considerations for 2025 are presented below:

This guidance represents significant growth from 2024 results, with adjusted diluted EPS expected to increase by approximately 26-31% at the midpoint compared to 2024 actual results of $6.10.

Management remains confident in Sterling’s ability to capitalize on strong secular growth trends in infrastructure, particularly in the E-Infrastructure segment which continues to benefit from investments in data centers and technology infrastructure. The company’s strategic positioning, strong backlog, and healthy balance sheet provide a solid foundation for continued growth throughout 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.